Introduction

Investing in a 401k is a smart way to plan for retirement and secure your financial future. However, it’s crucial to understand the rate of return on your 401k investments and what constitutes a good return. Your rate of return is a measure of how much your investments have grown over a specific period of time.

Many individuals wonder what is considered a good rate of return on their 401k investments. While there is no definitive answer, a good rate of return is generally considered to be around 7-8% annually. This takes into account both the average rate of return in the market and the inflation rate.

However, it’s important to note that the rate of return can vary based on several factors, including your investment strategy, risk tolerance, and market conditions. It’s essential to understand these factors and evaluate your investment options to achieve the best possible return.

In this article, we will explore what constitutes a good rate of return on 401k investments, the factors that influence it, investment strategies for higher returns, the risks and rewards associated with higher returns, common mistakes to avoid, and how to track and evaluate your rate of return. By understanding these concepts, you will be better equipped to make informed decisions regarding your 401k investments and maximize your returns.

Investing in a 401k is a long-term commitment, and aiming for a good rate of return is crucial in order to continue building your retirement savings. So, let’s dive into the world of 401k investments and discover the secrets to achieving a good rate of return.

Understanding 401k Investments

A 401k is a retirement savings plan offered by employers to their employees. It allows individuals to contribute a portion of their salary on a pre-tax basis, meaning that the contributions are deducted from their paycheck before taxes are applied. These contributions are then invested in a variety of funds, such as stocks, bonds, and mutual funds, with the goal of growing the account over time.

One of the main advantages of a 401k is the potential for tax-deferred growth. This means that any investment gains within the account are not subject to taxes until the funds are withdrawn during retirement. This can provide significant tax advantages and allow your investments to compound over the years.

Another important aspect of 401k investments is employer matching contributions. Many employers offer a matching program where they contribute a percentage of the employee’s salary to their 401k account. For example, if your employer has a 50% match up to 6% of your salary, it means that they will contribute 50 cents for every dollar you contribute, up to a maximum of 6% of your salary. This is essentially free money and can significantly boost your retirement savings.

It’s important to note that 401k plans have contribution limits set by the Internal Revenue Service (IRS). As of 2021, the maximum contribution limit is $19,500 for individuals under 50 years old. Individuals who are 50 or older can make an additional catch-up contribution of up to $6,500, for a total maximum contribution of $26,000. These limits are subject to change, so it’s essential to stay updated with the latest guidelines.

Understanding the basics of 401k investments is crucial to making informed decisions about your retirement savings. By taking advantage of tax benefits, employer matches, and maximizing your contributions within the allowed limits, you can set yourself up for a comfortable retirement. In the next section, we will delve into what constitutes a good rate of return on your 401k investments and the factors that influence it.

What Is a Good Rate of Return?

When it comes to a good rate of return on your 401k investments, there is no one-size-fits-all answer. What may be considered good for one individual may not be the same for another. However, as a general guideline, a good rate of return on your 401k investments is typically around 7-8% annually.

This range takes into account the average rate of return in the market, which historically has been around 7%, and factors in the average inflation rate of approximately 2-3%. By achieving a return of 7-8%, you are effectively staying ahead of inflation and growing your investments in real terms.

It’s important to note that the rate of return can vary significantly depending on a variety of factors. These factors include your investment strategy, risk tolerance, and market conditions. While it’s natural to desire higher returns, it’s essential to balance the potential for growth with the level of risk you are willing to accept.

Another factor to consider is the time horizon for your investments. If you are still early in your career and have several decades until retirement, you may be able to take on more aggressive investment strategies that have the potential for higher returns. On the other hand, if you are closer to retirement, capital preservation and more conservative investments may be a priority.

Additionally, it’s important to keep in mind that the stock market can be volatile, and past performance is not indicative of future results. While investments in stocks have historically provided higher returns over the long term, they also come with a higher level of risk. Diversifying your portfolio and considering a mix of stocks, bonds, and other asset classes can help mitigate risk while still aiming for a good rate of return.

Ultimately, what constitutes a good rate of return on your 401k investments will depend on your personal financial goals, risk tolerance, and time horizon. It’s crucial to have a well-thought-out investment strategy in place and regularly evaluate and adjust your portfolio as needed. In the next section, we will explore the factors that can affect your rate of return on 401k investments and how you can optimize it.

Factors Affecting Rate of Return

Several factors can influence the rate of return on your 401k investments. Understanding these factors is crucial to optimize your returns and make informed investment decisions. Here are some key factors to consider:

Asset Allocation: The allocation of your investments across different asset classes, such as stocks, bonds, and cash, can have a significant impact on your rate of return. A well-diversified portfolio that matches your risk tolerance and investment goals can help balance potential returns and risks.

Investment Strategy: The specific investments you choose within each asset class will play a role in your rate of return. Some investments may provide higher returns but come with greater risk, while others may offer more stable returns but with lower growth potential. Your investment strategy should align with your financial objectives.

Market Conditions: The overall state of the financial markets can impact your returns. Economic factors, such as interest rates, inflation, and geopolitical events, can affect the performance of different asset classes. It’s important to stay informed about market trends and adjust your portfolio accordingly.

Timing of Contributions and Withdrawals: The timing of your contributions and withdrawals can impact your rate of return. Regularly contributing to your 401k, especially during periods of market downturns, can help you take advantage of lower prices and potentially higher returns when the market recovers. Similarly, timing your withdrawals strategically during retirement can help stretch your savings.

Company Performance: If your 401k investments include company stocks or funds that invest in specific companies, the performance of those companies can impact your returns. Monitoring the financial health and growth prospects of the companies in which you are invested can help you make informed decisions.

Fee and Expense Structure: The fees and expenses associated with your 401k investments can impact your rate of return. High fees can eat into your returns over time, so it’s important to evaluate the expense ratio and transaction costs of the funds in your portfolio and consider lower-cost investment options.

By understanding these factors, you can make strategic decisions to optimize your rate of return on your 401k investments. It’s important to regularly review and adjust your portfolio to ensure it aligns with your financial goals and market conditions. In the next section, we will explore investment strategies that can potentially help you achieve higher returns on your 401k investments.

Investment Strategies for Higher Returns

When it comes to maximizing returns on your 401k investments, implementing effective investment strategies is crucial. Here are some strategies to consider:

1. Diversification: Diversifying your portfolio is an essential strategy to mitigate risk while potentially increasing returns. Allocate your investments across different asset classes, such as stocks, bonds, and cash, as well as various sectors and geographic regions. This can help you capture growth opportunities while reducing the impact of any specific investment’s poor performance.

2. Asset Allocation Rebalancing: Regularly review and rebalance your portfolio to maintain your desired asset allocation. This involves selling investments that have increased in value and buying more of those that have underperformed. Rebalancing ensures that your portfolio remains aligned with your risk tolerance and long-term goals.

3. Dollar-Cost Averaging: Implement a dollar-cost averaging strategy by investing a fixed-dollar amount at regular intervals, regardless of the market’s ups and downs. This helps smooth out the impact of market volatility, allowing you to buy more shares when prices are low and fewer shares when prices are high. Over time, this strategy may result in a lower average purchase price and potentially higher returns.

4. Take Advantage of Employer Matching: If your employer offers a matching program, contribute enough to your 401k to maximize the employer match. This is essentially free money that can dramatically boost your retirement savings. Take full advantage of this benefit, as it can significantly increase your overall rate of return.

5. Consider Growth-Oriented Investments: Depending on your risk tolerance and investment horizon, consider allocating a portion of your portfolio to growth-oriented investments such as stocks or equity funds. These investments have the potential to generate higher returns over the long term but come with higher volatility and risk.

6. Regularly Review Expense Ratios: Monitor the expense ratios of the funds in your portfolio. High expenses can eat into your returns over time. Look for low-cost index funds or exchange-traded funds (ETFs), which often have lower expense ratios compared to actively managed funds.

7. Stay Informed: Stay updated on market trends, economic indicators, and investment news. This knowledge allows you to make informed decisions about potential investment opportunities or adjustments to your portfolio.

Remember, there is no one-size-fits-all strategy for maximizing returns. Your investment strategy should align with your risk tolerance, time horizon, and retirement goals. It’s essential to regularly review and adjust your portfolio as needed to stay on track. In the next section, we will explore the risks and rewards associated with aiming for higher returns on your 401k investments.

Risks and Rewards of Higher Returns

Aiming for higher returns on your 401k investments can potentially yield greater rewards, but it’s important to understand the associated risks. Here are the risks and rewards to consider:

Risks:

1. Market Volatility: Investments with higher growth potential often come with increased volatility. Market fluctuations can lead to significant swings in the value of your investments, which can be unsettling for some investors.

2. Loss of Principal: Investments with higher potential returns also carry a higher risk of losing your principal. It’s important to carefully assess your risk tolerance and invest accordingly to avoid significant losses.

3. Concentration Risk: Concentrating your investments in a specific sector, industry, or company can expose you to higher risks. Diversification is crucial to minimize the impact of any particular investment’s poor performance.

4. Inflation Risk: While higher returns can help you stay ahead of inflation, there is always the risk that inflation may outpace your investment growth. It’s important to consider investments that have the potential to outpace inflation over the long term.

Rewards:

1. Increased Retirement Savings: Higher returns allow your investments to grow at a faster rate, potentially resulting in a larger nest egg for your retirement years.

2. Comfortable Retirement: Achieving higher returns can provide you with the financial security and flexibility to enjoy a comfortable retirement, pursue your passions, and meet your desired lifestyle goals.

3. Accelerated Wealth Building: Higher returns can help you accumulate wealth faster, allowing you to achieve financial milestones and reach your financial goals earlier.

4. Income Replacement: By aiming for higher returns, you may be able to generate a larger income stream from your investments during retirement, providing additional financial security.

It’s important to strike a balance between the risks and rewards when pursuing higher returns. Assess your risk tolerance, financial goals, time horizon, and investment knowledge to determine the appropriate level of risk for your portfolio. Consider diversifying your investments and regularly review and adjust your portfolio to maintain a suitable risk level.

Remember, past performance is not indicative of future results, and investing involves inherent risks. Work with a financial advisor or utilize reputable investment resources to make informed decisions and manage the risks associated with aiming for higher returns. In the next section, we will discuss common mistakes to avoid when it comes to your 401k investments.

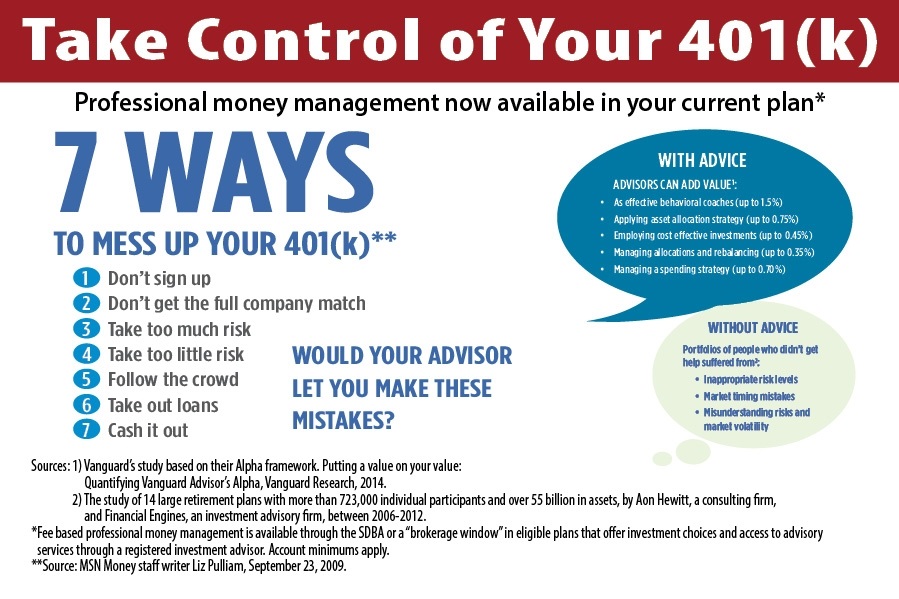

Common Mistakes to Avoid

When it comes to managing your 401k investments, avoiding common mistakes can help you maximize your returns and build a solid retirement fund. Here are some key mistakes to steer clear of:

1. Failing to Contribute Enough: One of the biggest mistakes is not contributing enough to your 401k. Take advantage of employer matching programs and strive to contribute at least the maximum amount allowed by the IRS. By not maximizing your contributions, you may be leaving valuable employer contributions on the table and missing out on potential tax advantages.

2. Neglecting to Diversify: Failing to diversify your portfolio is a grave mistake. Concentrating your investments in a single asset class or company leaves you highly exposed to the risks associated with that investment. Diversify across different asset types, sectors, and geographical regions to spread risk and potentially enhance returns.

3. Market Timing: Trying to time the market by buying and selling investments based on short-term market movements is a risky strategy. Research has shown that consistently timing the market is extremely difficult, if not impossible. Instead, focus on a long-term investment plan and stick to it, regardless of short-term market fluctuations.

4. Emotional Investing: Making investment decisions based on emotions, such as fear or greed, can lead to poor choices. Stay disciplined and avoid making impulsive investment decisions. Focus on your long-term financial goals and make decisions based on sound research and analysis.

5. Ignoring Fees and Expenses: High fees can eat into your investment returns over time. Be mindful of the fees and expenses associated with the funds in your 401k. Opt for low-cost index funds or exchange-traded funds (ETFs) that provide broad market exposure with lower expense ratios.

6. Overlooking Investment Reviews: Regularly review and evaluate your investment portfolio. Rebalance your allocations as needed to align with your investment objectives and risk tolerance. Failing to monitor and adjust your investments could result in an imbalanced portfolio that doesn’t align with your financial goals.

7. Cashing Out Early: Withdrawing money from your 401k account before retirement should be a last resort. Cashing out early not only incurs penalties and taxes but also robs you of the potential growth and compounding effect of your investments. Explore other financial options and alternatives before tapping into your retirement savings.

Avoiding these common pitfalls can help you make better choices with your 401k investments and increase your chances of building a robust retirement fund. Consult with a financial advisor or utilize reputable investment resources for guidance and support. In the next section, we will discuss how to track and evaluate your rate of return on your 401k investments.

Tracking and Evaluating Your Rate of Return

Tracking and evaluating your rate of return on your 401k investments is essential to gauge the performance of your portfolio and make informed adjustments. Here are some key steps to effectively track and evaluate your rate of return:

1. Regularly Monitor Account Statements: Review your 401k account statements on a regular basis. These statements provide details on your contributions, investment holdings, and any gains or losses. Examining these statements allows you to keep track of how your investments are performing over time.

2. Calculate the Rate of Return: To evaluate the rate of return on your 401k investments, calculate the percentage change in the account value over a specific period. You can use online calculators or financial software to simplify this process. Tracking your rate of return can help you assess the effectiveness of your investment strategy.

3. Compare Against Benchmarks: Compare your rate of return against relevant benchmarks, such as stock market indexes or industry-specific indices. This comparison provides insight into how your investments are performing relative to the broader market. It helps you assess whether you are achieving satisfactory returns or need to make adjustments to your portfolio.

4. Review Investment Performance: Evaluate the performance of individual investments within your portfolio. Identify the best-performing investments as well as any underperforming ones. Analyze the reasons behind the performance and determine whether it aligns with your expectations and goals.

5. Utilize Online Tools and Services: Take advantage of online tools and services that provide portfolio tracking and performance analysis. These resources often offer valuable insights, including portfolio allocation, risk assessment, and potential recommendations for optimization.

6. Work with a Financial Advisor: Consider consulting with a financial advisor specializing in retirement planning and investment management. A professional can provide expert guidance, help you analyze your rate of return, and suggest appropriate adjustments to align with your financial goals.

7. Regularly Rebalance Your Portfolio: Based on your evaluation and the guidance of a financial advisor, periodically rebalance your portfolio to ensure it aligns with your desired asset allocation and risk tolerance. This process involves selling overperforming investments and buying underperforming ones to maintain the desired balance.

Tracking and evaluating your rate of return allows you to make informed decisions about your 401k investments. It provides insights into your investment performance and helps you stay on track to achieve your retirement goals. By being proactive in monitoring and managing your account, you can optimize your returns and secure your financial future.

What to Do if Your Rate of Return is Below Average

If you find that your rate of return on your 401k investments is below average, there are several steps you can take to improve your performance and get back on track. Here are some actions to consider:

1. Reevaluate Your Investment Strategy: Take a closer look at your current investment strategy. Assess whether it aligns with your risk tolerance, time horizon, and financial goals. Consider adjusting your asset allocation and diversifying your investments to potentially increase your rate of return.

2. Consult with a Financial Advisor: Seek guidance from a financial advisor who specializes in retirement planning and investment management. They can review your portfolio, provide personalized recommendations, and help you make informed decisions to improve your returns.

3. Review and Adjust Fund Selection: Evaluate the performance of the individual funds in your portfolio. Replace underperforming funds with higher-performing alternatives that align with your investment strategy. Look for funds with solid track records and low expense ratios.

4. Increase Contributions: Consider increasing your contributions to your 401k account. By contributing a larger portion of your income, you can potentially boost your rate of return over time. Take advantage of any employer matching programs to maximize your retirement savings.

5. Utilize Catch-Up Contributions: If you are 50 years old or older, take advantage of catch-up contributions. These additional contributions, allowed by the IRS, allow you to contribute extra funds to your 401k beyond the regular contribution limit. Catch-up contributions can help accelerate the growth of your retirement savings.

6. Stay Invested for the Long Term: Avoid the temptation to make knee-jerk reactions based on short-term market fluctuations. Remember that investing in a 401k is a long-term strategy. Stay focused on your retirement goals and maintain a disciplined approach, holding investments that you believe have the potential for long-term growth.

7. Stay Educated and Informed: Continue to educate yourself about investment strategies, market trends, and retirement planning. Stay updated on the latest financial news and industry research. With ongoing education, you can make informed decisions and adapt your investment approach as needed.

Remember, it’s essential to be patient and make calculated adjustments to improve your rate of return. It may take time to see significant changes in performance. Regularly monitor your investments, review your strategy, and seek professional advice when necessary. By taking proactive steps, you can work towards achieving a more favorable rate of return on your 401k investments.

Conclusion

Understanding the rate of return on your 401k investments is crucial for planning your retirement and achieving your financial goals. While a good rate of return can vary, aiming for around 7-8% annually is generally considered favorable, taking into account market averages and inflation rates.

Several factors influence your rate of return, including asset allocation, investment strategy, market conditions, and the timing of contributions and withdrawals. By considering these factors and implementing effective investment strategies, such as diversification and regular portfolio reviews, you can potentially maximize your returns.

However, it’s important to balance the pursuit of higher returns with the associated risks. Investing comes with inherent risks, including market volatility, loss of principal, and concentration risk. It’s crucial to assess your risk tolerance and review your investments regularly to maintain a suitable risk level.

Avoiding common mistakes, such as failing to contribute enough, neglecting diversification, and emotional investing, is key to optimizing your 401k investments. Tracking and evaluating your rate of return allows you to gauge performance, make informed adjustments, and stay on track to meet your retirement goals.

If your rate of return is below average, reevaluating your investment strategy, seeking guidance from a financial advisor, and making adjustments can help improve performance. Additionally, increasing contributions, utilizing catch-up contributions, and staying invested for the long term can contribute to higher returns over time.

In conclusion, effectively managing your 401k investments requires knowledge, strategy, and a long-term perspective. By staying informed, being proactive, and making thoughtful decisions, you can navigate the complexities of investing and work towards achieving a successful rate of return on your 401k investments, securing a comfortable and financially stable retirement.