What is a 401(k)?

A 401(k) is a type of retirement savings account offered by employers as part of their employee benefits package. It is named after a section of the U.S. Internal Revenue Code that outlines the rules and regulations for these types of plans.

Simply put, a 401(k) allows individuals to save and invest a portion of their pre-tax income for retirement. Contributions to a 401(k) are made through automatic deductions from an employee’s paycheck. The money is then invested in a range of investment options, such as stocks, bonds, mutual funds, and other financial instruments.

One of the main advantages of a 401(k) is that contributions are typically tax-deductible, meaning that the money is invested before taxes are taken out of an employee’s paycheck. This allows individuals to lower their taxable income and potentially reduce their overall tax liability. However, withdrawals from a 401(k) are subject to income taxes at the time of distribution.

Another key feature of a 401(k) is that many employers offer a matching contribution, where they will contribute a certain percentage of an employee’s salary to their 401(k) account. This is essentially free money provided by the employer, and it’s a great incentive for employees to contribute to their retirement savings.

It’s important to note that there are contribution limits for 401(k) accounts. For 2021, the maximum contribution limit is $19,500 for individuals under the age of 50, and $26,000 for individuals aged 50 and older. These limits are set by the IRS and may change year to year.

One distinguishing factor of a 401(k) is that it is employer-sponsored, which means that individuals can only open and contribute to a 401(k) through their employer. However, if an individual changes jobs, they can either leave their 401(k) with their former employer, roll it over into a new employer’s 401(k) plan, or transfer it into an individual retirement account (IRA).

Overall, a 401(k) is a valuable retirement savings tool that allows individuals to save and invest for their golden years. By taking advantage of employer matching contributions and contributing regularly, individuals can grow their savings over time and secure a more comfortable retirement.

How does a 401(k) work?

A 401(k) is a retirement savings account that allows individuals to contribute a portion of their pre-tax income towards investments for their retirement. Let’s break down the key components of how a 401(k) works:

Automatic contributions: One of the main advantages of a 401(k) is the convenience of automatic contributions. These contributions are deducted directly from an employee’s paycheck before taxes are calculated. This allows individuals to save consistently without having to manually transfer money into their retirement account.

Employer matching: Many employers offer a matching contribution as an additional incentive for employees to save for retirement. The employer will match a percentage of the employee’s contribution, often up to a certain limit. For example, if an employee contributes 6% of their salary to their 401(k), the employer may match that with a 50% contribution, effectively adding 3% to the employee’s account. It’s important to take advantage of this match, as it is essentially free money.

Investment options: One of the key features of a 401(k) is the ability to invest in a range of options. These can include stocks, bonds, mutual funds, and other financial instruments. The investment choices are typically presented through a menu of options provided by the employer’s chosen plan administrator. Employees can select their preferred investment options based on their risk tolerance and long-term financial goals.

Tax advantages: Contributions to a traditional 401(k) are made with pre-tax dollars, meaning that the money contributed is not subject to income tax at the time of the contribution. This reduces an individual’s taxable income for that year. The investments in the 401(k) grow tax-deferred, meaning the gains are not taxed until withdrawals are made during retirement. This tax-deferred growth can help maximize the growth potential of the invested funds.

Withdrawal rules: While a 401(k) is primarily intended for retirement savings, there are specific rules regarding withdrawals. Typically, withdrawals before the age of 59 ½ are subject to a 10% early withdrawal penalty in addition to regular income taxes. However, there are exceptions to this penalty, such as financial hardship or certain qualified distributions. It’s important to understand the withdrawal rules and consult with a financial advisor before making any withdrawals from a 401(k).

Portability: If an employee changes jobs, they have a few options regarding their 401(k). They can leave the funds in their previous employer’s plan, which can continue to grow and be managed. Alternatively, they can roll over the funds into their new employer’s 401(k) plan if one is available, or into an individual retirement account (IRA). Rolling over the funds into an IRA can provide more investment options and flexibility.

Understanding how a 401(k) works is crucial for maximizing the benefits of this retirement savings account. By taking advantage of automatic contributions, employer matching, and investing wisely, individuals can build a solid foundation for their retirement years.

Types of 401(k) investments

When participating in a 401(k) plan, individuals have a variety of investment options to choose from. The specific investment options may vary depending on the plan provider, but here are some common types of investments you may find:

- Stock funds: These funds invest in shares of publicly traded companies. They offer the potential for long-term growth, but also come with higher risk compared to other investment options.

- Bond funds: Bond funds invest in fixed-income securities, such as government and corporate bonds. They generally provide lower returns compared to stocks, but offer a more stable source of income and can serve as a hedge against stock market volatility.

- Target-date funds: Target-date funds are a popular choice for many 401(k) investors. These funds invest in a mix of stocks, bonds, and other assets based on an individual’s target retirement date. As the individual approaches their retirement date, the fund automatically adjusts the asset allocation to become more conservative over time.

- Index funds: Index funds aim to replicate the performance of a specific market index, such as the S&P 500. These passively managed funds offer broad market exposure and typically have lower expense ratios compared to actively managed funds.

- Mutual funds: Mutual funds pool money from multiple investors to invest in a diversified portfolio of stocks, bonds, or other assets. They are managed by professional fund managers who make investment decisions on behalf of the investors.

- Exchange-Traded Funds (ETFs): ETFs are similar to mutual funds but trade on stock exchanges like individual stocks. They offer broad market exposure, low expense ratios, and can be bought or sold throughout the trading day.

- Company stock: Some 401(k) plans allow employees to invest a portion of their contributions in their employer’s company stock. While this can be an opportunity to align the employee’s financial interests with the company’s success, it’s important to diversify investments to mitigate risk and avoid having too much exposure to one company.

It’s crucial for individuals to carefully consider their risk tolerance, time horizon, and investment goals when selecting their 401(k) investments. Diversification is often recommended, as it helps spread risk across different asset classes and decreases the impact of any single investment. Many 401(k) plans provide tools and resources to help participants make informed investment decisions, such as risk assessment questionnaires and educational materials.

Remember, it’s important to regularly review and reassess your investment choices as your financial goals and market conditions change. Consulting with a financial advisor can also provide valuable guidance and help ensure your investment strategy aligns with your long-term objectives.

Understanding your investment options

When it comes to your 401(k), understanding your investment options is crucial for making informed decisions about where to allocate your retirement savings. Here are some key points to consider:

Read the plan’s investment materials: Your employer’s 401(k) plan will provide you with materials that outline the available investment options. Take the time to read through these materials to understand the investment objectives, risk profiles, historical performance, and costs associated with each option. This will help you make more informed decisions about which investments align with your goals and risk tolerance.

Consider your risk tolerance: Each investment option carries a certain level of risk. Stocks, for example, tend to have higher volatility and potential for higher returns, while bonds offer more stability but lower potential for growth. Assess your risk tolerance to determine how much volatility you’re comfortable with and choose investments accordingly.

Diversify your investments: Diversification is a key strategy for managing risk in your 401(k) portfolio. By spreading your investments across different asset classes, such as stocks, bonds, and mutual funds, you can potentially reduce the impact of any single investment on your overall portfolio. This can help mitigate risk and improve the likelihood of achieving your long-term financial goals.

Consider your time horizon: Your time horizon is the length of time you have until retirement. Generally, the longer your time horizon, the more aggressive you can be with your investments since you have more time to ride out market fluctuations. Conversely, if you’re nearing retirement, it may be prudent to adjust your investment strategy to focus more on preserving capital rather than pursuing high growth.

Review performance metrics: When evaluating investment options, consider performance metrics such as average annual returns, volatility measures, and expense ratios. Analyze the historical performance of each investment option and compare it against benchmark indices or similar funds to get a sense of how well it has performed relative to its peers.

Take advantage of professional advice: If you’re unsure about which investment options to choose, or if you want personalized guidance based on your unique financial situation, consider consulting with a financial advisor. They can provide valuable insights and help you create an investment strategy that aligns with your goals and risk tolerance.

Remember, investing involves risks, and past performance is not indicative of future results. Regularly review your investment options and make adjustments as needed to ensure your portfolio remains aligned with your long-term financial goals and evolving market conditions.

Evaluating investment performance

When it comes to managing your 401(k) investments, evaluating investment performance is an essential step in ensuring that your portfolio is on track to help you achieve your retirement goals. Here are some key factors to consider when evaluating the performance of your investments:

Investment objectives: First and foremost, evaluate your investment performance against your investment objectives. Are you aiming for long-term growth, capital preservation, or a combination of both? Understanding your investment objectives will help you determine if your investments are performing in line with your goals.

Time horizon: Consider your time horizon when evaluating investment performance. Short-term fluctuations in the market may not be as critical if you have a long time until retirement. Focus on the long-term performance and growth potential of your investments rather than short-term volatility.

Compare to benchmarks: Benchmark indices are a way to measure the performance of a specific market or asset class. Compare the performance of your investments to relevant benchmarks to see how they are performing relative to the broader market. This can provide valuable insights into whether your investments are outperforming or underperforming their respective benchmarks.

Consistency of returns: Evaluate the consistency of returns from your investments. Are the returns consistent over time or are they volatile? Consider whether the returns are meeting your expectations and if any substantial fluctuations require adjustment to your investment strategy.

Expense ratios: Take into account the expense ratios associated with your investment options. Expense ratios represent the costs associated with managing and operating the investment funds. Lower expense ratios generally mean higher returns for investors. If you notice that some of your investments have high expense ratios and are underperforming, it may be worth considering alternative options with lower costs.

Risk-adjusted returns: Evaluating risk-adjusted returns can provide a clearer picture of how well your investments are performing. Compare the returns to the level of risk taken. Investments that generate higher returns with lower levels of risk are generally considered to be performing well.

Review diversification: Assess the diversification of your portfolio. A well-diversified portfolio spreads the risk across different asset classes and investment options. Evaluate whether your investments are adequately diversified to mitigate risk and potentially enhance returns.

Consider market conditions: Market conditions can influence the performance of investments. Take into account the overall market trends and economic factors that may impact your investments. However, be cautious not to make knee-jerk reactions based solely on short-term market fluctuations.

Evaluating investment performance is an ongoing process. Regularly review your portfolio and make adjustments as needed to ensure that your investments remain aligned with your long-term financial goals. It’s also advisable to consult with a financial advisor who can provide professional guidance and help you make informed decisions about your 401(k) investments.

Making changes to your portfolio

As you progress through your career and your financial goals evolve, it’s important to periodically review and make changes to your 401(k) portfolio. Here are some key considerations and steps to follow when making changes:

Assess your risk tolerance: Start by reassessing your risk tolerance. As you go through different life stages, your risk tolerance may change. Determine whether you’re comfortable with the level of risk in your portfolio or if you need to adjust it to better align with your current financial situation and goals.

Review your investment objectives: Take the time to reevaluate your investment objectives. Are you primarily focused on long-term growth, capital preservation, or a combination of both? This will help you determine if your current investment holdings are still suitable or if adjustments need to be made.

Review performance: Evaluate the performance of your current investments. Compare their performance against relevant benchmarks and your own expectations. Identify any investments that consistently underperform or show signs of weakness. Consider whether it’s time to make changes to those specific holdings.

Consider asset allocation: Determine if your portfolio is properly diversified across different asset classes, such as stocks, bonds, and cash equivalents. Adjustments may be needed if your allocation is heavily skewed towards one asset class, which can expose you to undue risk. Strive to maintain a diversified portfolio that aligns with your risk tolerance and investment objectives.

Research new investment options: Take the time to research new investment options that may be available within your 401(k) plan. Familiarize yourself with the investment options provided by your plan administrator. Look for options that align with your investment goals and may offer the potential for better returns.

Consult with a financial advisor: If you’re unsure about making changes to your portfolio or need personalized guidance, consider consulting with a financial advisor. They can provide expert advice based on your specific financial situation and help you make informed decisions about your investments.

Implement changes gradually: When making changes to your portfolio, it’s generally recommended to implement them gradually rather than all at once. This approach helps manage volatility and reduces the potential impact of short-term market fluctuations. Consider adjusting your investments incrementally over time to achieve your desired portfolio composition.

Monitor and reassess regularly: After making changes to your portfolio, continue to monitor its performance and reassess your investment strategy on a regular basis. Track the performance of your investments, review their suitability, and make adjustments as necessary to keep your portfolio on track towards your long-term financial goals.

Making changes to your 401(k) portfolio is a proactive step that can help optimize your investment strategy. By regularly reviewing and adjusting your holdings, you can ensure that your portfolio remains aligned with your financial objectives and provides the best opportunity for achieving your retirement goals.

Tax implications of 401(k) investments

Understanding the tax implications of 401(k) investments is crucial for making informed decisions about your retirement savings strategy. Here are some key tax considerations to keep in mind:

Pre-tax contributions: One of the main benefits of contributing to a traditional 401(k) is that your contributions are made with pre-tax dollars. This means that the money you contribute to your 401(k) is deducted from your taxable income in the year it is contributed. Consequently, contributing to your 401(k) lowers your overall taxable income, potentially reducing the amount of income tax you owe.

Tax-deferred growth: Another advantage of 401(k) investments is that they grow tax-deferred. This means that you don’t have to pay taxes on the investment gains and earnings within your 401(k) until you make withdrawals during retirement. The compounding effect of tax-deferred growth allows your investments to potentially grow faster over time.

Withdrawals and taxes: When you start taking withdrawals from your 401(k) during retirement, the amount withdrawn is subject to ordinary income taxes. The tax rate applied to your withdrawals will depend on your income tax bracket at that time. It’s important to note that if you withdraw funds from your 401(k) before the age of 59 ½, you may incur a 10% early withdrawal penalty on top of the regular income taxes.

Roth 401(k) options: Some employers offer Roth 401(k) options alongside traditional 401(k) plans. Contributions to a Roth 401(k) are made with after-tax dollars, meaning that they are not tax-deductible in the year of contribution. However, qualified withdrawals from a Roth 401(k) are tax-free, including the investment gains. Choosing between traditional and Roth 401(k) contributions depends on your current and future tax situation.

Required Minimum Distributions (RMDs): Once you reach the age of 72, the IRS requires you to start taking distributions from your traditional 401(k) account, known as Required Minimum Distributions (RMDs). These distributions are subject to income taxes. Failing to take the RMD can result in a hefty penalty, so it’s crucial to understand the timing and the calculated minimum distribution amount.

Tax strategies in retirement: During retirement, you may have opportunities to employ tax strategies to minimize your tax liability. For example, you can strategically manage your withdrawals from different types of retirement accounts (such as 401(k)s, IRAs, and taxable accounts) to optimize taxes. Consulting with a tax advisor can provide valuable insights into these strategies and help ensure your retirement income is tax-efficient.

While 401(k) investments provide various tax advantages during the accumulation phase, it’s important to carefully plan for the potential tax consequences during retirement. Consulting with a tax professional or financial advisor can help you navigate the complex tax rules and develop a tax-efficient retirement plan.

Common mistakes to avoid

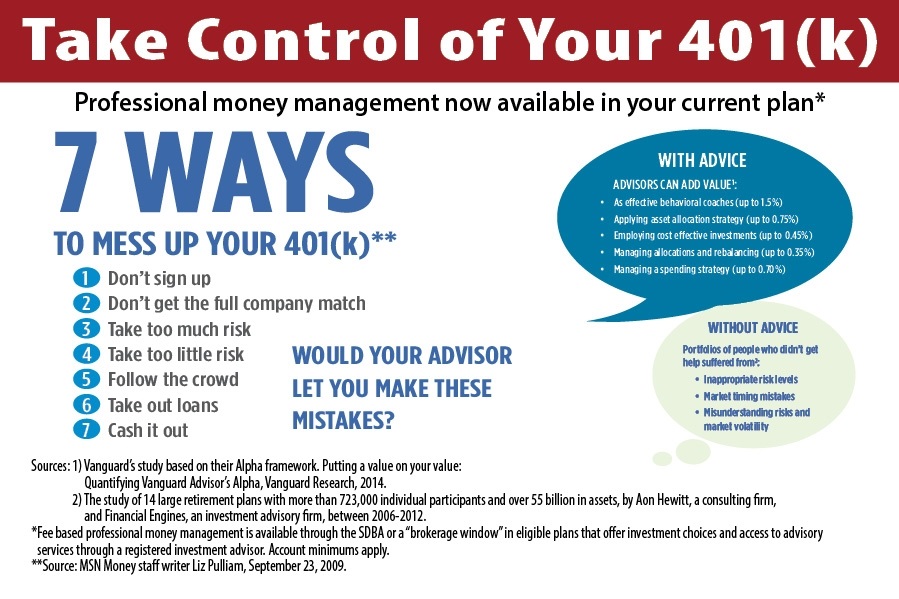

When it comes to managing your 401(k) investments, there are several common mistakes that individuals should be aware of and strive to avoid. By avoiding these mistakes, you can help maximize the growth potential of your retirement savings. Here are some pitfalls to watch out for:

Not taking full advantage of employer matching: One of the biggest mistakes is failing to contribute enough to your 401(k) to receive the full employer matching contribution. Employer matching is essentially free money, so be sure to contribute at least enough to capture the full match. Otherwise, you’re leaving valuable benefits on the table.

Overconcentration in company stock: Holding a significant portion of your 401(k) in your employer’s company stock can be a risky strategy. If the company experiences financial difficulties, your retirement savings may be severely impacted. Diversify your investments across different asset classes to mitigate risk and avoid having too much exposure to a single stock.

Ignoring fees and expenses: Many individuals overlook or underestimate the impact of fees and expenses associated with their 401(k) investments. High fees can eat into your investment returns over time, so pay close attention to expense ratios and any administrative fees. Choose low-cost investment options whenever possible to maximize your long-term returns.

Chasing short-term market trends: Trying to time the market or chasing short-term market trends is a common mistake. It’s nearly impossible to consistently predict market movements, and trying to do so can lead to poor investment choices and unnecessary trading fees. Maintain a long-term investment strategy and focus on your overall financial goals.

Not regularly reviewing and rebalancing: Failing to review and rebalance your portfolio on a regular basis can lead to an unbalanced asset allocation. Over time, certain investments may outperform or underperform, causing your portfolio to drift away from your desired risk level. Revisit your portfolio periodically and rebalance to ensure it remains aligned with your investment objectives.

Panic selling during market downturns: During periods of market turbulence, it’s common for investors to panic and sell their investments. However, this knee-jerk reaction often leads to selling low and missing out on potential market recoveries. Stay focused on your long-term goals and resist the urge to make impulsive decisions based on short-term market volatility.

Withdrawing funds prematurely: Withdrawing funds from your 401(k) before retirement should only be a last resort. Not only will you incur early withdrawal penalties, but you’ll also miss out on potential tax-deferred growth. Explore other avenues for emergency funds or consider taking out a loan against your 401(k) instead of prematurely depleting your retirement savings.

Not seeking professional advice: Lastly, not seeking professional advice when it comes to managing your 401(k) can be a mistake. A financial advisor can provide valuable guidance, help you navigate complex investment decisions, and develop a personalized retirement plan tailored to your unique needs and goals.

By avoiding these common mistakes, you can be better positioned to optimize your 401(k) investments and work towards a financially secure retirement.

Important factors to consider when choosing 401(k) investments

Choosing the right investments for your 401(k) is a key decision that can significantly impact your long-term financial well-being. Here are some important factors to consider when selecting your 401(k) investments:

Investment goals and time horizon: Clearly define your investment goals and time horizon. Are you saving for retirement in the next few years or several decades down the line? Your goals and time horizon will help determine appropriate investment strategies and asset allocations for your 401(k) investments.

Risk tolerance: Understand your risk tolerance—the degree of uncertainty and potential loss you are willing to bear. Some individuals have a high risk tolerance and are comfortable with the volatility of the stock market, while others prefer less risky investments. Choose investments that align with your risk tolerance to ensure you can sleep soundly at night.

Diversification: Diversification is a key risk management strategy. Spread your investments across different asset classes, such as stocks, bonds, and cash equivalents, to reduce concentration risk. Diversifying your portfolio can help mitigate the impact of any single investment’s performance on your overall returns.

Expense ratios: Pay attention to expense ratios—the annual fees charged by mutual funds and other investment options. Lower expense ratios directly impact your investment returns, so seek low-cost investment options whenever possible to maximize your long-term growth potential.

Past performance: While past performance does not guarantee future results, reviewing the historical performance of investment options can provide insights into their track record. Compare the performance of different funds against relevant benchmarks and consider consistent performers with strong long-term track records.

Quality of the investment management: Assess the quality and reputation of the investment management teams behind the available funds. Look for experienced fund managers with strong track records and a disciplined investment process. The expertise and decision-making of the fund managers can impact the performance of your investments.

Plan features and flexibility: Consider the features and flexibility of your 401(k) plan. Some plans offer a wide range of investment options, while others may have more limited choices. Evaluate if the available investment options align with your preferences and investment strategy.

Plan expenses and fees: In addition to expense ratios, review any other plan expenses and fees that may be charged. These can include administrative fees, record-keeping fees, or transaction fees. Be aware of any costs associated with your 401(k) plan and understand their impact on your overall investment returns.

Rebalancing options: Understand the availability and ease of rebalancing your portfolio. Regularly rebalancing your investments helps maintain your desired asset allocation and risk levels. Look for a plan that offers easy access to rebalancing features and the ability to realign your investments periodically.

Educational resources and support: Evaluate the educational resources and support available through your 401(k) plan. Access to tools, online resources, and educational materials can empower you to make informed investment decisions and grow your financial literacy.

When choosing your 401(k) investments, take the time to evaluate these important factors. Consider working with a financial advisor who can provide personalized guidance and help you create a well-structured investment strategy that aligns with your goals, risk tolerance, and time horizon.

Conclusion

Managing your 401(k) investments is a crucial aspect of planning for a financially secure retirement. Understanding how a 401(k) works, evaluating investment options, and making informed decisions can greatly impact the growth and success of your retirement savings. By considering factors such as risk tolerance, diversification, fees, and performance, you can create a well-rounded investment strategy that aligns with your goals and financial situation.

Avoiding common mistakes, such as not taking full advantage of employer matching, overconcentrating in company stock, or ignoring fees, can help optimize your 401(k) investments. Regularly reviewing and reassessing your portfolio, making necessary changes, and staying informed about tax implications are essential to stay on track to meet your retirement objectives.

Remember, managing your 401(k) investments is an ongoing process. Market conditions, personal circumstances, and financial goals may change over time, requiring adjustments to your investment strategy. Seeking professional advice, leveraging educational resources, and staying proactive in your investment decisions can provide valuable guidance and support along the way.

Building a strong retirement nest egg takes time, patience, and careful planning. By making wise investment choices, taking advantage of employer contributions, and staying disciplined, you can maximize the growth potential of your 401(k) investments and enjoy a financially secure retirement.