Introduction

When it comes to planning for retirement, one of the most common investment vehicles that individuals rely on is a 401(k) plan. A 401(k) plan offers individuals the opportunity to invest their pre-tax income, with the potential for tax-deferred growth over time. However, as with any investment, it’s important to regularly review and assess the performance of your 401(k) investments to ensure that they align with your financial goals and risk tolerance.

In this article, we will explore the question of how often you can change your 401(k) investments and the factors to consider before making any changes. We’ll also discuss the benefits of regularly monitoring and adjusting your portfolio, as well as common mistakes to avoid when making changes to your 401(k) investments.

Before diving into the specifics, it’s important to have a clear understanding of what a 401(k) plan is and how it works. Let’s take a closer look.

What is a 401(k) Plan?

A 401(k) plan is a retirement savings plan that is offered by employers to their employees. It is named after the section of the Internal Revenue Code that governs it. With a 401(k) plan, employees have the opportunity to save and invest a portion of their salary for retirement on a tax-deferred basis.

One of the main advantages of a 401(k) plan is that contributions are made with pre-tax income, meaning that the contributions are deducted from an employee’s salary before taxes are withheld. This reduces the employee’s taxable income, allowing them to save more money and potentially lower their overall tax liability.

In addition to the immediate tax benefits, contributions made to a 401(k) plan grow tax-free until the funds are withdrawn in retirement. This tax-deferred growth allows the investments in the 401(k) plan to compound over time, potentially resulting in significant growth and a larger retirement nest egg.

Employers often offer a matching contribution as part of a 401(k) plan, where they will match a certain percentage of an employee’s contributions. This employer match is essentially free money that can further boost an employee’s retirement savings.

401(k) plans typically offer a range of investment options, such as stocks, bonds, mutual funds, and target-date funds. These options allow employees to diversify their investments and customize their portfolio based on their risk tolerance and retirement goals.

It’s important to note that contributions to a 401(k) plan are subject to annual limits set by the IRS. For 2021, the maximum contribution limit is $19,500 for individuals under the age of 50, with an additional catch-up contribution of $6,500 for those who are 50 or older.

Now that we have a basic understanding of what a 401(k) plan is, let’s move on to the next section and delve into the various investment options that are available within a 401(k) plan.

Understanding 401(k) Investment Options

When it comes to investing in a 401(k) plan, it’s important to have a good understanding of the various investment options available. A 401(k) plan typically offers a range of investment choices, including stocks, bonds, mutual funds, and target-date funds.

Stocks: Investing in stocks provides individuals with ownership in a company. Stocks can offer the potential for higher returns over the long term, but they also come with a higher level of risk as their value can fluctuate greatly based on market conditions.

Bonds: Bonds are essentially loans made to corporations or governments, and investors receive fixed interest payments over a specified period of time. Bonds are generally considered lower-risk investments compared to stocks, as they provide a steady income stream, but they also offer lower potential returns.

Mutual Funds: A mutual fund is a pool of money that is invested in a diversified portfolio of stocks, bonds, or other securities. By investing in a mutual fund, individuals can gain exposure to a wide range of assets, which helps to spread out risk. Mutual funds are managed by professional fund managers, who make investment decisions on behalf of the investors in the fund.

Target-Date Funds: Target-date funds are designed to meet the needs of investors based on their expected retirement date. These funds typically include a mix of stocks, bonds, and other assets that are automatically rebalanced as the investor gets closer to retirement. Target-date funds offer a hands-off approach to investing, as the asset allocation is adjusted over time to become more conservative as the retirement date approaches.

It’s important to carefully consider your risk tolerance, investment goals, and time horizon when choosing the investment options within your 401(k) plan. Diversification is key to managing risk, as it helps to spread out investments across different asset classes and reduce the impact of any single investment on your overall portfolio.

Now that we have a better understanding of the investment options available within a 401(k) plan, let’s move on to the next section to discuss the importance of regularly reviewing your 401(k) investments.

The Importance of Reviewing Your 401(k) Investments

Regularly reviewing your 401(k) investments is essential to ensure that your portfolio remains aligned with your financial goals and risk tolerance. Here are some key reasons why this review process is important:

1. Assessing Performance: By reviewing your 401(k) investments, you can evaluate how well your portfolio is performing. This allows you to identify any underperforming investments or areas that may require adjustment. It’s important to compare the performance of your investments against appropriate benchmarks to gauge their effectiveness.

2. Rebalancing: Over time, the value of different investments within your portfolio can change, resulting in an unbalanced asset allocation. Regular review and rebalancing help to maintain your desired allocation and adjust for any deviations. For example, if a particular investment has exceeded its target allocation, you may need to sell some shares and reallocate the funds to investments that have fallen below their target.

3. Adjusting for Market Conditions: Markets are dynamic and can experience fluctuations based on economic conditions and other factors. Reviewing your investments regularly allows you to assess whether any adjustments are needed in response to market changes. This ensures that you remain aligned with your risk tolerance and investment objectives.

4. Changing Financial Goals: As life circumstances change, so too may your financial goals. For example, if you anticipate retiring earlier or needing more funds for a specific goal, like purchasing a home or funding your child’s education, you may need to adjust your investment strategy accordingly. Regularly reviewing your investments allows you to make any necessary changes to support your evolving goals.

5. Maximizing Tax Efficiency: Certain investment strategies or account types may offer tax advantages. By reviewing your investments, you can identify opportunities to maximize tax efficiency within your 401(k) plan. For instance, you may consider allocating a portion of your portfolio to tax-efficient index funds or taking advantage of tax-saving features like a Roth 401(k) option if available.

Remember, reviewing your 401(k) investments should be done with a long-term perspective in mind. It’s important to strike a balance between making informed adjustments and avoiding knee-jerk reactions to short-term market fluctuations.

Now that we understand why reviewing your 401(k) investments is crucial, let’s explore whether you can change your 401(k) investments and the factors to consider before doing so.

Can I Change My 401(k) Investments?

Yes, you have the ability to change your 401(k) investments. In fact, one of the advantages of a 401(k) plan is the flexibility it offers in terms of investment options. However, it’s important to understand the rules and guidelines set by your employer and the plan administrator.

Most 401(k) plans allow participants to make changes to their investments on a periodic basis. This can range from quarterly adjustments to monthly or even daily changes, depending on the specific rules of your plan. The frequency of changes may also vary based on the platform or provider through which your 401(k) plan is administered.

Typically, changes to your 401(k) investments can be made through an online portal, by contacting the plan administrator, or by submitting a paper form. The process may differ slightly depending on the specific procedures outlined by your employer and plan administrator.

It’s important to review the investment options available within your 401(k) plan and ensure that they align with your risk tolerance, investment goals, and time horizon. Consider factors such as the fund’s performance, expense ratio, and the overall asset allocation. If the available investment options do not meet your needs, you may want to discuss with the plan administrator if additional options can be made available or consider other retirement savings vehicles.

When making changes to your 401(k) investments, keep in mind that there may be restrictions or limitations imposed by your employer or the plan administrator. These could include restrictions on the frequency of changes, minimum investment amounts, or blackout periods during which no changes can be made. Familiarize yourself with these rules to ensure that you adhere to the guidelines set by your plan.

Additionally, it’s important to note that any changes you make to your 401(k) investments may have tax implications. For example, if you sell shares of a fund for a gain, you may be subject to capital gains taxes. Conversely, if you sell shares for a loss, you may be able to offset gains or deduct the losses on your tax return. Consider consulting with a tax professional to understand the potential tax consequences of any investment changes you make.

Now that we understand that changes can be made to 401(k) investments, let’s explore the factors you should consider before making any changes.

Factors to Consider Before Making Changes

Before making any changes to your 401(k) investments, it’s important to carefully consider a few key factors. These factors will help ensure that your investment decisions align with your financial goals and risk tolerance. Here are the main considerations:

1. Risk Tolerance: Assess your risk tolerance and investment comfort level. Ask yourself how comfortable you are with fluctuations in your investment value and whether you have a long-term perspective. Understanding your risk tolerance will help you determine the appropriate asset allocation for your 401(k) investments.

2. Time Horizon: Consider your time horizon for retirement. If you have several decades until retirement, you may have a higher risk tolerance and can afford to invest in more aggressive options. However, if retirement is imminent, you may want to adopt a more conservative approach to safeguard your investments.

3. Diversification: Ensure that your portfolio is properly diversified across different asset classes. Diversification helps to spread risk and can protect you from significant losses in any one investment. Assess whether your current allocation is in line with your desired level of diversification.

4. Performance: Evaluate the performance of your current investments. Consider the returns you have achieved over different time periods and compare them to relevant benchmarks. Review both short-term and long-term performance to assess whether any adjustments are warranted.

5. Fees and Expenses: Take a close look at the fees and expenses associated with the investment options in your 401(k) plan. High fees can eat into your returns over time, so it’s important to choose investments with reasonable expense ratios. Consider the impact of fees on your long-term investment growth.

6. Personal Financial Goals: Evaluate your personal financial goals and how your 401(k) investments align with them. Are there specific milestones or objectives you’re aiming to achieve? Consider whether any changes are necessary to help you meet those goals effectively.

7. Expert Advice: If you’re uncertain about how to navigate your 401(k) investment decisions, seek professional advice. Financial advisors can provide guidance tailored to your specific circumstances, helping you make informed choices that align with your objectives.

Remember, making changes to your 401(k) investments should be a thoughtful and well-informed decision. It’s important to avoid knee-jerk reactions to short-term market fluctuations and to take a long-term perspective on your investments.

Now that we’ve discussed the factors to consider before making changes, let’s explore how often you should change your 401(k) investments.

How Often Should I Change My 401(k) Investments?

The frequency at which you should change your 401(k) investments depends on several factors, including your investment strategy, risk tolerance, and overall market conditions. Here are a few considerations to help determine how often you should make changes:

1. Long-term Strategy: It’s important to remember that 401(k) investments are typically intended for long-term growth and retirement planning. Therefore, it’s generally recommended to have a long-term investment strategy and avoid frequent changes based on short-term market fluctuations. Instead, focus on a well-diversified portfolio that aligns with your financial goals.

2. Regular Portfolio Review: Even though a long-term approach is recommended, it’s still crucial to conduct regular portfolio reviews. This ensures that your investments remain in line with your risk tolerance and financial objectives. A general rule of thumb is to review your portfolio at least once a year or when significant life events occur, such as a job change or nearing retirement.

3. Market Conditions: Consider the prevailing market conditions when deciding whether to make changes to your 401(k) investments. If there are significant market movements or changes in economic outlook, it may be appropriate to review your portfolio more frequently. However, avoid making hasty decisions based solely on short-term market trends and instead focus on long-term performance.

4. Rebalancing Opportunities: One common reason to make changes to your 401(k) investments is to rebalance your portfolio. Rebalancing involves adjusting your asset allocation to maintain your desired risk level. It is typically recommended to rebalance annually or when your portfolio’s asset allocation deviates significantly from your target allocation.

5. Expert Advice: Seeking advice from a financial professional can help guide your decision on how often to change your 401(k) investments. They can provide valuable insights based on your specific financial situation, risk tolerance, and investment goals. Financial advisors can also help you navigate market cycles and make informed decisions.

Remember, the key is to strike a balance between actively monitoring your investments and avoiding unnecessary changes. Aim for a disciplined approach to investment management that aligns with your long-term objectives rather than reacting to short-term market fluctuations.

Now that we’ve explored how often you should change your 401(k) investments, let’s discuss the benefits of regularly monitoring and adjusting your portfolio.

Benefits of Regularly Monitoring and Adjusting Your Portfolio

Regularly monitoring and adjusting your portfolio within your 401(k) plan offers several benefits that can help optimize your investment strategy and improve long-term outcomes. Here are some key advantages of staying proactive with your portfolio management:

1. Maintaining Alignment with Goals: Regularly monitoring your portfolio allows you to ensure that your investments remain aligned with your financial goals. As your goals may change over time, such as nearing retirement or adjusting risk tolerance, making adjustments to your portfolio can help keep it in tune with your evolving objectives.

2. Risk Management: By actively monitoring your 401(k) investments, you can assess and manage the level of risk exposure in your portfolio. This allows you to make informed decisions about rebalancing assets and adjusting your allocation to mitigate unnecessary risk or take advantage of potential opportunities.

3. Capitalizing on Market Trends: Regular monitoring can help you identify emerging market trends or investment opportunities. By staying informed about market conditions and adjusting your portfolio accordingly, you can position yourself to potentially benefit from market upswings or make course corrections during periods of volatility.

4. Optimizing Performance: Monitoring performance allows you to evaluate the effectiveness of your investment strategy. By identifying underperforming assets or funds, you can make informed decisions on whether adjustments or replacements are necessary to improve overall performance and potentially maximize your returns.

5. Taking Advantage of Employer Matches: Regularly monitoring your 401(k) investments can help you maximize contributions and take full advantage of any employer match contributions. By reviewing your contributions and ensuring you meet the required percentage to receive the full match, you can boost your retirement savings and overall investment growth.

6. Maintaining Diversification: Portfolio monitoring ensures that your asset allocations remain diversified. Regularly assessing the balance of your investments helps prevent the overconcentration of certain stocks or sectors, which can help mitigate risk and protect your portfolio from significant market fluctuations.

7. Staying Informed: By actively monitoring your portfolio, you can stay informed about the performance and developments of your investments. This knowledge empowers you to make timely decisions based on sound information rather than relying solely on market rumors or emotions.

While regular monitoring and adjustments have their benefits, it’s important to strike a balance and avoid making frequent, impulsive changes based solely on short-term market movements. Consistency and a long-term investment perspective are key to achieving your retirement goals.

Now that we’ve discussed the benefits of regularly monitoring and adjusting your portfolio, let’s explore some common mistakes to avoid when making changes to your 401(k) investments.

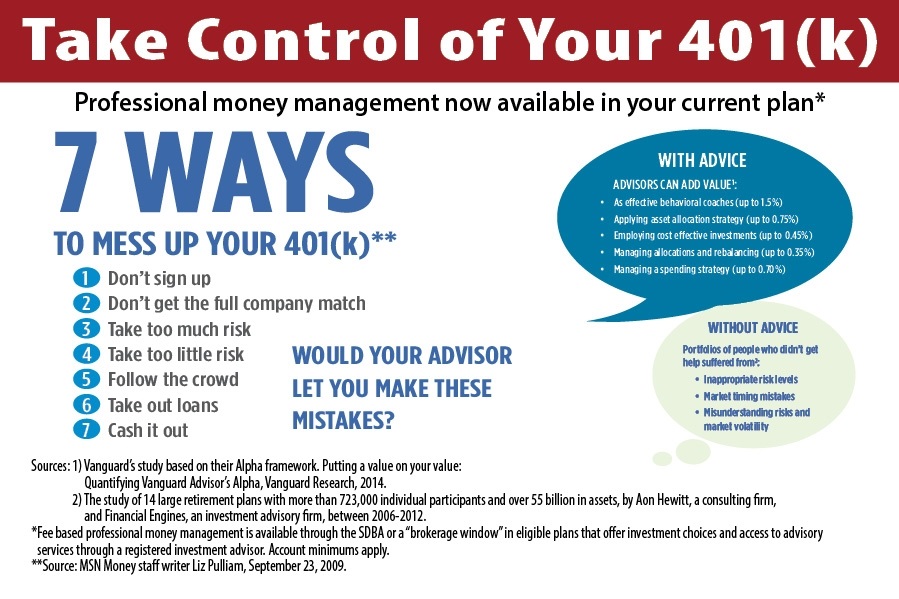

Common Mistakes to Avoid When Changing 401(k) Investments

When it comes to changing your 401(k) investments, it’s important to approach the process with careful consideration and avoid these common mistakes:

1. Timing the Market: Trying to time the market by making frequent changes to your investments based on short-term market fluctuations is a common mistake. It’s challenging to consistently predict market movements accurately. Instead, focus on a long-term investment strategy and resist the urge to make reactive decisions based on market timing.

2. Emotional Decision Making: Making investment decisions based on emotions, such as fear or greed, can lead to poor outcomes. Emotional decisions often result in buying high and selling low, which goes against the principles of disciplined investing. Keep a level head and stick to your investment strategy.

3. Lack of Diversification: Neglecting diversification by putting all your eggs in one basket can be risky. Avoid the mistake of being overly concentrated in one asset class, industry, or stock. Diversification helps spread out risk and can help protect your portfolio from significant market downturns.

4. Overreacting to Short-Term Performance: It’s natural to be concerned when an investment underperforms over a short period. However, it’s crucial to assess performance over the long term and avoid knee-jerk reactions. A disciplined approach based on a comprehensive evaluation of performance is key to making informed decisions.

5. Ignoring Fees and Expenses: Many investors overlook the impact of fees and expenses on their investment returns. High fees can eat into your overall portfolio growth over time. Take the time to understand the fees associated with your investment choices and select lower-cost options when appropriate.

6. Neglecting Regular Portfolio Reviews: Failing to review and adjust your portfolio regularly is a common mistake. Regular portfolio reviews help ensure that your investments are in line with your goals and risk tolerance. Without periodic assessments, your portfolio may become unbalanced and deviate from your intended investment strategy.

7. Not Seeking Professional Guidance: Some individuals may make investment decisions without seeking professional guidance. While it’s commendable to be proactive about managing your investments, consulting with a qualified financial advisor can provide valuable insights and help you make more informed decisions tailored to your specific situation.

8. Not Considering Tax Implications: When making changes to your 401(k) investments, it’s important to consider potential tax implications. Understanding the tax consequences of selling investments for gains or losses can help you make more informed decisions and optimize your overall tax situation.

Avoiding these common mistakes when making changes to your 401(k) investments can help position you for long-term success. Remember to stay focused on your investment strategy, maintain a diversified portfolio, and seek guidance when needed.

Now let’s explore some strategies for making changes to your 401(k) investments.

Strategies for Making Changes to Your 401(k) Investments

When it comes to making changes to your 401(k) investments, it’s important to approach the process with a thoughtful strategy. Here are some effective strategies to consider:

1. Review and Assess Your Goals: Start by reviewing your financial goals and risk tolerance. Determine if any changes are needed to align your investment strategy with your objectives. Consider factors such as your time horizon, desired retirement age, and income needs in retirement.

2. Evaluate Performance and Asset Allocation: Assess the performance of your current investments and the overall asset allocation of your portfolio. Identify any underperforming assets or significant deviations from your target allocation. This evaluation will guide you in making informed decisions about potential adjustments.

3. Rebalance Your Portfolio: If your asset allocation has deviated significantly from your target, consider rebalancing your portfolio. Rebalancing involves selling overweighted assets and buying underweighted assets to realign with your desired allocation. Regular rebalancing ensures that your risk exposure stays within your comfort zone and maintains diversification.

4. Consider Target-Date Funds: If you prefer a hands-off approach to investment management, consider investing in target-date funds. These funds automatically adjust their asset allocation based on your anticipated retirement date. They gradually shift towards a more conservative allocation as you approach retirement, providing a convenient and straightforward investment option.

5. Dollar-Cost Averaging: Implementing a dollar-cost averaging strategy can help smooth out market fluctuations. Instead of making large, lump-sum investments, contribute a fixed amount regularly. This approach allows you to buy more shares when prices are low and fewer shares when prices are high, reducing the impact of short-term market volatility.

6. Seek Professional Advice: If you’re unsure about how to navigate your 401(k) investment decisions, consider consulting with a financial advisor. A qualified advisor can provide personalized guidance based on your financial situation, risk tolerance, and investment goals. They can help you determine the most suitable investment options within your 401(k) plan and assist in creating a customized strategy.

7. Stay Informed and Educated: Take the time to stay informed about current market trends and changes in the investment landscape. Continue to educate yourself about different investment options and strategies. Regularly review financial news, reputable financial publications, and educational resources to enhance your investment knowledge.

Remember that making changes to your 401(k) investments should align with your long-term goals. Avoid making impulsive decisions based on short-term market fluctuations. Instead, develop and follow a well-thought-out investment strategy that supports your financial objectives.

Now that we’ve discussed strategies for making changes to your 401(k) investments, let’s summarize the key points we’ve covered in this article.

Conclusion

Managing your 401(k) investments is a crucial component of ensuring your financial security in retirement. By understanding the options available within your 401(k) plan and regularly reviewing and adjusting your investments, you can optimize your portfolio and increase the likelihood of achieving your long-term goals.

We started by understanding what a 401(k) plan is and how it works, emphasizing the importance of taking advantage of employer matches and selecting investment options that align with your risk tolerance and retirement goals.

We then explored the importance of reviewing your 401(k) investments, considering factors such as performance, risk, market conditions, and personal financial goals. We discovered that regular monitoring and adjustment can help maintain alignment with your objectives and safeguard your investments from unnecessary risk.

While it’s important to make informed changes to your 401(k) investments, we also identified common mistakes to avoid, such as emotional decision making, lack of diversification, and neglecting regular portfolio reviews. By recognizing these pitfalls, you can make more informed decisions and avoid potential pitfalls that could hinder your long-term success.

We also discussed how often you should change your investments, emphasizing the need for a balanced approach. Regular monitoring, portfolio reviews, and strategic adjustments are recommended, but timing the market and frequent changes based on short-term fluctuations should be avoided.

To make effective changes to your 401(k) investments, we provided strategies that include evaluating goals and performance, rebalancing your portfolio, utilizing target-date funds, dollar-cost averaging, seeking professional advice, and staying informed about the market and investment landscape.

Remember, your 401(k) is a long-term retirement savings tool, and decisions should be made within that context. Regular review, thoughtful adjustments, and adherence to your investment plan are key components of a successful retirement strategy.

If you are uncertain about managing your 401(k) investments or need assistance in developing a customized strategy, consider seeking advice from a financial professional who can provide personalized guidance based on your unique circumstances.

By following these principles and strategies, you can optimize your 401(k) portfolio and work towards achieving a financially secure retirement.