Introduction

Welcome to the world of 401k investments! Managing your 401k investments is an essential part of securing a financially stable future. Whether you are a novice investor or someone with experience, understanding how to make the most of your 401k is crucial.

So, what is a 401k? In simple terms, it is a retirement account provided by your employer that allows you to save and invest for your golden years. The beauty of a 401k lies in its tax advantages, as contributions are typically made with pre-tax dollars, and any gains within the account are tax-deferred until you withdraw the funds.

Now, you may be wondering why you should take an active role in managing your 401k investments. Well, the truth is that the performance of your retirement account can significantly impact your financial security in retirement. It’s not just about saving money; it’s about growing and optimizing your investments to ensure you have enough to live comfortably when you retire.

In this comprehensive guide, we will walk you through the essential steps to effectively manage your 401k investments. From understanding your risk tolerance and setting investment goals to diversifying your portfolio and making necessary adjustments as you approach retirement, we’ve got you covered.

Throughout this journey, it’s important to remember that managing your 401k investments is an ongoing process. It requires careful consideration, regular monitoring, and occasional adjustments to ensure your investments align with your goals and the ever-changing market conditions.

Without further ado, let’s dive into the world of 401k investments and learn how to take control of your financial future.

Understanding 401k Investments

Before diving into the intricacies of managing your 401k investments, it’s essential to have a solid foundation of understanding about how they work. A 401k is a retirement savings plan that allows employees to contribute a portion of their salary to a tax-advantaged investment account.

One of the primary benefits of a 401k is the ability to save for retirement on a pre-tax basis. This means that the money you contribute to your 401k is deducted from your gross income, reducing your taxable income for the year. As a result, you pay fewer taxes on your current income and have the opportunity for your investments to grow tax-deferred until you withdraw funds from the account, typically during retirement.

Another advantage of a 401k is employer matching contributions. Many employers match a percentage of their employees’ contributions, up to a certain limit. This is essentially free money that can significantly boost your retirement savings. If your employer offers a matching program, it’s important to contribute at least enough to maximize the match to take full advantage of this benefit.

It’s crucial to note that 401k investments are subject to certain restrictions and regulations. For example, there are contribution limits set by the IRS each year. As of 2021, the maximum contribution limit is $19,500 for individuals under the age of 50 and $26,000 for those aged 50 and above (including catch-up contributions).

Additionally, 401k investments are typically limited to a selection of investment options predetermined by the employer. These options may include mutual funds, stocks, bonds, and target-date funds. It’s important to review and understand the investment options available to you, as they can have a significant impact on the growth and performance of your retirement savings.

Understanding the basics of 401k investments is the first step to effectively managing your retirement savings. By taking full advantage of the tax benefits, employer matching contributions, and understanding the investment options available to you, you can position yourself for a financially secure retirement.

Assessing Risk Tolerance

One of the key considerations when managing your 401k investments is determining your risk tolerance. Risk tolerance refers to your ability and willingness to endure fluctuations in the value of your investments. It varies from person to person and plays a crucial role in shaping your investment strategy.

Assessing your risk tolerance is important because it helps you find the right balance between potential returns and the level of risk you are comfortable with. If you take on too much risk and the market experiences a downturn, you may be tempted to panic and sell when prices are low, which can lead to significant losses. On the other hand, if you are too conservative in your investments, you may miss out on potential growth opportunities.

There are several factors to consider when evaluating your risk tolerance. One factor is your investment timeframe. If you have many years until retirement, you may have a higher risk tolerance since you have more time to recover from market downturns. Conversely, if retirement is approaching soon, you may want to adopt a more conservative investment approach to protect your savings from market volatility.

Another factor to consider is your financial situation and goals. If you have a stable income and a substantial emergency fund, you may be more comfortable taking on additional risk in your investments. However, if you have limited savings and a higher need for capital preservation, a more conservative investment strategy may be suitable.

It is also crucial to reflect on your emotional response to market fluctuations. Are you able to stay calm during market downturns, knowing that these fluctuations are a normal part of investing? Or do you find yourself becoming anxious and losing sleep over the performance of your investments? Your ability to handle market volatility without making impulsive decisions is a strong indicator of your risk tolerance.

When assessing your risk tolerance, it is important to be honest with yourself. It is natural to want higher returns, but it’s equally important to consider the potential downsides and your ability to handle them. Remember, there is no one-size-fits-all approach to risk tolerance, and what works for someone else may not work for you.

By understanding your risk tolerance, you can align your investment strategy with your comfort level and long-term goals. It’s important to regularly reassess your risk tolerance as your financial situation and goals may change over time, ensuring that your 401k investments remain appropriate for your needs.

Setting Your Investment Goals

When managing your 401k investments, it is essential to establish clear investment goals. Setting specific goals helps guide your decision-making process and ensures that your investments align with your objectives. Here are a few key factors to consider when setting your investment goals:

1. Retirement Timeline: Start by determining your desired retirement age and the number of years you have until then. This will provide a framework for your investment strategy. If you have a longer timeline, you may have more room for growth-oriented investments, whereas a shorter timeline may require a more conservative approach to preserve your savings.

2. Retirement Lifestyle: Consider the type of lifestyle you envision during retirement. Do you plan to travel extensively, pursue hobbies, or maintain a frugal lifestyle? Understanding your desired retirement lifestyle will help you estimate the income and savings required to support it.

3. Income Needs: Evaluate your current income needs and estimate your future income needs during retirement. Consider factors such as inflation and healthcare costs, as these can significantly impact your retirement expenses. This assessment will help determine the amount of income your investments will need to generate to meet your needs.

4. Risk Tolerance: Reflect on your risk tolerance, as discussed in the previous section. Your investment goals should align with your comfort level for taking on investment risk. If you have a low risk tolerance, your goals may focus more on capital preservation, while those with a higher risk tolerance may aim for greater growth potential.

5. Other Financial Goals: Consider any other financial goals you may have, such as saving for a down payment on a house, paying for your children’s education, or starting a business. Balancing your 401k investments with other financial goals will help you prioritize your allocation of funds.

Once you have considered these factors, you can set specific investment goals. For example, your goal may be to accumulate a specific amount of savings by your desired retirement age or to generate a certain level of annual income after retirement. Make sure your goals are measurable, realistic, and have a specific timeframe attached to them.

Regularly review and reassess your investment goals as your circumstances change. Life events, such as career advancements, marriage, or the birth of a child, can impact your financial situation and necessitate adjustments to your goals.

Remember, setting investment goals is a crucial step in managing your 401k investments. Clear goals provide direction and help you stay focused on your long-term financial objectives.

Diversifying Your Portfolio

When it comes to managing your 401k investments, diversification is a fundamental principle that can help mitigate risk and potentially enhance returns. Diversifying your portfolio involves spreading your investments across different asset classes, industries, and geographical regions to reduce the impact of a single investment’s performance on your overall portfolio.

Why is diversification important? By diversifying, you can protect yourself from the volatility of any one investment or sector. Different assets tend to perform differently under various market conditions, so having a mix of investments can help stabilize your portfolio and minimize potential losses.

There are several ways to achieve diversification in your 401k portfolio:

1. Asset Classes: Invest in a variety of asset classes, such as stocks, bonds, and cash equivalents. Each asset class has different risk and return characteristics, allowing you to balance the potential for growth with stability.

2. Sector Allocation: Allocate your investments across different sectors of the economy, such as technology, healthcare, finance, and energy. This helps to reduce the concentration risk of having too much exposure to a single sector.

3. Geographic Allocation: Consider investing in both domestic and international markets. This diversifies your portfolio across various countries and economies, lessening the impact of any one market’s performance.

4. Investment Styles: Explore different investment styles, such as growth, value, or income-oriented investments. Each style has its own risk-return profile, so diversifying across styles provides a balanced approach to capturing market opportunities.

5. Company Size: Invest in companies of varying sizes, including large-cap, mid-cap, and small-cap stocks. This diversification across market capitalization can help balance the potential for growth and stability in your portfolio.

Remember that diversification does not guarantee profits or protect against losses, but it can help reduce risk and promote more stable long-term returns. Regularly review your portfolio to ensure it remains adequately diversified. As market conditions change, your asset allocation may need to be adjusted to maintain the desired level of diversification.

Analyze your risk tolerance and investment goals when diversifying your portfolio. A financial advisor or investment professional can provide guidance tailored to your specific needs and help you create a well-diversified 401k portfolio.

Choosing the Right Mix of Investments

When managing your 401k investments, selecting the right mix of investments is crucial to achieving your financial goals. The mix, also known as asset allocation, refers to the percentage of your portfolio allocated to different asset classes, such as stocks, bonds, and cash equivalents.

The right asset allocation depends on factors such as your risk tolerance, investment horizon, and financial goals. Here are some considerations to help you choose the right mix of investments:

1. Risk Tolerance: Assess your risk tolerance, as discussed earlier. If you have a higher risk tolerance, you may allocate a larger portion of your portfolio to stocks for potential growth. On the other hand, if you have a lower risk tolerance, you might lean towards a higher allocation to bonds or cash equivalents for stability.

2. Investment Horizon: Consider your investment horizon, which is the length of time until you will need to start tapping into your retirement savings. If you have many years until retirement, you may have a longer investment horizon and can afford to take on more risk. As you approach retirement, it is generally recommended to shift towards a more conservative allocation to protect your accumulated savings.

3. Financial Goals: Align your asset allocation with your financial goals. If your primary objective is growth and maximizing returns, you may have a higher allocation to stocks. However, if your focus is capital preservation or generating current income, you might allocate more to bonds or dividend-paying stocks.

4. Diversification: As discussed in the previous section, diversification is crucial for reducing risk. Ensure that your asset allocation includes a diversified mix of investments across different asset classes, sectors, and geographies. This can help offset the volatility of individual investments and enhance the stability of your portfolio.

5. Market Conditions: Take into account the prevailing market conditions when choosing your mix of investments. Different asset classes may perform differently in various market environments. For example, during periods of economic uncertainty, investors may seek more defensive assets like bonds or allocate to international markets to diversify risk.

6. Consider Professional Advice: If you feel overwhelmed or unsure about selecting the right mix of investments, consider seeking guidance from a financial advisor or investment professional. They can provide personalized recommendations based on your unique circumstances and help you create an asset allocation strategy that aligns with your goals.

Remember that your asset allocation should be regularly reviewed and adjusted as necessary. Over time, your risk tolerance, financial goals, and market conditions may change, requiring modifications to your investment mix. Monitoring and maintaining the appropriate mix of investments is key to successfully managing your 401k portfolio.

Monitoring and Reviewing Your Investments

Managing your 401k investments is an ongoing process that requires regular monitoring and review. By staying proactive and attentive to your investments, you can make informed decisions and take necessary actions to keep your portfolio on track. Here are some key steps to consider when monitoring and reviewing your investments:

1. Review Performance: Regularly review the performance of your investments. Monitor the returns of individual funds or securities within your 401k portfolio. Compare their performance against relevant benchmarks and evaluate whether they are meeting your expectations and investment goals. Identify any underperforming investments that may require attention.

2. Check Asset Allocation: Assess whether your asset allocation is still aligned with your risk tolerance and investment objectives. Review the percentage allocation to different asset classes, such as stocks, bonds, and cash equivalents. Consider rebalancing your portfolio if certain asset classes have deviated significantly from their target weights due to market movements.

3. Stay Informed: Stay updated on market news and trends that could affect your investments. Keep an eye on economic indicators, industry developments, and company-specific news. This information can help you make more informed decisions about managing your 401k portfolio and potentially anticipate market changes.

4. Consider Rebalancing: Rebalancing involves adjusting your portfolio back to its original target asset allocation. As market conditions change, certain investments may outperform or underperform, causing your asset allocation to drift. Regularly evaluate whether rebalancing is necessary to maintain your desired risk level and ensure that your portfolio remains diversified.

5. Review Investment Options: Periodically assess the investment options offered within your 401k plan. Market conditions, fund performance, and changes in the investment landscape may prompt the addition or removal of certain funds. Evaluate whether the available options still meet your investment needs and consider making adjustments if necessary.

6. Consult a Financial Professional: Consider consulting with a financial advisor or investment professional for guidance and advice. They can provide valuable insights and help you navigate complex investment decisions. They can also offer an objective perspective on your portfolio’s performance and assist with rebalancing strategies.

Remember, monitoring and reviewing your investments does not mean making frequent changes or reacting to short-term market fluctuations. It involves a disciplined approach of regular evaluation, aligning with your long-term investment goals, and making strategic adjustments when necessary.

By staying vigilant and proactive in monitoring your 401k investments, you can optimize your portfolio’s performance and make informed decisions to support your financial objectives.

Rebalancing Your Portfolio

Rebalancing your portfolio is an important aspect of managing your 401k investments. It involves adjusting the allocation of your investments back to their original target weights to maintain your desired asset allocation. Rebalancing is necessary because over time, the performance of different investments within your portfolio can cause your asset allocation to deviate from your intended risk level and long-term goals.

Here are some key considerations when it comes to rebalancing your portfolio:

1. Regular Monitoring: Regularly monitor the performance of your investments and the allocation of your portfolio. Set a schedule, such as quarterly or annually, to review and assess your portfolio’s performance. This monitoring will help you identify when it is time to rebalance.

2. Threshold Approach: Consider setting specific thresholds or bands for each asset class’s target allocation. For example, you may decide that if an asset class deviates more than 5% from its target weight, it is time to rebalance. This approach allows for some flexibility and avoids unnecessary rebalancing due to minor fluctuations.

3. Review Risk Tolerance: Periodically reassess your risk tolerance as it may change over time due to various factors such as life events or changes in financial circumstances. Your risk tolerance should align with your asset allocation. If your risk tolerance has changed, you may need to adjust your target asset allocation and rebalance accordingly.

4. Consider Contribution Flows: Take into account your ongoing contributions to your 401k plan. If your contributions are automatically invested in certain funds, it can impact your portfolio’s asset allocation. Factor in the new contributions when determining whether rebalancing is necessary.

5. Sell High, Buy Low: Rebalancing allows you to take advantage of the “sell high, buy low” strategy. As you trim overweighted investments and buy more of underweighted investments, you are essentially selling the assets that have performed well and buying more of the assets that have underperformed. This helps maintain the discipline of selling high and buying low, which can potentially improve your long-term returns.

6. Consider Tax Implications: Be mindful of any tax implications when rebalancing your portfolio, especially if you have taxable accounts outside of the 401k. Selling investments can trigger capital gains taxes. Evaluate the tax consequences and consult with a tax professional if needed to minimize any potential tax impact.

Rebalancing your portfolio is a proactive approach to ensure that your investments remain in line with your desired asset allocation and risk level. It helps to maintain a disciplined investment strategy and prevent your portfolio from becoming overly concentrated or exposed to excessive risk. Regularly reviewing and rebalancing your portfolio can contribute to long-term investment success.

Making Changes as You Approach Retirement

As you approach retirement, managing your 401k investments takes on added significance. The decisions you make during this stage can have a significant impact on your financial security in retirement. Here are some key considerations to keep in mind as you navigate this critical period:

1. Assess Risk Tolerance: Reevaluate your risk tolerance as you near retirement. Many individuals become more risk-averse at this stage in life, as they have less time to recover from market downturns. Consider gradually shifting your asset allocation to include a higher proportion of conservative investments such as bonds and cash equivalents.

2. Capital Preservation: Focus on capital preservation to protect your accumulated savings. As retirement approaches, your investment strategy may shift towards generating income and protecting your retirement nest egg. Prioritize stability and low volatility investments that can provide a steady stream of income to support your expenses.

3. Income Generation: Evaluate the income-generating potential of your investments. Dividend-paying stocks, bonds, and income-focused funds can provide a steady income stream during retirement. Consider a mix of both fixed income and equity investments to balance income generation with potential growth.

4. Account for Withdrawals: Estimate how much income you will need in retirement and determine the withdrawal rate from your 401k. Consider the impact of taxes, healthcare costs, and any other financial obligations. Ensure that your investment strategy aligns with your withdrawal needs to provide a steady income stream while preserving the longevity of your savings.

5. Plan for Longevity: With increased life expectancy, it’s important to plan for a longer retirement horizon. Ensure that your investment strategy accounts for a potentially longer retirement period, taking into consideration inflation and the need for growth to maintain your lifestyle.

6. Review Eligibility for Social Security and Other Benefits: Explore the timing and eligibility requirements for Social Security benefits and any other retirement benefits you may have. Assess how these benefits will factor into your overall retirement income plan and how they may influence your investment strategy.

7. Consult a Financial Advisor: Consider seeking guidance from a financial advisor who specializes in retirement planning. They can help you navigate the complexities of transitioning from accumulation to distribution phase, provide personalized advice tailored to your specific circumstances, and create a comprehensive retirement income strategy.

As retirement approaches, it becomes crucial to make strategic changes to your 401k investments. The goal is to strike a balance between capital preservation, income generation, and potential growth. Regularly reviewing and adjusting your investment strategy as you approach retirement can help ensure a smooth transition into this new phase of your financial journey.

Tax Considerations for 401k Investments

Understanding the tax implications of your 401k investments is critical for effective retirement planning. 401k accounts offer significant tax advantages that can help you maximize your savings. Here are some key tax considerations to keep in mind:

1. Pre-Tax Contributions: One of the main benefits of a 401k is the ability to make pre-tax contributions. This means that the money you contribute to your 401k is deducted from your gross income, reducing your taxable income for the year. As a result, you pay fewer taxes upfront and have the potential for tax-deferred growth within the account until you withdraw the funds in retirement.

2. Tax-Deferred Growth: Any gains or investment income generated within your 401k account are not subject to taxes until you make withdrawals. This tax-deferred growth allows your investments to compound over time, potentially leading to higher returns compared to taxable accounts.

3. Withdrawal Taxes: When you start withdrawing funds from your 401k during retirement, the distributions are subject to income taxes. The withdrawals are treated as ordinary income and added to your taxable income for the year. It’s important to plan your withdrawals strategically to minimize the impact of taxes and coordinate with other sources of income.

4. Penalty for Early Withdrawals: Withdrawals taken from your 401k before the age of 59½ are generally subject to a 10% early withdrawal penalty, in addition to income taxes. There are certain exceptions, such as for disability, substantial medical expenses, or as part of a series of substantially equal periodic payments. Understanding the penalty rules is crucial to avoid unnecessary tax consequences.

5. Roth 401k Option: Some employers offer a Roth 401k option, which allows you to make after-tax contributions. While these contributions do not provide an immediate tax benefit, qualified withdrawals from a Roth 401k, including earnings, are tax-free. Consider the long-term tax advantages of a Roth 401k when deciding between traditional pre-tax contributions and after-tax Roth contributions.

6. Required Minimum Distributions (RMDs): Once you reach the age of 72 (or 70½ if you reached that age before January 1, 2020), you are required to take annual minimum distributions from your traditional 401k account. These RMDs are taxable income and must be withdrawn by the specified deadline each year. Failing to take RMDs can result in significant tax penalties.

7. Tax Planning in Retirement: In retirement, managing your taxable income becomes critical for optimizing your tax situation. Coordinate your 401k withdrawals with other sources of income, such as Social Security or pension payments, to minimize your tax liability. Consider consulting with a tax professional or financial advisor who can help you develop a tax-efficient withdrawal strategy.

It’s important to note that tax laws and regulations surrounding 401k accounts can change, so it’s wise to stay informed and consult with a tax or financial advisor to navigate the complexities of the tax code effectively.

By understanding and leveraging the tax advantages of your 401k investments, you can make informed decisions that maximize your savings and minimize your tax burden, ultimately helping you achieve your retirement goals.

Avoiding Common Mistakes in 401k Investment Management

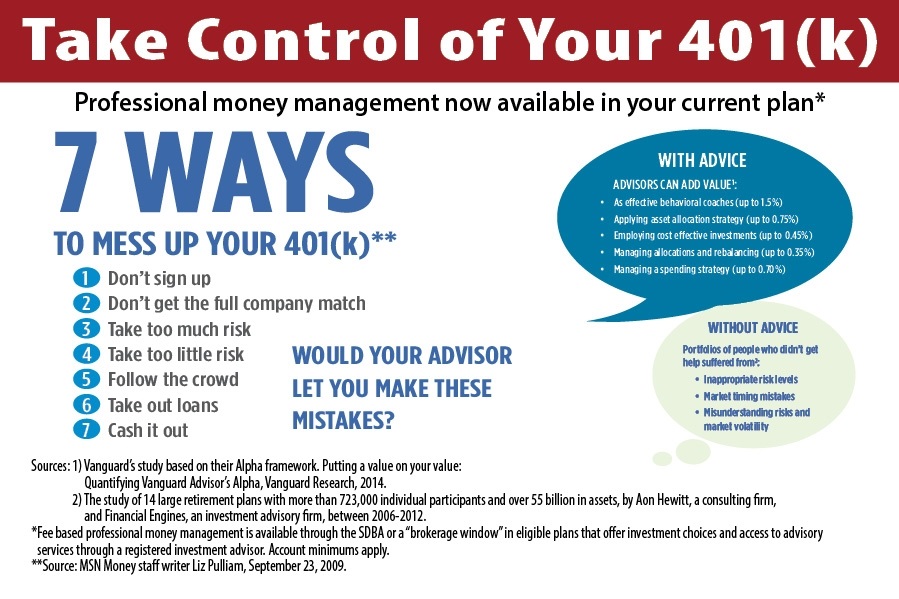

Managing your 401k investments requires careful consideration and strategic decision-making. Unfortunately, many individuals make common mistakes that can hinder the growth of their retirement savings. By being aware of these pitfalls, you can avoid them and set yourself up for long-term investment success. Here are some common mistakes to watch out for:

1. Not Saving Enough: One of the biggest mistakes is not contributing enough to your 401k account. Failing to take full advantage of employer matching contributions or not maximizing the annual contribution limit can significantly impact your retirement savings. Aim to contribute as much as you can afford, increasing your contributions over time to meet your long-term retirement goals.

2. Ignoring Asset Allocation: Neglecting to assess and adjust your asset allocation is another common mistake. Your asset allocation should align with your risk tolerance, investment goals, and time horizon. Regularly review and rebalance your portfolio to ensure it remains in line with your desired allocation. Failure to do so can result in an imbalanced or too risky portfolio.

3. Overreacting to Market Volatility: Letting emotions drive investment decisions during market volatility is a common mistake. It’s important to avoid making knee-jerk reactions based on short-term market fluctuations. Instead, focus on your long-term investment strategy and resist the urge to make impulsive changes that could negatively impact your returns.

4. Chasing Performance: Another mistake is chasing past performance by investing in funds or securities that have recently outperformed the market. Remember that past performance does not guarantee future success. Instead, focus on a diversified, well-balanced portfolio that aligns with your goals and risk tolerance.

5. Forgetting to Reevaluate Investments: Not regularly reviewing and reevaluating your investment choices is a common mistake. Market conditions change, investment options evolve, and your personal circumstances may shift. Stay informed and periodically reassess your investments to ensure they continue to meet your needs and align with your long-term goals.

6. Not Seeking Professional Advice: Failing to seek professional advice is a mistake that many individuals make. A financial advisor or investment professional can provide valuable guidance, especially when it comes to retirement planning and managing your 401k investments. They can help you develop a personalized investment strategy and provide ongoing support to navigate the complexities of the investment landscape.

7. Ignoring Fees: Overlooking the impact of fees can eat into your investment returns over time. Take the time to understand the fees associated with your 401k account and the investment options within it. Compare fees and consider lower-cost options to optimize your investment returns.

By avoiding these common mistakes, you can enhance your 401k investment management and set yourself up for long-term financial success. Remember the importance of consistent contributions, maintaining a well-balanced portfolio, and seeking professional advice when needed. With mindful and informed decision-making, you can maximize your 401k potential and achieve your retirement goals.

Conclusion

Managing your 401k investments is a critical aspect of securing a financially stable retirement. By understanding the fundamentals of 401k investments, assessing your risk tolerance, setting clear investment goals, diversifying your portfolio, and monitoring and reviewing your investments regularly, you can make informed decisions that align with your long-term objectives.

Throughout this guide, we’ve covered various aspects of 401k investment management, including tax considerations and common mistakes to avoid. It’s essential to leverage the tax advantages offered by your 401k account, such as pre-tax contributions and tax-deferred growth, to maximize your savings and minimize your tax liability during retirement.

Additionally, by avoiding common mistakes like not saving enough, neglecting asset allocation, reacting to market volatility, or failing to seek professional advice, you can set yourself up for investment success. Regularly review and adjust your portfolio, stay informed about market trends, and consult with financial advisors or investment professionals when needed to make strategic decisions that support your long-term financial goals.

Remember, managing your 401k investments is an ongoing process. It requires diligence, careful planning, and periodic adjustments to ensure your investments remain aligned with your risk tolerance, investment goals, and evolving market conditions.

By taking control of your 401k investments and making informed decisions, you can secure your financial future and enjoy a comfortable retirement. Start implementing the strategies outlined in this guide today and embark on the path to financial success.