Introduction

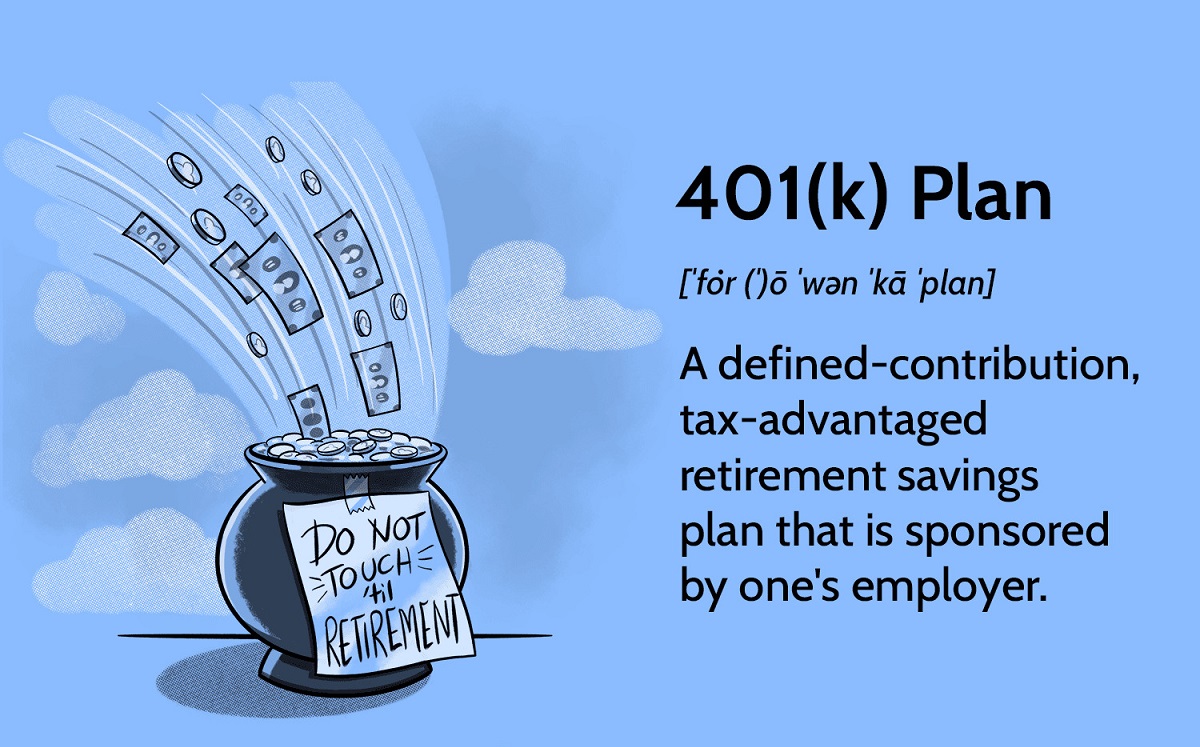

When it comes to managing your 401k investment, you have a choice between using a robo advisor or opting for individual management. A 401k is a retirement savings plan provided by employers, allowing employees to save and invest a portion of their salary before taxes are taken out. It is an essential tool for securing your financial future.

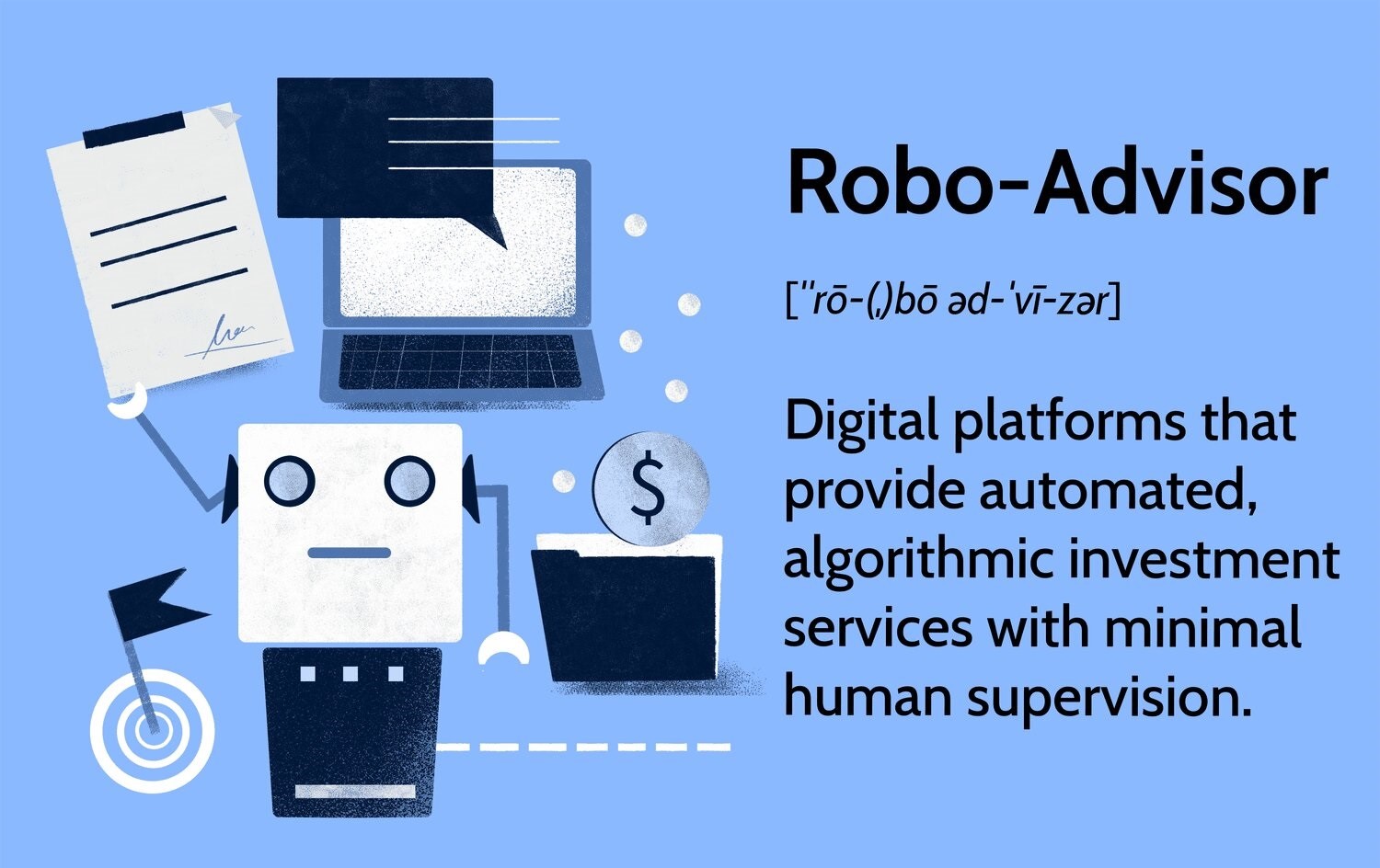

Robo advisors have gained popularity in recent years as an automated and cost-effective way to manage investments, including 401k accounts. These online platforms use algorithms to provide investment advice and portfolio management without the need for human intervention.

On the other hand, individual management involves a more hands-on approach, where individuals make their own investment decisions and actively manage their 401k portfolio. This offers more control and flexibility, but also requires a greater understanding of investment principles and regular monitoring of market trends.

Both robo advisors and individual management have their pros and cons, and choosing the right option depends on various factors, such as your investment knowledge, time commitment, and risk tolerance.

In the following sections, we will delve deeper into the role of robo advisors in 401k investments, assess their advantages and disadvantages, explore the benefits and drawbacks of individual management, and discuss the factors you should consider when deciding between the two.

What is a 401k and Why is it Important?

A 401k is a retirement savings plan that allows employees to contribute a portion of their salary, usually on a pre-tax basis, to save for their future. The contributions made to a 401k account are invested in a variety of assets, such as stocks, bonds, and mutual funds, with the goal of growing the savings over time.

One of the primary advantages of a 401k is the potential for tax-deferred growth. This means that any earnings and capital gains within the account are not subject to taxes until the money is withdrawn during retirement. This can result in significant tax savings over the long term.

Furthermore, many employers offer a matching contribution to employees’ 401k accounts, which can be a valuable perk. For example, an employer may match 50% of the employee’s contributions, up to a certain percentage of their salary. This free money can help accelerate the growth of your retirement savings.

401k plans also provide individuals with the flexibility to choose their investments from a range of options provided by the plan sponsor. This allows employees to tailor their portfolio to their risk tolerance and investment goals.

One of the key benefits of a 401k is the ability to accumulate a substantial nest egg for retirement. Over time, the power of compounding can work in your favor, as your contributions and investment returns generate additional earnings. This can significantly enhance your financial security in retirement.

In summary, a 401k is an important tool for retirement savings, offering tax advantages, potential employer matching contributions, investment flexibility, and the ability to accumulate a substantial retirement nest egg. It is crucial to make informed decisions about your 401k investments to ensure a secure and comfortable retirement.

The Role of a Robo Advisor in 401k Investments

A robo advisor plays a significant role in managing 401k investments by providing automated investment advice and portfolio management services. It employs sophisticated algorithms and technology to analyze various factors and make investment decisions based on individual goals, risk tolerance, and time horizon.

One of the key benefits of using a robo advisor for 401k investments is the convenience and accessibility it offers. Most robo advisors have user-friendly interfaces that allow investors to easily set up and manage their accounts online. This eliminates the need for extensive financial knowledge and makes investing more accessible to individuals with limited investment experience.

Robo advisors also provide a low-cost alternative to traditional financial advisors. By leveraging technology and automation, robo advisors incur fewer administrative costs and pass these savings onto investors. This can result in significant cost reductions compared to traditional investment management services, allowing individuals to keep more of their investment returns.

Furthermore, robo advisors utilize asset allocation strategies that are based on modern portfolio theory and diversification principles. They analyze an investor’s risk profile and investment goals and create a diversified portfolio across various asset classes. This helps to reduce the risk associated with 401k investments and optimize the potential for long-term returns.

In addition to portfolio management, robo advisors provide regular monitoring and rebalancing of investment portfolios. They automatically adjust the allocation of assets based on market conditions and the investor’s risk profile. This ensures that the portfolio stays aligned with the intended investment strategy and maintains the desired level of risk exposure.

It’s important to note that while robo advisors offer convenience and cost-effectiveness, they lack the human element and personalized guidance provided by traditional financial advisors. Robo advisors rely solely on algorithms and historical data, which may not always account for unique circumstances or changing market conditions. Therefore, they may not be suitable for individuals who require a more tailored approach or have complex investment needs.

In summary, the role of a robo advisor in 401k investments is to provide automated investment advice and portfolio management services. They offer convenience, accessibility, cost-effectiveness, and diversified investment strategies. However, they may not offer the personalized guidance of a traditional financial advisor. It’s essential to consider your individual needs and requirements before deciding whether to opt for a robo advisor for your 401k investments.

Advantages of Using a Robo Advisor for 401k Investments

Utilizing a robo advisor for your 401k investments offers several advantages that make it an appealing option for many individuals. Let’s explore some of these advantages:

- Lower Costs: One of the significant advantages of using a robo advisor for 401k investments is the lower costs involved. Robo advisors tend to have lower fees compared to traditional financial advisors. By leveraging automation and technology, robo advisors can provide similar services at a fraction of the cost.

- 24/7 Accessibility: Robo advisors are available round-the-clock, allowing you to monitor and manage your 401k investments at any time. This flexibility is particularly beneficial for individuals with busy schedules or those who prefer to have control over their investments outside of traditional working hours.

- Objective and Unbiased Advice: Robo advisors use algorithms to analyze data and provide investment advice based on objective metrics. Their recommendations are not influenced by personal biases, emotions, or conflicts of interest that can sometimes affect human financial advisors. This can lead to more objective and unbiased investment decisions.

- Portfolio Diversification: Robo advisors excel at creating diversified portfolios tailored to your risk tolerance and investment goals. They use innovative asset allocation strategies and consider a wide range of investment options to optimize portfolio performance and reduce risk. By diversifying your investments, you can potentially enhance returns and mitigate the impact of market volatility.

- Regular Monitoring and Rebalancing: Robo advisors continuously monitor the performance of your 401k investments. They also rebalance your portfolio periodically to maintain the desired asset allocation. This proactive approach ensures that your investments align with your goals and risk tolerance, without requiring you to actively manage the portfolio on your own.

These advantages make using a robo advisor an attractive option for those seeking cost-effective, convenient, and objective management of their 401k investments. However, it’s essential to keep in mind that robo advisors may not provide the personalized attention and customized advice that some individuals require, particularly those with complex financial situations or unique investment goals. Therefore, carefully evaluate your needs and preferences before deciding whether to opt for a robo advisor for your 401k investments.

Disadvantages of Using a Robo Advisor for 401k Investments

While robo advisors offer several advantages for managing 401k investments, there are also some potential disadvantages to consider. Let’s explore these disadvantages:

- Lack of Human Interaction: Robo advisors operate primarily through automated algorithms, which means they lack the human touch. For some individuals, the absence of face-to-face interaction and personalized advice from a human financial advisor may be a drawback. Human advisors can provide valuable insights, guidance, and emotional support during challenging market conditions.

- Difficulty with Complex Financial Situations: Robo advisors are designed to cater to a wide range of investors with basic to moderate investment needs. However, for individuals with more complex financial situations, such as those with multiple income sources, extensive assets, or unique tax considerations, a robo advisor may not have the expertise to address these complexities.

- Limited Customization: While robo advisors offer a certain level of customization, their options may be more limited compared to individual management. Investment decisions are based on algorithms and predefined models, which may not fully account for unique financial goals, preferences, or market conditions. This lack of customization can be a disadvantage for those seeking a more personalized approach.

- Reliance on Historical Data: Robo advisors rely heavily on historical data and algorithms to make investment decisions. While this approach can be effective in normal market conditions, it may not account for unprecedented events or sudden market fluctuations. During these times, a robo advisor’s inability to adapt quickly to changing market conditions can be a disadvantage.

- Limited Human Oversight: While robo advisors provide automated investment management, they lack the consistent human oversight that comes with individual management. Human advisors can provide ongoing monitoring, analysis, and adjustments based on market trends and economic factors that may not be captured by a robo advisor’s algorithms alone.

It’s essential to consider these disadvantages when deciding whether to use a robo advisor for your 401k investments. Evaluate your comfort level with technology-driven advice, your need for personalized guidance, and the complexity of your financial situation. If you require a more tailored approach or have unique circumstances, individual management with a human advisor may be a more suitable option.

Individual Management of 401k Investments

Individual management of 401k investments involves taking direct control of your investment decisions and actively managing your portfolio. Instead of relying on a robo advisor or financial advisor, you make all the investment choices based on your knowledge, research, and risk tolerance.

One of the key advantages of individual management is the level of control it provides. You have the freedom to choose specific investments that align with your preferences, risk appetite, and financial goals. This allows for a more personalized approach, as you can select investments that you believe will perform well based on your own analysis and research.

Individual management also provides the flexibility to react quickly to market changes. When managing your own 401k investments, you can make timely adjustments to your portfolio based on market trends or new investment opportunities. This agility can be particularly advantageous when navigating volatile or rapidly changing market conditions.

Another benefit of individual management is the potential for cost savings. By eliminating the fees associated with robo advisors or financial advisors, you can keep more of your investment returns. This can be especially valuable over the long term, as even small differences in fees can have a significant impact on your overall investment performance.

However, it’s important to acknowledge that individual management also comes with its own set of challenges and potential disadvantages. It requires a solid understanding of investment principles, market dynamics, and risk management strategies. Without proper knowledge and experience, there is a risk of making poor investment decisions or succumbing to emotional biases that can significantly impact your returns.

Additionally, individual management requires a significant time commitment. You must actively monitor your investments, stay up-to-date with market news, and regularly review and rebalance your portfolio. This can be time-consuming, especially for individuals with busy schedules or limited investment knowledge.

Furthermore, individual management may expose you to behavioral biases, such as overconfidence or herding mentality, which can negatively affect your investment decisions. Without the guidance and objective perspective of a financial advisor or robo advisor, it’s important to be aware of these biases and actively work to mitigate their influence.

In summary, individual management of 401k investments offers control, flexibility, and potential cost savings. However, it requires a deep understanding of investment principles, time commitment, and the ability to manage behavioral biases. Consider your level of investment knowledge, available time, and comfort with taking sole responsibility for your investment decisions before opting for individual management.

Advantages of Individual Management for 401k Investments

Individual management of 401k investments offers several advantages for those who prefer to take direct control of their investment decisions. Let’s explore some of these advantages:

- Greater Control and Personalization: With individual management, you have the freedom to make investment choices that align with your specific preferences, goals, and risk tolerance. You are not limited to a predefined investment strategy or model, allowing for a more personalized approach to your 401k investments.

- Flexibility and Agility: Managing your own 401k investments allows you to react quickly to market changes and take advantage of new investment opportunities. You can make timely adjustments to your portfolio based on market trends or economic indicators without relying on a robo advisor or financial advisor, which can potentially lead to better investment outcomes.

- Cost Savings: By eliminating the fees associated with robo advisors or financial advisors, individual management can lead to significant cost savings. Even small differences in fees can accumulate over time, allowing you to keep a larger portion of your investment returns.

- Education and Empowerment: Taking control of your 401k investments through individual management provides an opportunity for self-education and empowerment. You can develop a deeper understanding of investment principles, explore different asset classes, and enhance your financial knowledge, which can be valuable not only for your 401k but also for other investment endeavors.

- Tailored Risk Management: Individual management allows for customized risk management strategies. You can adjust the level of risk in your portfolio based on your risk tolerance and financial goals. This level of control can provide peace of mind and help align your investments with your desired risk-reward profile.

These advantages make individual management an attractive option for individuals who have a solid understanding of investment principles, time to dedicate to managing their portfolio, and the desire for greater control and personalization. However, it’s important to consider the potential challenges and pitfalls associated with individual management, such as the need for extensive investment knowledge, the time commitment required, and the potential for behavioral biases to influence decision-making. Evaluating your own capabilities and preferences is crucial in determining whether individual management is the right choice for your 401k investments.

Disadvantages of Individual Management for 401k Investments

While individual management of 401k investments offers certain advantages, there are also potential disadvantages to consider. Let’s explore some of these disadvantages:

- Limited Expertise: Managing your own 401k investments requires a deep understanding of investment principles, market trends, and risk management strategies. Without the expertise of a financial advisor, there is a risk of making poor investment decisions or being uninformed about potential risks and opportunities.

- Time Commitment: Successfully managing your 401k investments takes time and effort. You need to stay up-to-date with market news, research investment options, and regularly review and adjust your portfolio. This time commitment can be challenging for individuals with demanding schedules or those who are not interested in dedicating significant time to investment management.

- Emotional Biases: Individual management can expose you to behavioral biases, such as fear, greed, or overconfidence. These biases can cloud your judgment and lead to irrational investment decisions. Without the guidance and objective perspective of a financial advisor, it’s crucial to be aware of these biases and take steps to mitigate their impact.

- Lack of Diversification: Without expert guidance, there is a risk of inadequate diversification in your 401k portfolio. A lack of diversification can leave you vulnerable to the performance of a few individual investments or sectors, increasing the overall risk of your portfolio.

- Missing Out on Professional Advice: Individual management means forgoing the experience and knowledge of financial advisors who specialize in retirement planning and investment management. A financial advisor can provide valuable insights, offer personalized advice, and help you navigate complex financial situations.

It’s important to carefully consider these disadvantages when deciding whether individual management is suitable for your 401k investments. Assess your level of investment knowledge, available time, and comfort with taking responsibility for investment decisions. If you lack the expertise, time commitment, or desire for personalized advice, it may be more beneficial to seek the assistance of a financial advisor or utilize a robo advisor for your 401k investments.

Factors to Consider When Choosing Between a Robo Advisor and Individual Management

Choosing between a robo advisor and individual management for your 401k investments requires careful consideration of various factors. Let’s explore some key factors to help you make an informed decision:

- Investment Knowledge and Expertise: Assess your level of investment knowledge and expertise. If you have a strong understanding of investment principles, market trends, and risk management strategies, you may feel confident in managing your own 401k investments. However, if you lack expertise or are not interested in learning about investment management, a robo advisor or financial advisor may be a better option.

- Time Commitment: Consider the time commitment required for individual management. Managing your own 401k investments involves staying updated with market news, researching investment options, and regularly monitoring your portfolio. If you have the time and inclination to dedicate to investment management, individual management could be a good fit. Otherwise, a robo advisor offers the convenience of automated management with minimal time commitment.

- Cost Considerations: Evaluate the fees associated with both options. Robo advisors typically have lower fees compared to traditional financial advisors. If cost savings are important to you, using a robo advisor can help minimize expenses. On the other hand, if you prefer a personalized approach and are willing to pay for expert guidance, individual management or a financial advisor may be worth the cost.

- Need for Personalized Advice: Consider the level of personalized advice you require. If you have complex financial situations, unique goals, or specific investment preferences, individual management or working with a financial advisor offers more personalized guidance. Robo advisors provide more generalized advice based on algorithms, which may not account for your unique circumstances.

- Emotional Bias and Behavioral Considerations: Reflect on your ability to make rational investment decisions and control emotional biases. If you are prone to making impulsive decisions or are influenced by market fluctuations, using a robo advisor can provide a more objective approach, free from emotional biases. However, if you are confident in your ability to make disciplined decisions, individual management may be suitable.

It’s important to evaluate these factors and weigh your personal preferences, financial goals, and risk tolerance when deciding between a robo advisor and individual management for your 401k investments. Consider seeking advice from a financial professional to help assess your specific situation and determine the best approach for your needs.

Conclusion

When it comes to managing your 401k investments, you have the choice between using a robo advisor or opting for individual management. Each approach has its own advantages and disadvantages, and the decision should be based on your individual circumstances, preferences, and financial goals.

A robo advisor offers convenience, lower costs, diversified portfolios, and automated management. It is well-suited for individuals who are looking for a hands-off approach, have limited investment knowledge, and prefer a cost-effective solution. However, robo advisors may lack the personalization and human touch offered by financial advisors, and algorithmic decisions may not account for unique circumstances or unprecedented events.

Individual management, on the other hand, provides greater control, flexibility, and potential cost savings. It is suitable for individuals who have the time, expertise, and desire to actively manage their 401k investments. However, it requires investment knowledge, ongoing monitoring, and the ability to mitigate emotional biases that can impact decision-making.

When deciding between a robo advisor and individual management, consider factors such as your investment knowledge, time commitment, need for personalized advice, emotional biases, and cost considerations. It may also be beneficial to seek guidance from a financial professional who can help evaluate your specific situation and provide tailored advice.

Ultimately, the most effective approach may be a combination of both methods. Starting with a robo advisor to automate the investment process and gain experience can be a good first step. As your knowledge and confidence grow, you can gradually transition to individual management while leveraging the insights and advice provided by financial professionals.

Remember, the decision regarding the management of your 401k investments should align with your goals for retirement and financial well-being. Regularly review and assess your investment strategy to ensure it remains in line with your changing needs and market conditions. By making informed decisions and continuously monitoring your investments, you can work towards building a secure and prosperous retirement.