Introduction

Welcome to the world of robo-advisors, where technology meets investment management. Investing can be a daunting task, especially for those who are new to the financial markets. However, with the rise of robo-advisors, investing has become more accessible, convenient, and cost-effective for individuals of all backgrounds.

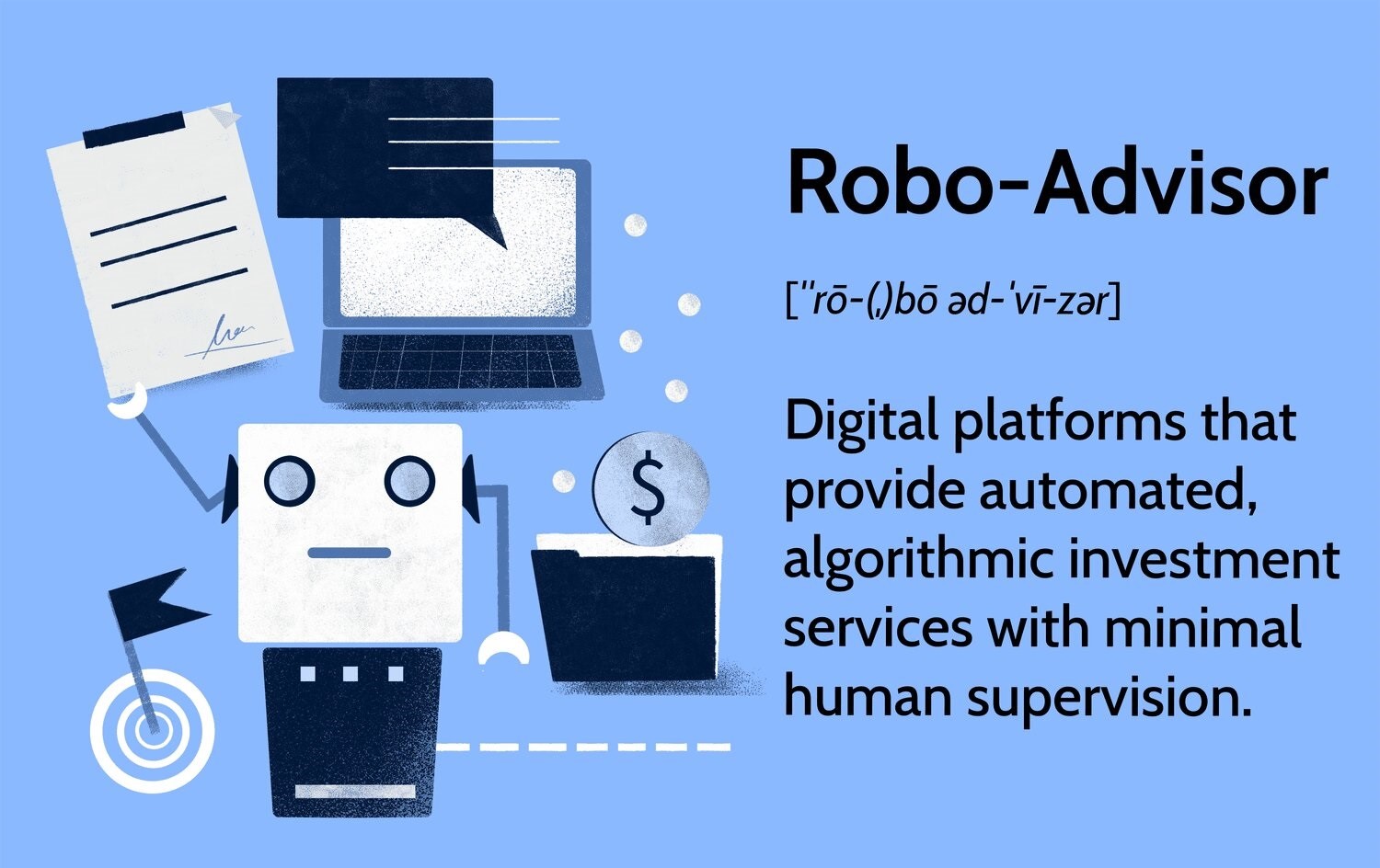

So, what exactly is a robo-advisor? Simply put, a robo-advisor is an online platform that uses advanced algorithms to automate investment decisions. These algorithms analyze various factors, such as risk tolerance, financial goals, time horizon, and market conditions, to determine the optimal portfolio allocation for an investor. This automated approach eliminates the need for traditional financial advisors and provides a streamlined investment experience.

Robo-advisors have gained immense popularity in recent years, revolutionizing the way people invest. By leveraging technology and machine learning capabilities, these platforms can offer personalized investment portfolios at a fraction of the cost typically charged by human financial advisors.

The purpose of this article is to delve into the inner workings of robo-advisors and explore how they determine the allocation of your investments. We will discuss the role of Modern Portfolio Theory in guiding investment decisions and explore other factors that robo-advisors consider, such as risk tolerance, time horizon, and financial goals. Additionally, we will touch on the importance of diversification, the role of algorithms and machine learning, and the difference between active and passive investing strategies. Lastly, we will address the topic of portfolio rebalancing and tax considerations.

By the end of this article, you will have a clear understanding of how robo-advisors work and how they make investment decisions on your behalf. Whether you are a beginner investor or looking to switch from traditional financial advisors to a robo-advisor, this knowledge will empower you to make informed decisions and take control of your financial future.

What is a Robo-Advisor?

In the world of finance, robo-advisors have emerged as a game-changer, revolutionizing the investment landscape. A robo-advisor is an online platform that provides automated investment services, combining technology with financial expertise to offer personalized and cost-effective investment management.

Unlike traditional financial advisors who offer personalized advice and portfolio recommendations, robo-advisors rely on algorithms and sophisticated software to analyze and manage investments. These algorithms consider a variety of factors, including an investor’s risk tolerance, financial goals, time horizon, and market conditions, to create and maintain a diversified portfolio.

Robo-advisors have democratized investing by making it more accessible to individuals of all backgrounds. The low minimum investment requirements and reduced fees offered by most robo-advisors have eliminated many of the barriers to entry that once limited smaller investors from accessing professional investment services.

Another defining characteristic of robo-advisors is their user-friendly and intuitive platforms. Investing no longer requires a deep understanding of financial markets or complex investment strategies. Robo-advisor platforms are designed to simplify the investment process, allowing users to easily set up an account, answer a few questions about their financial situation and investment preferences, and receive a recommended portfolio that aligns with their goals.

These portfolios are typically constructed using Modern Portfolio Theory (MPT), a framework developed by Nobel Laureate Harry Markowitz. MPT emphasizes the importance of diversification and the benefits of combining assets with different risk and return characteristics to maximize returns for a given level of risk.

Furthermore, robo-advisors typically offer a range of investment options tailored to individual investor preferences. These options may include socially responsible investing, thematic investing, or specific asset class preferences, providing investors with the ability to align their investment strategy with their personal values or interests.

With the rise of robo-advisors, investors now have more control over their investments. They can monitor their portfolio performance, track their progress towards their financial goals, and make adjustments as necessary, all through the convenience of a user-friendly online platform or mobile app.

In summary, robo-advisors have reshaped the investment landscape by providing accessible, cost-effective, and personalized investment management services. Through the power of algorithms and technology, robo-advisors empower individuals to take control of their financial futures and make informed investment decisions.

The Role of Modern Portfolio Theory

Modern Portfolio Theory (MPT) plays a crucial role in guiding the investment decisions made by robo-advisors. Developed by Nobel Laureate Harry Markowitz in the 1950s, MPT provides a framework for constructing portfolios that aim to optimize returns while minimizing risk.

At the core of MPT is the concept of diversification. MPT recognizes that different assets have varying levels of risk and return, and by combining assets with different characteristics, it is possible to create a balanced portfolio that can generate higher returns for a given level of risk.

Robo-advisors employ MPT principles when constructing investment portfolios for their clients. The algorithms consider the historical performance, volatility, and correlation of different asset classes and securities to create diversified portfolios that are aligned with an investor’s risk tolerance and financial goals.

One of the key benefits of MPT is its ability to optimize risk-adjusted returns. By spreading investments across different asset classes such as stocks, bonds, and alternative investments, robo-advisors aim to reduce the impact of any single investment’s performance on the overall portfolio. This diversification helps to mitigate risk and protect against significant losses that might occur in any particular asset class.

Furthermore, MPT recognizes that each investor has different risk preferences. Some individuals may be willing to take on higher levels of risk in the pursuit of potentially higher returns, while others may have a more conservative approach and prioritize capital preservation. Robo-advisors consider an individual’s risk tolerance through a series of questions that assess their comfort level with market fluctuations and losses. This information is used to create a portfolio that aligns with the investor’s risk profile.

Another important aspect of MPT is the concept of efficient frontiers. This theory plots different combinations of asset classes and provides a range of portfolios that offer the highest return for a given level of risk, or the lowest risk for a given level of return. Robo-advisors take advantage of simulated analyses to determine the optimal allocation of assets that can potentially maximize returns while minimizing risk within an individual’s risk tolerance.

In summary, the role of Modern Portfolio Theory in the world of robo-advisors is crucial. It provides the foundation for constructing diversified portfolios that aim to optimize returns and minimize risk based on an individual’s risk tolerance and financial goals. By leveraging the principles of MPT, robo-advisors can offer personalized and efficient investment solutions to investors of all backgrounds.

Determining Your Risk Tolerance

Risk tolerance is a key factor in the investment process and plays a significant role in determining the allocation of your investments by a robo-advisor. It refers to your ability and willingness to withstand fluctuations or potential losses in the value of your investments. Understanding your risk tolerance is essential for creating an investment portfolio that aligns with your comfort level and financial goals.

Robo-advisors employ various methods to assess an individual’s risk tolerance. Typically, they use a series of questions or risk assessment surveys to determine an investor’s risk profile. These questions may inquire about your investment knowledge, financial goals, time horizon, and willingness to accept losses. By analyzing your responses, robo-advisors can have a better understanding of your risk appetite and construct a suitable portfolio.

It is important to note that risk tolerance is subjective and varies from person to person. Some individuals may have a higher risk tolerance, being comfortable with potentially higher volatility, while others may have a lower risk tolerance and prioritize capital preservation over maximizing returns.

Based on your risk profile, robo-advisors will recommend an appropriate asset allocation for your portfolio. If you have a higher risk tolerance, a larger allocation to stocks or riskier assets like emerging market securities may be suggested to potentially achieve higher returns. On the other hand, if you have a lower risk tolerance, a more conservative asset allocation with a higher proportion of bonds or cash may be recommended to reduce the potential for significant losses.

Moreover, robo-advisors consider your risk tolerance in conjunction with your financial goals and time horizon. If you have a longer time horizon and can afford to take more risk, a robo-advisor might suggest a more aggressive portfolio that aims for higher returns over the long term. Conversely, if your financial goals are more short-term or if you have a lower risk tolerance, a more conservative approach with a focus on capital preservation might be recommended.

It is worth noting that risk tolerance is not static and may change over time due to various factors such as changes in financial circumstances, market conditions, or personal preferences. Therefore, it is important to periodically reassess your risk tolerance and adjust your investment portfolio accordingly.

In summary, determining your risk tolerance is a critical step in the investment process, and robo-advisors use various methods to assess your risk profile. By understanding your risk tolerance, robo-advisors can recommend an appropriate asset allocation that aligns with your comfort level, financial goals, and time horizon, providing you with a personalized investment solution.

Understanding Time Horizon

In investment management, your time horizon refers to the length of time you plan to invest before needing to access your funds. It is an important factor that robo-advisors consider when determining the allocation of your investments. Understanding your time horizon allows robo-advisors to recommend appropriate investment strategies that align with your specific goals.

The time horizon can vary from person to person, depending on individual circumstances and financial goals. Some investors may have a long-term time horizon, such as saving for retirement that is decades away, while others may have a short-term time horizon, such as saving for a down payment on a home within the next few years.

If you have a longer time horizon, robo-advisors may recommend a more aggressive investment approach that includes a higher allocation to growth-oriented assets such as stocks or equity funds. This strategy takes advantage of the potential for long-term capital appreciation and allows for the ability to weather shorter-term market fluctuations.

Conversely, if you have a shorter time horizon, robo-advisors may suggest a more conservative investment approach. This strategy focuses on preserving capital and minimizing the impact of short-term market volatility. A larger allocation to fixed-income investments like bonds or cash equivalents may be recommended for shorter-term financial goals.

Robo-advisors take into consideration your time horizon along with other factors like risk tolerance and financial goals to create a tailored asset allocation. They understand that while risk tolerance determines how much risk you are willing to take, the time horizon influences how long you can ride out potential market downturns and benefit from the potential growth of your investments.

It is important to review and reassess your time horizon periodically, especially as major life events or goals evolve. As you approach your financial goals or retirement, the time horizon may become shorter, and a more conservative investment approach may be recommended to safeguard your accumulated savings. On the other hand, if you have a longer time horizon due to a change in circumstances, robo-advisors may suggest a more aggressive investment strategy to capitalize on potential long-term growth.

In summary, understanding your time horizon is crucial in managing your investments effectively. Robo-advisors consider your time horizon along with other key factors to recommend an appropriate asset allocation that matches your goals and risk tolerance. By aligning your investments with your time horizon, you can optimize the potential for growth and achieve your financial objectives.

Assessing Your Financial Goals

One of the fundamental steps in the investment process is assessing your financial goals. These goals represent the desired outcomes you wish to achieve through your investments, such as saving for retirement, purchasing a home, funding education, or building a nest egg for a comfortable lifestyle.

When it comes to robo-advisors, assessing your financial goals is a crucial factor that influences the allocation of your investments. By understanding your goals, robo-advisors can create a customized investment strategy that aims to help you achieve those specific objectives.

To assess your financial goals, robo-advisors typically ask a series of questions to gather information about your personal circumstances, preferences, and aspirations. These questions may pertain to your target amount, time frame, and the level of risk you are willing to undertake to achieve your goals.

Based on your responses, robo-advisors can suggest an appropriate investment approach that aligns with your financial goals. For instance, if your goal is long-term wealth accumulation, robo-advisors may recommend a more growth-oriented investment strategy with a higher allocation to equities or diversified index funds known for their potential for higher returns over an extended period.

Conversely, if your goal is more short-term in nature, such as purchasing a home in the next few years or funding education expenses, robo-advisors may suggest a more conservative investment strategy. This could involve a larger allocation to fixed-income investments, such as bonds or money market funds, to provide stability and liquidity when you need the funds for your specific goal.

It’s worth noting that robo-advisors not only consider your financial goals but also take into account other factors such as your risk tolerance, time horizon, and market conditions. By considering these various aspects, robo-advisors can develop a diversified investment portfolio tailored to your specific circumstances and aspirations.

Regularly reviewing and reassessing your financial goals is important, as goals may change over time. For example, as you approach retirement, your goal may shift from accumulating wealth to preserving capital and generating income. Robo-advisors can help you adjust your investment strategy to match your evolving goals and ensure you stay on track throughout your financial journey.

In summary, assessing your financial goals is a vital step in the investment process, and robo-advisors use this information to create a customized investment approach. By considering your goals alongside other factors, robo-advisors can provide personalized advice and an appropriate asset allocation that aligns with your objectives, helping you navigate the path towards financial success.

Diversification and Asset Allocation

Diversification and asset allocation are key principles that robo-advisors utilize when determining the allocation of your investments. These strategies aim to manage risk and optimize returns by spreading investments across different asset classes, sectors, and geographical regions.

Robo-advisors recognize that diversification is an essential component of a well-constructed investment portfolio. It helps reduce the potential impact of any single investment on the overall portfolio’s performance. By diversifying, you can potentially mitigate risk and improve the likelihood of achieving long-term financial goals.

Asset allocation refers to the division of investment funds across different asset classes, such as stocks, bonds, cash equivalents, and alternative investments. The allocation is customized to match your risk tolerance, time horizon, and financial goals.

Robo-advisors use algorithms and mathematical models to analyze historical performance and correlations between different asset classes. Based on this analysis, they determine an optimal asset allocation that seeks to maximize returns while minimizing risk within your specified risk tolerance.

For example, if you have a higher risk tolerance, robo-advisors may recommend a higher allocation to stocks, which historically have the potential for higher returns but also come with greater volatility. On the other hand, if you have a lower risk tolerance, a more conservative asset allocation with a larger proportion of bonds may be suggested to reduce the potential for significant losses.

Additionally, robo-advisors consider the benefits of geographic and sector diversification. By investing in a variety of countries and industries, robo-advisors aim to reduce the risk associated with any one specific region or sector experiencing economic or market fluctuations.

One of the advantages of using robo-advisors for diversification and asset allocation is that these platforms can provide access to a wide range of investment options. They often offer portfolios consisting of exchange-traded funds (ETFs) or mutual funds that provide diversification within each asset class. These investment vehicles hold a basket of underlying securities, providing exposure to a broad range of companies or bonds.

Another advantage is that robo-advisors continually monitor and rebalance portfolios to maintain the desired asset allocation. As market conditions change, certain asset classes may outperform or underperform relative to others, resulting in a deviation from the target allocation. Robo-advisors automatically rebalance the portfolio by selling or buying assets to bring it back to the intended allocation, ensuring that your investments stay on track.

In summary, diversification and asset allocation are essential strategies employed by robo-advisors to manage risk and optimize returns. By spreading investments across various asset classes and continuously rebalancing the portfolio, robo-advisors aim to create a well-diversified investment solution tailored to your risk tolerance, time horizon, and financial goals.

The Role of Algorithms and Machine Learning

Algorithms and machine learning algorithms play a vital role in the operations of robo-advisors. These advanced technologies enable robo-advisors to analyze vast amounts of data, make data-driven decisions, and provide personalized investment advice to their clients.

Robo-advisors leverage algorithms to automate the investment process. These algorithms consider a wide range of factors, including an investor’s risk tolerance, financial goals, time horizon, market conditions, and historical performance data. By combining and analyzing these data points, robo-advisors can create customized investment portfolios that align with an individual’s unique circumstances.

The algorithms incorporated by robo-advisors employ mathematical models, statistical analysis, and optimization techniques to determine the optimal asset allocation for a given investor. These models aim to maximize returns while managing risk within the specified risk tolerance of the investor.

Machine learning is also utilized by robo-advisors to continuously improve their investment strategies. Machine learning algorithms analyze historical data on market trends, asset performances, and other variables to identify patterns and make predictions about future market behavior. This helps robo-advisors make more accurate investment decisions and adapt to changing market conditions.

As machine learning algorithms learn from new data and investor behavior, they can refine their recommendations over time. This adaptability allows robo-advisors to provide personalized and dynamic investment advice that aligns with an investor’s evolving needs and goals.

Another advantage of incorporating algorithms and machine learning is the ability to automate portfolio rebalancing. As market conditions and asset performances fluctuate, the asset allocation of a portfolio may deviate from the desired target. Robo-advisors use automated algorithms to trigger the rebalancing process, ensuring that the portfolio is brought back to its intended allocation. This helps maintain the desired risk and return characteristics of the portfolio.

Furthermore, robo-advisors leverage algorithms to optimize tax efficiency. Through tax-loss harvesting strategies, they can identify and sell securities that have experienced losses to offset taxable gains, potentially reducing the investor’s tax liability. This automated tax optimization can significantly enhance overall investment returns.

Overall, the role of algorithms and machine learning in robo-advisors is to provide efficient and personalized investment management. By leveraging these advanced technologies, robo-advisors can analyze data, identify patterns, and make informed investment decisions that align with an investor’s risk profile, financial goals, and market conditions. The use of algorithms and machine learning enables robo-advisors to offer cost-effective and technology-driven investment solutions to a broad range of investors.

Active vs Passive Investing Strategies

When it comes to investing, there are two primary strategies: active and passive investing. Robo-advisors offer both options, allowing investors to choose a strategy that aligns with their investment preferences and goals.

Active investing is characterized by a hands-on approach, where portfolio managers or fund managers actively buy, sell, and trade securities in an attempt to outperform the market. This strategy relies on research, analysis, and the expertise of the investment professionals to identify undervalued securities or market trends.

Passive investing, on the other hand, takes a more passive approach by aiming to replicate the performance of a specific market index or benchmark. This strategy involves investing in index funds or exchange-traded funds (ETFs) that track the performance of a particular index, such as the S&P 500. Passive investors believe that it is difficult to consistently beat the market, so they seek to capture the broad market returns instead.

Robo-advisors offer both active and passive investment strategies based on an investor’s preferences and risk tolerance. For investors seeking active strategies, robo-advisors may provide access to professionally managed portfolios or mutual funds that actively pick and choose securities based on specific investment objectives or criteria.

Passive investment strategies are also popular among robo-advisors due to their cost-effectiveness and simplicity. Robo-advisors often recommend portfolios consisting of low-cost index funds or ETFs that offer broad market exposure and aim to replicate the performance of a specific market index. These passive strategies generally have lower expense ratios compared to actively managed funds.

It is worth noting that passive investing does not mean complete inaction. Portfolio rebalancing, tax optimization, and periodic review of the investment strategy are commonly implemented by robo-advisors to ensure the portfolio remains aligned with an investor’s objectives.

Both active and passive investing strategies have their advantages and disadvantages. Active investing can potentially offer higher returns if successful in outperforming the market, but it comes with higher costs and requires diligent research and monitoring. Passive investing, on the other hand, tends to have lower costs, greater diversification, and a focus on long-term market trends rather than short-term market fluctuations.

Ultimately, the choice between active and passive investing strategies depends on an investor’s risk tolerance, investment goals, and confidence in the ability to beat the market. Robo-advisors provide transparency and flexibility in selecting the appropriate strategy, allowing investors to take advantage of either approach.

In summary, robo-advisors offer both active and passive investment strategies to cater to the diverse needs and preferences of investors. These strategies differ in their level of involvement, costs, and beliefs about the ability to outperform the market. By providing access to both strategies, robo-advisors empower investors to choose an approach that aligns with their investment philosophy and objectives.

Rebalancing Your Portfolio

Portfolio rebalancing is a critical aspect of investment management that robo-advisors handle efficiently and automatically. Rebalancing involves adjusting the allocation of assets in a portfolio to bring it back in line with the target asset allocation initially set by the investor.

Over time, the performance of different asset classes can vary. As a result, the percentages of various assets in a portfolio can deviate from the desired allocation. Rebalancing ensures that the portfolio maintains the intended risk and return characteristics.

Robo-advisors use automated algorithms to periodically review the asset allocation of a portfolio and trigger rebalancing when deviations from the target allocation exceed predefined thresholds. For example, if the target allocation for stocks is 60%, but due to market movements, it exceeds 65%, the robo-advisor will automatically sell a portion of the stocks and buy other assets to bring the allocation back to the desired level.

Rebalancing provides several benefits to investors. Firstly, it mitigates the potential risks associated with an overly concentrated portfolio. By periodically rebalancing, investors ensure that their investments are not overly weighted towards a specific asset class that may be experiencing significant market fluctuations.

Secondly, rebalancing helps investors to “sell high and buy low” by following a disciplined approach. As certain asset classes outperform others, rebalancing forces investors to sell some of the appreciated assets and purchase the underperforming assets at lower prices. This approach helps to maintain a disciplined investment strategy and potentially take advantage of market volatility.

Thirdly, rebalancing ensures that the portfolio remains aligned with an investor’s risk tolerance and financial goals. As an investor’s circumstances and objectives change over time, rebalancing allows the portfolio to adapt accordingly. For example, if an investor has a shorter time horizon and wants to reduce risk, the robo-advisor can rebalance the portfolio with a higher allocation to more conservative assets.

One additional benefit of using a robo-advisor for portfolio rebalancing is the ability to efficiently execute transactions at a lower cost. Robo-advisors typically use low-cost index funds or ETFs for investment strategies, which have lower expense ratios compared to actively managed funds. This helps to minimize costs associated with buying and selling securities during rebalancing.

It is essential to note that the frequency of rebalancing depends on various factors, such as an investor’s risk tolerance, investment goals, and market conditions. Some robo-advisors offer automatic rebalancing on a predetermined schedule, while others rebalance opportunistically based on specific market triggers or percentage deviations from the target allocation.

In summary, portfolio rebalancing is a crucial practice in investment management, and robo-advisors automate this process to maintain the desired asset allocation. Rebalancing provides benefits such as risk management, disciplined investing, and alignment with an investor’s changing circumstances. By leveraging algorithms and cost-effective investment vehicles, robo-advisors offer efficient and seamless portfolio rebalancing for investors of all backgrounds.

Tax Considerations

Tax implications are an important consideration when it comes to investing, and robo-advisors take into account various tax considerations to optimize investment outcomes for their clients. By utilizing intelligent algorithms and automated tax optimization strategies, robo-advisors aim to minimize the tax burden on investment portfolios.

One common tax optimization strategy employed by robo-advisors is tax-loss harvesting. This strategy involves strategically selling investments that have experienced losses to offset capital gains and potentially reduce an investor’s tax liability. By realizing losses, investors can offset gains and lower their tax bill, ultimately enhancing overall portfolio returns.

Robo-advisors utilize algorithms and automated systems to identify securities that have declined in value and may be suitable candidates for tax-loss harvesting. When such opportunities arise, the robo-advisor will automatically sell the securities and replace them with similar investments to maintain the asset allocation and market exposure of the portfolio.

Another aspect of tax optimization involves asset location. Depending on the type of accounts an investor holds, such as taxable accounts, individual retirement accounts (IRAs), or 401(k) plans, robo-advisors will strategically allocate investments across these accounts to maximize tax efficiency. For example, tax-inefficient assets that generate interest income may be placed in tax-advantaged accounts, whereas tax-efficient assets such as index funds may be held in taxable accounts.

Robo-advisors also take into account the impact of capital gains taxes when managing investment portfolios. By monitoring an investor’s holding period and capital gains, robo-advisors can recommend appropriate actions to mitigate tax implications. They may suggest holding investments for more than one year to benefit from long-term capital gains rates, which are typically lower than short-term capital gains rates.

It is important to note that tax optimization strategies employed by robo-advisors should align with an investor’s specific tax situation and consider any applicable tax laws and regulations. It is always recommended to consult with a tax advisor to ensure compliance with tax rules and regulations.

Furthermore, robo-advisors provide investors with access to tax documents and reports, making it easier to prepare tax returns and accurately report investment income and capital gains. These platforms often generate detailed tax statements that summarize the tax impact of various transactions and provide information necessary for filing tax returns.

While tax optimization strategies can play a significant role in enhancing investment returns, it is important to recognize that taxes should not be the sole determinant of investment decisions. Investment strategies should align with an investor’s risk tolerance, financial goals, and overall investment objectives.

In summary, robo-advisors consider various tax considerations and employ algorithms to optimize tax efficiency. Through tax-loss harvesting, asset location strategies, and mindful management of capital gains taxes, robo-advisors aim to reduce tax liability and enhance overall investment returns. It is important for investors to understand the tax implications of their investments and consult with a tax advisor to ensure compliance with tax laws and regulations.

Conclusion

Robo-advisors have revolutionized the investment landscape by leveraging technology and algorithms to provide accessible, cost-effective, and personalized investment management. These platforms offer a range of services, from determining risk tolerance to rebalancing portfolios, all while considering factors such as financial goals, time horizon, and tax implications.

Through the use of algorithms and machine learning, robo-advisors can analyze data, make informed investment decisions, and continuously improve their strategies. They have democratized investing by offering low minimum investment requirements and providing access to diversified portfolios previously only available to high-net-worth individuals.

Robo-advisors offer both active and passive investment strategies, allowing investors to choose an approach that aligns with their investment preferences and goals. They understand the significance of diversification and asset allocation in managing risk and optimizing returns, and employ techniques such as tax optimization and periodic portfolio rebalancing to ensure the portfolio remains on track.

It is crucial for investors to understand their risk tolerance, financial goals, and time horizon in order to make informed decisions. By partnering with a robo-advisor, investors gain access to sophisticated investment management tools and technologies that guide them towards achieving their financial objectives.

However, while robo-advisors offer numerous benefits, it is important to recognize that they are not a replacement for human financial advisors. Some investors may still prefer the personalized guidance and expertise that human advisors provide, especially in complex financial situations.

In conclusion, robo-advisors have transformed the investment landscape by incorporating technology, algorithms, and machine learning into the investment process. They offer a range of services, including risk assessment, portfolio construction, rebalancing, and tax optimization. By embracing the benefits of robo-advisors, investors can gain access to professional investment management and achieve their financial goals with greater ease and efficiency.