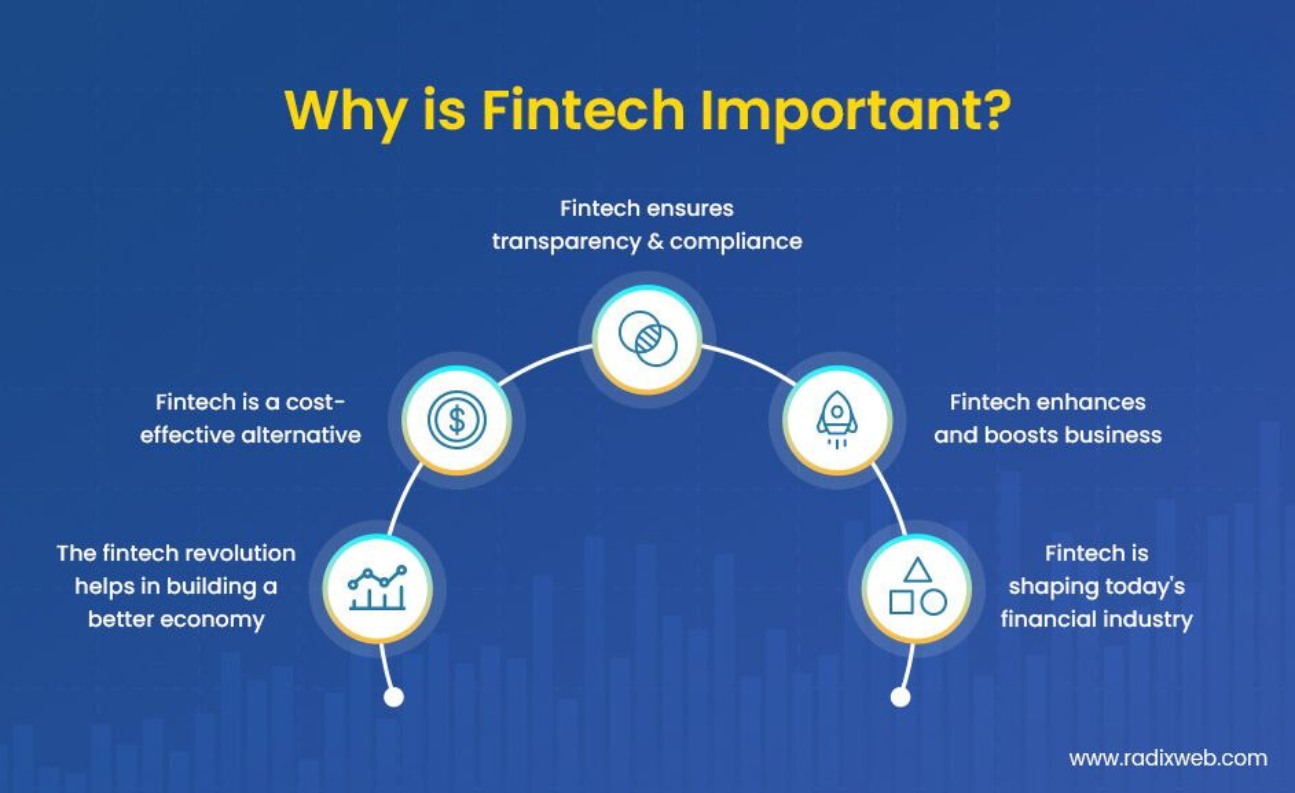

The financial services landscape has undergone a seismic shift in recent years, with the rise of financial technology (fintech) companies challenging traditional banking institutions. As consumers demand more convenience, transparency, and personalized experiences, fintechs and traditional banks are navigating a new era of collaboration, competition, and innovation.

The Fintech Revolution

Fintech companies have disrupted the financial services industry by leveraging cutting-edge technologies, such as artificial intelligence, blockchain, and cloud computing, to offer innovative products and services. These companies have capitalized on the growing demand for digital banking solutions, providing customers with seamless and user-friendly experiences.

From mobile banking apps to peer-to-peer payment platforms and crowdfunding platforms, fintechs have transformed the way we manage our finances. Their agility and customer-centric approach have made them a force to be reckoned with, attracting millions of users and gaining significant market share.

Traditional Banks: Adapting to the Digital Age

While fintechs have been the disruptors, traditional banks have recognized the need to adapt to the changing landscape. Many have embraced digital transformation, investing heavily in technology and partnering with fintech companies to enhance their offerings and remain competitive.

Traditional banks have leveraged their vast resources, established customer bases, and regulatory expertise to develop their own digital banking solutions. They have introduced mobile apps, online banking platforms, and innovative services like contactless payments and virtual assistants.

However, the challenge for traditional banks lies in overcoming their legacy systems and bureaucratic structures, which can hinder their ability to innovate and respond quickly to market demands.

Collaboration and Competition

As the lines between fintechs and traditional banks blur, the future of financial services is likely to be shaped by a combination of collaboration and competition. Both entities bring unique strengths to the table, and by working together, they can create powerful synergies.

Fintechs can benefit from the vast customer bases, regulatory expertise, and financial resources of traditional banks, while banks can leverage the agility, innovation, and customer-centric approaches of fintechs. Partnerships and acquisitions have become increasingly common, allowing both parties to enhance their offerings and expand their reach.

At the same time, competition remains fierce as both fintech and traditional banks strive to capture market share and remain relevant in an ever-changing landscape. Fintechs continue to disrupt traditional banking models, offering innovative solutions that cater to specific consumer needs, while traditional banks leverage their brand recognition and trust to retain and attract customers. In this highly competitive environment, transparency in communicating the annual percentage rate and other financial metrics has become crucial for both parties.

Regulatory Challenges and Consumer Protection

As the fintech industry continues to grow, regulatory bodies are grappling with the challenge of ensuring consumer protection while fostering innovation. Concerns surrounding data privacy, cybersecurity, and financial stability have led to increased scrutiny and the implementation of new regulations.

Traditional banks have long operated within a well-established regulatory framework, but fintechs have often found themselves navigating uncharted territory. Striking the right balance between promoting innovation and safeguarding consumer interests has been a delicate dance for regulators.

Emerging Trends and Future Outlook

The future of financial services is likely to be shaped by several emerging trends, including:

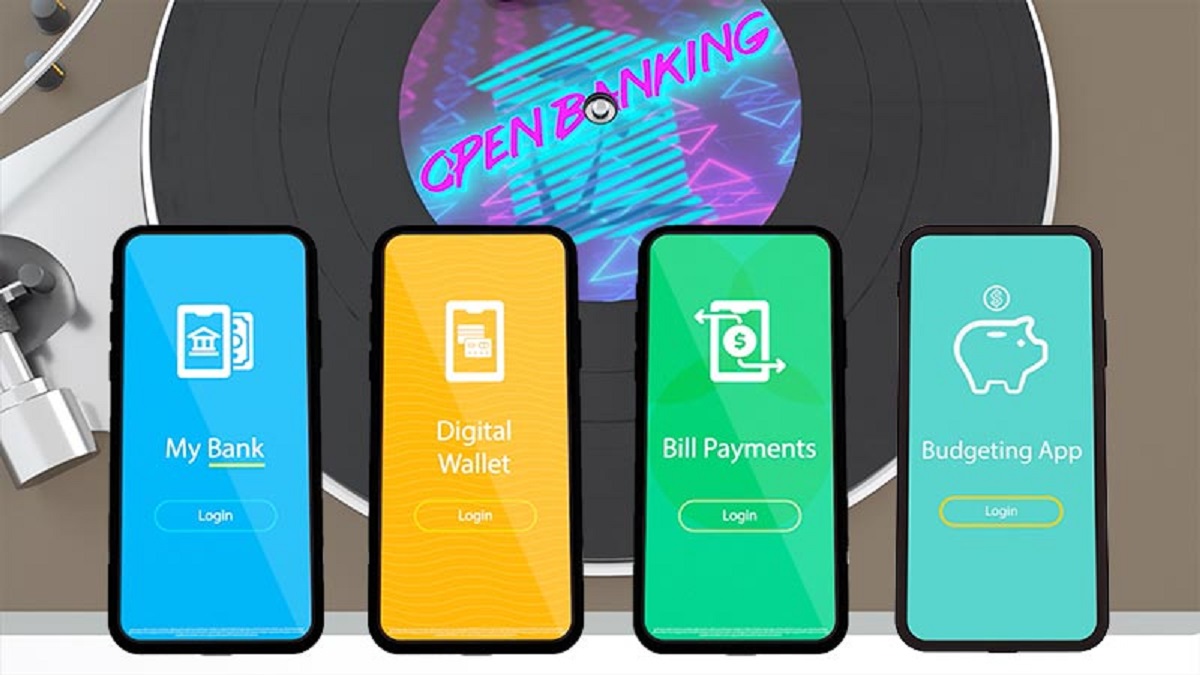

Open Banking: The concept of open banking, which allows third-party providers to access financial data with customers’ consent, is gaining traction globally. It could lead to a more collaborative ecosystem, fostering greater innovation and personalized financial solutions.

Embedded Finance: Fintechs and traditional banks are exploring opportunities to embed financial services into non-financial platforms and applications, making financial products and services more accessible and integrated into consumers’ daily lives.

Sustainability and Ethical Banking: As environmental, social, and governance (ESG) considerations gain prominence, both fintechs and traditional banks are incorporating sustainable and ethical practices into their operations and product offerings.

Personalization and Artificial Intelligence: The adoption of artificial intelligence and machine learning technologies will enable more personalized and tailored financial services, enhancing customer experiences and driving greater efficiency.

Balancing Innovation and Stability

As the financial services industry continues to evolve, both fintechs and traditional banks must strike a delicate balance between innovation and stability. While fintechs drive disruptive change and push the boundaries of what’s possible, traditional banks provide the necessary foundation of trust, security, and regulatory compliance.

Consumers today demand the best of both worlds – the convenience and cutting-edge solutions offered by fintechs, combined with the reliability and trustworthiness of traditional banks. This convergence of innovation and stability will shape the future of financial services, creating a landscape where collaboration, competition, and consumer-centric solutions thrive.

Ultimately, the future of financial services will be defined by those entities that can successfully navigate the complexities of the industry, embrace technological advancements, and prioritize customer needs while maintaining a strong foundation of trust and regulatory compliance.