Introduction

Welcome to the world of Open Banking, a revolutionary approach to financial services that is transforming the way we manage our money. In this increasingly digital age, traditional banking models are being disrupted, making way for open and secure access to financial data and services.

So, what exactly is Open Banking? In simple terms, Open Banking is a system that enables individuals and businesses to share their financial information securely with authorized third-party providers (TPPs). This information includes transaction history, account balances, and other data that can be used to develop innovative financial products and services.

The concept of Open Banking gained momentum with the advent of digital technology and the desire for more personalized and efficient financial services. The goal is to empower consumers and businesses with control over their financial data, allowing them to access a wider range of products and services that meet their specific needs.

Open Banking has gained significant traction around the world, with countries embracing this approach to varying degrees. In some regions, regulatory frameworks have been implemented to ensure the safe and transparent sharing of financial data, while in others, market forces and industry collaboration are driving the transformation.

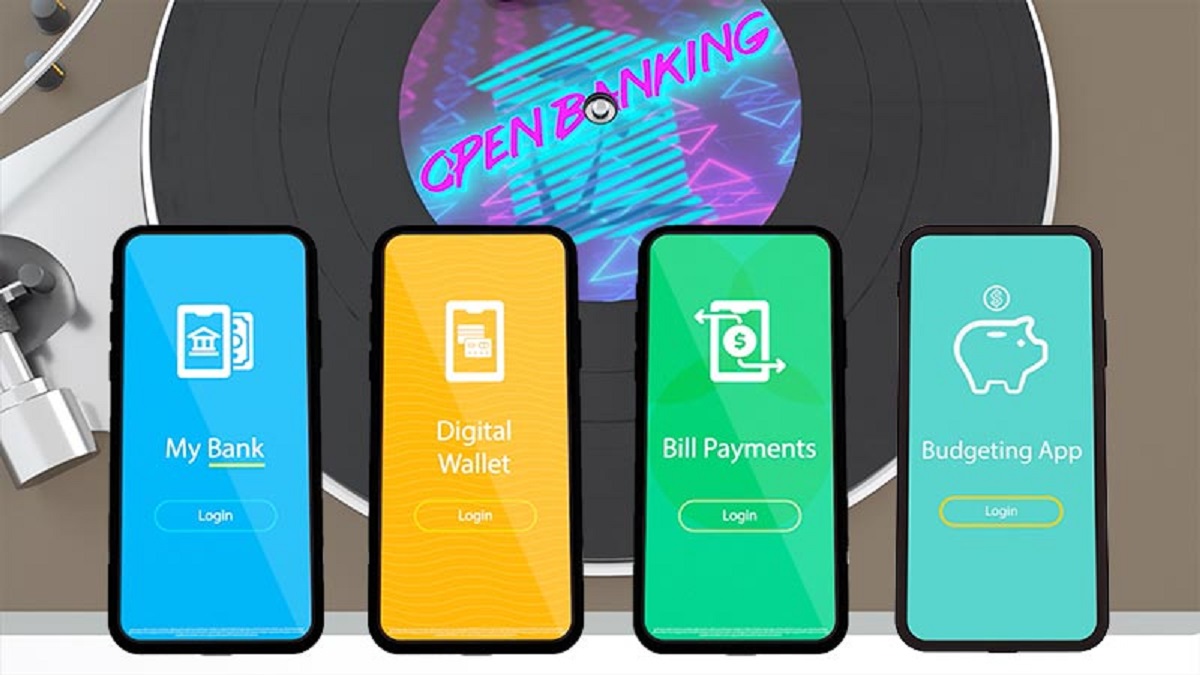

So, what does Open Banking mean for you as an individual or as a business owner? It means greater convenience, choice, and control over your financial information. Instead of being confined to the services provided by a single bank, Open Banking enables you to access a curated marketplace of financial products and services from various providers.

Imagine being able to seamlessly compare and switch between different banks and financial institutions, all from a single platform or app. It’s like having a personal financial advisor who understands your unique needs and can offer tailored solutions.

Open Banking also fosters innovation and competition within the financial industry. By encouraging collaboration between banks and fintech companies, it sparks creativity and drives the development of new and improved financial products and services. This not only benefits consumers and businesses but also promotes a more dynamic and inclusive financial ecosystem.

In the following sections, we will delve deeper into the concept of Open Banking, exploring its benefits, how it works, the role of APIs (Application Programming Interfaces), security considerations, and more. So, fasten your seatbelts and get ready to embark on a journey into the exciting world of Open Banking.

Definition of Open Banking

Open Banking is a term used to describe a system that allows individuals and businesses to securely share their financial data with authorized third-party providers (TPPs). By granting permission to access their accounts, customers can benefit from a wide range of innovative financial products and services.

At its core, Open Banking is built on the principles of transparency, control, and competition. It aims to break down the traditional barriers in the financial industry and enable customers to have a more comprehensive view of their financial information.

Under Open Banking, banks and other financial institutions are required to provide secure access to customer data through Application Programming Interfaces (APIs). These APIs allow authorized TPPs to retrieve customer data from multiple financial sources, such as transaction histories, account balances, and payment information. The data is then used to develop tailored financial solutions that better meet the needs of customers.

One of the key features of Open Banking is customer consent. Customers have full control over which TPPs can access their data and for what purposes. This ensures that customers are in charge of their personal information and have the power to revoke access at any time.

Open Banking is not limited to traditional banks; it also includes other financial institutions, such as fintech companies, payment service providers, and credit reference agencies. The goal is to create a more open and collaborative financial ecosystem, where different players can work together to bring about innovative solutions and improved customer experiences.

Regulatory bodies play a crucial role in overseeing and driving the implementation of Open Banking. In some jurisdictions, regulators have introduced specific frameworks and guidelines to ensure that the sharing of financial data is done securely and in compliance with privacy regulations. This helps to build trust among customers and encourages the adoption of Open Banking services.

Open Banking is a global movement, with various countries around the world adopting this concept in their financial systems. While the scope and pace of implementation may vary, the overarching objective remains the same: to empower customers with greater control over their financial information and to foster a more competitive and innovative financial industry.

In the next section, we will explore the benefits of Open Banking and how it is transforming the financial landscape for individuals and businesses.

Benefits of Open Banking

Open Banking has the potential to revolutionize the way individuals and businesses manage their finances by offering a range of benefits that enhance convenience, choice, and control. Let’s explore some of the key advantages of Open Banking:

1. Enhanced Financial Control: Open Banking puts individuals and businesses in the driver’s seat, allowing them to have a better understanding and control over their financial data. With access to comprehensive and real-time information, customers can make more informed decisions about their finances, such as comparing and switching between different financial products and services.

2. Personalized Financial Solutions: By sharing their financial data with authorized third-party providers, customers can benefit from personalized financial solutions that are tailored to their specific needs. This could include customized budgeting tools, personalized investment advice, or targeted product recommendations based on their spending patterns and financial goals.

3. Access to a Wider Range of Services: Open Banking enables customers to access a curated marketplace of financial products and services from various providers. This means they are not limited to the offerings of a single bank but can choose from a wide range of options that best suit their preferences and requirements. Whether it’s finding a better mortgage rate, selecting a more rewarding credit card, or exploring innovative digital payment solutions, Open Banking opens up new possibilities.

4. Seamless Account Aggregation: With Open Banking, customers no longer need to juggle multiple banking apps or websites to keep track of their accounts. Account aggregation services allow individuals and businesses to view and manage all their financial information in one place. This simplifies the financial management process and provides a holistic view of their financial situation.

5. Faster and Streamlined Payments: Open Banking facilitates faster and more streamlined payments through the use of secure APIs. It enables individuals to make instant payments and transfers between different accounts, eliminating the need for traditional, time-consuming processes. This is particularly beneficial for businesses, as it enhances cash flow management and optimizes payment processes, leading to increased efficiency and cost savings.

6. Promotes Innovation and Competition: Open Banking encourages collaboration and innovation within the financial industry. By allowing different providers to access customer data, it stimulates competition and drives the development of new and improved financial products and services. This ultimately benefits customers by providing them with more innovative, cost-effective, and customer-centric solutions.

7. Improved Fraud Detection and Security: The use of secure APIs in Open Banking enhances fraud detection and security measures. With real-time access to financial data, banks and TPPs can quickly identify and flag suspicious activities, leading to improved protection against fraud. Furthermore, Open Banking requires rigorous security protocols to ensure the privacy and protection of customer data, providing customers with peace of mind.

These are just a few of the many benefits that Open Banking brings to individuals and businesses. As the adoption of Open Banking continues to grow, we can expect even more innovative and customer-centric financial services that will transform the way we manage our money.

How Does Open Banking Work?

Open Banking operates through a secure and standardized system that allows the sharing of financial data with authorized third-party providers (TPPs). Here’s a simplified overview of how Open Banking works:

1. Customer Consent: Open Banking begins with the customer granting explicit consent to share their financial information with third-party providers. Customers have full control over which TPPs can access their data and for what specific purposes, ensuring their privacy and protection.

2. Secure APIs: Banks and financial institutions provide access to customer data through secure Application Programming Interfaces (APIs). These APIs serve as the gateways that allow authorized TPPs to retrieve specific data from the customers’ accounts, such as transaction histories, account balances, and payment information.

3. Data Transmission: When a customer gives consent, the authorized TPPs establish a secure connection with the respective bank’s API. This connection ensures that the customer’s data is transmitted in a secure and encrypted manner, safeguarding it from unauthorized access.

4. Data Retrieval and Analysis: Once connected, the TPPs retrieve the agreed-upon customer data from the respective banks’ APIs. They analyze this data to develop innovative financial products and services tailored to the customer’s needs. This could include personalized budgeting tools, financial management apps, or even investment advice based on the customer’s spending habits.

5. Service Provision: After analyzing the data, the TPPs provide their services to the customer. This could involve offering customized financial recommendations, facilitating faster and seamless payments, or providing access to a range of financial products from different providers. These services are designed to provide customers with enhanced convenience, choice, and control over their financial lives.

6. Ongoing Authorization: Customers have the right to revoke or change their consent at any time. They can manage their authorized TPPs through their banking portals or dedicated Open Banking apps. This ensures that customers maintain control over their financial data and can adapt their preferences as needed.

7. Regulatory Oversight: Open Banking is regulated by various regulatory bodies in different jurisdictions. These regulators ensure that financial institutions and TPPs comply with strict security and privacy standards to safeguard customer data. They also monitor the implementation of Open Banking frameworks to ensure fair competition and protect the interests of customers.

It’s important to note that Open Banking operates based on customer consent and data privacy regulations. The system prioritizes the security and protection of customer data, allowing customers to benefit from the advantages of Open Banking while maintaining control over their financial information.

In the next section, we will discuss the role of APIs (Application Programming Interfaces) in Open Banking and their significance in enabling seamless data sharing and integration among different financial institutions and service providers.

The Role of APIs in Open Banking

APIs, or Application Programming Interfaces, play a vital role in enabling the secure and seamless sharing of financial data in Open Banking. APIs act as bridges that facilitate communication and data exchange between different systems, allowing authorized third-party providers (TPPs) to access and analyze customer data. Here’s a closer look at the role of APIs in Open Banking:

1. Secure Data Access: APIs provide a secure method for banks and other financial institutions to grant access to customer data. By using standardized programming interfaces, APIs allow TPPs to retrieve specific data from the banks’ systems, such as transaction history, account balances, and payment information. This data transmission occurs within a secure environment, ensuring the privacy and protection of customer information.

2. Standardization and Interoperability: APIs in Open Banking rely on standardized protocols and formats, ensuring compatibility and interoperability between different financial institutions and TPPs. Standardization enables seamless integration and data exchange, allowing customers to securely share their financial information with multiple service providers without the need for complex and custom integration efforts.

3. Real-Time Data Access: APIs enable real-time access to financial data, allowing TPPs to retrieve up-to-date information directly from the banks’ systems. This real-time data availability fosters faster and more accurate financial services, such as instant payments, personalized financial recommendations, and real-time budgeting tools. It empowers customers with timely insights and allows TPPs to offer more responsive and dynamic solutions.

4. Data Consistency and Accuracy: APIs ensure that the data retrieved from different financial institutions remains consistent and accurate. Through standardized API protocols, TPPs can access and integrate customer data across multiple accounts and institutions, providing a holistic view of the customer’s financial information. This enables the development of comprehensive and accurate financial services that take into account the customer’s complete financial picture.

5. Customizable Access Permissions: APIs allow customers to customize their access permissions when interacting with TPPs. Customers have the freedom to grant or revoke access to their financial data, choose the type of data that can be accessed, and specify the purposes for which the data can be used. This level of control ensures that customers can provide access to their data only to trusted and authorized TPPs.

6. Facilitating Innovation and Competition: APIs foster innovation and competition within the financial industry by enabling collaboration between banks, fintech companies, and other service providers. Through APIs, financial institutions can offer their services to TPPs, who can then create value-added products and services for customers. This collaborative ecosystem encourages the development of innovative solutions and promotes healthy competition, benefiting customers with a wider range of choices and improved financial services.

Overall, APIs are the foundation of Open Banking, enabling secure and efficient data sharing between financial institutions and TPPs. They facilitate the seamless integration of financial services and empower customers with greater choice and control over their financial information.

In the next section, we will explore the security and privacy considerations associated with Open Banking, ensuring that customers’ data remains protected in this new era of financial services.

Security and Privacy Considerations

With the rise of Open Banking and the sharing of financial data with third-party providers (TPPs), ensuring the security and privacy of customer information becomes paramount. To address these concerns, robust measures are in place to safeguard customer data. Here are some key security and privacy considerations in Open Banking:

1. Data Encryption: One of the fundamental security measures in Open Banking is data encryption. Customer data is encrypted before transmission, ensuring that it remains protected from unauthorized access. Encryption algorithms, such as HTTPS/TLS (Secure Hypertext Transfer Protocol/Transport Layer Security), are used to secure data in transit, making it nearly impossible for hackers to intercept and decipher the information.

2. Authorization and Consent: Open Banking relies on explicit customer consent for the sharing of financial data. Customers have the authority to grant or revoke consent to TPPs, ensuring that their information is accessed only by trusted entities. The consent process is typically managed through secure banking portals or dedicated Open Banking apps, giving customers full control over their data and maintaining their privacy preferences.

3. Secure APIs: The use of secure Application Programming Interfaces (APIs) is crucial in Open Banking. APIs act as gateways for data exchange between banks and TPPs, and they employ robust security mechanisms. Authentication protocols, such as OAuth (Open Authorization), are used to authenticate TPPs, ensuring that only authorized entities can access customer data. Additionally, APIs frequently undergo rigorous security testing and vulnerability assessments to identify and address any potential weak points.

4. Compliance with Regulations: Open Banking frameworks are backed by regulatory bodies that enforce strict security and privacy standards. Financial institutions and TPPs must comply with these regulations to ensure the protection of customer data. The regulations outline requirements for data protection, account access, and consent management, among other security and privacy considerations.

5. Data Minimization: Open Banking promotes the concept of data minimization, which means that only the necessary data required for specific services is accessed and shared. This reduces the risk of unauthorized access, as sensitive customer information is limited to what is essential for delivering the requested financial services. TPPs are required to adhere to these principles to ensure that customer data is handled responsibly and with the highest level of security.

6. Monitoring and Fraud Detection: Banks and TPPs utilize advanced monitoring systems to detect and prevent fraudulent activities. Real-time monitoring of transactions and account activity helps identify suspicious behavior and unauthorized access attempts. Additionally, machine learning algorithms and artificial intelligence systems analyze customer behavior patterns to identify any anomalies and flag potential security breaches.

7. Transparency and Accountability: Open Banking promotes transparency in terms of how customer data is accessed, shared, and used. Financial institutions and TPPs have a responsibility to clearly communicate their privacy policies and data handling practices to customers. This enhances trust and ensures that customers are aware of how their data is being utilized, promoting greater accountability within the Open Banking ecosystem.

While Open Banking is designed with strong security and privacy measures, it is essential for customers to remain vigilant and adopt best practices to protect their data. This includes using strong and unique passwords, regularly updating their apps and devices, and being cautious of phishing attempts or suspicious requests for personal information.

By addressing security and privacy considerations effectively, Open Banking can deliver the benefits of expanded financial services while ensuring the protection and confidentiality of customer data in this new era of banking.

Open Banking around the World

Open Banking is a global movement that is being embraced by countries around the world, although the pace and scope of implementation vary across different regions. Let’s take a closer look at how Open Banking is evolving in various parts of the world:

1. Europe: Europe has been at the forefront of Open Banking, with the implementation of the revised Payment Services Directive (PSD2) in 2018. PSD2 mandates that banks provide access to customer data through secure APIs, enabling third-party providers to offer innovative financial services. The European Union is also fostering collaboration and standardization through initiatives such as the Open Banking Europe Forum.

2. United Kingdom: The United Kingdom was one of the early adopters of Open Banking. The Open Banking Implementation Entity (OBIE) was established in 2016 to drive the implementation of Open Banking standards and ensure compliance with PSD2. Open Banking has gained significant traction in the UK, with millions of customers using Open Banking-enabled services for improved financial management and access to innovative products.

3. Australia: Australia introduced Open Banking as part of the Consumer Data Right (CDR) legislation. The CDR aims to give consumers greater control over their data, starting with the banking sector. The Australian Competition and Consumer Commission (ACCC) oversees the implementation of Open Banking, with a phased approach that began in 2020. The CDR will eventually expand to other sectors like energy and telecommunications.

4. Canada: Canada has expressed interest in Open Banking and is exploring its potential benefits. The Canadian government has conducted consultations and discussions with industry stakeholders to gather insights on the design and implementation of Open Banking frameworks. Although formal regulations have not been introduced yet, several Canadian banks have started offering open APIs to support innovation and collaboration with FinTechs.

5. Singapore: Singapore, known for its thriving FinTech ecosystem, has been actively promoting Open Banking. The Monetary Authority of Singapore (MAS) has introduced guidelines to encourage financial institutions to adopt Open APIs and facilitate secure data sharing. The aim is to drive innovation and create a more vibrant and competitive financial sector in Singapore.

6. Latin America: Countries in Latin America are also recognizing the potential of Open Banking. Brazil has been leading the way with the implementation of regulations requiring banks to provide APIs for data sharing. Other countries in the region, such as Mexico and Colombia, are exploring the adoption of Open Banking frameworks to enable innovation and provide customers with improved financial services and options.

These are just a few examples of how Open Banking is unfolding around the world. Other countries, including Japan, South Korea, and India, are also exploring or in the early stages of implementing Open Banking initiatives. As the benefits of Open Banking become more apparent, we can expect to see further global adoption and collaboration in the financial industry.

In the next section, we will explore some examples of the innovative services and solutions that have emerged as a result of Open Banking.

Examples of Open Banking Services

Open Banking has paved the way for the development of innovative financial services and solutions that offer enhanced convenience, personalization, and value to customers. Here are some examples of how Open Banking is transforming the financial landscape:

1. Personal Financial Management Apps: Open Banking has fueled the growth of personal financial management apps that provide users with a comprehensive view of their financial accounts from multiple institutions. These apps use Open Banking APIs to securely access and aggregate data, allowing users to track their spending, set budgeting goals, and receive personalized insights and recommendations to manage their finances effectively.

2. Instant Payments and Transfers: Open Banking has facilitated the development of instant payment and transfer services. Customers can make real-time payments directly from their bank accounts to another individual or business, eliminating the need for traditional payment methods like checks or bank transfers that can take days to process. This convenience is particularly beneficial for businesses that require fast and secure payment processing.

3. Account Aggregation Platforms: Open Banking enables the creation of account aggregation platforms that offer customers a centralized view of all their financial accounts, regardless of the institution. These platforms allow users to manage their accounts, track transactions, and access personalized financial recommendations, all from a single interface. The seamless integration of data made possible by Open Banking APIs ensures data consistency and accuracy.

4. Personalized Lending Solutions: Open Banking has revolutionized the lending landscape by making it easier for borrowers to access personalized loan offers. With customer consent, lending platforms can securely access financial data to assess creditworthiness and provide tailored loan options. This enables individuals and businesses to find competitive loan rates and terms that suit their specific financial circumstances.

5. Open Marketplaces: Open Banking has spurred the development of open marketplaces where customers can compare and access a wide range of financial products and services from different providers. These marketplaces provide a transparent and customer-centric approach to finding the best deals on banking products, insurance policies, investments, and more. Customers can make informed decisions based on personalized recommendations and easily switch between providers.

6. Improved Foreign Exchange Services: Open Banking APIs have facilitated the development of currency exchange platforms that offer more transparent and competitive foreign exchange rates. These platforms leverage real-time access to customer data to provide personalized currency exchange services, allowing individuals and businesses to enjoy better rates and lower fees when converting currencies.

These are just a few examples of the many innovative services and solutions that have emerged as a result of Open Banking. As Open Banking continues to evolve, we can expect even more exciting and customer-centric financial products and services that will transform the way we manage our money.

In the following section, we will explore the challenges and risks associated with implementing Open Banking and how they can be effectively addressed.

Challenges and Risks of Open Banking

While Open Banking offers numerous benefits, its implementation also presents certain challenges and risks that need to be effectively addressed. Here are some key challenges and risks associated with Open Banking:

1. Data Security: With the increased sharing of financial data, ensuring adequate data security becomes paramount. Cybersecurity threats such as data breaches and unauthorized access to customer information pose significant risks. Financial institutions and TPPs must implement robust security measures, including encryption, strong authentication protocols, and ongoing monitoring, to safeguard customer data from potential vulnerabilities.

2. Privacy Concerns: Open Banking involves the sharing of personal financial data, which can raise privacy concerns among customers. There is a need for transparent communication about data usage, storage, and retention policies to address these concerns. Regulatory frameworks play a crucial role in ensuring that customer privacy rights are protected, and strict compliance with privacy regulations is required to maintain trust in Open Banking.

3. Trust and Consumer Adoption: Building trust among customers is vital for the successful adoption of Open Banking. Customers need to feel confident about sharing their financial data with TPPs and financial institutions. Banks and TPPs must prioritize data protection, transparency, and clear communication to foster trust and encourage customers to embrace Open Banking services.

4. Technical Integration: Implementing Open Banking requires the integration of different systems and APIs across financial institutions and TPPs. This can be a complex and time-consuming process, requiring collaboration, standardization, and adherence to industry specifications. Technical challenges, such as system compatibility and maintaining data consistency, must be overcome to ensure a seamless and efficient Open Banking ecosystem.

5. Regulatory Compliance: Open Banking frameworks are accompanied by regulatory requirements that banks and TPPs must adhere to. Compliance with these regulations, which vary across jurisdictions, can be challenging. Financial institutions and TPPs need to invest in robust compliance frameworks to ensure that they meet the regulatory obligations and maintain a secure and compliant Open Banking environment.

6. Market Competition: Open Banking introduces increased competition in the financial industry. While this is beneficial for consumers, it can pose challenges for traditional financial institutions that may face pressure to innovate and offer more competitive services. Banks need to adapt to the changing landscape and embrace collaboration with TPPs to foster innovation and provide better customer experiences.

To address these challenges and mitigate risks, collaboration between regulators, financial institutions, and TPPs is crucial. Establishing robust security standards, effective risk management practices, and continuous monitoring frameworks will help build a secure and trustworthy Open Banking ecosystem.

In the next section, we will explore the future prospects and potential advancements of Open Banking in the financial industry.

The Future of Open Banking

The future of Open Banking looks promising as it continues to reshape the financial industry and empower customers with enhanced access, convenience, and control over their financial lives. Here are some potential advancements and trends that shape the future of Open Banking:

1. Artificial Intelligence and Machine Learning: The integration of artificial intelligence (AI) and machine learning (ML) technologies will enhance the capabilities of Open Banking services. AI-powered chatbots and virtual assistants will provide personalized financial advice and support, while ML algorithms will analyze customer data to offer tailored financial products and recommendations.

2. Open Finance: Open Banking lays the foundation for a broader concept known as Open Finance. As regulations evolve, Open Finance aims to extend the principles of Open Banking to other sectors, including insurance, investments, and pensions. This expansion will offer customers a holistic view of their financial lives and enable seamless integration between various financial services.

3. Enhanced Security and Privacy: Technology advancements will strengthen security and privacy measures in Open Banking. Biometric authentication methods, such as fingerprint or facial recognition, will provide an extra layer of security. Privacy-enhancing technologies will give customers more control over their data, including options for selective data sharing and encryption techniques that protect sensitive information.

4. Global Interoperability: As Open Banking continues to evolve worldwide, there will be an increasing focus on global interoperability. Efforts will be made to establish standardization and compatibility between different Open Banking frameworks, allowing customers to access services across borders and enabling seamless integration for multinational financial institutions and TPPs.

5. Blockchain Technology: The use of blockchain technology has the potential to revolutionize Open Banking by offering enhanced security, transparency, and efficiency in data sharing and transactions. Blockchain can provide tamper-proof and decentralized platforms for secure identity verification, real-time payments, and smart contracts, ensuring trust and speeding up financial processes.

6. Collaboration and Partnerships: Collaboration between traditional financial institutions and fintech companies will increase, fostering innovation and improving customer experiences. Banks and TPPs will form strategic partnerships to leverage each other’s strengths and offer a wider range of integrated financial services to meet the evolving needs of customers.

The future of Open Banking will depend on continuous innovation, regulatory frameworks, and customer trust. As consumers become more accustomed to digital banking experiences and demand more personalized and efficient financial services, Open Banking will play a central role in meeting these expectations.

Overall, the future of Open Banking looks promising, with advancements in technology, regulatory developments, and customer-centric solutions ensuring a dynamic and competitive financial landscape.

Conclusion

Open Banking is transforming the financial industry, revolutionizing the way individuals and businesses access, manage, and benefit from financial services. With the secure sharing of customer data through APIs, Open Banking offers numerous advantages, including enhanced control over financial information, personalized solutions, and access to a wider range of products and services.

Throughout this article, we explored the definition of Open Banking and its global implementation. We discussed the benefits it brings, such as improved financial control, personalized experiences, and increased innovation and competition. We also examined the role of APIs in enabling seamless data sharing and integration, as well as the importance of security and privacy considerations to protect customer data.

Open Banking is not without its challenges and risks. Data security threats, privacy concerns, technical integration complexities, and regulatory compliance are some of the issues that need to be effectively addressed. However, with robust security measures, trust-building efforts, collaboration, and continuous advancements in technology, these challenges can be overcome.

The future of Open Banking looks promising. Advancements such as AI and ML technologies, Open Finance, enhanced security and privacy measures, global interoperability, blockchain applications, and collaborations between traditional banks and fintech companies are driving the evolution of Open Banking. These advancements will provide customers with even more personalized, efficient, and secure financial experiences.

In conclusion, Open Banking represents a remarkable shift in the financial industry, empowering individuals and businesses with greater control and choice over their finances. It is shaping the future of financial services, fostering innovation and competition, and ultimately improving the overall customer experience. As Open Banking continues to evolve and expand worldwide, it holds the potential to revolutionize how we manage money and access financial services, creating a more inclusive, transparent, and customer-centric financial landscape.