Introduction

The advent of open banking has revolutionized the financial industry, transforming the way consumers interact with their banks and creating new opportunities for innovation in the financial sector. Open banking refers to the practice of granting third-party developers and service providers access to customer financial data through secure Application Programming Interfaces (APIs).

In recent years, open banking has gained traction as a global movement, driven by technological advancements and regulatory initiatives aimed at fostering competition, enhancing customer experience, and promoting financial inclusion. By enabling customers to share their financial information with authorized third-party providers, open banking allows for the development of innovative financial products and services that cater to individual needs and preferences.

Open banking originated from a desire to empower consumers, giving them more control over their financial lives and enabling them to make more informed decisions. It also aims to break down the barriers that traditionally hindered competition in the financial industry, promoting a more level playing field for fintech startups and established institutions alike.

This article will explore the origins of open banking, the role of government regulations, its global adoption, as well as the benefits and concerns associated with this emerging trend. We will delve into the mechanics of how open banking works and discuss its future implications for the financial landscape.

So, let’s embark on a journey to uncover the fascinating world of open banking, where data becomes not just a valuable asset but also a catalyst for innovation and financial empowerment.

The Origins of Open Banking

The concept of open banking can be traced back to the early 2000s when the digital revolution began to reshape various industries, including finance. However, it wasn’t until later years that the idea of opening up customer data and granting access to third-party providers gained significant attention.

One of the key catalysts for open banking was the growing demand for financial innovation and improved customer experiences. Traditional banking systems were often characterized by limited accessibility, slow processes, and a lack of personalization. Customers wanted more flexibility, choice, and convenience in managing their finances, leading to calls for a more open and collaborative approach to banking.

The rise of fintech startups also played a crucial role in pushing the boundaries of traditional banking practices. These startups, armed with cutting-edge technology and a customer-centric mindset, saw the potential in leveraging customer data to create innovative financial solutions. However, accessing that data proved to be a significant challenge due to the tightly controlled nature of banking systems.

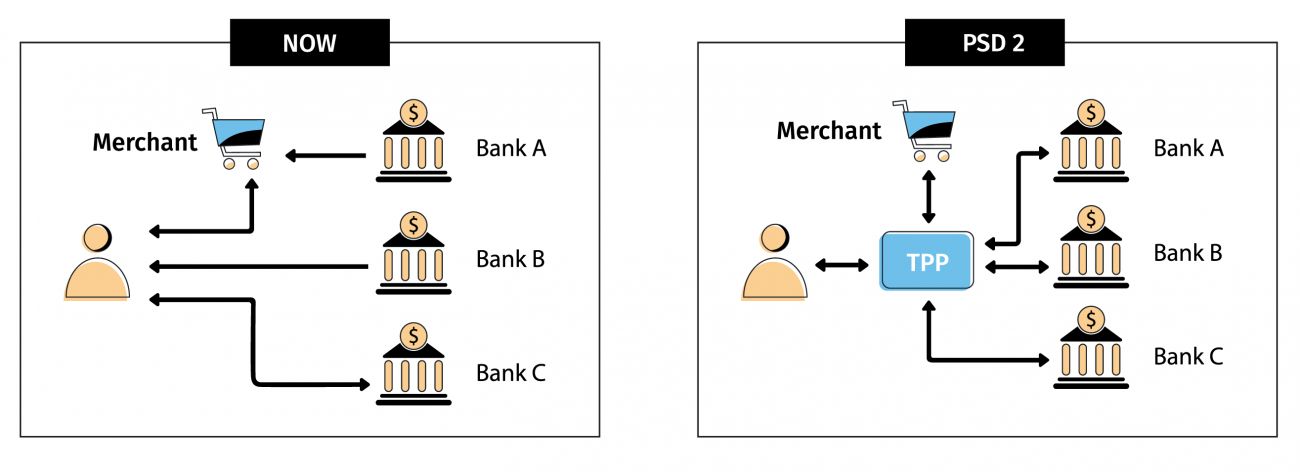

The turning point came in 2016 when the European Union introduced the revised Payment Services Directive (PSD2). Under PSD2, banks were required to open up their customer data to authorized third-party providers via secure APIs. This directive aimed to increase competition, foster innovation, and enhance customer choice by enabling individuals to share their financial information with trusted third parties.

PSD2 set the stage for the open banking movement, inspiring other countries and regions to follow suit. In the United Kingdom, the Competition and Markets Authority (CMA) mandated that nine of the largest banks create open APIs to allow for secure data sharing. This initiative, known as the Open Banking Implementation Entity, aimed to empower consumers with greater control over their financial data and stimulate competition and innovation within the industry.

Since then, open banking has gained momentum globally, with countries such as Australia, Canada, Singapore, and others exploring or implementing similar measures to foster open and collaborative financial ecosystems.

Overall, the origins of open banking can be attributed to the convergence of technological advancements, customer demands for improved banking services, and regulatory initiatives aimed at promoting competition and innovation in the financial sector.

The European Directive

The European Union’s revised Payment Services Directive (PSD2) stands as a landmark regulation in the development of open banking. Introduced in 2016, PSD2 laid the foundation for open banking in Europe by mandating banks to provide access to customer data to authorized third-party providers.

PSD2 aimed to create a more competitive and innovative financial landscape by opening up the traditionally closed banking industry. It recognized the potential of sharing customer data with trusted third parties to drive financial innovation, improve customer experiences, and foster greater choice and control for consumers.

Under PSD2, banks in the European Economic Area (EEA) have to facilitate secure access to account information and payment initiation services through APIs. This means that customers can choose to share their financial data, such as transaction history, account balances, and other relevant information, with authorized third-party providers, securely and with their explicit consent.

This access to customer data has paved the way for a range of innovative financial products and services. Fintech startups and established financial institutions can now leverage this data to build user-friendly applications, personal finance management tools, budgeting apps, loan comparison platforms, and many other solutions tailored to the specific needs of customers.

PSD2 also introduced strong customer protection measures to ensure data security and privacy. Any third-party provider seeking access to customer data must be authorized and regulated by local authorities, ensuring strict compliance with data protection regulations like the General Data Protection Regulation (GDPR).

The implementation of PSD2 across the EEA has led to the emergence of numerous innovative fintech companies and open banking platforms. These platforms act as intermediaries, connecting banks and third-party developers, facilitating secure data exchange, and stimulating collaboration within the financial industry.

Furthermore, PSD2 has prompted traditional banks to embrace digital transformation and adopt open banking principles. Some banks have proactively developed their own APIs, opening up their infrastructure and services to foster partnerships and drive innovation. This shift towards open banking has led to improved customer experiences, increased competition, and a more vibrant financial ecosystem.

Overall, the European Directive PSD2 has been a game-changer, revolutionizing the banking industry by requiring banks to open up their systems and embrace open banking principles. It has paved the way for greater collaboration between banks and third-party providers, leading to the development of innovative financial solutions and empowering customers with more choice and control over their financial lives.

Open Banking Around the World

While the European Union has been at the forefront of the open banking movement, other countries around the world have also recognized the benefits of open banking and are exploring or implementing similar initiatives.

Australia, for example, introduced the Consumer Data Right (CDR) in 2019, which aims to give consumers greater control over their data across various sectors, including banking. The CDR requires banks to share customer data with accredited third-party providers upon customer consent. This initiative has the potential to drive competition, foster innovation, and empower consumers in the Australian financial market.

The United States, traditionally known for its highly regulated banking sector, is also witnessing a shift towards open banking. Although there is no national open banking regulation at the moment, several initiatives have emerged at the state level. For instance, states like California and Vermont have passed laws that require banks to share data with authorized third parties. Additionally, industry initiatives such as the Financial Data Exchange (FDX) are working towards establishing common standards for secure data sharing between financial institutions and third-party providers.

In Canada, the government has expressed interest in exploring open banking as a means to increase competition and innovation in the financial industry. A consultation process was initiated in 2019 to gather feedback from stakeholders and assess the potential benefits and risks of open banking. The outcome of this consultation may shape the future landscape of open banking in Canada.

Singapore is another country actively embracing open banking principles. The Monetary Authority of Singapore (MAS) has launched an open banking initiative, known as the API Exchange (APIX), which aims to facilitate collaboration between financial institutions and fintech companies. APIX provides a platform for secure data sharing and promotes innovation in the financial sector through open APIs.

As open banking continues to gain traction globally, it is evident that the approach and implementation may vary across jurisdictions. Some countries opt for regulatory mandates, while others rely on industry-led initiatives. However, the underlying objective remains the same – to enhance competition, innovation, and customer experiences in the financial industry.

It is worth noting that each country’s specific legal and regulatory frameworks may influence the pace and scope of open banking implementation. Privacy and data protection laws, consumer rights, and existing financial regulations play a crucial role in shaping the open banking landscape in each jurisdiction.

As the world embraces open banking, it is essential for countries to collaborate and share best practices to ensure harmonization and interoperability between different open banking ecosystems. This level of collaboration will enable seamless cross-border transactions and ensure the security and privacy of customer data in an interconnected world.

Benefits of Open Banking

Open banking has the potential to bring a wide range of benefits to consumers, businesses, and the overall financial industry. Here are some of the key advantages:

- Increased Competition: Open banking fosters competition by breaking down barriers to entry and encouraging new players to enter the financial market. This leads to a greater variety of products and services, improved customer experiences, and competitive pricing.

- Enhanced Customer Experience: Open banking enables customers to access a wide range of financial products and services from different providers all in one place. This allows for a more personalized and tailored experience, as customers can choose the solutions that best meet their specific needs and preferences.

- Improved Financial Management: Open banking empowers consumers with access to a consolidated view of their financial data. This makes it easier for individuals to manage their finances, track spending, analyze trends, and make more informed financial decisions.

- Increased Innovation: With open access to customer data, fintech startups and other innovative companies can develop new and exciting financial solutions. From budgeting apps to personalized investment platforms, open banking paves the way for groundbreaking innovations that address the evolving needs of consumers.

- Financial Inclusion: Open banking has the potential to improve financial inclusion by making financial services more accessible to underserved populations. By providing access to transaction data and credit information, open banking allows for a more accurate assessment of creditworthiness, helping individuals without traditional credit histories access loans and other financial services.

- Increased Security: While data sharing is a vital component of open banking, strong security measures are also put in place to protect customer data. Banks and third-party providers must comply with stringent data protection regulations to ensure the privacy and security of sensitive financial information.

- Efficient Payments: Open banking allows for faster, more secure, and convenient payment methods. With payment initiation services, customers can initiate transactions directly from their bank accounts without the need for traditional card-based payments, resulting in streamlined processes and reduced transaction costs.

These benefits demonstrate the transformative potential of open banking in revolutionizing the financial landscape. By promoting competition, empowering consumers, driving innovation, and improving financial inclusion, open banking has the ability to reshape how individuals interact with financial services and unlock new opportunities for growth and prosperity.

Risks and Concerns

While open banking offers numerous benefits, it also raises several important risks and concerns that need to be addressed to ensure a secure and trustworthy financial ecosystem. Here are some key risks and concerns associated with open banking:

- Data Privacy and Security: The sharing of personal financial data introduces potential privacy and security risks. Customers must have confidence that their data is protected and only accessed by authorized and trusted third-party providers. Robust data protection measures, encryption techniques, and strong authentication protocols are essential to mitigate these risks.

- Consent and Control: Open banking relies on customer data sharing based on explicit consent. However, ensuring customers have complete control over their data and fully understand the implications of sharing is challenging. Safeguards must be in place to ensure informed consent, easy revocation, and transparent data management processes.

- Unauthorized Access and Fraud: Open banking can be exploited by malicious actors who seek to gain unauthorized access to sensitive financial information. Strong security measures, including multi-factor authentication and fraud detection systems, are crucial to protect against unauthorized access and fraudulent activities.

- Lack of Standardization and Interoperability: The absence of standardized interfaces and data formats across different banks and regions poses challenges for third-party developers and the seamless integration of services. Interoperability efforts and common industry standards are needed to ensure smooth operations and enhance customer experiences.

- Unequal Regulatory Environments: As open banking evolves globally, disparities in regulations across jurisdictions can create compliance challenges for financial institutions and third-party providers operating in multiple markets. Harmonization efforts and international collaboration are necessary to foster a level playing field and ensure consistency in data protection and consumer rights.

- Credential Sharing and Phishing Attacks: The proliferation of API connections and third-party access points increases the risk of phishing attacks and credential sharing. Educating consumers about cybersecurity best practices, implementing strong authentication methods, and monitoring for fraudulent activities are essential to mitigate these risks.

- Customer Confusion and Trust: The complexity of open banking and the involvement of multiple service providers may lead to confusion and concerns among customers. Building trust through effective communication, transparency, and robust customer support systems is crucial to ensure customer confidence in open banking services.

Addressing these risks and concerns is vital for the long-term success and sustainability of open banking. Regulatory bodies, financial institutions, and technology providers must work together to establish robust frameworks, implement strong security measures, and educate consumers about the benefits and risks of open banking to foster trust and confidence in the ecosystem.

How Open Banking Works

Open banking operates on the principle of secure data sharing between financial institutions and authorized third-party providers. Understanding how open banking works involves grasping the steps involved in data exchange and the role of application programming interfaces (APIs). Here is a simplified overview:

- Consent and Authorization: The customer provides explicit consent to allow their financial data to be shared with third-party providers. This consent can be given through the customer’s online banking portal or other authorized platforms.

- Authentication and Authorization: Once consent is given, the identity of the customer is authenticated by the bank. This ensures that only authorized individuals can access and share the financial data.

- Data Retrieval: Using secure APIs, authorized third-party providers can retrieve the customer’s financial data from the bank’s systems. This may include information such as transaction history, account balances, and other relevant data.

- Data Analysis and Service Provision: Third-party providers analyze the retrieved data to develop innovative financial products and services. This analysis may involve assessing spending patterns, offering personalized recommendations, or creating budgeting tools tailored to the customer’s needs.

- Customer Experience: The customer can then access the services and solutions offered by the third-party providers through their preferred channels, such as mobile apps, websites, or other digital platforms. This consolidated view of financial information allows for a seamless and integrated customer experience.

- Data Security and Privacy: Robust security measures are in place to protect the customer’s financial data throughout the entire process. Encryption techniques, secure connections, and compliance with data protection regulations ensure that data is handled safely and securely.

- Revocation and Control: Customers have the right to revoke their consent for data sharing at any time. They can also control which specific data elements or accounts they want to share with third-party providers. This enables customers to maintain control over their data and exercise their data privacy rights.

The success of open banking depends on the collaboration between banks, third-party providers, and regulatory bodies. Banks need to develop open APIs that are secure, reliable, and accessible for authorized third parties to retrieve data. Third-party providers must adhere to strict security standards and comply with data protection regulations to ensure the privacy and security of customer data. Regulatory bodies play a crucial role in establishing frameworks, standards, and guidelines to govern open banking practices and protect consumer rights.

Overall, open banking transforms the traditional banking landscape by enabling secure data sharing, fostering innovation, and providing customers with a more personalized and integrated financial experience.

The Future of Open Banking

The future of open banking holds immense potential for further revolutionizing the financial industry and shaping the way customers engage with their finances. Here are some key trends and possibilities that may shape the future of open banking:

- Expanding Ecosystem: Open banking is likely to witness the continued expansion of its ecosystem, with more banks, fintech startups, and traditional financial institutions embracing open banking principles. This expansion will result in a wider range of innovative products and services for consumers.

- Personalization and Customization: Open banking enables the delivery of highly personalized and customized financial experiences. With access to comprehensive customer financial data, financial institutions and third-party providers can offer tailored recommendations, personalized budgeting tools, and investment advice based on individual preferences and goals.

- Collaboration and Partnerships: Collaboration between banks, fintech providers, and non-financial entities will continue to accelerate. Partnerships will allow for the development of integrated solutions, seamless customer experiences, and innovative financial offerings that span multiple industries.

- Artificial Intelligence and Advanced Analytics: The integration of artificial intelligence (AI) and advanced analytics will play a significant role in open banking. These technologies will drive real-time data analysis, fraud detection, risk assessment, and the automation of financial processes, enhancing efficiency and enabling faster and more accurate decision-making.

- Open Finance: Open banking may extend beyond traditional banking services to include other sectors of finance, such as insurance, lending, and wealth management. The concept of Open Finance envisions a holistic approach to data sharing, allowing individuals to have a consolidated view of their overall financial well-being.

- Global Interoperability: As open banking continues to expand worldwide, efforts to establish global interoperability and standardization will become increasingly important. This will enable seamless cross-border transactions, data sharing, and collaboration between different open banking ecosystems.

- Blockchain and Distributed Ledger Technology: Blockchain and distributed ledger technology offer secure, decentralized data storage and transfer mechanisms. These technologies have the potential to enhance data security, privacy, and transparency in open banking, further strengthening trust and mitigating risks.

- Regulatory Evolutions: Regulatory frameworks surrounding open banking are likely to evolve as the industry matures. Regulatory bodies will adapt to technological advancements and changing customer demands, striking a balance between fostering innovation and ensuring consumer protection.

- Enhanced Financial Inclusion: Open banking has the potential to drive financial inclusion by leveraging data to assess creditworthiness more accurately. This can provide individuals with limited or no credit histories access to financial services, enabling greater economic participation and empowerment.

It is important to note that the future of open banking will depend on addressing ongoing challenges such as privacy concerns, cybersecurity threats, and regulatory complexities. Collaborative efforts between industry stakeholders, robust security measures, and clear regulatory frameworks will be vital for realizing the full potential of open banking while delivering optimal value for consumers and businesses.

Conclusion

Open banking has ushered in a new era in the financial industry, transforming the way individuals interact with their finances and creating opportunities for innovation and competition. It originated from the need for improved customer experiences, increased financial transparency, and enhanced control over personal data.

The European Directive PSD2 served as a catalyst for the global open banking movement, inspiring other countries to follow suit and implement similar initiatives. Open banking has gained momentum worldwide, with each jurisdiction adapting the concept to their unique regulatory frameworks and market dynamics.

The benefits of open banking are far-reaching. It fosters competition, enhances customer experiences, improves financial management, increases innovation, and promotes financial inclusion. With secure data sharing and robust authentication protocols, customers can access a wide range of innovative financial products and services tailored to their needs and preferences.

However, open banking also comes with risks and challenges. These include concerns related to data privacy and security, the need for standardization and interoperability, and the importance of building trust and maintaining customer control over their data.

The future of open banking holds exciting possibilities. It is expected to expand its ecosystem, accelerate partnerships and collaborations, leverage technologies like AI and blockchain, and embrace the concept of Open Finance. Regulatory frameworks will continue to evolve, ensuring a balance between fostering innovation and safeguarding consumer rights.

In conclusion, open banking provides a pathway to a more customer-centric and innovative financial ecosystem. By prioritizing data privacy, security, and transparency, open banking has the potential to revolutionize the way individuals manage their finances, unlock new opportunities for businesses, and drive economic growth.