Introduction

Open Banking has emerged as a revolutionary concept in the realm of finance, promising increased competition, innovation, and transparency. In Australia, Open Banking has gained significant traction and has the potential to reshape the way individuals and businesses interact with their banking data.

Open Banking is part of a global movement aimed at giving consumers greater control and access to their financial information. By allowing banking customers to securely share their data with third-party providers, Open Banking enables the development of new and innovative financial products and services. This shift towards openness is driven by advancements in technology and regulatory frameworks, which aim to foster a more competitive and customer-centric financial industry.

Australia’s journey towards Open Banking started in July 2020 when the Consumer Data Right (CDR) was implemented. The CDR grants individuals the right to access and share their banking data with accredited third-party providers securely. This move has opened up new opportunities for fintech companies, startups, and established financial institutions to leverage customer data to deliver personalized, tailored services.

The benefits of Open Banking are multifold. Firstly, it promotes competition by breaking down the monopoly held by traditional banks. As customers gain more control over their financial information, they can compare products, services, and interest rates more effectively, leading to a more competitive marketplace. This increased competition fosters innovation, as financial institutions strive to develop better, more customer-focused offerings to attract and retain customers.

Furthermore, Open Banking enhances customer experience by enabling individuals to access a wide range of financial services through a single platform. This convenience allows customers to effectively manage their finances, make more informed decisions, and improve their overall financial well-being. Open Banking also facilitates the integration of financial data with other applications, such as budgeting tools and personal finance management apps, providing users with a holistic view of their financial health.

Implementing Open Banking in Australia involves collaboration between various stakeholders. Banks, as data holders, play a crucial role in securely sharing customer data with authorized third-party providers through Application Programming Interfaces (APIs). These APIs ensure that data transfers are secure, standardized, and compliant with data protection regulations.

Consumers’ rights and protections are paramount in the Open Banking ecosystem. Robust security measures, consent frameworks, and data privacy regulations are in place to safeguard individuals’ data and prevent unauthorized access or misuse. Customers have full control over their data and can grant or revoke access to third-party providers at any time.

While Open Banking holds immense potential, it also poses challenges and concerns. Data security and privacy are crucial issues that need to be addressed comprehensively to maintain public trust and confidence. Ongoing regulatory oversight and collaboration between industry players and policymakers are essential to mitigate potential risks associated with data breaches or misuse.

The future of Open Banking in Australia looks promising. As the industry matures and evolves, we can expect to see an increasing number of innovative financial services emerging, tailored to the individual needs and preferences of banking customers. Open Banking has the power to transform the financial landscape, promoting customer empowerment, driving competition, and fueling innovation to create a more inclusive and accessible financial system for all.

History of Open Banking in Australia

The journey towards Open Banking in Australia can be traced back to the announcement of the Consumer Data Right (CDR) in November 2017. The CDR, initially known as Open Banking, was introduced as part of the Federal Government’s plan to empower consumers by providing them with control over their personal data.

In 2018, the Australian Competition and Consumer Commission (ACCC) was appointed as the lead agency responsible for implementing and enforcing the CDR. The ACCC worked closely with industry stakeholders, including banks, fintech companies, and consumer advocacy groups, to develop the necessary framework for Open Banking.

The implementation of Open Banking in Australia was scheduled in multiple phases. The first phase, known as “Open Banking – Product Reference Data,” commenced in July 2020. It required the four major banks – ANZ, Commonwealth Bank, National Australia Bank, and Westpac – to share their product data, including interest rates and fees, with accredited third-party providers.

The second phase, “Open Banking – Consumer Data Right,” began in February 2021. It expanded the scope of Open Banking to include the sharing of more detailed customer information, such as account transaction data and customer details, with accredited third parties upon customer consent.

The CDR implementation required banks to develop and maintain secure Application Programming Interfaces (APIs) to facilitate the seamless transfer of customer data to authorized third-party providers. The APIs ensure data security and compliance with regulations, making data sharing more efficient and secure.

The journey towards Open Banking has not been without its challenges. The complexity of data sharing, ensuring robust cybersecurity provisions, and developing a fair and competitive environment for all stakeholders posed significant hurdles in the implementation process.

However, these challenges were met with an overarching commitment to enhance customer experience and promote a more dynamic, innovative banking sector. Industry collaboration, regulatory oversight, and ongoing consultation with stakeholders have been critical in driving the Open Banking agenda forward.

The phased approach to Open Banking implementation allowed for iterative learning and continuous improvement. Feedback and insights gathered during the initial phases were used to refine the framework and address any issues or concerns that arose.

Looking ahead, the future of Open Banking in Australia holds great promise. The ongoing expansion of the CDR to other sectors, such as energy and telecommunications, further reinforces the government’s commitment to empowering consumers through data rights.

As Open Banking continues to evolve, we can expect to see increased innovation, competition, and customer-centric solutions emerging in the financial industry. The ability for individuals to easily access and share their banking data will unlock new opportunities for fintech companies and other financial service providers.

With proper data protection measures in place, Open Banking has the potential to revolutionize the way individuals and businesses interact with their financial information, enabling greater financial control, choice, and convenience.

What is Open Banking?

Open Banking refers to a system that allows individuals and businesses to securely share their financial data with authorized third-party providers, such as fintech companies and other financial institutions. It is an initiative aimed at enhancing competition, innovation, and customer choice in the banking industry.

At its core, Open Banking is built on the principle that individuals should have control over their own financial information. It empowers customers by granting them the ability to access and share their banking data, including transaction history, account details, and financial products, with other trusted providers of their choosing.

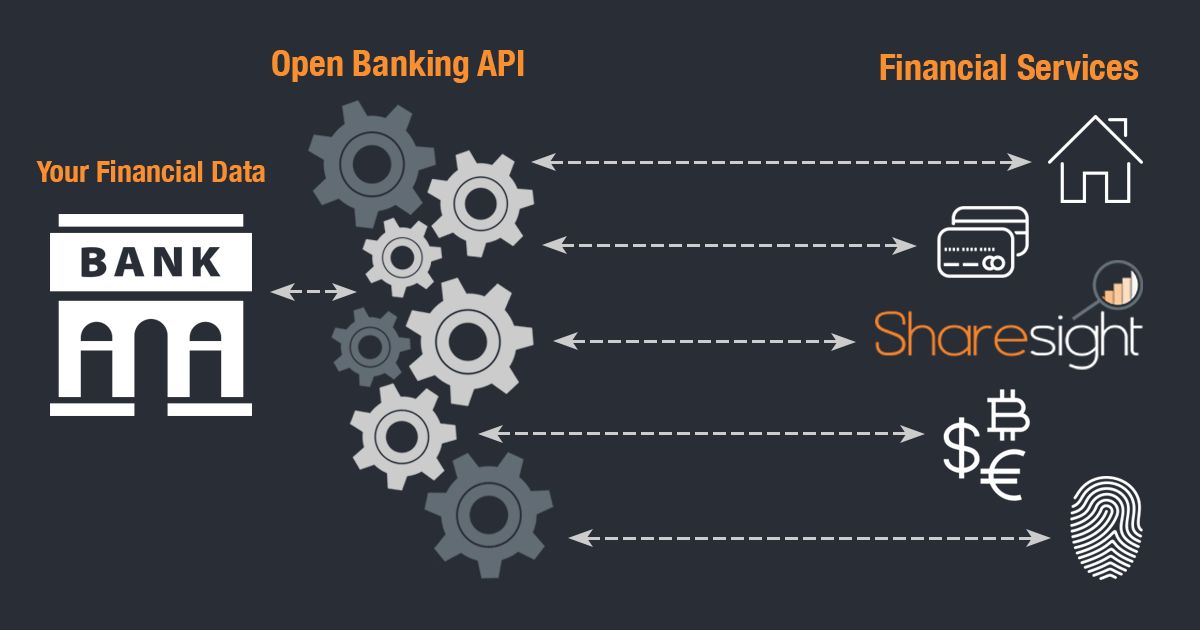

The foundation of Open Banking lies in the use of Application Programming Interfaces (APIs), which enable the secure and standardized transfer of data between banks and third-party providers. APIs act as intermediaries, facilitating the seamless flow of information while maintaining data protection and privacy.

Through Open Banking, customers have the opportunity to benefit from a range of personalized and tailored financial products and services. Third-party providers can leverage customer data to offer innovative solutions, such as budgeting tools, personalized recommendations, and streamlined loan applications, all designed to meet the unique needs and preferences of individual users.

One of the key features of Open Banking is the concept of “consent-based data sharing.” Customers have full control over their data and must provide explicit consent for its sharing. This ensures that individuals have complete transparency and control over who can access their financial information and for what purpose.

Open Banking is not limited to individuals alone; businesses can also take advantage of this initiative. Small and medium-sized enterprises (SMEs) can benefit from improved access to financial services, such as lending and cash flow management, through Open Banking-enabled platforms.

Furthermore, Open Banking promotes competition in the banking industry by breaking down the traditional barriers to entry for fintech companies and other innovative players. It allows for the creation of new, customer-centric financial products and services, challenging the monopoly held by traditional banks and empowering customers with more choices.

In Australia, the implementation of Open Banking is driven by the Consumer Data Right (CDR), which grants individuals the right to access and share their banking data. The CDR provides a regulatory framework that ensures data security, privacy, and customer control, safeguarding individuals’ interests in the Open Banking ecosystem.

Overall, Open Banking represents a significant shift in the financial industry, enabling greater transparency, competition, and customer empowerment. It harnesses the power of technology to unlock the immense value of banking data, leading to a more innovative, customer-centric, and accessible financial system.

Benefits of Open Banking

Open Banking offers a myriad of benefits for individuals, businesses, and the overall banking ecosystem. By providing individuals with greater control and access to their financial data, Open Banking fosters competition, drives innovation, and enhances customer experience in the following ways:

- Increased competition: Open Banking opens up the banking industry to new players, such as fintech companies and technology startups. This increased competition encourages traditional banks to innovate and offer better products and services to attract and retain customers. Consumers benefit from a wider range of options and more competitive pricing.

- Enhanced customer experience: Open Banking enables individuals to access and manage their financial information through a single platform. This streamlines the banking experience, allowing customers to view multiple accounts, make transfers, and analyze their spending habits in one place. With Open Banking-enabled applications, users can also benefit from personalized recommendations, budgeting tools, and tailored financial advice to improve their financial well-being.

- Improved access to credit: Open Banking allows consumers to securely share their financial data with lenders, simplifying and expediting the loan application process. By having access to a more comprehensive picture of a customer’s financial situation, lenders can make better-informed decisions, leading to greater access to credit for individuals and businesses that may have previously been underserved.

- Increased financial transparency: Open Banking promotes transparency by providing customers with real-time access to their financial information. This empowers individuals to monitor their accounts, spot fraudulent activities, and track their spending more effectively. It also encourages financial institutions to be more transparent with their fees, charges, and interest rates, as this information becomes more readily available for comparison.

- Personalized financial products and services: Open Banking fosters the development of personalized and tailored financial products and services. With customer consent, third-party providers can access banking data and create offerings that cater to individual needs and preferences. This includes targeted savings plans, investment recommendations, and customized insurance packages, providing customers with more relevant and valuable financial solutions.

- Efficient account switching: Open Banking simplifies the process of changing banks by enabling the secure transfer of customer data. With Open Banking, individuals can switch their bank accounts more seamlessly, without the hassle of manually transferring direct debits and standing orders. This encourages individuals to seek better deals and services without the fear of being tied down to their current bank.

These benefits of Open Banking contribute to a more customer-centric and competitive financial industry, where individuals have greater control over their financial information and access to innovative and tailored financial solutions. As the Open Banking ecosystem continues to evolve, we can expect to see even more benefits and positive changes in the way we interact with our financial data.

How Open Banking works in Australia

In Australia, Open Banking operates under the Consumer Data Right (CDR) framework, which grants individuals the right to access and share their banking data with authorized third-party providers. The implementation of Open Banking in Australia follows a structured process to ensure data security, privacy, and consumer protection.

Open Banking in Australia is implemented in a phased approach to gradually expand the scope of data sharing and enable a smooth transition for banks and third-party providers. The implementation is overseen by the Australian Competition and Consumer Commission (ACCC), the regulatory body responsible for the CDR.

The first phase, known as “Open Banking – Product Reference Data,” was launched in July 2020. The four major banks – ANZ, Commonwealth Bank, National Australia Bank, and Westpac – are required to share their product data, such as interest rates, fees, and terms and conditions, with accredited third-party providers. This phase allows consumers to compare products and make informed decisions based on transparent and easily accessible information.

The second phase, “Open Banking – Consumer Data Right,” began in February 2021. It expands the scope of Open Banking to include the sharing of more detailed customer information, such as account transaction data, customer details, and account balances. Customers can safely share their data with accredited third-party providers upon explicit consent.

For Open Banking to work effectively, banks and other financial institutions are required to develop and maintain secure Application Programming Interfaces (APIs). APIs act as intermediaries, allowing authorized third-party providers to securely access customer data with customer consent. These APIs facilitate the standardized and secure transfer of data, maintaining data protection and privacy.

In order to access banking data, third-party providers must gain accreditation from the ACCC. Accreditation ensures that these providers meet certain criteria, including data security and privacy standards, customer consent frameworks, and compliance with relevant regulations.

Individuals have full control over their data in the Open Banking ecosystem. They can choose which third-party providers can access their data, grant and revoke access at any time, and determine the duration of access. This customer-centric approach ensures that individuals have complete transparency and control over the sharing of their financial information.

Data security and privacy are paramount in the Open Banking framework. Banks and third-party providers are required to adhere to strict security protocols, ensuring that customer data is protected from unauthorized access, breaches, or misuse. Regular monitoring and assessments are conducted to maintain compliance and address any potential security risks.

Additionally, Open Banking in Australia is subject to ongoing oversight and regulation. The ACCC monitors compliance, investigates complaints, and enforces penalties for non-compliance. This regulatory framework ensures that Open Banking operates in a fair and transparent manner, safeguarding consumer interests and promoting trust in the system.

Overall, Open Banking in Australia operates through the secure sharing of data via APIs, with customer consent and accreditation of third-party providers. This framework promotes competition, innovation, and customer control, allowing individuals to access a wider range of financial services and make more informed decisions regarding their finances.

Key Players in Open Banking

Open Banking involves collaboration between various stakeholders, each playing a crucial role in shaping and implementing the framework. The key players in Open Banking include:

- Banks: Traditional banks are the primary data holders in Open Banking. They are responsible for securely storing and managing customer data. Banks are also required to develop and maintain secure Application Programming Interfaces (APIs) to facilitate the secure transfer of data to authorized third-party providers.

- Third-party providers: These are the entities that leverage customer data obtained through Open Banking to provide innovative financial products and services. Third-party providers may include fintech companies, startups, technology companies, and even established financial institutions. They must be accredited by the regulatory body to access and use the banking data.

- Regulatory bodies: In Australia, the Australian Competition and Consumer Commission (ACCC) is the regulatory body responsible for implementing and enforcing the Consumer Data Right (CDR) framework. They oversee the compliance of banks and third-party providers with data security, privacy, and consumer protection regulations.

- Consumer advocacy groups: These organizations advocate for the interests and rights of consumers in Open Banking. They engage in policy discussions, provide consumer education, and work to ensure that Open Banking operates in a fair and transparent manner, ultimately benefiting consumers.

- Technology providers: Technology companies play a vital role in developing the infrastructure and tools necessary for Open Banking implementation. They provide the technological solutions, including APIs, data storage, security systems, and data analytics, that enable the smooth and secure transfer of data between banks and third-party providers.

- Government and policymakers: The government and policymakers play a significant role in shaping the regulatory environment for Open Banking. They establish the legal and regulatory framework, oversee its implementation, and ensure that consumer rights and data privacy are protected.

Collaboration between these key players is essential for the successful implementation of Open Banking. Banks ensure the secure storage and transfer of customer data, while third-party providers leverage the data to deliver innovative financial solutions. Regulatory bodies and consumer advocacy groups work to protect consumer rights and ensure compliance with regulations, while technology providers offer the necessary infrastructure and tools for seamless data sharing.

The interaction and cooperation between these stakeholders result in a dynamic and competitive Open Banking ecosystem that benefits customers, fosters innovation, and promotes a customer-centric approach to financial services.

Consumer Rights and Protections in Open Banking

Consumer rights and protections are of paramount importance in the Open Banking ecosystem. The implementation of Open Banking in Australia is built on a robust framework to safeguard individuals’ data security, privacy, and control over their financial information.

Here are some key consumer rights and protections in Open Banking:

- Consent-based data sharing: Consumers have complete control over their data in Open Banking. They must provide explicit consent for their information to be shared with third-party providers. This consent can be granted or revoked at any time, enabling consumers to maintain control over who can access their financial data and for what purpose.

- Data privacy and security: Robust measures are in place to ensure the privacy and security of consumer data. Banks and third-party providers are required to adhere to strict data protection standards and employ secure data transfer protocols. Regular monitoring and assessments are conducted to identify and mitigate any potential security risks.

- Transparency and accountability: Open Banking promotes transparency and accountability in the financial industry. Banks and third-party providers are required to be transparent about the data they collect, how it is used, and who has access to it. This enables consumers to make informed decisions and have confidence in the handling of their data.

- Regulatory oversight: The Australian Competition and Consumer Commission (ACCC) is responsible for regulating and overseeing Open Banking. They monitor compliance, investigate complaints, and enforce penalties for non-compliance. This regulatory oversight ensures that consumer rights are protected and that Open Banking operates in a fair and transparent manner.

- Redress mechanisms: In the event of any issues or disputes, consumers have access to redress mechanisms. They can lodge complaints with the relevant authorities or seek resolution through established dispute resolution processes. These mechanisms provide consumers with avenues to address any concerns or grievances related to their data and the services provided through Open Banking.

- Education and awareness: Consumer education and awareness play a crucial role in Open Banking. Initiatives are in place to inform and educate individuals about their rights, the benefits of Open Banking, and how to protect their data. This empowers consumers to make informed choices and ensures they understand the risks and benefits associated with sharing their financial information.

The consumer rights and protections in Open Banking are designed to give individuals control, transparency, and confidence in the use of their financial data. The framework is continually evaluated and enhanced to adapt to evolving technologies, emerging risks, and changing consumer needs.

It is important for consumers to stay informed about their rights and responsibilities in Open Banking. By understanding the protections in place and being proactive in managing their data, individuals can fully realize the benefits of Open Banking while maintaining control over their personal and financial information.

Challenges and Concerns in Open Banking

While Open Banking offers numerous benefits, it also presents certain challenges and concerns that need to be addressed to ensure its successful implementation and widespread adoption. Some of the key challenges and concerns in Open Banking include:

- Data security and privacy: With the increased sharing of financial data, ensuring robust data security and privacy becomes paramount. It is crucial to have stringent measures in place to protect consumer data from unauthorized access, data breaches, and misuse. Continuous monitoring, strong encryption, and compliance with data protection regulations are essential to address these concerns.

- Consent management: The management of consents for data sharing can be complex. It is important to establish clear and user-friendly consent mechanisms to ensure that individuals understand and have control over the access and use of their data. There is a need for standardized consent frameworks that are easily understood by consumers and implemented consistently across different providers.

- Technical interoperability: Open Banking relies on the use of APIs to facilitate data sharing between banks and third-party providers. Ensuring seamless interoperability and compatibility of APIs across different systems and institutions can be a technical challenge. Standardization and collaboration among industry players are crucial to address this challenge effectively.

- Fraud and cybersecurity risks: Open Banking introduces new avenues for fraudsters and cybercriminals to exploit vulnerabilities in the system. Banks and third-party providers must strengthen their cybersecurity measures and adopt robust authentication mechanisms to protect against data breaches and unauthorized access. Ongoing monitoring and collaboration with cybersecurity experts are necessary to stay ahead of emerging threats.

- Customer trust and confidence: Building trust and confidence among consumers is essential for the success of Open Banking. Concerns about data security, privacy, and potential misuse of personal information can undermine trust in the system. Transparent communication, effective privacy policies, and continuous education about the benefits and safeguards of Open Banking are necessary to address these concerns and foster consumer confidence.

- Regulatory compliance: Compliance with the regulatory framework, including data protection and consumer rights, is crucial for the successful implementation of Open Banking. Banks and third-party providers need to ensure that they meet the requirements imposed by regulatory bodies, maintain accurate records, and handle customer data ethically and responsibly.

Addressing these challenges and concerns requires collaboration among banks, third-party providers, regulators, and consumer advocacy groups. Ongoing dialogue, regular risk assessments, and continuous improvement of security measures and industry standards are essential to mitigate risks and build a safe and trusted Open Banking ecosystem.

Open Banking is an evolving landscape, and challenges will continue to arise as technology advances and consumer expectations change. However, with comprehensive measures in place, strong industry collaboration, and continuous monitoring and adaptation, these challenges can be overcome, leading to a secure and customer-centric Open Banking environment.

Future of Open Banking in Australia

The future of Open Banking in Australia holds immense potential for transformative changes in the financial industry. As the ecosystem evolves and matures, we can expect to see several key developments:

- Innovation and new opportunities: Open Banking serves as a catalyst for innovation, fostering the development of new financial products and services. With increased access to customer data, fintech companies, startups, and established financial institutions will continue to leverage this information to create innovative solutions tailored to individual needs. We can anticipate the emergence of new and improved services, such as personalized financial planning tools, smart budgeting apps, and innovative lending products.

- Expansion beyond banking: While Open Banking primarily focuses on banking data, it is likely to expand into other sectors, such as energy, telecommunications, and insurance. This will enable individuals to have greater control over their data in various aspects of their lives. The expansion of the Consumer Data Right (CDR) beyond banking will empower consumers to access and share their data across multiple industries, leading to a more comprehensive and interconnected ecosystem.

- Collaboration and partnerships: Open Banking thrives on collaboration between traditional banks, fintech companies, and other industry players. We can expect to see an increase in partnerships and collaborations between banks and third-party providers to deliver innovative solutions and enhance customer experiences. Traditional banks may explore strategic alliances with fintech companies to leverage their agility and creativity, while fintech companies can benefit from the established customer base and infrastructure of traditional banks.

- Greater financial inclusion: Open Banking has the potential to drive greater financial inclusion by increasing access to financial services for underserved populations. With more comprehensive and real-time data, lenders can make more informed decisions when assessing creditworthiness, resulting in increased access to credit for individuals and businesses with limited credit histories. Open Banking can also unlock opportunities for financial education and guidance, helping consumers make more informed and responsible financial decisions.

- International collaboration: Open Banking is a global phenomenon, with countries around the world implementing similar frameworks. Australia’s experience and expertise in Open Banking can lead to increased international collaboration, knowledge exchange, and harmonization of standards. This collaboration can drive innovation, create cross-border financial services, and benefit consumers and businesses globally.

While the future of Open Banking is promising, it is essential to address ongoing challenges and concerns, such as data security, privacy, and consumer trust. Ongoing regulatory oversight, industry collaboration, and continuous improvement of security measures and privacy frameworks will be vital to ensure the long-term success and sustainability of Open Banking.

As Open Banking continues to evolve, it is crucial for individuals to stay informed, embrace the opportunities presented, and understand their rights and responsibilities within the framework. Open Banking has the potential to foster a more inclusive, innovative, and customer-centric financial industry, enhancing financial well-being and empowering individuals to have greater control over their financial lives.

Conclusion

Open Banking is transforming the banking landscape in Australia, ushering in a new era of increased competition, innovation, and consumer empowerment. With the implementation of the Consumer Data Right (CDR), individuals now have greater control over their financial information and can securely share it with trusted third-party providers.

The benefits of Open Banking are far-reaching. It promotes competition among financial institutions, leading to better products, more competitive pricing, and improved customer experiences. Open Banking also enables personalized financial solutions, empowering individuals to make more informed decisions about their money.

Implementing Open Banking comes with its challenges. Data security and privacy remain top concerns, requiring ongoing vigilance, robust security measures, and regulatory oversight. Consenting mechanisms and interoperability of technical systems also need to be addressed to ensure seamless data sharing.

The future of Open Banking in Australia is promising. We can anticipate continued innovation, expansion of services beyond banking, partnerships between traditional banks and fintech companies, and increased international collaboration. Moreover, Open Banking holds the potential to drive greater financial inclusion by providing more access to credit and financial services for underserved populations.

As Open Banking evolves, it is crucial for consumers to stay informed, exercise their rights, and be responsible participants in the ecosystem. Education, transparency, and ongoing consumer advocacy will be key to building trust and ensuring that Open Banking operates in a fair and consumer-centric manner.

In conclusion, Open Banking is reshaping the financial industry in Australia. It brings opportunities for greater choice, convenience, and customized financial solutions. By fostering competition, driving innovation, and empowering individuals, Open Banking is paving the way for a more accessible, inclusive, and customer-centered financial ecosystem.