Introduction

The world of banking has undergone a significant transformation over the years, as advancements in technology and shifts in consumer demands have compelled the industry to adapt and innovate. One such innovation that has gained traction in recent years is Open Banking. This revolutionary concept has the potential to reshape the way we manage our finances, offering increased convenience, security, and control to consumers.

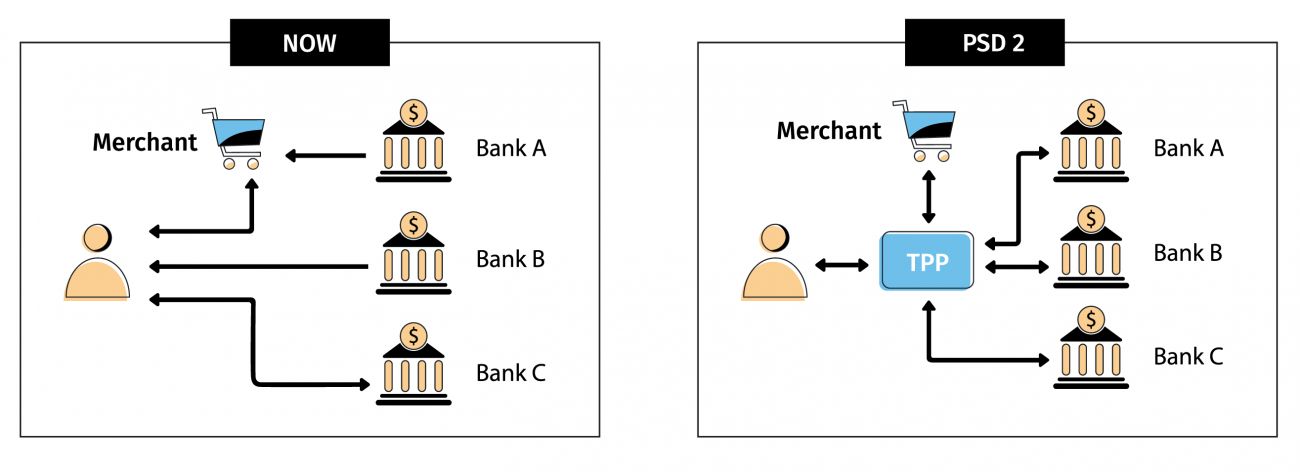

Open Banking is a term used to describe the practice of sharing financial information between banks and authorized third-party providers (TPPs). This sharing of data is made possible through the use of application programming interfaces (APIs), which allow secure and controlled access to users’ account information.

By embracing Open Banking, financial institutions are opening up their systems and data to external parties, enabling them to develop innovative products and services that meet the evolving needs of customers. This collaboration between banks and TPPs fosters competition and encourages the creation of a vibrant ecosystem that benefits both consumers and businesses.

At the heart of Open Banking is the principle of customer consent. Users have complete control over their data and must explicitly authorize the sharing of their financial information with TPPs. This ensures that their data is protected and used only for the purposes they have consented to.

Open Banking is not a new concept. It gained prominence in Europe with the introduction of the revised Payment Services Directive (PSD2) in 2018. However, for a better understanding, it is essential to first explore the origins and foundations of Open Banking by delving into its predecessor, PSD1.

What is Open Banking?

Open Banking is a groundbreaking concept that enables customers to share their financial data securely with authorized third-party providers (TPPs) through the use of application programming interfaces (APIs). This sharing of data allows TPPs to develop innovative products and services that enhance the banking experience for customers.

At its core, Open Banking aims to give individuals greater control over their financial information and empower them to make more informed decisions about their money. By enabling customers to share their data with trusted TPPs, Open Banking facilitates the development of personalized financial solutions that cater to individual needs and preferences.

Open Banking is not just about sharing data; it also encompasses the concept of interoperability. This means that an individual can securely connect their financial accounts from different institutions and view them all in one place through a preferred platform or app. This seamless integration of financial accounts provides a comprehensive overview of one’s financial standing, making it easier to manage finances and track spending.

One of the foundational principles of Open Banking is customer consent. Users have full control over their data and must explicitly grant permission for TPPs to access their financial information. This ensures that individuals have complete privacy and control over how and when their data is used. Additionally, Open Banking adheres to robust security standards, utilizing encryption and other measures to protect the confidentiality of customer data.

Open Banking also promotes competition within the banking industry. By allowing TPPs to access customer data, it encourages innovation and the development of new products and services. This increased competition benefits consumers by driving down costs, improving the quality of services, and offering a wider range of options to choose from.

Overall, Open Banking represents a significant shift in the banking landscape, placing control back into the hands of the customers. By fostering collaboration between banks and TPPs, it paves the way for a more connected, secure, and personalized banking experience.

Key Features of Open Banking

Open Banking comes with a range of features that enhance the banking experience for consumers and promote competition within the industry. Understanding these key features is essential to appreciate the transformative impact that Open Banking can have on the way we manage our finances.

Secure Data Sharing: One of the fundamental principles of Open Banking is the secure sharing of financial data. Through the use of robust authentication and encryption methods, customers can grant authorized third-party providers (TPPs) access to their financial information while ensuring the privacy and security of their data.

Customer Consent: Open Banking is built on the principle of customer consent. Individuals have complete control over their data and must explicitly provide consent for TPPs to access their financial information. This ensures that customers have the final say in how their data is used and gives them peace of mind knowing that their privacy is protected.

Enhanced Financial Insights: Open Banking enables individuals to gain a deeper understanding of their financial health. By securely connecting their accounts from different institutions, users can access consolidated financial information, including transactions, balances, and spending patterns. This comprehensive overview allows for better financial planning, budgeting, and decision-making.

Personalized Financial Services: Open Banking opens the door to personalized financial services tailored to individual needs and preferences. With access to customer data, TPPs can develop innovative solutions such as budgeting tools, savings apps, and specialized loan offerings. These personalized services empower customers to make more informed financial decisions.

Seamless Account Aggregation: Open Banking allows for seamless integration of financial accounts from different institutions. Customers can view all their account information in one place, whether it’s checking accounts, credit cards, or investment portfolios. This simplifies financial management and eliminates the need to log in to multiple platforms or apps.

Increased Competition and Innovation: Open Banking promotes competition within the banking sector. By enabling TPPs to access customer data, it encourages innovation and the development of new and improved financial products and services. This competition benefits consumers by providing more choices, better pricing, and enhanced customer experiences.

Improved Payment Solutions: Open Banking has the potential to revolutionize the way we make payments. With the ability to securely share financial data, individuals can authorize payments directly from their bank accounts using third-party apps. This streamlines the payment process and introduces new convenient payment options.

These key features highlight the transformative potential of Open Banking. By leveraging secure data sharing, customer consent, and personalized financial services, Open Banking is reshaping the way we manage our money and unlocking new opportunities for individuals and businesses alike.

Benefits of Open Banking

Open Banking offers a plethora of benefits for both consumers and businesses, revolutionizing the way banking services are provided and accessed. By enabling secure data sharing and encouraging collaboration between financial institutions and authorized third-party providers (TPPs), Open Banking brings about numerous advantages that enhance the overall banking experience.

Enhanced Financial Control: Open Banking puts customers in control of their financial data. With the ability to securely share their information with trusted TPPs, individuals can access personalized financial services, better manage their finances, and make more informed decisions about their money. This empowerment promotes financial literacy and helps individuals achieve their financial goals.

Improved Convenience: Open Banking simplifies the banking experience by integrating accounts from various institutions into a single interface or application. This eliminates the need to switch between multiple banking apps or websites, streamlining financial management and providing a seamless user experience.

Increased Transparency: Open Banking fosters transparency by giving customers greater visibility into their financial transactions and fees. By being able to access and review their financial data through third-party apps, individuals can easily identify any irregularities or hidden charges and take appropriate actions. This transparency builds trust between banks, TPPs, and customers, fostering a healthier banking ecosystem.

Greater Competition: Open Banking promotes competition within the banking industry. With TPPs gaining access to customer data, they can develop innovative solutions that offer better pricing, improved products, and enhanced customer experiences. This competition benefits consumers by providing more options, driving down costs, and stimulating innovation.

Personalized Financial Solutions: Open Banking enables the development of personalized financial services tailored to individual needs. By leveraging customer data, TPPs can offer customized budgeting tools, investment advice, and mortgage solutions. This personalization enhances the overall banking experience, ensuring that individuals receive the specific financial services that meet their unique requirements.

Efficient Account Switching: Open Banking simplifies the process of switching banks. Instead of filling out lengthy forms and providing paper documentation, customers can authorize trusted TPPs to securely transfer their financial data from one institution to another. This makes the switch seamless and hassle-free, encouraging individuals to explore better banking options.

Stimulated Innovation: Open Banking fosters a culture of innovation within the banking industry. By allowing TPPs to access customer data, it encourages the development of new and creative financial products, services, and technologies. This leads to continuous improvement and establishes a dynamic ecosystem that benefits both consumers and businesses.

Enhanced Financial Security: Open Banking prioritizes data security and privacy. Financial institutions and TPPs must adhere to strict security standards and protocols to ensure the confidentiality and integrity of customer data. Additionally, customer consent is a core principle of Open Banking, giving individuals full control over how their data is used and shared.

Overall, Open Banking offers an array of benefits that transform the traditional banking landscape. From improved financial control and convenience to enhanced transparency and innovation, Open Banking empowers individuals and businesses alike, creating a more customer-centric and dynamic banking experience.

What is PSD1?

The Payment Services Directive 1 (PSD1) was a directive introduced by the European Union (EU) in 2007 to establish a legal framework for payment services within the European Economic Area. It aimed to harmonize payment regulations across member states and enhance the efficiency, innovation, and security of payment services.

PSD1 defined payment services as activities related to the execution, initiation, or processing of payment transactions, including money transfers, direct debits, and card payments. It introduced several key provisions and requirements for payment service providers (PSPs) operating within the EU.

Licensing: PSD1 introduced a licensing regime for payment service providers. PSPs were required to obtain authorization from their national competent authority before providing payment services. This licensing requirement ensured that only legitimate, trustworthy, and compliant entities could engage in payment activities.

Access to Payment Systems: PSD1 aimed to promote equal access to payment systems for PSPs, fostering competition and innovation in the payment services market. It prohibited unfair access practices and discrimination against non-bank PSPs, enabling them to compete on a level playing field with traditional banking institutions.

Consumer Protection: PSD1 put a strong emphasis on consumer protection. It introduced provisions to ensure transparency in pricing, fees, and terms and conditions for payment services. PSPs were required to provide clear and comprehensive information to customers, enabling them to make informed decisions and understand the cost and risks associated with payment services.

Security Requirements: PSD1 mandated that PSPs implement security measures to protect customer funds and personal data. It required PSPs to establish fraud prevention systems, secure authentication protocols, and strong data protection measures. These security requirements aimed to safeguard the integrity and confidentiality of payment transactions and promote user trust in the payment ecosystem.

Dispute Resolution: PSD1 established clear procedures for resolving disputes between PSPs and their customers. It introduced an effective and transparent dispute resolution mechanism, ensuring that customers had access to fair and efficient procedures to address payment-related issues.

While PSD1 was a significant step towards harmonizing payment services regulations in the EU, it became clear that further improvements were needed to keep up with technological advancements and emerging market trends. As a result, the EU introduced the revised Payment Services Directive (PSD2) in 2018 to build upon the foundations laid by PSD1 and address new challenges and opportunities in the payment industry.

Key Provisions of PSD1

The Payment Services Directive 1 (PSD1) introduced several key provisions and requirements for payment service providers (PSPs) operating within the European Economic Area (EEA). These provisions aimed to harmonize payment regulations, enhance consumer protection, foster competition, and promote the security and efficiency of payment services.

Licensing and Authorization: PSD1 established a licensing regime for PSPs. It mandated that PSPs obtain authorization from their national competent authorities before providing payment services. This requirement ensured that only reputable and compliant entities could engage in payment activities, providing a basic level of trust and security for consumers.

Access to Payment Systems: PSD1 promoted equal and non-discriminatory access to payment systems for payment service providers. It prohibited unfair access practices and discriminatory behavior, ensuring that non-bank PSPs had access to necessary infrastructure and systems to compete with traditional banking institutions. This provision fostered competition and innovation in the payment services market.

Security Requirements: PSD1 mandated that PSPs implement robust security measures to protect customer funds and personal data. It required PSPs to establish effective fraud prevention systems, secure authentication protocols, and strong data protection measures. These security requirements aimed to safeguard the integrity and confidentiality of payment transactions, protecting consumers from fraudulent activities and enhancing their trust in payment services.

Consumer Protection: PSD1 placed a strong emphasis on consumer protection within the payment services industry. It introduced provisions to ensure transparent pricing, fees, and terms and conditions for payment services. PSPs were required to provide clear and comprehensive information to their customers, enabling them to make informed decisions and understand the costs and risks associated with payment services. These consumer protection measures aimed to enhance the transparency and fairness of the payment ecosystem.

Dispute Resolution: PSD1 established clear procedures for resolving disputes between PSPs and their customers. It mandated that PSPs provide an effective and transparent dispute resolution mechanism, ensuring that consumers had access to fair and efficient procedures to address payment-related issues. This provision protected the rights and interests of consumers, promoting trust and confidence in the payment services sector.

Transparency and Disclosure: PSD1 required PSPs to provide clear and comprehensive information to their customers regarding payment transactions, fees, exchange rates, and terms and conditions. These disclosure requirements aimed to enhance transparency and enable consumers to make informed decisions when using payment services. PSPs were obligated to provide pre-contractual information and regular transaction statements to ensure transparency and accountability.

Cross-Border Transactions: PSD1 facilitated cross-border payment services within the EEA by removing unnecessary barriers and simplifying authorization procedures. It introduced a framework for the harmonization of payment regulations between EEA member states, streamlining cross-border transactions and promoting the integration of the European payment market.

These key provisions of PSD1 laid the foundation for a harmonized, secure, and consumer-friendly payment services environment within the EEA. However, to address emerging challenges and developments in the payment industry, the EU introduced the revised Payment Services Directive (PSD2) in 2018, which built upon the provisions of PSD1 and further advanced the landscape of payment services in Europe.

The Impact of PSD1 on the Banking Industry

The Payment Services Directive 1 (PSD1) has had a profound impact on the banking industry, revolutionizing the way payment services are provided, accessed, and regulated within the European Economic Area (EEA). PSD1 introduced key provisions that have transformed the landscape of banking and stimulated competition, innovation, and consumer protection.

Promotion of Innovation: PSD1 fostered innovation within the banking industry by encouraging competition and promoting access to payment systems for non-bank payment service providers (PSPs). This opened up opportunities for new market entrants, fintech companies, and startups to offer innovative payment solutions, driving advancements in technology, customer experiences, and financial services as a whole.

Increased Transparency: PSD1 introduced transparency requirements for payment services, ensuring that customers have access to clear and comprehensive information regarding fees, exchange rates, and terms and conditions. This increased transparency promotes consumer confidence, enabling individuals to make informed decisions and compare different payment service providers based on pricing and service quality.

Enhanced Consumer Protection: PSD1 prioritized consumer protection within the banking industry. It mandated that PSPs adhere to strict security protocols, implement fraud prevention measures, and establish effective dispute resolution mechanisms. These requirements aimed to safeguard customers’ funds, personal data, and rights, instilling trust in the payment services ecosystem.

Promotion of Competition: PSD1 played a pivotal role in promoting competition within the banking industry. By granting non-bank PSPs access to payment systems and establishing a framework for fair access, PSD1 encouraged new players to enter the market and compete with traditional banking institutions. This competition led to improved services, greater choice, and more competitive pricing options for consumers.

Harmonization of Payment Regulation: PSD1 aimed to harmonize payment regulations across the EEA member states. This harmonization simplified cross-border payments, removed unnecessary barriers, and facilitated the integration of the European payment market. It created a more unified and efficient payment services landscape, benefiting businesses and consumers engaging in cross-border transactions.

Challenges for Traditional Banks: PSD1 presented challenges for traditional banks, as it opened the door for new entrants and non-traditional players in the payment services market. Banks had to adapt to a more competitive environment and find ways to differentiate their services to retain customers. Many traditional banks embraced collaboration with fintech companies and developed their own innovative payment solutions to stay relevant in the changing landscape.

Overall, PSD1 had a transformative impact on the banking industry within the EEA. It stimulated competition, innovation, and consumer protection, while promoting transparency and harmonization of payment regulations. The legacy of PSD1 laid the groundwork for subsequent regulations, including the revised Payment Services Directive (PSD2), which built upon its foundations and further advanced the payments ecosystem in Europe.

Conclusion

Open Banking, driven by the Payment Services Directive 1 (PSD1), has ushered in a new era of banking and payment services within the European Economic Area (EEA). It has revolutionized the way customers access and manage their financial information, fostering innovation, competition, and consumer protection.

Open Banking enables secure data sharing between financial institutions and authorized third-party providers (TPPs) through the use of application programming interfaces (APIs). This collaboration empowers customers with greater control over their financial data, personalized financial services, and enhanced transparency in the banking industry.

The key features of Open Banking, including secure data sharing, customer consent, personalized financial solutions, and seamless account aggregation, have redefined the banking experience for consumers. It has put the power in the hands of customers, allowing them to manage their finances more efficiently and make informed decisions about their money.

PSD1, as the foundation of Open Banking, introduced critical provisions such as licensing and authorization requirements, access to payment systems, security measures, consumer protection rules, and harmonization of payment regulations. These provisions have shaped the banking industry, fostering innovation, driving competition, and strengthening consumer trust in payment services.

The impact of PSD1 on the banking industry has been significant. It has stimulated innovation, encouraged new entrants, and prompted traditional banks to adapt to evolving customer demands. Moreover, it has led to increased transparency, consumer empowerment, and improved safeguards for customer funds and personal data.

In conclusion, Open Banking and the framework established by PSD1 have transformed the banking landscape within the EEA, delivering benefits to both consumers and businesses. As the banking industry continues to evolve, it is important to build upon the foundations of Open Banking, harnessing technological advancements and regulatory updates to drive further innovation, competition, and consumer-centric solutions in the financial services sector.