What is Fintech?

Fintech, short for financial technology, is a term used to describe the use of innovative technology to deliver financial services. It encompasses a wide range of applications, from mobile payment solutions to online lending platforms and cryptocurrency exchanges. Fintech companies leverage advancements in areas such as cloud computing, artificial intelligence, and blockchain to disrupt traditional financial systems and provide more efficient and convenient services.

One of the key characteristics of fintech is its ability to democratize financial services. Traditional banking and financial institutions have often been inaccessible to certain populations due to various barriers, such as high fees, strict eligibility criteria, and limited physical branch networks. Fintech aims to bridge this gap by providing inclusive and affordable alternatives for financial services.

Fintech innovations have transformed various sectors of the financial industry. For example, mobile payment platforms like PayPal, Venmo, and Alipay have revolutionized how individuals and businesses make transactions. Peer-to-peer lending platforms, such as LendingClub and Prosper, have provided alternative sources of funding for individuals and small businesses. Additionally, cryptocurrencies like Bitcoin have introduced decentralized digital currencies that operate without the need for intermediaries.

The rise of fintech has also prompted traditional financial institutions to embrace technology and adapt their services to meet evolving customer expectations. Many banks now offer mobile banking apps, online investment platforms, and digital wallets to compete with fintech startups.

Overall, fintech is reshaping the financial industry by making it more accessible, efficient, and consumer-centric. It has disrupted traditional models, challenging established players to adapt or risk becoming obsolete. However, with these advancements come the need for appropriate regulations to ensure consumer protection, financial stability, and fair market competition.

The Importance of Fintech Regulation

In the fast-paced world of fintech, regulation plays a crucial role in ensuring the stability and integrity of financial systems. While fintech brings numerous benefits, such as increased accessibility and convenience, it also presents unique risks and challenges that need to be addressed through effective regulation.

One of the key reasons why fintech regulation is important is to protect consumers. Fintech innovations have the potential to revolutionize financial services, but they also introduce new risks and vulnerabilities. Regulations help safeguard consumers by ensuring fair and transparent practices, protecting their personal data, and providing mechanisms for dispute resolution. Without proper regulation, consumers could be exposed to fraud, inadequate protection, or unethical practices.

Another important aspect of fintech regulation is maintaining financial stability. As fintech disrupts traditional financial models, it can cause fluctuations in markets and create new systemic risks. Regulatory frameworks help monitor and manage these risks, ensuring that fintech companies operate in a safe and sustainable manner. By enforcing controls and best practices, regulation can prevent the concentration of risk and promote market stability.

Fintech regulation also promotes fair competition and a level playing field. Startups and established financial institutions compete in the same market, but the latter often faces more stringent regulations. Regulatory frameworks that are adaptable and responsive can encourage innovation while ensuring that large incumbents do not hinder competition. This fosters a healthy ecosystem where new players can thrive and consumers have access to a diverse range of financial services.

Moreover, fintech regulation helps attract investment and foster trust in the industry. Investors are more likely to invest in fintech startups if they feel confident that there are clear rules and mechanisms in place to protect their investments. Regulatory oversight can also enhance the reputation of the industry and foster trust among consumers, who may be hesitant to adopt new technologies without the assurance of regulatory oversight.

Overall, fintech regulation is essential for the sustainable growth of the industry. It provides a framework for innovation, protects consumers, ensures financial stability, promotes fair competition, and builds trust. However, striking the right balance between regulation and innovation is crucial. Regulations should be flexible enough to accommodate new technologies and business models while addressing potential risks and protecting the interests of all stakeholders.

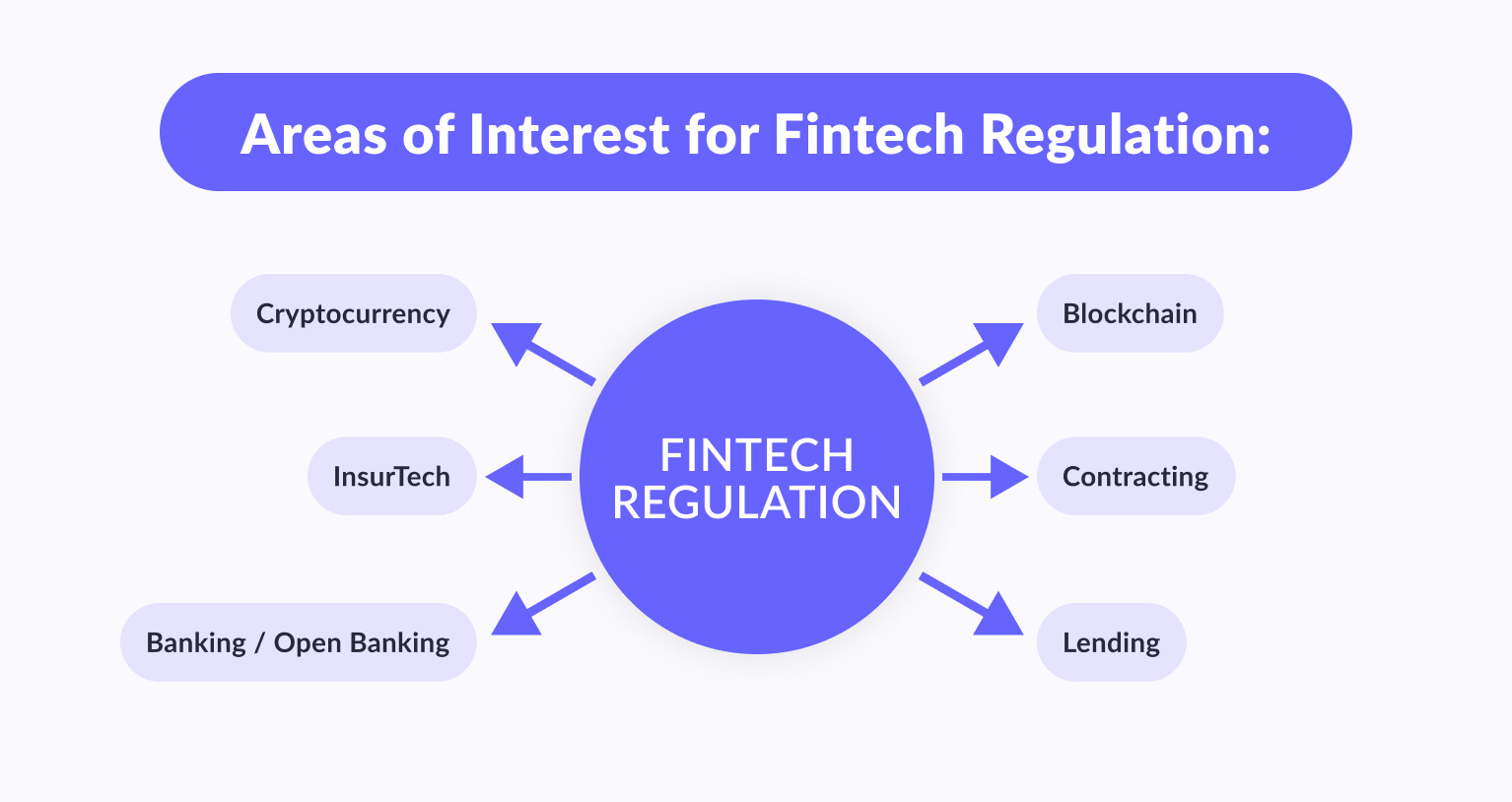

Types of Fintech Regulations

Fintech regulations can take various forms, depending on the jurisdiction and the specific area of financial services being regulated. These regulations aim to provide a clear legal framework for fintech companies and ensure consumer protection, market integrity, and financial stability. Here are some common types of fintech regulations:

1. Licensing and Registration: Many countries require fintech companies to obtain licenses or register with regulatory authorities before offering certain financial services. This helps ensure that companies meet minimum standards of operation, including robust risk management, compliance with anti-money laundering (AML) and know-your-customer (KYC) regulations, and adherence to consumer protection laws.

2. Data Privacy and Security: Fintech companies handle vast amounts of sensitive personal and financial data. Regulations on data privacy and security are crucial to protect consumer information from unauthorized access, breaches, and misuse. These regulations often outline requirements for data encryption, secure storage, and notification procedures in the event of a data breach.

3. Anti-Money Laundering (AML) and Counter-Terrorist Financing (CTF): Fintech companies, especially those involved in payments and remittances, are required to have robust AML and CTF measures in place. These measures aim to prevent money laundering, terrorist financing, and other illicit activities by implementing customer due diligence, transaction monitoring, and reporting suspicious activities to regulatory authorities.

4. Consumer Protection: Regulations pertaining to consumer protection in fintech cover a range of aspects, including fair lending practices, disclosure of fees and terms, dispute resolution mechanisms, and transparency in advertising. These regulations ensure that consumers are treated fairly and have access to accurate information to make informed financial decisions.

5. Crowdfunding and Peer-to-Peer Lending: Fintech platforms that facilitate crowdfunding and peer-to-peer lending activities are often subject to specific regulations. These regulations may include limits on the amount of funds that can be raised, investor eligibility criteria, disclosure requirements, and measures to prevent fraud and misleading practices.

6. Cryptocurrency and Digital Assets: With the rise of cryptocurrencies and digital assets, regulations in this area are evolving rapidly. Some jurisdictions are implementing frameworks to govern the issuance, trading, and custody of cryptocurrencies, with a focus on investor protection, market integrity, and anti-money laundering measures.

7. Open Banking and API Regulations: Open banking initiatives, which allow third-party access to customer banking data through APIs, are being regulated in some jurisdictions. These regulations usually focus on data privacy, consent frameworks, security standards, and liability provisions to ensure a secure and transparent sharing of financial information.

It’s important to note that fintech regulations can vary significantly from one country to another, as well as within different sectors of the financial industry. As fintech continues to evolve and disrupt traditional financial models, regulatory frameworks will need to adapt and respond to emerging challenges and opportunities.

Regulation by Country

Fintech regulation varies from country to country, as each jurisdiction has its own approach to overseeing and governing financial technology activities. Here are some examples of how different countries regulate the fintech industry:

1. United States (US): In the US, fintech regulation is multi-layered, with various federal and state-level regulatory bodies involved. The Office of the Comptroller of the Currency (OCC) oversees fintech companies engaged in banking activities, while the Securities and Exchange Commission (SEC) regulates crowdfunding, digital assets, and securities-related activities. The Consumer Financial Protection Bureau (CFPB) focuses on consumer protection, and the Financial Crimes Enforcement Network (FinCEN) monitors AML and CTF compliance.

2. European Union (EU): The EU has implemented comprehensive fintech regulations through initiatives like the Revised Payment Services Directive (PSD2) and General Data Protection Regulation (GDPR). PSD2 promotes open banking and requires banks to provide access to customer account data through APIs. GDPR ensures data protection and privacy rights for individuals. EU member states also have their own financial regulatory bodies overseeing fintech activities.

3. United Kingdom (UK): The UK has established a regulatory sandbox, allowing fintech startups to test innovative products and services under the supervision of the Financial Conduct Authority (FCA). The FCA also regulates peer-to-peer lending, crowdfunding, and digital currencies. The Bank of England oversees financial stability, and the Information Commissioner’s Office (ICO) enforces data protection regulations.

4. Singapore: Singapore has positioned itself as a fintech hub through proactive regulation. The Monetary Authority of Singapore (MAS) has established a regulatory sandbox to foster innovation. They regulate various aspects of fintech, including payments, digital assets, crowdfunding, and cryptocurrency exchanges. MAS also promotes data protection, cybersecurity, and AML measures.

5. China: China has a unique regulatory landscape for fintech, where regulatory oversight is shared between multiple government agencies. The People’s Bank of China (PBOC) oversees payment systems, while the China Securities Regulatory Commission (CSRC) regulates online lending and crowdfunding platforms. The Cyberspace Administration of China (CAC) focuses on data privacy and cybersecurity, and the Anti-Money Laundering Office (AMLO) monitors AML compliance.

These examples highlight the diverse approaches to fintech regulation across different countries. Some jurisdictions have implemented specific regulations to foster innovation and provide a supportive environment for fintech startups, while others prioritize consumer protection and financial stability. As fintech continues to advance globally, regulatory frameworks will continue to evolve to address the unique challenges and opportunities posed by these technological advancements.

Challenges in Fintech Regulation

Fintech regulation poses several challenges for regulatory bodies, mainly due to the rapid pace of technological advancements and the global nature of the industry. Here are some key challenges faced in fintech regulation:

1. Technological Innovation Outpacing Regulation: Fintech innovation moves at a swift pace, often surpassing the ability of regulatory frameworks to keep up. New technologies, such as blockchain, artificial intelligence, and decentralized finance, introduce novel business models and risks that traditional regulations may not adequately address. Regulatory bodies need to adopt a flexible and adaptive approach to stay abreast of emerging trends and developments.

2. Cross-Border Jurisdictional Challenges: Fintech companies often operate across borders, challenging the effectiveness of regulations confined to national boundaries. The nature of digital transactions and the decentralized nature of technologies like blockchain make it difficult for traditional regulatory frameworks to exert control. Regulatory collaboration and harmonization efforts across jurisdictions are necessary to address these cross-border challenges.

3. Balancing Innovation and Consumer Protection: Fintech regulation should strike a delicate balance between encouraging innovation and ensuring consumer protection. Strict regulations can stifle innovation, creating barriers for startups and limiting competition. On the other hand, insufficient regulation may expose consumers to risks, such as fraud or data breaches. Regulatory bodies must find the right balance to foster innovation while maintaining consumer trust and confidence.

4. Evolving Nature of Risks: Fintech introduces new risks, such as cyber threats, data privacy breaches, and money laundering vulnerabilities. These risks are constantly evolving as new technologies and business models emerge. Regulatory bodies need to stay vigilant and proactive in identifying and mitigating these risks through appropriate regulations, compliance requirements, and oversight mechanisms.

5. Regulatory Fragmentation: In some jurisdictions, fintech regulation is fragmented, with different regulatory bodies responsible for various aspects of fintech activities. This can create overlapping or conflicting regulations, leading to compliance challenges for fintech companies. Harmonizing regulations and establishing clear lines of responsibility is necessary to provide a cohesive regulatory framework that fosters innovation while ensuring compliance.

6. Skills and Expertise Gap: Regulating fintech requires specialized knowledge and technical expertise in areas such as blockchain, cybersecurity, and data analytics. Regulatory bodies often face challenges in recruiting and retaining professionals with the necessary skills to understand and effectively regulate these complex technologies. Investing in training and collaboration with industry experts is crucial to bridge this skills gap.

Addressing these challenges requires collaborative efforts between regulators, industry stakeholders, and policymakers. Regular dialogue, information sharing, and ongoing evaluations of regulatory frameworks are essential to create a regulatory environment that supports innovation, protects consumers, and fosters the sustainable growth of the fintech industry.

Benefits of Fintech Regulation

Fintech regulation brings several benefits that contribute to the growth and stability of the financial technology industry. While regulation is sometimes seen as a hindrance to innovation, when implemented effectively, it can provide a framework that enhances consumer protection, fosters market integrity, and promotes responsible innovation. Here are some key benefits of fintech regulation:

1. Consumer Protection: Fintech regulation exists to safeguard the interests of consumers. It ensures that fintech companies adhere to ethical business practices and operate in a transparent and fair manner. Regulations on data privacy, security, and consumer rights protect individuals from fraud, identity theft, and misuse of personal information. Consumers can have confidence in fintech products and services, fostering trust and promoting wider adoption.

2. Market Integrity: Regulations promote market integrity by establishing rules and standards that foster fair competition and prevent market manipulation. Regulations on disclosure requirements, financial reporting, and risk management ensure that fintech companies operate with transparency and accountability. This helps maintain trust in the financial system and encourages investors to participate in the fintech market.

3. Financial Stability: Fintech regulation plays a crucial role in maintaining the stability of the financial system. Regulations on risk management, capital requirements, and liquidity ensure that fintech companies have adequate safeguards in place to mitigate risks. This reduces the likelihood of financial crises and systemic risks. Regulatory oversight also helps prevent the concentration of risk and promotes a resilient and stable fintech ecosystem.

4. Innovation Encouragement: Contrary to popular belief, fintech regulation can actually encourage and foster innovation. Clear regulatory frameworks provide certainty and guidance for fintech startups, enabling them to navigate the regulatory landscape and attract necessary investment. Regulatory sandboxes and collaborative platforms allow fintech companies to test and refine their products and services in a controlled environment, benefiting both regulators and startups.

5. Investor Confidence: Fintech regulation enhances investor confidence in the industry. Clear rules and regulatory oversight provide assurance to investors that their funds are protected and that they have legal recourse in case of fraud or misconduct. Investor confidence attracts capital, which is vital for the growth and sustainability of fintech startups, allowing them to scale their operations and expand their offerings.

6. Global Standards and Cooperation: International cooperation in fintech regulation promotes harmonization and consistent standards across jurisdictions. This facilitates cross-border fintech activities, opens up new markets, and encourages innovation on a global scale. Common regulatory frameworks also reduce compliance costs for fintech companies operating in multiple countries, enabling them to allocate resources more efficiently.

Overall, fintech regulation provides a framework that supports the growth, stability, and responsible development of the financial technology industry. It protects consumers, ensures market integrity, promotes innovation, and enhances investor confidence. By striking the right balance between regulation and innovation, regulatory bodies can foster an ecosystem that benefits both fintech companies and the consumers they serve.

The Role of Fintech Regulatory Bodies

Fintech regulatory bodies play a crucial role in overseeing and supervising the activities of the fintech industry. Their responsibilities include creating and enforcing regulations, promoting market integrity, protecting consumers, and fostering responsible innovation. Here are some key roles that fintech regulatory bodies fulfill:

1. Regulatory Framework Development: Fintech regulatory bodies are responsible for developing and updating regulatory frameworks that govern fintech activities. They assess the risks and challenges posed by emerging technologies and business models and adapt regulations accordingly. The regulatory frameworks provide guidelines on licensing, compliance requirements, risk management, and consumer protection measures.

2. Licensing and Supervision: Fintech regulatory bodies issue licenses and permits to fintech companies, ensuring that they meet the requirements of operating in the financial services industry. They conduct due diligence assessments to evaluate the fitness and propriety of key individuals within the fintech companies. Supervisory activities include ongoing oversight and monitoring to ensure compliance with regulations and to identify potential risks or weaknesses.

3. Consumer Protection: Fintech regulatory bodies have a responsibility to protect consumers from fraudulent activities, unfair practices, and privacy breaches. They develop and enforce regulations that require fintech companies to maintain adequate safeguards to protect customer data and ensure fair treatment. These bodies may also handle consumer complaints and establish mechanisms for dispute resolution.

4. Market Integrity: Fintech regulatory bodies work to maintain market integrity by preventing fraudulent activities, market manipulation, and ensuring fair competition. They enforce regulations that promote transparency, disclosure requirements, and standards for financial reporting. Market surveillance is conducted to detect and deter potential misconduct, contributing to the integrity and stability of the financial system.

5. Risk Management and Stability: Fintech regulatory bodies play a critical role in managing and mitigating risks within the fintech industry. They establish prudential requirements such as capital adequacy, liquidity, and risk management standards. These regulations are designed to maintain the stability of the financial system and prevent systemic risks that could arise from the activities of fintech companies.

6. Collaboration and International Cooperation: Fintech regulatory bodies often collaborate and engage in international cooperation to tackle cross-border regulatory challenges. They participate in forums, share information with their counterparts from other jurisdictions, and work towards harmonizing regulations. These international efforts facilitate cross-border fintech activities, promote innovation, and ensure consistent standards.

7. Innovation Facilitation: Fintech regulatory bodies aim to foster responsible innovation in the financial technology industry. They often establish regulatory sandboxes or innovation hubs that provide a controlled environment for fintech startups to test their products and services. This allows companies to refine their offerings while providing regulatory bodies with valuable insights to develop appropriate regulations.

In summary, fintech regulatory bodies have a multifaceted role in the fintech industry. They are responsible for creating and enforcing regulations, safeguarding consumers, promoting market integrity, managing risk, and fostering responsible innovation. By fulfilling these roles effectively, they contribute to the growth, stability, and sustainability of the fintech ecosystem.

Future Trends in Fintech Regulation

The dynamic nature of the fintech industry calls for continuous evolution and adaptation of regulatory frameworks. As technology continues to advance and new fintech innovations emerge, several future trends in fintech regulation are expected to shape the regulatory landscape. Here are some key trends to watch:

1. Regulatory Sandboxes: Regulatory sandboxes have gained popularity in recent years and are expected to become more prevalent in the future. These controlled environments allow fintech startups to test their products and services without facing full regulatory requirements immediately. Regulatory sandboxes enable regulators to understand new technologies and business models while providing startups with guidance and the opportunity to refine their offerings.

2. International Collaboration: Fintech regulation is increasingly becoming a global challenge due to the cross-border nature of fintech activities. Future trends in fintech regulation will likely see an increase in international collaboration and cooperation among regulatory bodies. This includes sharing best practices, harmonizing regulatory approaches, and exchanging information to address regulatory challenges posed by fintech companies with a global presence.

3. Robust Data Protection Regulations: With the increasing reliance on data in the fintech industry, data protection regulations are expected to become more stringent and comprehensive. Regulators will focus on enhancing data privacy, consent mechanisms, and ensuring secure storage and transmission of personal and financial information. Stricter regulations will be crucial to address concerns related to data breaches, identity theft, and unauthorized access to consumer data.

4. Enhancing Cybersecurity Measures: As fintech companies become appealing targets for cybercriminals, regulators will place a greater emphasis on cybersecurity measures. Fintech regulations will require companies to implement robust cybersecurity frameworks, incident response plans, and regular vulnerability assessments. Regulators may also establish cybersecurity standards and promote information sharing on emerging cyber threats.

5. Regulating Artificial Intelligence (AI) and Machine Learning (ML): The increasing use of AI and ML in fintech applications presents unique challenges for regulators. Future trends in fintech regulation will involve setting guidelines and standards for the ethical and responsible use of these technologies. Regulators will need to address fairness, explainability, and accountability in algorithms, as well as potential biases in AI-powered decision-making processes.

6. Distributed Ledger Technology (DLT) Regulations: The adoption of blockchain and other distributed ledger technologies will require specific regulations to address their unique characteristics. Regulators may focus on creating frameworks for digital asset custody, smart contracts, and initial coin offerings (ICOs). They will work towards striking a balance between facilitating innovation in the blockchain space while ensuring investor protection, market integrity, and compliance with AML and CTF regulations.

7. Regulatory Sandboxes for Central Bank Digital Currencies (CBDCs): As central banks explore the potential of CBDCs, regulatory sandboxes may be used to pilot and test these digital currencies. Regulators will need to address issues related to privacy, financial stability, transaction monitoring, and cross-border interoperability. Regulatory sandboxes can facilitate collaboration between central banks and fintech companies to understand the implications and risks associated with CBDCs.

These future trends in fintech regulation reflect the need for regulators to adapt to the rapidly evolving fintech landscape. By embracing these trends, regulatory bodies can promote innovation, protect consumers, ensure market integrity, and create a supportive regulatory environment that fosters the sustainable growth of the fintech industry.