Introduction

Welcome to the world of fintech, where finance meets technology. In today’s digital age, the fintech industry has emerged as a disruptor, revolutionizing the way we handle money, investments, and financial transactions. With innovative technologies at its core, fintech companies have transformed traditional banking systems, offering a wide range of financial services accessible at our fingertips.

Fintech, short for financial technology, encompasses a vast array of companies that leverage technology to deliver financial products and services. From mobile banking apps to online lending platforms, robo-advisors, and digital payment solutions, fintech has revolutionized the financial landscape, empowering individuals and businesses with greater convenience and accessibility.

The rise of fintech has democratized finance, allowing individuals from all walks of life to access financial services that were once limited to the privileged few. This democratization has not only provided financial inclusion but also opened up new avenues for innovation, investment, and economic growth.

In this article, we will explore the various facets of the fintech industry. We will delve into the different types of fintech companies, highlight key players in the industry, and shed light on how fintech is transforming traditional banking. Furthermore, we will discuss the benefits of fintech for consumers, the challenges faced by the industry, the regulatory environment it operates in, and the emerging trends that are shaping the future of fintech.

So, whether you’re a tech enthusiast, an investor, or simply curious about the fintech revolution, this article will provide you with a comprehensive understanding of the fintech industry and its impact on our daily lives. Prepare to embark on a journey that explores the intersection of finance and technology, where traditional financial institutions are being challenged, and innovative solutions are paving the way for a more efficient and inclusive financial world.

What is Fintech?

Fintech, short for financial technology, refers to the intersection of finance and technology. It encompasses a wide range of innovative solutions and technologies that are disrupting and transforming the traditional financial industry. Fintech companies leverage advanced software, algorithms, and digital platforms to offer financial services in a faster, more efficient, and accessible manner.

At its core, fintech is all about leveraging technology to enhance and streamline financial processes. It aims to empower individuals and businesses by providing them with convenient access to financial products and services, eliminating the need for traditional brick-and-mortar banks or intermediaries.

One of the key areas where fintech has made a significant impact is in payments and transfers. With the advent of digital wallets, mobile payment apps, and peer-to-peer payment platforms, transferring money has become seamless and effortless. Fintech has eliminated the need for physical currency or paper checks, enabling quick and secure digital transactions.

Another prominent sector within the fintech industry is lending and borrowing. Fintech has revolutionized lending by introducing online lending platforms that connect borrowers directly with investors or lenders, bypassing the traditional banking system. These platforms leverage technology and data analytics to assess creditworthiness and offer personalized loan options swiftly and transparently.

Investing and wealth management have also witnessed a significant shift with the rise of fintech. Robo-advisors have emerged as a popular choice for individuals seeking low-cost and automated investment advice. These platforms utilize algorithms and artificial intelligence to create and manage personalized investment portfolios tailored to individual goals and risk preferences.

Furthermore, fintech has expanded financial inclusion by providing access to financial services for the unbanked and underbanked populations. Mobile banking applications have revolutionized banking and financial services in developing countries, allowing individuals to perform banking operations through their smartphones, even in remote areas with limited physical infrastructure.

In summary, fintech is redefining the financial services landscape by leveraging technology to offer fast, convenient, and accessible solutions across various domains, such as payments, lending, investing, and banking. As the industry continues to evolve and innovate, it holds the potential to reshape how individuals and businesses interact with money and financial institutions, ultimately creating a more inclusive and technologically advanced financial world.

Types of Fintech Companies

The fintech industry encompasses a diverse range of companies that cater to different segments of the financial services sector. These companies leverage technology to provide innovative solutions across various domains. Let’s explore some of the common types of fintech companies:

1. Payment and Remittance Platforms: These fintech companies offer digital payment solutions that allow individuals and businesses to send and receive money securely and conveniently. From mobile payment apps to peer-to-peer payment platforms, these companies have transformed the way we transact and handle our finances.

2. Online Lending Platforms: Fintech lending platforms have revolutionized the lending landscape by connecting borrowers directly with lenders or investors. These platforms use algorithms and data analytics to assess creditworthiness and provide personalized loan options. By streamlining the borrowing process, they offer faster loan approvals, lower costs, and greater transparency.

3. Robo-advisors: These digital wealth management platforms use algorithms and artificial intelligence to provide automated investment advice. Robo-advisors create customized investment portfolios based on an individual’s financial goals, risk tolerance, and time horizon. They offer low-cost investment options, making wealth management more accessible to a wider audience.

4. Digital Banks: Fintech has disrupted the traditional banking sector with the emergence of digital-only banks or neobanks. These banks operate entirely online, without the need for physical branches. They offer a range of banking services, such as current accounts, savings accounts, and loans, with a seamless digital experience and enhanced efficiency.

5. Insurtech Companies: These fintech companies leverage technology to enhance and streamline the insurance industry. They offer digital platforms for policy management, claims processing, and underwriting. Insurtech companies utilize data analytics and artificial intelligence to provide personalized insurance products and create a more efficient insurance ecosystem.

6. Blockchain and Cryptocurrency: Blockchain technology has revolutionized financial transactions and security. Fintech companies in this space leverage blockchain technology for secure and transparent peer-to-peer transactions, smart contracts, and decentralized finance. Cryptocurrency exchanges and wallets provide platforms for buying, selling, and storing digital currencies like Bitcoin and Ethereum.

7. Regtech Companies: Regulatory technology, or regtech, companies provide solutions that help financial institutions comply with regulations and mitigate risks. These companies use advanced technologies, such as artificial intelligence and machine learning, to automate compliance processes, monitor transactions, and ensure regulatory adherence.

These are just a few examples of the diverse range of fintech companies. Each type of company plays a unique role in transforming and modernizing the financial industry. As technology continues to evolve, we can expect to see even more innovative fintech solutions emerging to address various financial needs and challenges.

Key Players in the Fintech Industry

The fintech industry is home to a plethora of innovative companies that are revolutionizing the financial services landscape. These key players have not only disrupted traditional banking systems but have also transformed how individuals and businesses manage their finances. Let’s take a closer look at some of the prominent names in the fintech industry:

1. PayPal: As one of the pioneers in the online payment space, PayPal has been a game-changer in facilitating digital transactions. It allows individuals and businesses to make online payments, transfer money, and receive payments securely, both domestically and internationally.

2. Square: Square is known for its popular payment processing solutions, including its point-of-sale (POS) system and Square Cash App. Square has revolutionized how small businesses accept payments by providing easy-to-use tools and affordable processing fees.

3. Ant Group: Ant Group, formerly known as Ant Financial, is the parent company of Alipay, the leading digital payment platform in China. It offers a range of financial services, including payments, loans, wealth management, and insurance, serving millions of users in China and beyond.

4. Stripe: Stripe is a prominent player in the world of online payments. It provides a seamless and customizable platform for accepting online payments, making it a popular choice for e-commerce businesses around the globe.

5. Robinhood: Robinhood disrupted the investment landscape by offering commission-free trading through its user-friendly mobile app. It has made investing accessible to a broader audience, particularly young and novice investors.

6. Revolut: Revolut is a digital-only bank that has gained popularity for its multi-currency accounts, low-cost international transfers, and budgeting features. It offers a range of banking services through its app, making it a convenient option for individuals who frequently travel internationally.

7. Coinbase: Coinbase is one of the leading cryptocurrency exchanges, allowing users to buy, sell, and store digital currencies securely. It has played a significant role in the growth and adoption of cryptocurrencies, making it easier for individuals to enter the crypto space.

8. SoFi: SoFi, short for Social Finance, is a fintech company that focuses on student loan refinancing, personal loans, mortgages, and investment services. SoFi has disrupted the lending industry by providing competitive rates and customer-centric solutions.

9. Klarna: Klarna is a Swedish fintech company that offers a buy-now-pay-later option for online shoppers. It allows users to make purchases and pay in installments, creating a flexible and convenient shopping experience.

10. Chime: Chime is a neobank that provides a range of banking services, including fee-free checking and savings accounts, early access to direct deposits, and a user-friendly mobile app. It has gained popularity for its customer-centric approach and no hidden fees.

These are just a few examples of the key players in the fintech industry. Each of these companies has disrupted traditional finance with their innovative products and services, reshaping how we manage and interact with our finances. As technology continues to advance, we can expect to see new players emerging and existing ones further pushing the boundaries of fintech innovation.

How Fintech is Transforming Traditional Banking

The advent of fintech has brought about a monumental transformation in the traditional banking sector. Fintech companies have disrupted long-established banking systems by leveraging technology to provide more efficient, cost-effective, and customer-centric financial services. Let’s explore how fintech is reshaping the landscape of traditional banking:

1. Enhanced Convenience: Fintech has made banking services more accessible and convenient than ever before. With the rise of mobile banking apps and digital wallets, individuals can perform a wide range of banking activities on their smartphones, anytime and anywhere. From checking account balances to making payments, transferring funds, or applying for loans, these services can be accessed quickly and conveniently, eliminating the need to visit physical bank branches.

2. Personalized Experience: Fintech companies prioritize personalized experiences for customers. Through advanced data analytics and artificial intelligence, these companies can gather and analyze customer data to offer tailored financial products and services. Whether it’s personalized investment advice, customized loan options, or personalized budgeting tips, fintech ensures that customers receive solutions that align with their specific needs and preferences.

3. Improved Access to Credit: Traditional banking systems often have strict criteria for lending, making it difficult for certain individuals and businesses to access credit. Fintech lending platforms have revolutionized the lending landscape by utilizing advanced algorithms to assess creditworthiness in a more comprehensive and unbiased manner. This has significantly increased access to credit for underserved populations, small businesses, and individuals with limited credit histories.

4. Cost Savings: Fintech solutions have effectively reduced the costs associated with traditional banking. Digital banks and neobanks, for example, operate without physical branches, leading to reduced overhead costs. Additionally, fintech innovators have streamlined processes, eliminated manual paperwork, and automated routine tasks, leading to operational efficiency and cost savings. These cost savings are often passed on to customers in the form of reduced fees and more competitive interest rates.

5. The Rise of Open Banking: Open banking, fueled by fintech, promotes the sharing of financial data securely between banks and authorized third-party providers. This allows users to have greater control over their financial information and enables fintech companies to develop innovative and integrated services that may span across multiple banking institutions. Open banking fosters competition and innovation, providing customers with more choice and better financial products and services.

6. Enhanced Security: Fintech companies place a strong emphasis on security and data protection. They employ robust encryption techniques, multi-factor authentication, and sophisticated fraud detection systems to ensure the safety of customer information and transactions. Additionally, decentralized technologies like blockchain enhance security by ensuring transparent and tamper-proof transaction records.

7. Financial Inclusion: Fintech has played a critical role in promoting financial inclusion. By offering digital and mobile-based financial services, fintech has bridged the gap between traditional banking systems and the unbanked or underbanked populations. Mobile banking apps, for instance, have empowered individuals in remote and underserved areas to access basic financial services, such as transferring money and making payments.

In summary, fintech is transforming traditional banking by prioritizing convenience, personalization, accessibility, and cost savings. As fintech continues to evolve, we can expect more innovative solutions that embrace emerging technologies, such as artificial intelligence, blockchain, and the Internet of Things. These advancements will further reshape the banking industry, enhancing customer experiences and driving greater financial inclusion.

Benefits of Fintech for Consumers

Fintech has brought about numerous benefits for consumers, transforming the way individuals manage their finances and interact with financial institutions. These advancements have democratized finance, empowering consumers with greater control, convenience, and accessibility. Let’s explore some of the key benefits that fintech offers to consumers:

1. Convenient Access to Financial Services: One of the primary benefits of fintech is the convenience it offers. Fintech companies provide digital platforms and mobile apps that enable consumers to access a wide range of financial services at their fingertips. Whether it’s checking account balances, transferring funds, or paying bills, these services can be performed anytime and anywhere, reducing the need for physical visits to brick-and-mortar bank branches.

2. Enhanced Personalization: Fintech leverages advanced data analytics and artificial intelligence to personalize financial products and services. Through algorithms and customer insights, fintech companies can offer tailored recommendations, investment advice, and loan options that align with individuals’ unique financial goals and preferences. This level of personalization helps consumers better manage their finances and achieve their financial objectives.

3. Cost Savings: Fintech solutions often come with reduced costs compared to traditional banking. Digital banks and neobanks, for example, have lower overhead costs, allowing them to offer competitive interest rates and fewer fees. Additionally, fintech enables more efficient and automated processes, eliminating manual paperwork and reducing administrative costs, ultimately leading to cost savings for consumers.

4. Greater Financial Inclusion: Fintech has played a significant role in promoting financial inclusion by providing access to financial services for underserved populations. Mobile banking apps and digital wallets have enabled individuals without access to traditional banking services to perform financial transactions and manage their money using their smartphones. This empowers individuals in remote areas or with limited physical infrastructure to participate in the formal financial system.

5. Improved Transparency: Fintech solutions often prioritize transparency, providing consumers with a clearer understanding of their financial transactions, fees, and account information. With real-time updates and notifications, consumers can stay informed about their financial activities, helping them make more informed decisions and avoid surprises.

6. Quicker and Seamless Transactions: Fintech companies have simplified and accelerated financial transactions. From instant peer-to-peer payments to quick loan approvals, fintech solutions remove unnecessary bureaucracy and streamline processes. Consumers can enjoy faster and more efficient transactions, saving time and reducing friction.

7. Enhanced Security and Fraud Prevention: Fintech companies prioritize security and employ advanced encryption techniques, multi-factor authentication, and robust fraud detection systems to protect consumer data and transactions. Moreover, decentralized technologies like blockchain provide an added layer of security, ensuring transparent and tamper-proof transaction records.

In summary, fintech offers a multitude of benefits to consumers, including convenience, personalization, cost savings, financial inclusion, transparency, quick transactions, and enhanced security. As fintech continues to evolve and innovate, consumers can expect even more innovative solutions that cater to their unique financial needs, empowering them to make smarter financial decisions and achieve their financial goals.

Challenges in the Fintech Industry

While the fintech industry has experienced rapid growth and innovation, it is not without its challenges. These challenges stem from various factors such as regulatory hurdles, cybersecurity risks, customer trust, and competition from traditional financial institutions. Let’s explore some of the key challenges faced by the fintech industry:

1. Regulatory Landscape: Fintech operates in a highly regulated environment that varies from one jurisdiction to another. Navigating complex regulatory frameworks and complying with financial regulations can be challenging for fintech companies, especially startups with limited resources. Compliance costs and the need for licenses can pose barriers to market entry and hinder innovation.

2. Data Privacy and Cybersecurity: With the increasing reliance on technology and the handling of sensitive customer data, fintech companies face significant cybersecurity risks. The protection of customer information and the prevention of data breaches are critical challenges. Fintech firms must invest in robust cybersecurity measures, continuously monitor and update their systems, and educate customers about data privacy risks.

3. Customer Trust and Adoption: Building and maintaining customer trust is crucial for the success of fintech companies. While fintech offers convenience and innovation, some consumers may still be hesitant to adopt these new technologies due to concerns about the security and privacy of their financial information. It is essential for fintech companies to reassure customers, provide transparent communication, and demonstrate their commitment to data protection.

4. Access to Funding: Scaling and expanding fintech operations often require substantial investments. However, access to funding can be a challenge for startups, particularly those without a proven track record. Convincing investors and securing funding in a competitive market can be difficult, especially if the business model or technology is perceived as risky or untested.

5. Legacy Infrastructure Integration: Fintech companies often need to integrate with existing legacy systems and traditional financial institutions to provide seamless services to customers. However, legacy banking infrastructure can be complex, outdated, and resistant to change. Integrating fintech solutions with legacy systems can pose technical challenges, requiring substantial time and resources.

6. Regulatory Compliance and Risk Management: Fintech companies must adhere to various regulations, including anti-money laundering (AML) and know-your-customer (KYC) requirements. Compliance with these regulations can be burdensome and costly, particularly for startups with limited resources. Additionally, managing risks, such as fraudulent activities and cybersecurity breaches, requires robust risk management practices and ongoing monitoring.

7. Competition from Incumbents: Traditional financial institutions are increasingly embracing technology and investing in their own digital solutions. The competition from incumbent banks and established financial institutions can pose a significant challenge for fintech companies. Fintech firms must differentiate themselves by offering superior user experiences, innovative features, and niche services to stand out in a crowded market.

In summary, while fintech has disrupted the financial industry and brought numerous opportunities, it faces challenges such as regulatory complexities, cybersecurity risks, customer trust, access to funding, legacy infrastructure integration, regulatory compliance, and competition from traditional financial institutions. Overcoming these challenges requires innovation, collaboration with regulators, strong risk management practices, and a customer-centric approach to build trust and ensure the long-term success of fintech ventures.

Regulatory Environment for Fintech

The regulatory environment for the fintech industry is complex and constantly evolving. As fintech companies provide innovative financial services, regulators strive to strike a balance between fostering innovation and protecting consumers. Let’s explore some key aspects of the regulatory environment for fintech:

1. Regulatory Frameworks: Fintech companies must navigate a web of regulatory frameworks that vary by jurisdiction. These frameworks typically encompass financial regulations, consumer protection laws, data privacy regulations, and anti-money laundering (AML) and know-your-customer (KYC) requirements. Compliance with these regulations is essential for fintech companies to operate legally and maintain consumer trust.

2. AML and KYC Requirements: Fintech companies are subject to stringent AML and KYC regulations to prevent money laundering, terrorist financing, and other illicit activities. These regulations require fintech companies to verify the identity of their customers, conduct due diligence on transactions, and report suspicious activities to regulatory authorities.

3. Data Privacy and Protection: Fintech companies handle a vast amount of customer data, which necessitates compliance with data privacy and protection regulations. In many countries, regulations like the General Data Protection Regulation (GDPR) in Europe govern the collection, storage, and processing of personal data. Fintech companies must implement robust security measures and obtain customer consent for data usage to comply with these regulations.

4. Licensing and Registration: Depending on the nature of their operations, fintech companies may be required to obtain specific licenses or registrations to operate legally. These licenses are typically issued by relevant regulatory bodies, such as banking authorities, securities commissions, or payment regulators. Compliance with licensing requirements ensures consumer protection and the integrity of the financial system.

5. Regulatory Sandboxes: Some jurisdictions have implemented regulatory sandboxes or innovation hubs to facilitate fintech innovation. These sandboxes provide a controlled environment where fintech companies can test their products and services with regulatory support and guidance. It allows companies to assess regulatory compliance, identify risks, and refine their solutions before full-scale deployment.

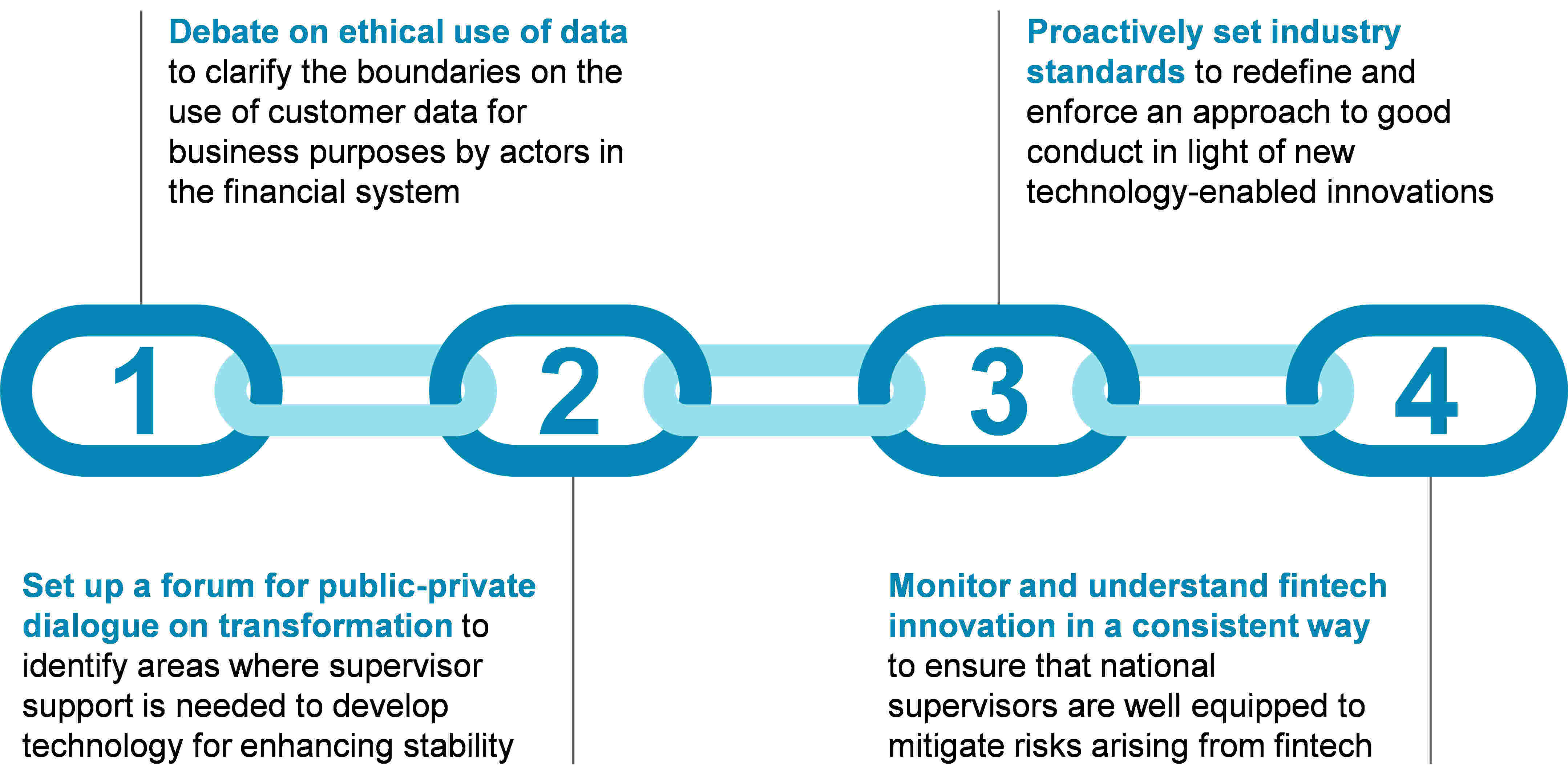

6. Collaboration and Engagement with Regulators: Collaboration between fintech companies and regulators is crucial to foster innovation while maintaining regulatory compliance. Regulatory bodies often seek input from industry stakeholders to understand the potential impact of regulations on fintech innovation. Engaging in dialogue and maintaining open lines of communication with regulators enables fintech companies to provide insights and ensure regulations are effective, proportionate, and supportive of innovation.

7. International Coordination: Fintech operates across borders, and regulatory cooperation between jurisdictions is essential for cross-border transactions and services. International coordination allows regulatory bodies to share best practices, harmonize regulations, and address challenges posed by the global nature of fintech. Organizations such as the Financial Stability Board and the International Organization of Securities Commissions play a role in promoting global cooperation and regulatory consistency.

In summary, the regulatory environment for fintech is complex and varies by jurisdiction. Fintech companies must navigate financial regulations, AML and KYC requirements, data privacy regulations, licensing and registration processes, and engage with regulators and international bodies to foster innovation while ensuring consumer protection and regulatory compliance. Ongoing collaboration and dialogue between fintech companies and regulators are essential to strike the right balance in regulating this rapidly evolving industry.

Emerging Trends in Fintech

The fintech industry is constantly evolving, driven by advancements in technology and changing consumer needs. Emerging trends in fintech reflect the industry’s dynamic nature and offer a glimpse into the future of financial services. Let’s explore some key emerging trends in fintech:

1. Open Banking and API Integration: Open banking is gaining traction, as regulations require financial institutions to share customer data securely with third-party providers. This trend promotes collaboration and innovation, enabling fintech companies to develop integrated services and solutions that leverage banking data, leading to enhanced customer experiences and personalized offerings.

2. Artificial Intelligence (AI) and Machine Learning (ML): AI and ML are transforming various aspects of fintech. Chatbots and virtual assistants enhance customer service and provide personalized recommendations. Machine learning algorithms analyze vast amounts of data to identify patterns, predict customer behavior, and improve fraud detection. AI-powered robo-advisors provide automated investment advice, making wealth management more accessible and affordable.

3. Blockchain and Cryptocurrencies: Blockchain technology continues to disrupt the financial industry. It offers immutable and transparent transaction records, reducing fraud and improving security. Cryptocurrencies, such as Bitcoin and Ethereum, gain popularity as alternative forms of digital currency and investment assets. The focus has shifted beyond cryptocurrencies to explore the potential applications of blockchain in areas like supply chain management and smart contracts.

4. Biometric Authentication: Fintech companies are increasingly adopting biometric authentication methods, such as fingerprint and facial recognition, for secure and convenient user verification. Biometrics provide enhanced security and reduce the reliance on traditional passwords or PINs, improving the user experience and protecting against identity theft and fraud.

5. Internet of Things (IoT) Integration: The integration of fintech with IoT devices offers new possibilities for seamless and secure financial transactions. IoT devices, such as smartwatches and connected cars, can facilitate contactless payments, automated billing, and real-time transaction monitoring. This integration enhances convenience and further blurs the lines between physical and digital banking experiences.

6. Regtech and Compliance automation: Regtech solutions leverage technology, such as AI and data analytics, to streamline regulatory compliance for fintech companies. Automated compliance processes help companies adhere to regulatory requirements, monitor transactions for suspicious activities, and manage risk efficiently. Regtech reduces compliance costs, enhances transparency, and ensures regulatory adherence in an ever-changing regulatory landscape.

7. Gig Economy and Alternative Lending: Fintech has enabled the growth of the gig economy by providing alternative lending options for independent contractors and freelancers. Fintech platforms use non-traditional data sources, such as transaction history and social media presence, to assess creditworthiness and offer tailored loan products. This trend addresses the financial needs of individuals within the gig economy who may have unconventional income streams.

In summary, emerging trends in fintech signal a shift towards collaboration, personalization, enhanced security, and automation. Open banking, AI and ML, blockchain, biometric authentication, IoT integration, regtech, and alternative lending are just a few examples of the exciting innovations shaping the future of financial services. As technology advances, we can expect fintech to continue revolutionizing the way we manage our finances, providing greater accessibility, efficiency, and innovation for consumers and businesses alike.

Conclusion

The fintech industry has emerged as a disruptive force, transforming traditional banking systems and revolutionizing the way we handle finances. Through the convergence of finance and technology, fintech has introduced a wide range of innovative solutions that enhance convenience, accessibility, and personalization for consumers. From mobile banking apps and digital payment platforms to robo-advisors and blockchain applications, fintech has democratized finance and empowered individuals and businesses with greater control over their financial lives.

The benefits of fintech are evident, as it offers consumers convenient access to financial services, cost savings, personalized experiences, and improved financial inclusion. Fintech has also challenged traditional banking models, forcing incumbents to adopt technology and offer competitive digital solutions. However, the industry faces challenges, including navigating complex regulatory environments, ensuring data privacy and cybersecurity, building customer trust, and securing funding for growth.

As technology continues to advance, several trends are shaping the future of fintech. Open banking, artificial intelligence, blockchain, biometric authentication, IoT integration, and regtech are transforming how financial services are delivered and experienced. These emerging trends emphasize collaboration, personalization, security, and automation, promising a future of enhanced customer experiences, efficiency, and innovation.

In conclusion, fintech is a dynamic and evolving industry that holds immense potential to reshape the financial landscape. As fintech companies continue to innovate and overcome challenges, they have the opportunity to foster financial inclusion, drive economic growth, and provide individuals and businesses with unprecedented access to financial services. With the right balance between innovation and regulation, fintech will continue to revolutionize how we manage and interact with money, paving the way for a more inclusive, efficient, and technologically advanced financial world.