Introduction

Welcome to the world of banking, where security, trust, and compliance are of utmost importance. In the rapidly evolving landscape of financial services, it is essential for banks to have robust measures in place to prevent fraud, money laundering, and other illegal activities. This is where KYC, or Know Your Customer, comes into play.

KYC is the process banks and financial institutions use to verify the identity of their customers before establishing a business relationship with them. It involves gathering relevant information and documents to assess the customer’s risk level and ensure compliance with regulatory requirements.

With the rise of digital banking and online transactions, the need for a secure and reliable KYC process has become even more critical. Banks must not only protect their customers’ funds but also uphold the integrity of the financial system. In this article, we will explore what KYC is, why it is vital in the banking sector, and how it is implemented.

Additionally, we will discuss the documents typically required for KYC, the benefits it provides to banks and customers, the challenges faced in its implementation, and any recent developments or updates in KYC regulations.

By the end of this article, you will have a clear understanding of the significance of KYC in banking, the steps involved in the process, and the implications for all stakeholders involved. Let’s embark on this informative journey and unravel the mysteries of KYC in the world of banking.

What is KYC?

KYC, which stands for Know Your Customer, is a set of processes and procedures designed to verify the identity and assess the risk level of customers in the banking sector. It serves as a crucial tool for banks and financial institutions to mitigate risks and ensure compliance with regulatory frameworks.

The primary objective of KYC is to prevent financial crimes such as fraud, money laundering, terrorist financing, and identity theft. By verifying the identities of customers, banks can establish the legitimacy of their transactions and detect any suspicious activities.

The KYC process typically involves obtaining information and documents from customers to confirm their identity, address, and other relevant details. This information is then verified, and the risk associated with the customer is assessed based on factors such as their occupation, source of income, and transaction history.

KYC regulations may vary from country to country, but the core principles remain the same. Banks must implement thorough due diligence procedures to ensure that they only engage in legitimate business relationships and comply with applicable laws and regulations.

With the advancement of technology, KYC processes have become more streamlined and efficient. Many banks now utilize digital platforms and online verification methods to reduce paperwork and expedite the process. This not only enhances the customer experience but also helps in preventing fraud and unauthorized account access.

It is important to note that KYC is an ongoing process, rather than a one-time event. Banks are required to regularly update customer information, monitor transactions for any suspicious activities, and report any potential breaches of regulations to the appropriate authorities.

Overall, KYC serves as a crucial mechanism to protect both banks and customers from financial crimes. By instituting effective KYC procedures, banks can establish trust with their customers, maintain the integrity of the financial system, and contribute to the overall stability of the economy.

Why is KYC important in banking?

KYC plays a vital role in the banking industry due to its numerous benefits and the crucial role it plays in maintaining the integrity of the financial system. Let’s explore why KYC is important in banking:

1. Preventing Financial Crimes: KYC acts as the first line of defense against financial crimes such as fraud, money laundering, and terrorist financing. By verifying the identity of customers, banks can ensure that they are not facilitating illicit activities and can detect any suspicious transactions.

2. Risk Mitigation: Effective KYC procedures allow banks to assess the risk associated with each customer. This helps in identifying high-risk individuals or entities and applying appropriate risk mitigation measures. By understanding the risk profile of their customers, banks can make informed decisions to safeguard their interests.

3. Compliance with Regulations: Financial institutions operate under stringent regulations imposed by regulatory authorities. KYC is crucial for banks to comply with these regulations and avoid penalties and legal consequences. By following KYC procedures, banks demonstrate their commitment to regulatory compliance and contribute to the overall stability of the financial system.

4. Protecting Customers: KYC not only protects banks but also safeguards the interests of customers. By verifying the identity of customers, banks ensure that funds are not being used by fraudsters or criminals. This helps in maintaining customer trust and confidence in the banking system.

5. Enhancing due diligence: KYC processes require banks to gather information about customers’ source of funds, occupation, and transaction history. This enables banks to conduct thorough due diligence and assess the legitimacy of business relationships. It helps in establishing transparency and preventing financial malpractices.

6. Preventing Identity Theft: Identity theft is a growing concern in today’s digital age. KYC acts as a deterrent against identity theft by ensuring that the person opening the bank account is indeed the rightful owner of the identity documents provided. This helps protect individuals from becoming victims of identity theft and financial fraud.

Overall, KYC is crucial for banks to maintain their reputation, mitigate risks, comply with regulations, and protect themselves and their customers from financial crimes. It is an essential tool in the fight against money laundering, fraud, and other illicit activities in the banking sector.

The purpose of KYC in banking

KYC, or Know Your Customer, serves several important purposes in the banking industry. Let’s explore the key objectives and benefits of KYC:

1. Verification of Customer Identity: The primary purpose of KYC is to verify the identity of customers seeking to establish a business relationship with a bank. This ensures that the customer is who they claim to be, preventing identity theft and fraudulent activities.

2. Risk Assessment: KYC helps banks assess the level of risk associated with each customer. By gathering information and conducting due diligence, banks can identify high-risk individuals or entities and apply appropriate risk mitigation strategies. This helps in protecting the bank from potential financial and reputational losses.

3. Compliance with Regulations: KYC is essential for banks to comply with regulatory frameworks and anti-money laundering (AML) laws. Regulatory authorities require banks to have robust KYC procedures in place to prevent money laundering, terrorist financing, and other financial crimes. Compliance with these regulations helps ensure the integrity of the financial system.

4. Prevention of Financial Crimes: KYC plays a critical role in preventing financial crimes such as fraud, money laundering, and terrorist financing. By verifying the identity of customers, banks can detect and deter individuals or entities attempting to use the banking system for illicit purposes.

5. Enhanced Customer Due Diligence: KYC processes enable banks to conduct thorough due diligence on their customers. This includes gathering information about their source of funds, occupation, business activities, and transaction history. By understanding their customers better, banks can make informed decisions and identify any potential red flags.

6. Protection of Bank and Customers: KYC protects the interests of both the bank and its customers. By verifying customer identities and conducting ongoing monitoring of transactions, banks can prevent unauthorized account access and protect customers from financial fraud and identity theft.

7. Establishment of Trust and Confidence: Effective KYC procedures help build trust and confidence between banks and their customers. Customers feel secure in the knowledge that their financial institution is committed to ensuring their safety and complying with regulatory requirements. This fosters a positive relationship between banks and customers.

Overall, the purpose of KYC in banking is to establish the identity of customers, assess the risk associated with them, comply with regulations, prevent financial crimes, and protect the interests of the bank and its customers. It is a crucial mechanism to maintain the integrity of the financial system and promote transparency within the industry.

The KYC process in banking

The KYC process, or Know Your Customer process, is a series of steps that banks and financial institutions undertake to verify the identity of their customers and assess the associated risks. Let’s explore the typical steps involved in the KYC process in banking:

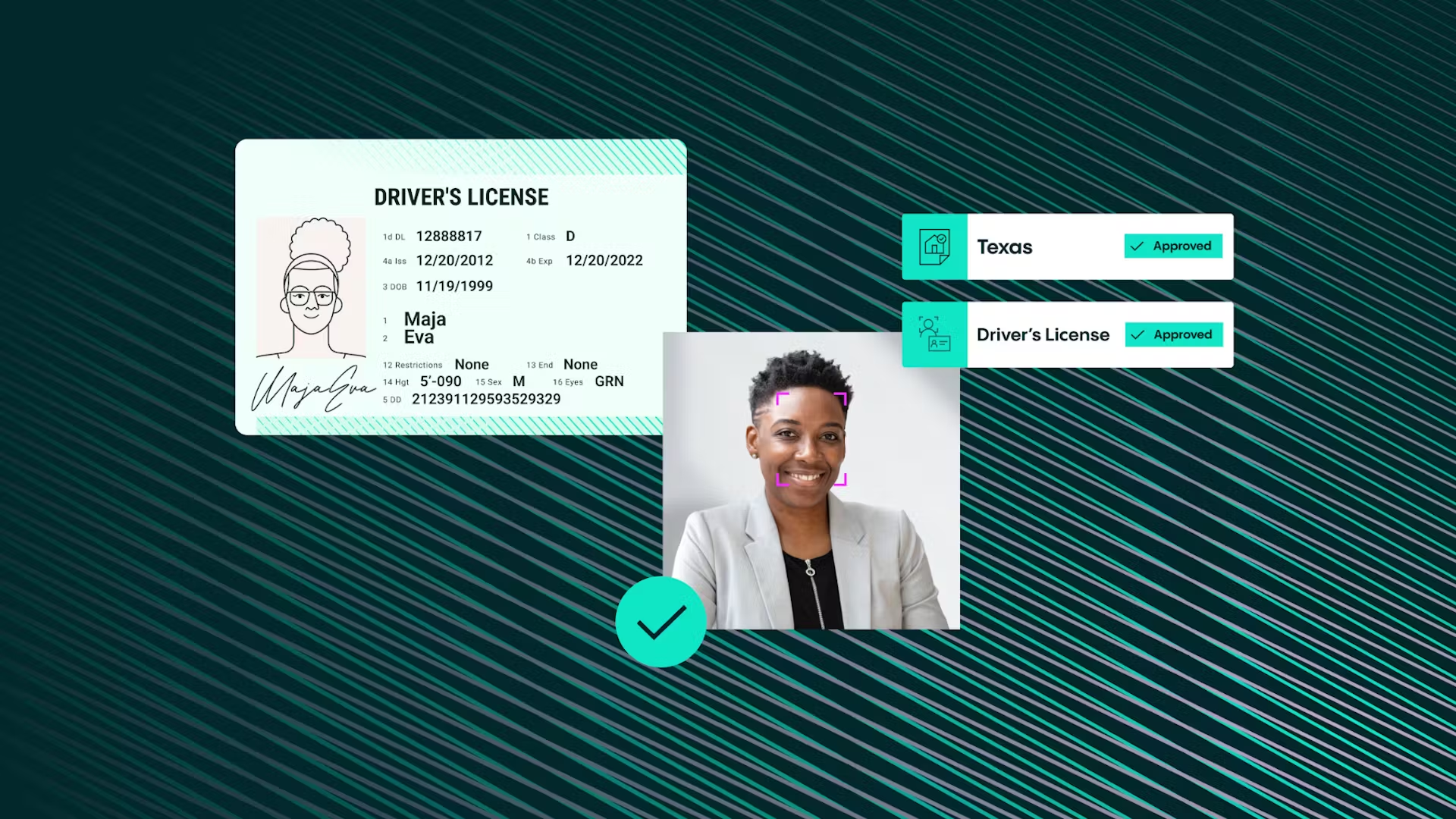

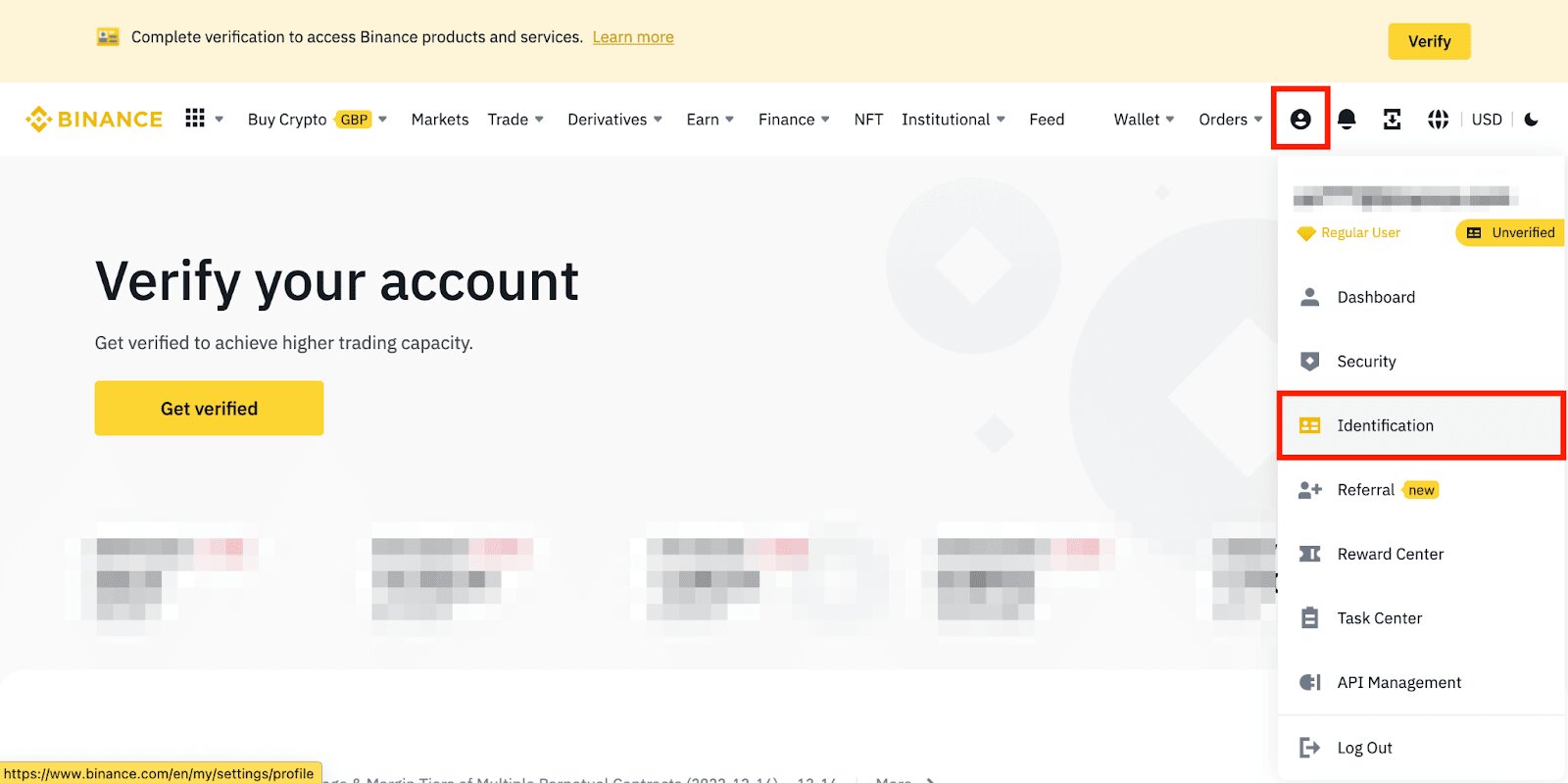

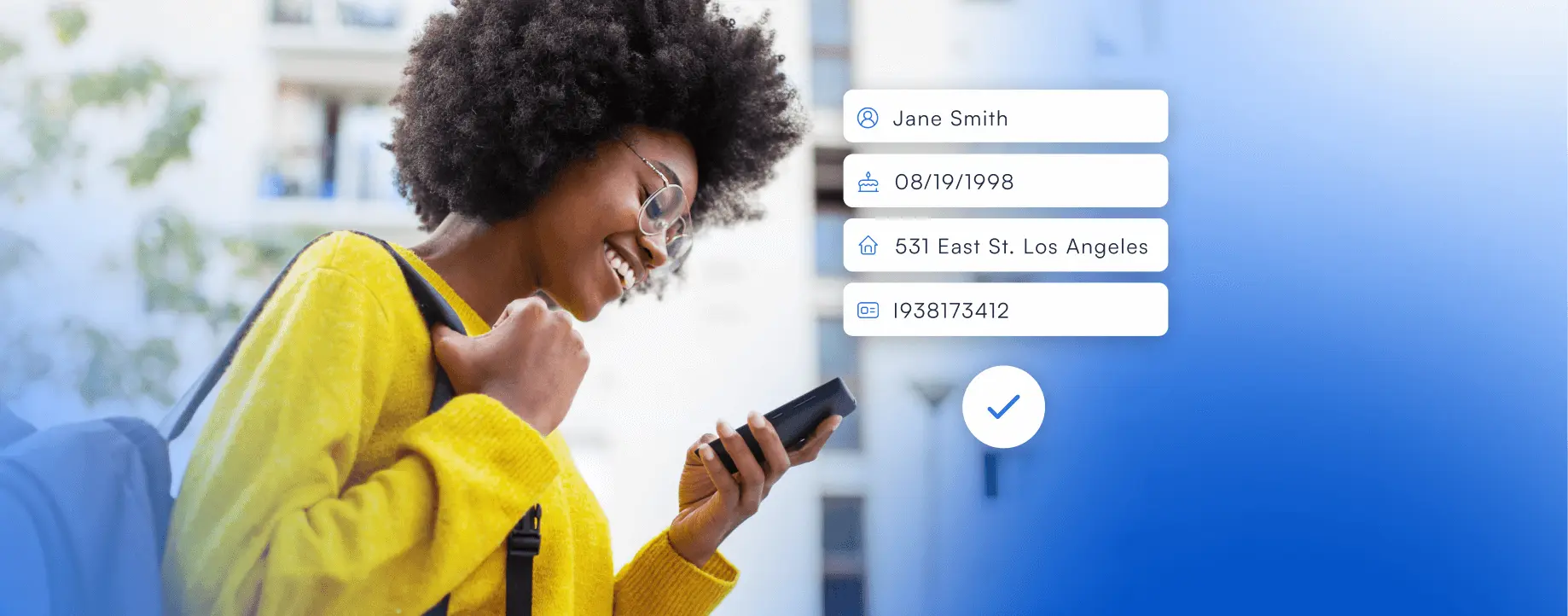

1. Customer Identification: The first step in the KYC process is to collect information and documents to identify the customer. This includes obtaining personal details such as name, date of birth, address, and contact information. Banks may require customers to provide identity proof, such as a government-issued ID card, passport, or driver’s license.

2. Document Verification: Once the necessary identification documents are obtained, banks verify their authenticity by matching the information provided with the documents’ details. This may involve comparing photographs, signatures, and other relevant information. In some cases, banks may use third-party services or technology to conduct this verification process.

3. Address Verification: Banks also verify the customer’s residential or business address to ensure accuracy and validity. Documents such as utility bills, bank statements, or government-issued documents with the customer’s address may be requested and verified.

4. Risk Assessment: After the customer’s identity and address are verified, banks assess the risk associated with the customer. This involves evaluating factors such as the customer’s occupation, source of income, transaction history, and any potential exposure to politically exposed persons (PEPs) or high-risk jurisdictions. Risk assessment helps banks determine the level of due diligence required and appropriate risk mitigation measures to implement.

5. Ongoing Monitoring: KYC is not a one-time process; it is an ongoing obligation for banks. Banks are required to monitor their customers’ transactions continuously to detect any suspicious activities or changes in customer behavior. This includes monitoring large transactions, unusual patterns, and any potential breaches of regulatory thresholds.

6. Record Keeping: Banks are required to maintain records of their customers’ identity verification, documents, and transaction history. This is crucial for regulatory compliance and providing evidence of compliance during audits or investigations. The duration for which records are kept may vary based on local regulations.

7. Periodic Review and Updating: Banks are also obligated to periodically review and update customer information. This ensures that the customer’s profile remains current and accurate. It may involve requesting customers to provide updated documentation or verifying their information through other means.

8. Reporting Suspicious Activities: In the event of detecting suspicious activities or potential money laundering, banks are required to report such activities to the relevant authorities. This is a critical step in combating financial crimes and maintaining the integrity of the financial system.

By following these steps, banks ensure that they have a comprehensive understanding of their customers, evaluate the associated risks, and comply with regulatory requirements. The KYC process helps banks establish trust, mitigate risks, and contribute to a safer and more secure financial ecosystem.

Documents required for KYC in banking

The KYC (Know Your Customer) process in banking requires customers to provide specific documents to verify their identity and address. These documents serve as proof of identity and are essential for regulatory compliance and risk assessment. The exact documents required may vary depending on the country and the bank’s internal policies. Here are some commonly requested documents for KYC in banking:

1. Identity Proof: Customers are typically required to provide a valid identification document. This can include a government-issued ID card, passport, driver’s license, or any other official document that proves their identity. The document should have a clear photograph, full name, and a unique identification number.

2. Address Proof: Proof of address is essential to verify the customer’s residential or business address. Accepted documents may include utility bills (electricity, water, gas), bank statements, rental agreements, or official government correspondence. The document should display the customer’s name and address, be recent, and not older than a specified timeframe determined by the bank.

3. Proof of Tax Identification Number: In some jurisdictions, customers may be required to provide their tax identification number (TIN) as part of the KYC process. This helps in complying with tax reporting obligations and preventing tax evasion. The TIN can be obtained from tax authorities or relevant government agencies.

4. Proof of Income: Banks may request proof of income to assess the customer’s financial stability and determine the level of risk associated with them. Documents such as salary slips, bank statements showing regular income deposits, and tax returns are commonly requested. Self-employed individuals may be required to provide business financial statements or other documents to verify their source of income.

5. Business Documents (for business customers): When opening accounts for business entities, additional documents are typically required. These may include business registration certificates, articles of incorporation, partnership agreements, board resolutions, and documents establishing the authority of the company’s representatives to conduct banking transactions.

6. Additional Information or Documents: Depending on the risk profile of the customer or specific regulatory requirements, banks may request additional information or documents. This could include source of funds or wealth documents, details about the nature of business activities, and any other relevant documentation deemed necessary by the bank.

It is important to note that banks have strict protocols for handling and storing customer information and documents in a secure manner. These documents are used solely for the purpose of KYC compliance and are subject to confidentiality and privacy safeguards.

Customers are advised to ensure that they provide accurate and up-to-date documents to avoid any delays or complications in the KYC process. Failure to provide the required documentation in a timely manner may result in the rejection of the account opening or transaction requests.

By gathering and verifying these documents, banks can fulfill their due diligence obligations, mitigate risks, and comply with regulatory requirements, ensuring the integrity of the banking system.

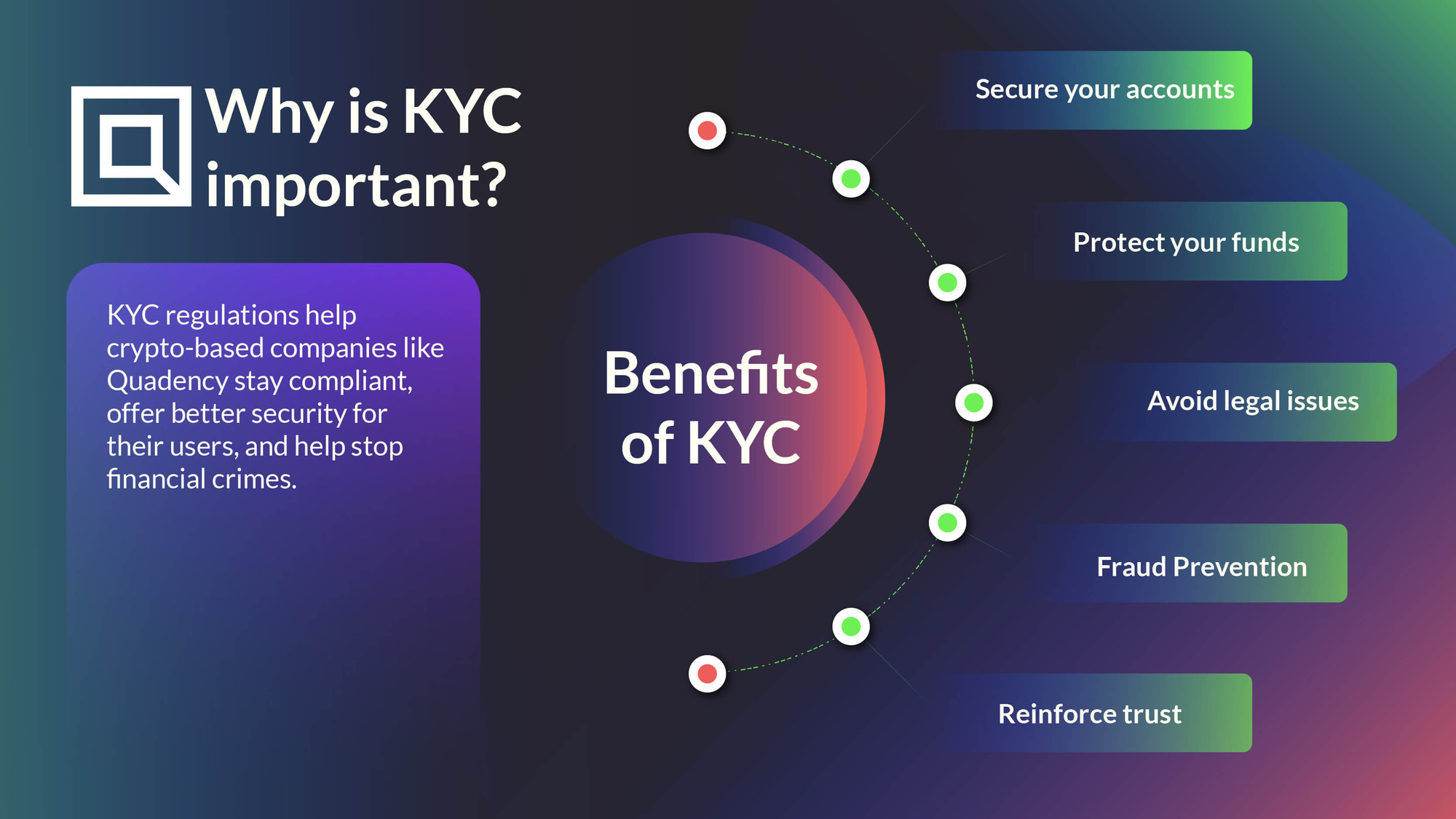

Benefits of KYC in banking

The implementation of KYC (Know Your Customer) in the banking sector offers various benefits for both banks and customers. Let’s explore the key advantages of KYC:

1. Stronger Security Measures: KYC allows banks to establish the identity of their customers, ensuring that the accounts and transactions are legitimate. This helps in preventing fraud, identity theft, and unauthorized access to accounts, enhancing the overall security of the banking system.

2. Effective Risk Management: KYC enables banks to assess the risk associated with each customer and account. By gathering relevant information, such as the source of funds and transaction history, banks can identify and mitigate any potential risks. This helps in minimizing financial losses and reputational damage.

3. Compliance with Regulatory Requirements: KYC is a regulatory obligation for banks to prevent money laundering, terrorist financing, and other financial crimes. By implementing robust KYC procedures, banks ensure compliance with local and international regulations, reducing the risk of regulatory penalties and legal consequences.

4. Enhanced Customer Trust: Strong KYC processes build trust and confidence among customers. Knowing that their bank conducts thorough identity verification and due diligence, customers feel secure and protected. This fosters long-term relationships and customer loyalty, as they trust the bank to protect their financial interests.

5. Efficient Customer Onboarding: With well-established KYC procedures, banks can streamline the customer onboarding process. Digital KYC solutions enable faster verification by eliminating the need for physical documentation and manual processes. This enhances the customer experience, reduces paperwork, and accelerates the account opening process.

6. Preventing Financial Crimes: KYC acts as a deterrent against money laundering, fraud, and other financial crimes. By verifying the identity of customers and monitoring their transactions, banks can detect and prevent suspicious activities in a timely manner. This contributes to maintaining the integrity of the financial system.

7. Facilitating Cross-Border Transactions: KYC helps banks comply with international regulations related to cross-border transactions. By fulfilling the necessary due diligence requirements, banks can facilitate seamless and secure international transfers, supporting global trade and economic activities.

8. Effective Risk-Based Approach: KYC allows banks to implement a risk-based approach to customer due diligence. By assessing the risk level of each customer, banks can allocate resources, focus on higher-risk customers, and apply appropriate levels of scrutiny. This enhances the efficiency and effectiveness of their anti-money laundering and risk management frameworks.

In summary, KYC brings numerous benefits to both banks and customers. It strengthens security measures, ensures compliance with regulations, builds trust with customers, prevents financial crimes, and facilitates efficient customer onboarding and cross-border transactions. By prioritizing KYC, banks can establish a safer and more secure banking environment for all stakeholders involved.

Challenges in implementing KYC in banking

While the KYC (Know Your Customer) process is crucial in the banking industry, it poses certain challenges that banks must navigate. Let’s explore some of the key challenges in implementing KYC in banking:

1. Complex Regulatory Environment: Banks operate in a complex regulatory landscape with numerous laws and regulations governing customer due diligence. Compliance with these regulations requires banks to invest significant resources in developing and maintaining robust KYC processes to meet evolving regulatory requirements.

2. Data Quality and Integrity: A major challenge in KYC implementation is ensuring the accuracy and integrity of customer data. Errors, inconsistencies, or outdated information can undermine the effectiveness of the KYC process. Banks must establish robust data management systems and processes to maintain data quality and keep customer records up to date.

3. Customer Experience: Balancing stringent KYC requirements with a seamless customer experience is another challenge. Lengthy and cumbersome KYC processes can lead to customer frustration and abandonment of the account opening or transaction processes. Striking the right balance between compliance and a smooth customer journey is crucial.

4. Technological Integration: As technology continues to transform the banking industry, integrating digital solutions for KYC implementation can be challenging. Banks must invest in advanced technologies, such as artificial intelligence and automation, to streamline the KYC process, improve efficiency, and enhance fraud detection capabilities.

5. Changing Customer Expectations: Customers now expect seamless digital experiences and quicker onboarding processes. However, stringent KYC requirements and regulatory obligations can create friction in meeting these expectations. Banks need to find innovative ways to meet customer demands while adhering to KYC compliance standards.

6. Cost and Resource Allocation: Implementing and maintaining a robust KYC framework can be cost-intensive for banks. The investment in technology, staff training, and compliance measures requires significant financial resources. Banks must carefully allocate resources to ensure effective KYC implementation while managing the overall operational costs.

7. Global Compliance Challenges: Banks operating across borders face the challenge of complying with different and sometimes conflicting KYC regulations in various jurisdictions. Harmonizing these regulations and establishing consistent processes across multiple geographies can be complex and time-consuming.

8. Evolving Fraud Techniques: Fraudsters continuously develop new techniques to bypass KYC controls and exploit vulnerabilities. Banks must stay vigilant and regularly update their KYC processes and systems to detect emerging fraud patterns and mitigate risks effectively.

Despite these challenges, banks recognize the importance of KYC in maintaining the integrity of the financial system and protecting themselves and their customers from financial crimes. Overcoming these challenges requires continuous investment in technology, ongoing staff training, collaboration with regulators, and staying ahead of evolving regulatory environments and fraud trends.

Recent developments in KYC regulations in banking

The field of KYC (Know Your Customer) regulations in the banking industry is continuously evolving to keep pace with changing financial landscapes and emerging risks. Let’s explore some of the recent developments in KYC regulations:

1. Emergence of Digital Identity Verification: Regulatory authorities and banks are increasingly embracing digital identity verification methods. This involves using advanced technologies such as biometrics, facial recognition, and machine learning algorithms to verify customer identities remotely and securely. Digital identity verification not only enhances the speed and convenience of the KYC process but also improves accuracy and fraud detection capabilities.

2. Focus on Risk-Based Approach: Regulatory frameworks are placing more emphasis on a risk-based approach to KYC. Instead of applying a one-size-fits-all approach, this approach allows banks to allocate their resources more efficiently by conducting enhanced due diligence on higher-risk customers. By adopting a risk-based approach, banks can tailor their KYC processes and apply stricter controls only when necessary.

3. Global Collaboration and Information Sharing: International regulatory bodies are promoting greater collaboration and information sharing between banks and regulatory authorities to combat financial crimes more effectively. Initiatives such as the FATF (Financial Action Task Force) recommendations and regional regulatory forums encourage sharing of KYC-related information and best practices to strengthen AML (Anti-Money Laundering) efforts and enhance cross-border compliance.

4. Enhanced Customer Due Diligence Requirements: Regulators are increasing their focus on customer due diligence (CDD) requirements as part of KYC processes. This includes gathering more comprehensive information about beneficial owners, conducting in-depth risk assessments, and scrutinizing politically exposed persons (PEPs) and high-risk entities more closely. These measures aim to prevent money laundering, terrorist financing, and other financial crimes.

5. Technological Innovations: Banks are investing in advanced technologies to streamline their KYC processes and enhance compliance. Robotic process automation (RPA), artificial intelligence (AI), and machine learning (ML) algorithms are being used to automate routine tasks, detect suspicious transactions, and improve the accuracy and efficiency of KYC procedures. These technological advancements enable banks to stay compliant while improving the customer experience.

6. Data Privacy and Protection: With the increasing collection and processing of customer data for KYC purposes, data privacy and protection have become paramount. Regulations such as the European Union’s General Data Protection Regulation (GDPR) require banks to implement stringent measures to secure and protect customer data. Compliance with data privacy regulations is a crucial aspect of KYC implementation.

7. Focus on KYC Training and Awareness: Regulatory authorities are emphasizing the importance of training and awareness programs for bank employees involved in KYC processes. Proper training helps ensure that employees understand the regulatory requirements, recognize red flags and suspicious activities, and apply KYC procedures effectively. Ongoing training and awareness programs enhance the overall effectiveness of the KYC process and contribute to a strong culture of compliance within banks.

These recent developments in KYC regulations reflect the industry’s commitment to combating financial crimes, improving operational efficiency, and safeguarding the financial system. By staying updated on these developments, banks can adapt their KYC processes to meet regulatory requirements and adopt technological advancements, contributing to a more secure and trustworthy banking environment.

Conclusion

KYC, or Know Your Customer, is a fundamental process in the banking industry that ensures the verification of customer identities, assessment of risks, and compliance with regulatory requirements. The importance of KYC cannot be overstated, as it serves to protect banks, customers, and the integrity of the financial system.

Through KYC, banks are able to prevent financial crimes such as fraud, money laundering, and terrorist financing. By gathering and verifying customer information, banks can detect and deter illicit activities, enhancing the overall security of the banking system. KYC also facilitates effective risk management by enabling banks to assess the risks associated with each customer and implement appropriate mitigation measures.

Compliance with KYC regulations is critical for banks to operate within the confines of the law. By adhering to regulatory requirements, banks mitigate the risk of penalties, legal consequences, and damage to their reputation. KYC also promotes transparency and accountability in the banking industry, contributing to a more robust and stable financial system.

Furthermore, KYC plays a significant role in building trust and confidence between banks and their customers. By implementing rigorous KYC procedures, banks assure customers that their financial interests are protected and that they are operating in a secure and regulated environment. This trust fosters long-term relationships and customer loyalty, benefiting both banks and customers.

While implementing KYC comes with its challenges, such as complex regulatory environments, technological integration, and customer experience considerations, banks must navigate these obstacles to ensure successful implementation. By investing in advanced technologies, effective training programs, and strong internal controls, banks can overcome these challenges and reap the benefits of KYC.

Recent developments in KYC regulations, such as digital identity verification, a risk-based approach, global collaboration, and technological innovations, have shaped the KYC landscape. Banks must adapt to these changes to maintain compliance, improve efficiency, and stay ahead of emerging risks in the financial industry.

In conclusion, the KYC process is essential in banking, offering numerous benefits including enhanced security, effective risk management, regulatory compliance, customer trust, and seamless onboarding experiences. By embracing the principles of KYC and continuously evolving to meet emerging challenges, banks can establish a safer, more secure, and resilient banking ecosystem for all stakeholders involved.