Introduction

In the world of banking, there are numerous acronyms and terms that can be confusing to individuals who are not familiar with the industry. One such term is CIP, which stands for Customer Identification Program. In the context of banking, CIP refers to the process through which financial institutions verify the identity of their customers. This is an important requirement that helps prevent money laundering, fraud, and other illicit activities.

As the banking industry becomes increasingly digitalized, it becomes even more crucial for financial institutions to have robust customer identification programs in place. In an era where personal information is vulnerable to cyber threats, ensuring the security and legitimacy of customer identities is essential.

The Customer Identification Program aims to establish and verify the identity of customers. By doing so, banks can better understand their customers, assess the risks associated with their accounts, and ensure compliance with regulatory requirements.

Through the CIP process, banks obtain various pieces of information from customers, such as their name, address, date of birth, and identification documents. This information is then used to verify the customer’s identity through reliable data sources, such as government databases and credit bureaus.

Although the CIP process may seem like an inconvenience to customers, it plays a vital role in protecting their assets and maintaining the integrity of the financial system. By implementing a strong Customer Identification Program, banks can minimize the risk of identity theft, money laundering, and terrorist financing.

Furthermore, the CIP process also acts as a deterrent to financial criminals. Knowing that their identities will be thoroughly checked and verified, potential wrongdoers are less likely to target banks as a platform for illegal activities.

It is important to note that the CIP is not a one-time process. Financial institutions are required to periodically update and re-verify customer information to ensure ongoing compliance and protection against fraudulent activities.

In the following sections, we will delve deeper into the details of the CIP process, its requirements, and the regulations that govern it. We will also examine the differences between CIP and the Know Your Customer (KYC) process, as well as the benefits and limitations of CIP in the banking industry.

Definition of CIP

The Customer Identification Program (CIP) is a fundamental aspect of banking operations that refers to the process through which financial institutions verify the identity of their customers. It is an essential component of the broader Know Your Customer (KYC) framework. The purpose of CIP is to establish the identity of individuals or entities who wish to open an account or conduct financial transactions with a bank.

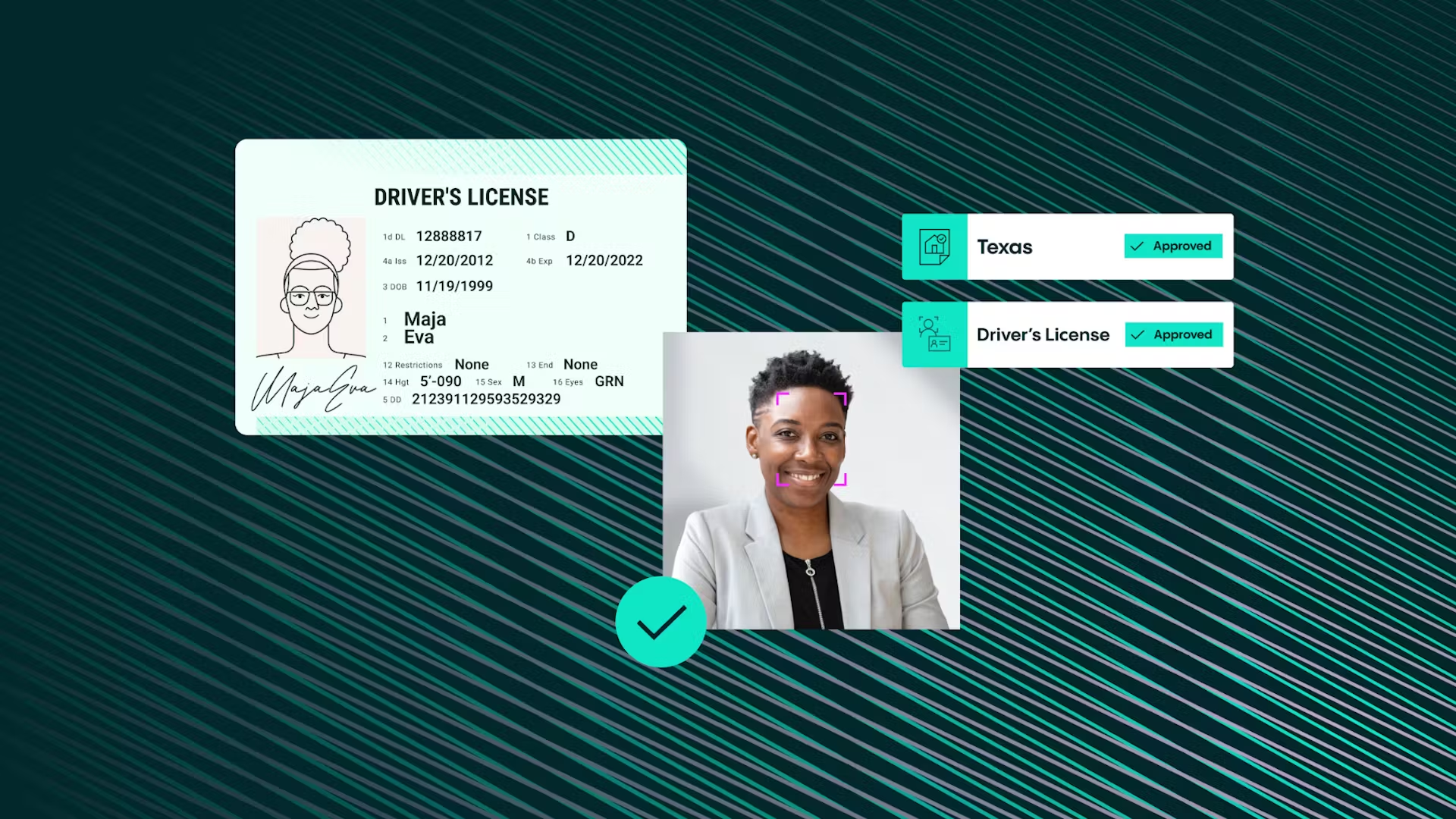

Under the CIP, financial institutions are required to collect specific information from customers, such as their full legal name, date of birth, residential or business address, and identification documentation. This information is used to verify the customer’s identity and assess any risks associated with their account.

The CIP process typically involves the collection of primary identification documents, such as government-issued IDs or passports, as well as secondary documents, like utility bills or bank statements, to confirm the customer’s address. Additionally, financial institutions may also employ technology-based verification methods, such as biometric identification or identity verification services.

It is important to note that the CIP requirements may vary slightly between countries and regulatory authorities. However, the overarching objective remains the same – to prevent financial crimes, including money laundering, terrorist financing, and fraud.

Financial institutions are responsible for developing and implementing robust CIP policies and procedures that comply with applicable laws and regulations. These policies ensure that banks have the necessary infrastructure and processes in place to effectively verify the identity of customers and assess any associated risks.

By enforcing customer identification through CIP, banks can not only mitigate the risks posed by financial crimes but also gain a deeper understanding of their customers. This understanding allows banks to tailor their products and services to meet the individual needs and risk profiles of their customers.

Furthermore, the CIP process enhances customer trust and confidence in the banking system. Customers can feel secure in knowing that their identities are being verified, especially in an increasingly digitized world where the risks of identity theft and fraud are ever-present.

In the upcoming sections, we will explore the importance of CIP in banking, the specific requirements of the CIP process, and how it differs from the broader KYC framework.

Importance of CIP in Banking

The Customer Identification Program (CIP) plays a vital role in the banking industry by ensuring the security, integrity, and compliance of financial transactions. The importance of CIP in banking cannot be overstated as it serves multiple purposes that benefit both financial institutions and their customers.

First and foremost, CIP helps banks prevent financial crimes such as money laundering, fraud, and terrorist financing. By verifying the identity of customers, financial institutions can deter criminals from using the banking system for illegal activities. The CIP process acts as a robust initial defense mechanism, mitigating the risk of funds being sourced from illicit activities and safeguarding the integrity of the financial system as a whole.

Secondly, CIP aids in fraud prevention and identity theft protection. By verifying the accuracy of customer information and confirming their identities, banks can better protect their customers’ accounts and mitigate the risks associated with unauthorized access. CIP helps ensure that financial transactions are conducted by legitimate account holders, reducing the likelihood of fraudulent activities.

Moreover, CIP enhances regulatory compliance for financial institutions. Compliance with Know Your Customer (KYC) rules and anti-money laundering regulations is a requirement for banks, and CIP serves as a critical component of these compliance efforts. By implementing a robust CIP process, financial institutions demonstrate their commitment to adhering to regulatory standards and maintaining a sound business reputation.

Additionally, CIP enables banks to assess and manage risks associated with their customers effectively. By capturing essential customer information during the identification process, banks can evaluate the potential risks of providing financial services to individuals or entities. This risk assessment allows banks to design appropriate risk management strategies, such as transaction monitoring systems and enhanced due diligence measures, to minimize financial risks.

Furthermore, CIP fosters a culture of trust and transparency between banks and their customers. When customers are required to provide identification and personal information as part of the CIP process, they can have confidence that their identities are being verified and their accounts are being protected. This assurance of security and integrity builds trust in the banking system and strengthens customer relationships.

In summary, the importance of CIP in banking cannot be understated. It safeguards the financial system, protects against financial crimes, prevents fraud, ensures regulatory compliance, manages risks, and fosters trust between banks and their customers. The robust implementation of CIP measures by financial institutions not only benefits their own operations but also contributes to the overall stability and integrity of the banking industry.

CIP Process and Requirements

The Customer Identification Program (CIP) process is a systematic approach employed by financial institutions to verify the identity of their customers. It involves the collection of specific information and supporting documentation to ensure compliance with regulatory requirements and mitigate risks associated with illicit activities. Let’s delve into the CIP process and its requirements.

1. Information Collection: When a customer wants to open an account or engage in financial transactions, the bank collects their personal information. This typically includes their full legal name, date of birth, residential or business address, and identification documentation.

2. Primary Identification Documents: Financial institutions require customers to provide primary identification documents to prove their identity. These documents can include government-issued IDs like passports, driver’s licenses, or national ID cards. The primary documents serve as the main source of verification for the customer’s identity.

3. Secondary Verification Documents: In addition to primary identification documents, banks may request secondary verification documents to confirm the customer’s address. These documents can include utility bills, bank statements, or other official statements that clearly show the customer’s name and address.

4. Technology-Based Verification: To enhance the verification process, financial institutions may employ technology-based methods. This can include biometric identification, where the customer’s fingerprints or facial features are scanned for verification, or using identity verification services that cross-reference customer information with reliable data sources.

5. Screening Processes: As part of the CIP process, financial institutions are required to screen customers against lists of individuals or entities known for involvement in money laundering, terrorism, or other illegal activities. This helps to ensure that banks do not unknowingly facilitate illicit financial activities.

6. Ongoing Monitoring and Updating: The CIP process is not a one-time event. Financial institutions are obligated to periodically monitor and update customer information to stay compliant with regulatory guidelines. This may involve requesting customers to provide updated identification documents or confirming their address if there are any changes.

7. Record-Keeping: Financial institutions are required to maintain records of the CIP process, including customer information and supporting documents. These records serve as evidence of compliance with regulatory requirements and may be subject to audits and examinations by the relevant authorities.

To ensure effective implementation of the CIP process, financial institutions are responsible for developing and implementing comprehensive policies and procedures. These policies outline the steps to be followed, the documentation required, and the responsibilities of bank employees involved in the CIP process.

CIP requirements may vary depending on the jurisdiction and regulatory authority. Banks need to stay updated with the specific rules and guidelines relevant to their operating region to ensure compliance.

In the next section, we will discuss the differences between the Customer Identification Program (CIP) and the Know Your Customer (KYC) process, and how they complement each other in the banking industry.

Customer Identification Program (CIP) vs. Know Your Customer (KYC)

The Customer Identification Program (CIP) and Know Your Customer (KYC) are two essential components of the regulatory framework that governs the banking industry. While they share similar objectives and are often used interchangeably, there are distinct differences between CIP and KYC.

CIP focuses specifically on the verification of the customer’s identity. It is a process through which financial institutions collect and verify customer information to establish their identity before opening an account or conducting financial transactions. The CIP process ensures compliance with anti-money laundering (AML) regulations and helps mitigate risks associated with financial crimes.

On the other hand, KYC is a broader concept that goes beyond customer identification. It encompasses the entire relationship between the financial institution and the customer. KYC involves the assessment of not only the customer’s identity but also their risk profile, source of funds, and overall suitability as a customer. It is a comprehensive procedure that aims to understand the customer’s financial activities, potential risks, and compliance with regulatory guidelines.

While CIP is a mandatory requirement for all customers, KYC is an ongoing process that involves periodic review and risk assessment of customers. Financial institutions use KYC measures to identify any changes in a customer’s risk profile and to ensure the continued compliance of customer accounts with applicable regulations.

Although CIP and KYC serve distinct purposes, they are interconnected. CIP acts as a foundational step within the broader spectrum of KYC. By verifying the identity of customers through CIP, financial institutions can gather the necessary information to conduct a comprehensive KYC assessment.

Through KYC, banks assess the customer’s risk profile based on factors such as their occupation, source of income, financial transactions, and relationship with high-risk jurisdictions. This helps financial institutions monitor for any suspicious activities or potential money laundering risks throughout the customer’s relationship with the bank.

Additionally, KYC also involves enhanced due diligence (EDD) measures that are applied to higher-risk customers or business relationships. These measures go beyond standard CIP procedures and involve more stringent verification and ongoing monitoring to mitigate the risks associated with these customers.

Both CIP and KYC are critical for financial institutions to maintain a robust compliance framework, prevent financial crimes, and ensure the integrity of the banking system. Through the combined efforts of CIP and KYC, banks can better assess and manage the risks associated with their customer base, protect against money laundering and fraud, and comply with regulatory requirements.

Next, we will explore the compliance and regulations related to CIP in the banking industry.

CIP Compliance and Regulations

The Customer Identification Program (CIP) is subject to various compliance requirements and regulations that financial institutions must adhere to. These regulations are put in place to ensure the integrity of the banking system, prevent money laundering, and combat financing of terrorist activities. Let’s take a closer look at CIP compliance and the regulations that govern it.

In the United States, the CIP framework is primarily regulated by the Bank Secrecy Act (BSA) and its implementing regulations, enforced by the Financial Crimes Enforcement Network (FinCEN). The BSA requires financial institutions to establish and maintain effective CIPs as part of their overall anti-money laundering (AML) programs.

Under the BSA’s CIP requirements, financial institutions are obligated to verify the identity of customers opening new accounts. They must collect specific customer information, such as the customer’s full legal name, date of birth, residential or business address, and identify verification documents.

Financial institutions are also required to screen customers against government lists of known or suspected terrorists or other persons engaged in illegal activities. This screening helps prevent financial institutions from unknowingly facilitating illegal transactions or providing services to high-risk individuals or entities.

Additionally, financial institutions must have written CIP policies and procedures in place that are approved by their board of directors. These policies and procedures outline the steps to be followed, the documentation required, and the responsibilities of bank employees involved in the CIP process.

It is important to note that CIP compliance requirements may vary from jurisdiction to jurisdiction, as different countries have their own regulatory bodies and guidelines. Financial institutions must stay informed about the specific regulatory requirements in their operating jurisdictions to ensure compliance.

Non-compliance with CIP regulations can have severe consequences for financial institutions, including monetary penalties, reputational damage, and legal consequences. Regulatory authorities conduct regular examinations and audits to assess the effectiveness of financial institutions’ CIP programs and ensure compliance with applicable regulations.

To ensure compliance with CIP requirements, financial institutions should implement robust internal controls, provide ongoing training to employees involved in the CIP process, and maintain proper record-keeping. Regular internal audits and assessments can help identify any weaknesses or gaps in the CIP program and facilitate remedial actions.

Financial institutions also collaborate with regulatory bodies, industry associations, and other stakeholders to stay up-to-date with emerging trends, regulatory changes, and best practices in CIP compliance.

In the next section, we will discuss the benefits and limitations of implementing a strong Customer Identification Program in the banking industry.

Benefits and Limitations of CIP

The Customer Identification Program (CIP) offers several benefits to financial institutions and customers alike. However, it is not without its limitations. Let’s explore the benefits and limitations of implementing a strong CIP in the banking industry.

Benefits of CIP:

1. Risk Mitigation: CIP helps financial institutions mitigate the risks associated with money laundering, fraud, and terrorist financing. By verifying the identity of customers, banks can deter criminals from using the banking system for illegal activities, thus protecting their own reputation and integrity.

2. Enhanced Security: CIP plays a critical role in protecting customer accounts from unauthorized access and identity theft. By ensuring that financial transactions are conducted by legitimate account holders, CIP fosters a secure environment for customers to engage in banking activities.

3. Regulatory Compliance: Implementing a robust CIP program ensures regulatory compliance with anti-money laundering and counter-terrorism financing regulations. Financial institutions that comply with these regulations maintain their licenses, avoid monetary penalties, and protect themselves from reputational damage.

4. Strengthened Customer Trust: When customers know that their identities are being verified and their accounts are protected, they develop trust and confidence in the banking system. CIP fosters transparency and reassures customers that their financial transactions are conducted securely.

Limitations of CIP:

1. Customer Inconvenience: The CIP process can be time-consuming and may require customers to provide various documents and information. Some customers may find this additional step inconvenient, leading to potential frustration or hindrances in the account opening process.

2. False Sense of Security: While CIP is designed to verify the identity of customers, it does not guarantee that all risks associated with financial transactions will be eliminated. Sophisticated fraudsters may still find ways to bypass the CIP process, potentially resulting in financial losses for customers and banks alike.

3. High Cost of Compliance: Implementing and maintaining a comprehensive CIP program can be costly for financial institutions. This includes investing in technology, employee training, and establishing internal controls to ensure compliance with regulatory requirements.

4. Incomplete Coverage: CIP focuses primarily on individual customers and may not be as effective in identifying risks and red flags associated with complex business structures or transactions involving multiple parties. This limitation highlights the importance of coupling CIP with other due diligence measures to enhance risk assessment.

Despite the limitations, the benefits of a robust CIP program outweigh the challenges faced. By implementing comprehensive procedures, leveraging technology, and staying updated on regulatory changes, financial institutions can effectively mitigate risks, protect customer accounts, and maintain compliance with the evolving landscape of financial regulations.

In the next section, we will conclude with a summary of the key points discussed in this article.

Conclusion

The Customer Identification Program (CIP) is a crucial aspect of banking operations that ensures the verification of customer identities and compliance with regulatory requirements. By establishing the identity of customers, financial institutions can mitigate the risks associated with financial crimes, protect customer accounts, and maintain the integrity of the banking system.

CIP plays a vital role in preventing money laundering, fraud, and terrorist financing. Through the collection and verification of customer information, banks can deter criminals from using the banking system for illegal activities and protect themselves from reputational damage and regulatory penalties.

Furthermore, CIP enhances customer trust and confidence in the banking system. By verifying their identities and protecting their accounts, customers can engage in financial transactions with peace of mind, knowing that their information is secure.

However, it is important to recognize the limitations of CIP, such as the inconvenience it may pose to customers or the potential for false security. Financial institutions must strike a balance between implementing robust CIP procedures and addressing the challenges presented by evolving financial crimes and fraud techniques.

To ensure CIP compliance, financial institutions must develop comprehensive policies and procedures, leverage technology, and invest in employee training. Regular internal audits and assessments are also essential to identify any weaknesses or gaps in the CIP program and rectify them promptly.

In conclusion, the Customer Identification Program is a critical component of the banking industry that serves to protect financial institutions, customers, and the broader financial system. By diligently implementing and maintaining a strong CIP program, banks can mitigate risks, comply with regulations, and strengthen customer trust in the security and integrity of their financial services.