What is BSA in Banking?

BSA, which stands for the Bank Secrecy Act, is a crucial piece of legislation in the financial industry. Enacted in 1970, the BSA is aimed at combating money laundering, terrorist financing, and other financial crimes. It requires U.S. financial institutions to establish and maintain effective programs to detect and report suspicious activities that may indicate money laundering or other illicit activities.

The primary objective of BSA is to assist law enforcement agencies in their investigations by providing a paper trail of financial activity. This information can be invaluable in identifying and apprehending criminals involved in illegal financial transactions.

BSA compliance is mandatory for all banks and financial institutions operating in the United States, including commercial banks, credit unions, thrifts, and trust companies. These institutions are required to implement comprehensive compliance programs, conduct due diligence, and report suspicious transactions to the Financial Crimes Enforcement Network (FinCEN), a division of the U.S. Department of the Treasury.

Under BSA, financial institutions must establish customer identification procedures and maintain records of customer transactions. They must also monitor account activity for suspicious patterns and report any suspicious transactions to FinCEN in the form of currency transaction reports (CTRs) or suspicious activity reports (SARs).

BSA also requires banks to conduct ongoing staff training to ensure that employees are aware of their responsibilities and understand how to identify and report suspicious activities. This training is crucial for maintaining a high level of vigilance and compliance within the financial institution.

Overall, BSA plays a vital role in safeguarding the integrity of the financial system by deterring and detecting illicit financial activities. It not only protects banks from being exploited by criminals but also helps maintain the trust and confidence of customers in the banking system.

The Basics of BSA

The Bank Secrecy Act (BSA) establishes the framework for regulations and requirements relating to anti-money laundering (AML) and combating the financing of terrorism (CFT) in the United States. It serves as a crucial tool in detecting and reporting suspicious financial activities. Understanding the basics of BSA is essential for all banking professionals and financial institutions.

One of the key components of the BSA is the implementation of a comprehensive compliance program. This program includes policies, procedures, and internal controls designed to prevent money laundering and terrorist financing. It requires financial institutions to conduct due diligence on their customers, maintain accurate records of customer transactions, and report suspicious activities to the appropriate authorities.

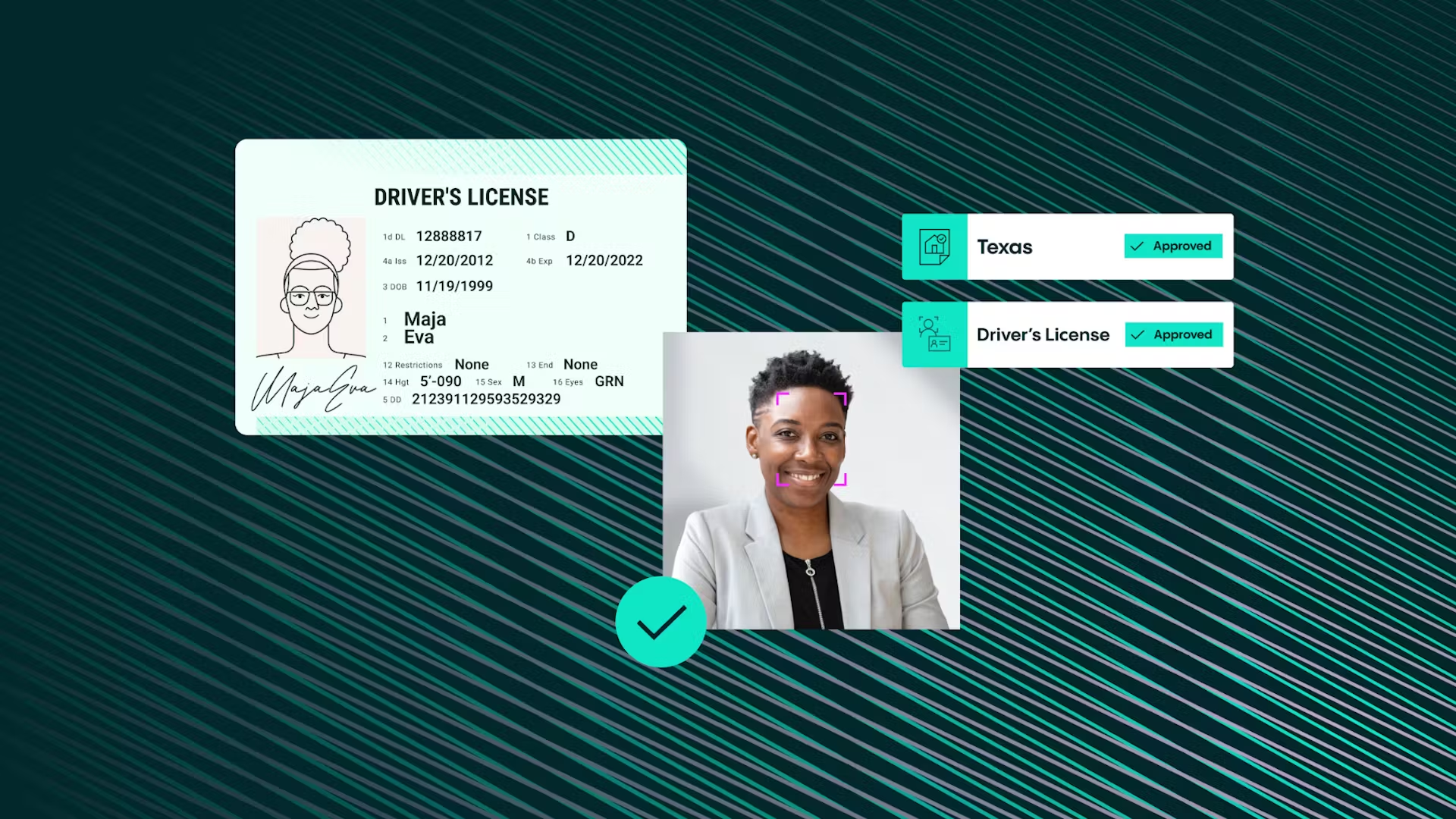

Another fundamental aspect of BSA is the requirement for banks and financial institutions to establish customer identification procedures. These procedures involve verifying the identity of customers through various means, such as obtaining identification documents and conducting background checks. By implementing robust customer identification procedures, banks can mitigate the risk of facilitating illicit financial activities.

BSA also mandates the filing of various reports to the Financial Crimes Enforcement Network (FinCEN). Currency Transaction Reports (CTRs) must be filed for cash transactions exceeding $10,000 in a single day. Suspicious Activity Reports (SARs) are filed when a transaction or pattern of transactions appears suspicious or may involve illegal activities.

Compliance with BSA is not optional; it is a legal requirement for all financial institutions operating in the United States. Failure to comply with BSA can result in severe penalties, including hefty fines, reputation damage, and even criminal charges. Therefore, it is crucial for banks and financial institutions to dedicate resources to ensure full compliance with the BSA regulations.

Training and education are essential components of BSA compliance. Banks must provide ongoing training to their employees, ensuring they are knowledgeable about BSA requirements and equipped to identify red flags associated with money laundering and terrorist financing. Training programs should cover topics such as customer due diligence, transaction monitoring, recordkeeping, and reporting obligations.

By adhering to the basics of BSA, financial institutions play a vital role in protecting the integrity of the financial system and preventing the misuse of their services for illicit purposes. Compliance with BSA not only helps banks identify and report suspicious activities but also ensures a level playing field among financial institutions, fostering transparency and accountability.

Why is BSA important for banks?

The Bank Secrecy Act (BSA) holds immense importance for banks and financial institutions. It serves as a crucial framework for identifying and combatting illegal financial activities, such as money laundering and terrorist financing. Here are several reasons why BSA compliance is vital for banks:

1. Preventing Money Laundering: BSA regulations require banks to establish robust systems and controls to detect and deter money laundering. By implementing strong customer identification procedures, conducting thorough due diligence, and monitoring transactions, banks can identify suspicious activities and report them to the appropriate authorities. This helps prevent money laundering and protects the integrity of the financial system.

2. Combating Terrorist Financing: BSA regulations play a significant role in the fight against terrorism. Financial institutions are required to monitor and report any financial transactions that may be linked to terrorist activities. By complying with BSA requirements, banks contribute to national security efforts and help disrupt funding for terrorist organizations.

3. Upholding Regulatory Compliance: Compliance with BSA is not optional; it is a legal requirement for banks and financial institutions. Ensuring BSA compliance helps banks avoid potential penalties, fines, and legal actions. It also helps maintain a positive reputation and fosters trust among regulators, customers, and other stakeholders.

4. Protecting Customers and the Financial System: BSA regulations aim to protect both banks and their customers. By implementing customer identification procedures and conducting ongoing monitoring, banks can identify and prevent fraudulent activities that may harm their customers. Additionally, BSA compliance helps safeguard the financial system from the risks posed by illicit activities.

5. Enhancing the Bank’s Risk Management Framework: BSA compliance is an integral part of a bank’s overall risk management framework. Implementing the necessary systems, policies, and procedures helps banks effectively manage and mitigate the risks associated with money laundering, terrorist financing, and other financial crimes.

6. Supporting Law Enforcement: BSA regulations require banks to report suspicious activities to the appropriate authorities. By doing so, banks provide valuable information and contribute to law enforcement efforts in investigating and prosecuting financial crimes. Banks act as a crucial bridge between the financial sector and law enforcement agencies.

7. Strengthening International Cooperation: BSA compliance promotes international cooperation and coordination in combatting financial crimes. Financial institutions that adhere to the BSA requirements contribute to the sharing of information and the united fight against money laundering and terrorist financing on a global scale.

In summary, BSA compliance is essential for banks to fulfill their legal obligations, protect the financial system, and prevent money laundering and terrorist financing. By implementing robust systems, conducting thorough due diligence, and reporting suspicious activities, banks play a crucial role in maintaining the integrity of the financial sector and supporting the broader efforts in combating financial crimes.

The Role of BSA Officers

BSA Officers play a critical role in ensuring compliance with the Bank Secrecy Act (BSA) and regulations related to anti-money laundering (AML) and combating the financing of terrorism (CFT). These dedicated individuals are responsible for overseeing the development, implementation, and maintenance of comprehensive BSA compliance programs within financial institutions. Here is an overview of the key responsibilities and duties of BSA Officers:

1. Designing and Implementing BSA Compliance Programs: BSA Officers are responsible for developing and implementing effective BSA compliance programs in accordance with regulatory requirements. This involves creating policies, procedures, and internal controls that address customer identification, transaction monitoring, and reporting of suspicious activities.

2. Ensuring Ongoing Compliance: BSA Officers are responsible for ensuring that the financial institution remains compliant with BSA regulations on an ongoing basis. This involves conducting regular risk assessments to identify areas of potential vulnerability and implementing necessary measures to mitigate those risks.

3. Conducting Training and Education: BSA Officers are responsible for providing training and educational programs to employees throughout the organization. This ensures that all staff members are aware of BSA requirements, understand their role in compliance, and can identify and report suspicious activities.

4. Overseeing Customer Due Diligence: BSA Officers are responsible for developing and implementing procedures for customer due diligence (CDD), including customer identification and risk assessment. They ensure that appropriate measures are in place to verify customer identities and assess the risk associated with their financial transactions.

5. Monitoring and Reporting Suspicious Activities: BSA Officers oversee the monitoring of customer transactions for suspicious patterns or activities. They are responsible for ensuring that adequate systems are in place to identify and report suspicious activities to the appropriate regulatory authorities, such as filing Currency Transaction Reports (CTRs) and Suspicious Activity Reports (SARs).

6. Maintaining Documentation and Records: BSA Officers are responsible for keeping accurate records of customer transactions and implementing appropriate recordkeeping systems. They ensure that all required documentation is properly maintained and readily available for examination during regulatory audits or investigations.

7. Liaising with Regulatory Agencies: BSA Officers act as the main point of contact between the financial institution and regulatory agencies, such as the Financial Crimes Enforcement Network (FinCEN). They stay updated on changes in BSA regulations and guidelines, communicate with regulators, and address any queries or concerns raised by regulatory authorities.

8. Conducting Internal Audits and Assessments: BSA Officers are responsible for conducting regular internal audits and assessments to evaluate the effectiveness of the BSA compliance program. These audits help identify areas of improvement, ensure adherence to policies and procedures, and address any deficiencies or weaknesses in the compliance program.

Overall, BSA Officers play a vital role in ensuring that financial institutions adhere to BSA regulations and implement effective measures to combat money laundering and terrorist financing. Their expertise and dedication are crucial in protecting the integrity of the financial system, mitigating risks, and maintaining compliance with applicable laws and regulations.

BSA Compliance Requirements

Compliance with the Bank Secrecy Act (BSA) is essential for all banks and financial institutions operating in the United States. Failure to meet BSA compliance requirements can result in severe penalties and reputational damage. Here are the key compliance requirements that financial institutions must adhere to:

1. Developing a BSA Compliance Program: Financial institutions are required to establish and maintain an effective BSA compliance program. This program should include comprehensive policies, procedures, and internal controls designed to detect and prevent money laundering, terrorist financing, and other illicit activities. The program must be tailored to the specific risks faced by the institution.

2. Customer Identification Program (CIP): Financial institutions must implement a robust customer identification program (CIP) to verify the identity of customers. This includes obtaining identifying information, such as name, address, date of birth, and social security number, and verifying the accuracy of this information through reliable sources.

3. Ongoing Monitoring of Customer Transactions: Financial institutions are responsible for conducting ongoing monitoring of customer transactions to identify suspicious activities. This includes monitoring account activity for unusual patterns, large cash transactions, frequent structuring of transactions, and other red flags that may indicate potential money laundering or illicit financial activities.

4. Reporting Suspicious Activities: Financial institutions are required to file suspicious activity reports (SARs) with the Financial Crimes Enforcement Network (FinCEN) for transactions or patterns of transactions that appear suspicious. This includes any activity that may indicate money laundering, terrorist financing, or involvement in other criminal activities.

5. Currency Transaction Reports (CTRs): Financial institutions must file currency transaction reports (CTRs) with FinCEN for cash transactions exceeding $10,000 in a single day. This helps identify potential instances of structuring or other attempts to avoid reporting requirements.

6. Conducting Due Diligence: Financial institutions are required to conduct customer due diligence (CDD) to assess the risk posed by their customers. This includes collecting information about the customer’s background, occupation, and source of funds, as well as periodically updating this information based on risk factors.

7. Recordkeeping Requirements: Financial institutions must maintain records of customer transactions and other relevant documents for a specified period, typically five years. This includes records of CIP verification, CTRs, SARs, and other supporting documents that demonstrate compliance with BSA regulations.

8. Staff Training and Education: Financial institutions must provide regular training and education to their staff to ensure they are aware of BSA compliance requirements and understand their roles and responsibilities in detecting and reporting suspicious activities. Training should cover topics such as customer due diligence, transaction monitoring, and reporting obligations.

9. Independent Testing and Internal Controls: Financial institutions are required to conduct independent testing of their BSA compliance programs to evaluate their effectiveness and identify any weaknesses or deficiencies. They must also establish and maintain adequate internal controls to ensure compliance with BSA regulations.

By adhering to these BSA compliance requirements, financial institutions can effectively combat money laundering, terrorist financing, and other illicit financial activities. It is essential for institutions to dedicate resources and implement robust measures to ensure ongoing compliance and protect themselves from potential legal and reputational risks.

Common BSA Violations and Penalties

Compliance with the Bank Secrecy Act (BSA) is of utmost importance for financial institutions. Failure to meet BSA requirements can result in severe consequences, including significant penalties and reputational damage. Here are some common BSA violations and the potential penalties associated with them:

1. Failure to Establish a BSA Compliance Program: Financial institutions that fail to develop and maintain an effective BSA compliance program can face substantial penalties. The penalties can range from monetary fines to restrictions on business operations. Regulators expect financial institutions to have comprehensive policies, procedures, and internal controls in place to detect and report suspicious activities.

2. Inadequate Customer Due Diligence (CDD): Financial institutions must conduct thorough customer due diligence, including verifying customer identities and assessing the risk associated with their financial transactions. Failure to conduct proper CDD exposes institutions to potential penalties, as it undermines the ability to identify and report suspicious activities. Penalties for inadequate CDD can include significant fines and regulatory enforcement actions.

3. Failure to Report Suspicious Activities: Financial institutions are required to file suspicious activity reports (SARs) with the Financial Crimes Enforcement Network (FinCEN) for transactions or patterns of transactions that appear suspicious. Failure to timely and accurately file SARs can result in substantial penalties, including monetary fines and regulatory sanctions.

4. Failure to File Currency Transaction Reports (CTRs): Financial institutions must file currency transaction reports (CTRs) for cash transactions exceeding $10,000 in a single day. Failure to file CTRs or deliberate attempts to structure transactions to avoid reporting requirements can lead to penalties, including significant fines and possible criminal charges.

5. Inadequate Recordkeeping: Financial institutions must maintain accurate and complete records of customer transactions and other relevant documents. Inadequate recordkeeping practices can result in penalties, as it hampers the ability to demonstrate compliance with BSA regulations. Penalties for inadequate recordkeeping can include fines, regulatory actions, and reputational damage.

6. Failure to Provide Adequate BSA Training: Financial institutions must provide regular BSA training to their employees to ensure they are aware of compliance requirements and understand their obligations. Failure to provide adequate training can result in penalties, as it increases the risk of non-compliance and inability to detect and report suspicious activities.

7. Knowingly Assisting in Money Laundering or Terrorist Financing: Financial institutions or individuals within the institution who knowingly assist in money laundering or terrorist financing activities can face severe penalties, including imprisonment, fines, and forfeiture of assets. The authorities take a strong stance against those who intentionally facilitate illicit financial activities.

It is important for financial institutions to prioritize BSA compliance and establish effective internal controls to mitigate the risk of violations. Proactive measures to identify and address potential compliance gaps can help institutions avoid penalties and safeguard their reputation within the financial industry.

How BSA Affects Customers

The Bank Secrecy Act (BSA) has a direct impact on customers of financial institutions. While the main objective of BSA is to combat money laundering and terrorist financing, it also affects customers in several ways. Here are some ways in which BSA regulations can impact customers:

1. Enhanced Customer Due Diligence: BSA requires financial institutions to implement robust customer due diligence measures. As a result, customers may experience additional scrutiny during the account opening process or when conducting large transactions. They may be required to provide additional identification documents or answer questions about the sources of their funds. While this may cause a slight inconvenience, it helps ensure the integrity of the financial system and protects customers from potential risks.

2. Increased Account Monitoring: Financial institutions are obligated to monitor customer accounts for suspicious activities as part of their BSA compliance. This may involve the use of advanced technology and systems that analyze transactions for unusual patterns or signs of illicit activities. Customers may notice increased oversight of their account activity, such as notifications or inquiries from the bank regarding specific transactions. This monitoring is necessary to detect and prevent fraudulent or criminal activities that could harm both the customer and the financial institution.

3. Privacy and Confidentiality: BSA regulations require financial institutions to maintain customer information and transaction records. While this helps in combating financial crimes, it also raises concerns about privacy and confidentiality. However, financial institutions are bound by strict confidentiality laws, and customer information is only shared with authorized individuals or disclosed as required by law. The aim is to strike a balance between protecting customer privacy and preventing illicit financial activities.

4. Enhanced Security Measures: BSA regulations encourage financial institutions to implement robust security measures to protect customer accounts and sensitive information. This can include technologies like multi-factor authentication, encryption, and sophisticated fraud detection systems. Customers benefit from these security measures as they provide an additional layer of protection against unauthorized access, identity theft, and fraudulent transactions.

5. Availability of Financial Services: BSA compliance helps maintain the integrity of the financial system, which in turn improves the availability and reliability of financial services. By preventing money laundering and terrorist financing, BSA regulations contribute to a stable and trustworthy banking environment. This instills confidence in customers, ensuring that they can access the necessary financial services and products without undue risks.

6. Reporting of Suspicious Activities: BSA requires financial institutions to report any suspicious activities to the appropriate authorities. This reporting obligation helps protect customers from potential financial crimes and contributes to the overall safety of the financial system. Through the detection and reporting of suspicious activities, financial institutions play a vital role in preventing fraud and ensuring the security of customer assets.

While BSA compliance may introduce additional processes and requirements for customers, its ultimate goal is to safeguard the financial system and protect customers from potential risks. By adhering to BSA regulations, financial institutions work towards creating a secure and transparent banking environment, maintaining the trust and confidence of their customers.

BSA Reporting and Recordkeeping Requirements

The Bank Secrecy Act (BSA) imposes specific reporting and recordkeeping requirements on financial institutions to ensure transparency and facilitate the detection of money laundering, terrorist financing, and other illicit financial activities. Here are the key elements of BSA reporting and recordkeeping requirements:

1. Currency Transaction Reports (CTRs): Financial institutions are required to file Currency Transaction Reports (CTRs) for cash transactions exceeding $10,000 in a single business day. CTRs provide a record of large cash transactions and help authorities monitor potential money laundering or illegal activities. It is important for financial institutions to accurately and timely submit CTRs to the Financial Crimes Enforcement Network (FinCEN).

2. Suspicious Activity Reports (SARs): Financial institutions must file Suspicious Activity Reports (SARs) when they detect or suspect suspicious activities that may indicate money laundering, terrorist financing, or other illicit activities. SARs help law enforcement agencies investigate and prevent financial crimes. Financial institutions should have robust internal mechanisms and procedures to identify, document, and report suspicious activities promptly and accurately to FinCEN.

3. Recordkeeping: BSA requires financial institutions to maintain detailed records about their customers, transactions, and compliance efforts. This includes accurate records of customer identification, account activity, CTRs, SARs, and other relevant documentation. Records should be retained for a minimum of five years, and they must be readily available for inspection by regulatory authorities.

4. Customer Identification Program (CIP) Records: Financial institutions must maintain records related to their Customer Identification Programs (CIPs). This includes records of customer identification verification, such as copies of identification documents, as well as any additional information obtained during the CIP process. These records can help demonstrate compliance with CIP requirements and provide evidence of due diligence in customer onboarding.

5. Beneficial Ownership Records: Under FinCEN’s Customer Due Diligence (CDD) rule, financial institutions must collect beneficial ownership information for certain types of accounts. This includes maintaining records of the beneficial owners of legal entity customers and the verification steps taken to identify them. Accurate and up-to-date beneficial ownership records are crucial for demonstrating compliance with CDD requirements and preventing the misuse of accounts for illicit purposes.

6. Wire Transfer Records: Financial institutions must retain records of wire transfers and be able to provide certain information upon request. This includes details such as the originator and beneficiary of the transfer, the amount, and any accompanying messages. Wire transfer records are important for tracking and investigating potential money laundering or terrorist financing activities.

7. Compliance Program Documentation: Financial institutions must maintain documentation related to their BSA compliance programs. This includes policies, procedures, training materials, risk assessments, and any assessments or audits conducted to measure program effectiveness. Documentation helps demonstrate the institution’s commitment to compliance and assists in identifying areas for improvement in the compliance program.

8. Information Sharing Records: Financial institutions may participate in information sharing initiatives to facilitate the exchange of information related to potential money laundering or terrorist financing activities. They should maintain records of any information shared with other institutions or law enforcement agencies to document their contribution to anti-money laundering efforts.

Adhering to BSA reporting and recordkeeping requirements is crucial for financial institutions to ensure compliance, facilitate investigations of financial crimes, and contribute to the overall integrity of the financial system. Institutions must establish robust systems and processes to accurately report and maintain necessary records and cooperate with regulatory authorities in their efforts to combat illicit financial activities.

BSA and Money Laundering

The Bank Secrecy Act (BSA) plays a pivotal role in combating money laundering, a process used to disguise the illicit origins of criminal proceeds. By imposing strict reporting and recordkeeping requirements, BSA helps financial institutions detect and prevent money laundering activities. Here’s how BSA contributes to the fight against money laundering:

1. Identification and Reporting of Suspicious Activities: BSA mandates financial institutions to establish systems to identify and report suspicious activities that may indicate money laundering or other illicit financial transactions. This includes monitoring customer transactions for red flags such as large cash deposits, structuring transactions to avoid reporting requirements, or unexplained fund transfers. Prompt reporting through Suspicious Activity Reports (SARs) enables law enforcement agencies to investigate potential money laundering activities.

2. Currency Transaction Reports (CTRs): Financial institutions are required to file Currency Transaction Reports (CTRs) for cash transactions exceeding $10,000 in a single day. CTRs provide a record of large cash transactions, which is valuable in detecting structuring or layering techniques commonly used in money laundering schemes. CTRs, combined with other reports and information, help authorities identify potential money laundering activities and follow the money trail.

3. Customer Due Diligence (CDD) Measures: BSA regulations require financial institutions to implement robust Customer Due Diligence measures to identify their customers, understand the nature and purpose of their accounts, and assess the risk of money laundering. These measures include verifying customer identities, understanding the source of their funds, and monitoring transactions for any unusual or suspicious activities.

4. Enhanced Compliance Programs: BSA requires financial institutions to develop and maintain comprehensive compliance programs tailored to their specific risks. These programs include policies, procedures, and internal controls that focus on detecting, preventing, and reporting money laundering activities. By establishing effective compliance programs, financial institutions can mitigate the risk of being exploited by money launderers and contribute to the overall effort to combat money laundering.

5. International Cooperation: BSA fosters international cooperation in the fight against money laundering. Financial institutions that comply with BSA requirements contribute to the sharing of information and cooperation with foreign counterparts to trace and track cross-border money laundering activities. Such collaboration helps expose and disrupt complex money laundering networks operating globally.

6. Assistance to Law Enforcement Agencies: BSA facilitates the collaboration between financial institutions and law enforcement agencies in combating money laundering. Financial institutions act as front-line gatekeepers by detecting and reporting suspicious activities. By promptly providing valuable information through SARs and other required reports, financial institutions assist law enforcement agencies in their investigations, leading to the identification and prosecution of money launderers.

Overall, BSA serves as a critical tool in the fight against money laundering. By compelling financial institutions to establish robust compliance programs, monitor transactions, and report suspicious activities, BSA helps disrupt money laundering schemes, protect the integrity of the financial system, and contribute to the global efforts to combat crime and illicit financial activities.

BSA Programs and Training for Banks

BSA Programs and training are essential for banks to ensure compliance with the Bank Secrecy Act (BSA), effectively detect and prevent money laundering, terrorist financing, and other financial crimes. Here’s how banks establish BSA programs and provide training to their employees:

1. BSA Compliance Programs: Banks are required to develop and implement comprehensive BSA compliance programs tailored to their specific risks. These programs should include policies, procedures, and controls designed to detect and mitigate the risk of money laundering and terrorist financing. BSA officers and compliance teams play a crucial role in developing and overseeing these programs, ensuring that they meet regulatory requirements and align with the bank’s risk profile.

2. Risk Assessment: As part of BSA compliance programs, banks conduct periodic risk assessments to identify and evaluate their exposure to money laundering and other illicit financial activities. The risk assessment helps banks understand their vulnerabilities and determines the adequacy of controls and mitigation measures. It also guides the allocation of resources for monitoring, reporting, and training efforts.

3. Employee Training: Banks provide regular BSA training to their employees to enhance their knowledge and understanding of BSA compliance requirements. Training programs cover a wide range of topics, including customer due diligence, transaction monitoring, suspicious activity reporting, recordkeeping, and regulatory updates. Training ensures that employees are aware of their obligations, know how to identify potential risks and suspicious activities, and understand the proper protocols for reporting.

4. Senior Management Oversight: Banks must have active involvement and oversight from senior management in BSA compliance programs. Senior management plays a crucial role in establishing a culture of compliance, allocating resources, and making informed decisions to address compliance risks. They also champion the importance of BSA compliance within the organization and provide the necessary support for training initiatives.

5. Ongoing Monitoring and Review: Banks continuously monitor their BSA programs to ensure effectiveness and make necessary adjustments as regulations and risks evolve. This includes periodic reviews of policies, procedures, and internal controls to identify areas for improvement. Internal audits and assessments are conducted to evaluate the adequacy of BSA compliance programs and identify any deficiencies or weaknesses that require corrective action.

6. Regulatory Updates: Banks stay updated on changes to BSA regulations and guidance issued by regulatory authorities such as the Financial Crimes Enforcement Network (FinCEN). They actively monitor updates and incorporate any necessary changes into their BSA programs and training materials. This ensures that employees remain informed and trained on the latest compliance requirements.

7. Employee Engagement and Reporting: Banks encourage a culture of compliance by fostering employee engagement and providing channels for reporting potential suspicious activities. Employees are the frontline defense against money laundering and are encouraged to report any suspicions or red flags to the bank’s compliance department. Whistleblower protection policies may be implemented to protect employees who report suspicious activities in good faith.

Through robust BSA programs and comprehensive employee training, banks can establish a strong foundation for BSA compliance. These efforts enable banks to proactively detect and prevent illicit financial activities, maintain the integrity of the financial system, and protect themselves and their customers from the risks associated with money laundering and terrorist financing.

BSA and the Role of FinCEN

The Bank Secrecy Act (BSA) is enforced and regulated by the Financial Crimes Enforcement Network (FinCEN), a bureau of the U.S. Department of the Treasury. FinCEN plays a crucial role in ensuring compliance with BSA regulations and combating money laundering, terrorist financing, and other financial crimes. Here’s how FinCEN contributes to the enforcement and oversight of BSA:

1. Regulatory Guidance and Rulemaking: FinCEN provides regulatory guidance and issues rules and regulations to help financial institutions interpret and comply with BSA requirements. This includes providing interpretive guidance, Frequently Asked Questions (FAQs), and Advisory Notices that assist banks in implementing effective compliance programs and addressing emerging issues.

2. Reporting and Analysis: Financial institutions are required to submit various reports to FinCEN, including Currency Transaction Reports (CTRs) and Suspicious Activity Reports (SARs). FinCEN collects, stores, and analyzes this information to gain insights into money laundering patterns, detect trends, and develop strategies to disrupt illicit financial activities. The data collected by FinCEN also assists law enforcement agencies in their investigations.

3. Information Sharing and Coordination: FinCEN facilitates the sharing of information among financial institutions, regulatory agencies, and law enforcement entities both domestically and internationally. FinCEN acts as a central hub for the collection, analysis, and dissemination of BSA-related information. This collaboration strengthens the collective effort to combat money laundering and terrorist financing.

4. FinCEN Exchange: FinCEN Exchange is an initiative launched by FinCEN to enhance public-private partnerships and information sharing. It brings together financial institutions and representatives from law enforcement agencies to collaborate and exchange information on money laundering and other illicit financial activities. The FinCEN Exchange facilitates an open dialogue to identify and mitigate common risks.

5. Enforcement and Penalties: FinCEN has the authority to enforce BSA compliance and impose penalties for violations. It conducts examinations and investigations of financial institutions to assess their compliance with BSA regulations. In cases of non-compliance, FinCEN may impose civil monetary penalties, issue cease and desist orders, or refer cases for criminal prosecution.

6. International Cooperation: FinCEN actively collaborates with international counterparts, financial intelligence units, and regulatory bodies to combat global money laundering and terrorist financing networks. FinCEN participates in and promotes international initiatives that facilitate the exchange of financial intelligence and enhance coordination in the fight against financial crimes.

7. Supervision and Guidance: FinCEN provides supervision and guidance to financial institutions through the BSA examination process. Their examiners review financial institutions’ compliance with BSA regulations, conduct risk assessments, and provide guidance on areas that need improvement. This supervision helps ensure consistent and effective implementation of BSA requirements across the financial industry.

Through its regulatory oversight, information analysis, enforcement actions, and international cooperation, FinCEN plays a fundamental role in the effective implementation and enforcement of BSA. By closely partnering with financial institutions, regulatory agencies, and law enforcement bodies, FinCEN contributes to the ongoing fight against money laundering, terrorist financing, and other financial crimes, ultimately safeguarding the integrity of the U.S. financial system.