What is Nacha?

Nacha, an acronym for the National Automated Clearing House Association, is an organization that oversees the ACH (Automated Clearing House) network in the United States. Established in 1974, Nacha facilitates the efficient and secure movement of electronic payments between financial institutions. It functions as a self-regulatory body, creating and enforcing rules and standards to ensure the smooth operation of electronic transactions.

The ACH network managed by Nacha encompasses a variety of payment types, including direct deposits, direct payments, and business-to-business transactions. It serves as a crucial backbone for financial institutions and businesses, enabling them to process electronic payments quickly, securely, and cost-effectively.

Nacha plays a pivotal role in the modern banking industry by providing a reliable infrastructure for electronic payments. It sets the standards for secure transmission, clearance, and settlement of funds, ensuring that transactions are processed accurately and efficiently. With the growth of e-commerce and the increasing reliance on electronic payments, Nacha continues to evolve and adapt to meet the changing needs of the banking sector.

As a governing body, Nacha collaborates with financial institutions, businesses, and other stakeholders to develop and implement rules that govern ACH transactions. These rules promote transparency, security, and uniformity in electronic payment systems, fostering trust and confidence in the banking industry.

By adhering to Nacha’s rules and regulations, financial institutions and businesses can offer their customers a reliable and efficient means of electronic payment. Nacha’s standardized processes and guidelines ensure that transactions are processed accurately, minimizing errors and reducing the risk of fraudulent activity.

In addition to managing the ACH network, Nacha also provides education and training resources to help professionals in the banking industry stay updated on the latest trends and developments. These resources enable financial institutions to adapt to new technologies and regulatory changes more effectively, ensuring the continued success of electronic payments.

In summary, Nacha plays a vital role in the banking industry by overseeing the ACH network and establishing rules and standards for electronic payments. Its efforts ensure the secure and efficient movement of funds between financial institutions, promoting the growth and stability of the banking sector.

The Role of Nacha in the Banking Industry

Nacha, the National Automated Clearing House Association, holds a crucial role in the banking industry as it oversees the operation of the ACH (Automated Clearing House) network in the United States. This network facilitates the electronic transfer of funds between financial institutions, allowing for efficient and secure transactions. Nacha’s primary responsibility is to establish and enforce rules and regulations that govern the ACH network, ensuring its integrity and reliability.

One of the key roles of Nacha is to promote the widespread adoption and usage of electronic payments in the banking sector. By establishing a standardized framework for electronic transactions, Nacha enables financial institutions and businesses to adopt innovative payment solutions while maintaining security and efficiency. This encourages the transition from traditional paper-based payment methods to electronic alternatives, offering benefits such as faster processing times, lower costs, and enhanced convenience for consumers and businesses alike.

Nacha also plays a significant role in risk management within the banking industry. The organization continually monitors and evaluates the ACH network to identify potential risks and vulnerabilities, implementing measures to mitigate them. By establishing and enforcing regulations related to transaction security, fraud prevention, and data privacy, Nacha helps safeguard the financial system against unauthorized activity and fosters trust among participants in the banking industry.

Furthermore, Nacha encourages innovation and collaboration within the banking sector. The organization actively engages with financial institutions, payment processors, technology providers, and other stakeholders to promote dialogue, share best practices, and drive improvements in the electronic payment landscape. This collaboration serves to enhance the overall efficiency, accessibility, and interoperability of electronic payments, benefiting consumers and businesses nationwide.

Additionally, Nacha plays a critical role in educating and training professionals in the banking industry. The organization provides resources, workshops, and seminars to ensure that individuals involved in the processing of electronic payments stay informed about industry trends, regulatory changes, and best practices. This knowledge-sharing fosters expertise and professionalism within the sector, enhancing the quality and security of electronic payment transactions.

Overall, Nacha’s role in the banking industry is multifaceted. It sets and enforces standards, promotes the adoption of electronic payments, manages risk, encourages innovation, and provides education and training. These efforts contribute to the growth, stability, and efficiency of the banking sector while ensuring the secure and seamless movement of funds between financial institutions.

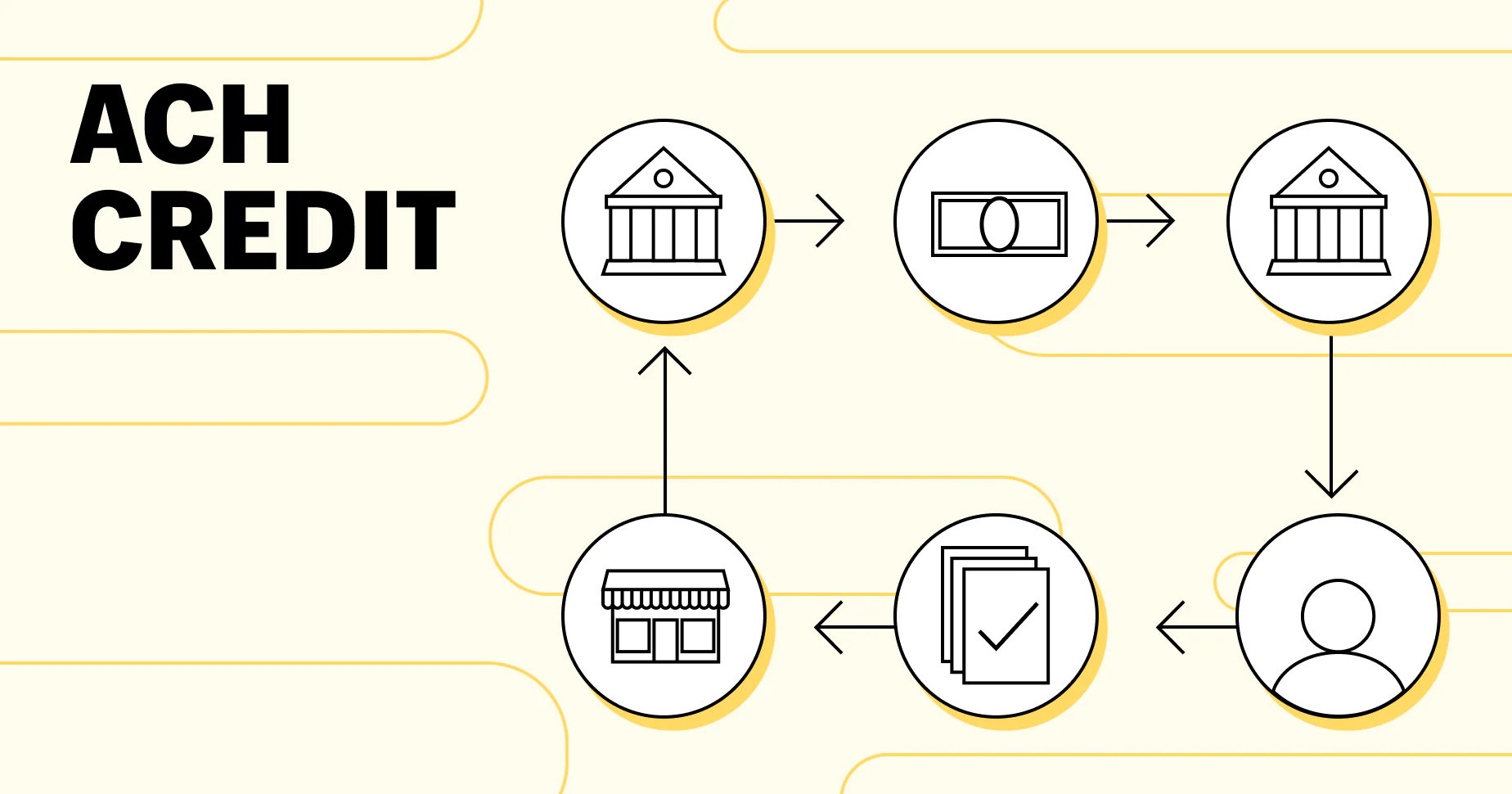

The ACH Network

The ACH (Automated Clearing House) network is a vital component of the banking industry in the United States, and Nacha plays a pivotal role in overseeing its operation. The ACH network provides a secure and efficient infrastructure for electronic funds transfer between financial institutions, enabling various types of electronic payments such as direct deposits, bill payments, and business-to-business transactions.

ACH transactions involve the electronic transfer of funds from one bank account to another, facilitated by the ACH network. This network acts as a central hub that connects participating financial institutions, allowing them to exchange payment instructions and settle transactions electronically. By utilizing the ACH network, financial institutions can process large volumes of transactions quickly and cost-effectively.

The ACH network operates on a batch-based processing system, where transactions are accumulated throughout the day and processed in batches at specific times. This batch processing allows financial institutions to consolidate multiple transactions into a single electronic file, reducing processing costs and increasing efficiency. Typically, ACH transactions are settled within one to two business days, providing timely funds exchange between parties involved.

One of the significant advantages of the ACH network is its widespread accessibility. Financial institutions of all sizes, from large national banks to community banks and credit unions, can participate in the ACH network, providing a level playing field for electronic payments. This inclusivity ensures that businesses and individuals across the country can enjoy the benefits of electronic transactions, regardless of their banking preferences.

The ACH network is a secure payment system, primarily due to the rigorous rules and regulations set by Nacha. These regulations govern the transmission, clearance, and settlement of funds, ensuring that transactions are processed accurately and securely. Nacha establishes guidelines and standards for participant identification, transaction formatting, and security measures, mitigating the risk of fraudulent activity and protecting the integrity of the ACH network.

Furthermore, the ACH network offers cost advantages compared to traditional payment methods, such as paper checks. Electronic transactions conducted through the ACH network are typically more affordable, with lower processing fees and reduced costs associated with printing, handling, and transporting physical checks. This cost-effectiveness makes electronic payments an attractive option for businesses, government agencies, and consumers, contributing to the widespread adoption of the ACH network.

In summary, the ACH network acts as a robust and secure infrastructure for electronic funds transfer, enabling various types of electronic payments. Nacha’s oversight ensures the integrity and efficiency of the ACH network, allowing financial institutions and businesses to process transactions quickly, securely, and cost-effectively. The ACH network’s accessibility, security, and cost advantages have made it an essential component of the banking industry, providing a reliable platform for electronic payments in the United States.

How Nacha Works

Nacha, the National Automated Clearing House Association, operates as the governing body overseeing the ACH (Automated Clearing House) network in the United States. Understanding how Nacha works is essential to comprehend the processes and mechanisms behind electronic funds transfer within the banking industry.

Nacha acts as a self-regulatory organization, responsible for creating and enforcing rules and guidelines that financial institutions and businesses must follow when participating in the ACH network. These rules ensure the smooth and secure movement of funds between banks, promoting efficiency, reliability, and consistency in electronic transactions.

Financial institutions and businesses that wish to participate in the ACH network must become Nacha members and adhere to its rules. Nacha membership provides access to the network, allowing participants to initiate and receive electronic payments. Nacha sets the standards for transaction formatting, participant identification, security protocols, and other critical aspects of ACH processing.

To facilitate the exchange of funds, Nacha acts as an intermediary between participating financial institutions. It receives transaction requests from originating banks and processes them by transmitting payment instructions to the appropriate receiving banks. By providing this centralized coordination, Nacha enables seamless communication and interoperability among financial institutions, ensuring the accurate and timely transfer of funds.

To ensure compliance with its rules and regulations, Nacha monitors and enforces adherence by conducting regular audits and assessments of member institutions. Any violations or non-compliance can result in penalties or sanctions. This commitment to enforcement helps maintain the integrity and security of the ACH network, protecting both financial institutions and consumers from fraudulent activity.

Nacha continuously works on improving and evolving the ACH network to meet the changing needs and advancements in the banking industry. The organization collaborates with various stakeholders, including financial institutions, businesses, and technology providers, to identify opportunities for innovation and make enhancements to the network. These efforts aim to maximize efficiency, security, and accessibility in electronic funds transfer, ensuring the continued effectiveness of the ACH network in the modern banking landscape.

Additionally, Nacha provides educational resources and training programs to support member institutions and professionals in staying up to date with the latest developments in ACH processing. These resources enable financial institutions to remain informed about regulatory changes, best practices, and emerging technologies, enhancing their ability to deliver secure and efficient electronic payment services to their customers.

In summary, Nacha operates as the regulatory body governing the ACH network. It sets and enforces rules and guidelines, facilitates communication among participating financial institutions, monitors compliance, and promotes continuous improvement in the electronic funds transfer process. By overseeing these essential functions, Nacha ensures the effective functioning of the ACH network, benefiting financial institutions, businesses, and consumers alike.

Nacha Rules and Regulations

Nacha, the National Automated Clearing House Association, establishes a comprehensive set of rules and regulations that govern the operation of the ACH (Automated Clearing House) network in the United States. These rules are critical to ensure secure, reliable, and consistent electronic funds transfer between participating financial institutions and businesses.

One of the primary objectives of Nacha’s rules and regulations is to maintain the integrity of the ACH network. This includes establishing guidelines for transaction formatting, participant identification, and data security. By ensuring that transactions are properly structured and authenticated, Nacha reduces the risk of fraud, errors, and misinformation, promoting confidence and trust in the electronic payment system.

Nacha rules also address the handling of unauthorized or fraudulent transactions. Financial institutions have specific obligations, known as the “Unauthorized Entry Fee,” to promptly investigate and resolve claims of unauthorized ACH transactions. These rules provide protection to both consumers and businesses by placing responsibility on financial institutions to handle fraudulent transactions appropriately.

Additionally, Nacha regulations govern the processing timelines for electronic transactions. For example, the organization specifies the timeframes for funds availability, such as the Standard Entry Class (SEC) codes for different types of transactions and their associated processing windows. These rules help ensure that payments are processed within reasonable timeframes, providing certainty and predictability for businesses and individuals.

Another crucial aspect of Nacha rules is compliance with privacy regulations. Nacha establishes requirements for protecting sensitive customer information during the transmission, processing, and storage of ACH data. This includes rules related to data encryption, secure transmission protocols, and the proper handling and disposal of customer information. Adherence to these rules helps maintain the confidentiality and privacy of customer data, safeguarding against unauthorized access and potential breaches.

Nacha also plays a vital role in promoting transparency and accountability in payment processing. The organization has established detailed guidelines for ACH transaction reporting and audit requirements. This ensures that financial institutions have the necessary mechanisms in place to monitor and report transaction details accurately. By providing a clear audit trail, Nacha rules enable financial institutions to maintain robust internal controls and facilitate effective oversight of ACH operations.

In instances where disputes arise regarding ACH transactions, Nacha provides a framework for resolving conflicts through its Rules Enforcement Process. This process allows parties involved to submit claims, present evidence, and engage in impartial dispute resolution. By providing this mechanism, Nacha helps maintain fairness and impartiality, ensuring all participants in the ACH network have a transparent means of resolving disputes.

In summary, Nacha’s rules and regulations are designed to promote the integrity, security, and efficiency of the ACH network. By establishing guidelines for transaction formatting, participant identification, privacy measures, and dispute resolution, Nacha ensures that electronic funds transfer is conducted in a standardized and secure manner. These rules provide a foundation for the reliable and consistent functioning of the ACH network, benefiting financial institutions, businesses, and consumers alike.

Benefits of Using Nacha in Banking

Nacha, the National Automated Clearing House Association, offers several key benefits to both financial institutions and businesses involved in the banking industry. By utilizing Nacha’s services and adhering to its rules and regulations, entities can enjoy enhanced efficiency, security, and convenience in their electronic payment processes.

One significant benefit of using Nacha in banking is the increased speed and efficiency of transactions. The ACH network overseen by Nacha allows for swift electronic funds transfer between financial institutions, reducing the time it takes for payments to be processed and settled. This speed enables businesses and consumers to have quicker access to funds, resulting in improved cash flow and greater flexibility in managing their finances.

Cost-effectiveness is another advantage of utilizing Nacha in banking. The ACH network offers lower processing fees compared to traditional payment methods, such as paper checks or wire transfers. By leveraging Nacha’s electronic payment infrastructure, financial institutions and businesses can significantly reduce transaction costs, resulting in savings and increased profitability.

Security is a top priority in the banking industry, and Nacha helps ensure the protection of electronic transactions. The organization sets strict rules and regulations regarding data encryption, secure transmission protocols, and participant identification, mitigating the risk of fraudulent activity. By adhering to Nacha’s security guidelines, financial institutions and businesses can maintain the confidentiality and integrity of customer information, fostering trust and confidence among their stakeholders.

Using Nacha in banking also offers convenience and accessibility to consumers and businesses alike. The ACH network allows for seamless and automated electronic payment processing, eliminating the need for paper-based checks or manual transaction handling. This streamlines the payment process, reduces administrative burdens, and simplifies financial transactions for individuals and organizations.

Furthermore, Nacha provides standardization and consistency in electronic payment processing. The organization establishes clear guidelines for transaction formatting, settlement windows, and participant identification, ensuring uniformity across different financial institutions. This standardization simplifies the reconciliation and reporting processes, making it easier for businesses to track and manage their payment activities.

In addition to these benefits, Nacha offers educational resources and training programs to assist financial institutions in staying up to date with industry trends, regulatory changes, and best practices in electronic payments. This knowledge-sharing helps enhance the skills and expertise of banking professionals, enabling them to provide better services and support to their customers.

Overall, utilizing Nacha in banking provides numerous advantages, including increased speed and efficiency, cost-effectiveness, enhanced security, convenience, and standardization. By leveraging the services and guidelines provided by Nacha, financial institutions and businesses can optimize their electronic payment processes, providing better experiences to their customers while benefiting from improved operational efficiency.

Nacha Operating Rules and Guidelines

Nacha, the National Automated Clearing House Association, has established comprehensive operating rules and guidelines that financial institutions and businesses must adhere to when participating in the ACH (Automated Clearing House) network. These rules provide a framework for secure, efficient, and standardized electronic funds transfer.

The Nacha Operating Rules govern various aspects of ACH transactions, including transaction formatting, participant identification, security measures, dispute resolution, and compliance requirements. These rules ensure consistency and uniformity across the ACH network, promoting transparency and confidence in electronic payment processing.

One key element of the Nacha Operating Rules is transaction formatting guidelines. These rules specify the required data elements and formats for different types of ACH transactions, ensuring that payment instructions are accurately communicated between financial institutions. By standardizing the structure and content of ACH transactions, Nacha facilitates seamless interoperability and reduces the potential for errors or misinterpretation.

Participant identification is another crucial aspect of the Nacha Operating Rules. Financial institutions and businesses must follow prescribed procedures to accurately identify and validate the identities of parties involved in ACH transactions. These identification requirements help strengthen the security and integrity of the ACH network, mitigating the risk of unauthorized or fraudulent activity.

Nacha’s rules also dictate the security measures that participants must employ to protect sensitive information during ACH transactions. This includes requirements for data encryption, secure transmission protocols, and authentication mechanisms. By implementing these security measures, financial institutions and businesses can safeguard customer data and minimize the risk of data breaches or unauthorized access.

Dispute resolution procedures are another critical component of the Nacha Operating Rules. In the event of transaction disputes or errors, the rules outline a clear process for parties to submit claims, present evidence, and engage in dispute resolution. This mechanism ensures fair and impartial resolution of conflicts, helping to maintain trust and credibility within the ACH network.

Compliance with regulatory requirements is also addressed in the Nacha Operating Rules. Financial institutions and businesses must adhere to applicable laws and regulations, such as the Bank Secrecy Act (BSA), anti-money laundering (AML) regulations, and data privacy laws. Nacha provides guidelines and recommendations to help ensure that ACH transactions comply with these regulations, fostering compliance and minimizing the risk of regulatory violations.

As technology and industry practices evolve, Nacha regularly updates its operating rules and guidelines to address emerging trends and developments. These updates reflect the dynamic nature of the banking industry and help financial institutions and businesses stay current with the evolving requirements of electronic payment processing.

In summary, the Nacha Operating Rules and Guidelines provide a comprehensive framework for secure, efficient, and standardized electronic funds transfer through the ACH network. By adhering to these rules, financial institutions and businesses can ensure that their ACH transactions are compliant, secure, and conducted in a consistent manner. Nacha’s ongoing efforts to update and refine these rules reflect its commitment to the continuous improvement of electronic payment processes within the banking industry.

The Future of Nacha in Banking

Nacha, the National Automated Clearing House Association, is poised to play an increasingly significant role in the future of banking. As the banking industry continues to evolve and technology advances, Nacha is at the forefront of shaping the future of electronic payment processing.

One area where Nacha will continue to focus its efforts is in promoting faster payment options. The organization is actively working on initiatives to enhance the speed of ACH transactions, allowing for near real-time settlement. These faster payment capabilities will provide businesses and consumers with enhanced convenience and quicker access to funds, enabling greater financial flexibility in an increasingly fast-paced digital economy.

Moreover, Nacha recognizes the importance of ensuring security and combating fraud in electronic transactions. As techniques and threats evolve, Nacha will continue to develop and implement advanced security measures to protect sensitive financial data and prevent unauthorized access. This includes exploring emerging technologies such as biometric authentication, artificial intelligence, and machine learning to enhance the security of the ACH network.

In line with technological advancements, Nacha is also actively exploring the use of new payment channels. This includes embracing innovations such as mobile payments, peer-to-peer transfers, and cryptocurrency transactions. By embracing these emerging payment methods, Nacha can stay relevant in the ever-changing landscape of digital banking and offer secure and efficient solutions to meet the evolving needs of consumers and businesses.

Another aspect of Nacha’s future lies in expanding its global reach. The organization is working towards greater interoperability with international payment systems, fostering collaborations and partnerships with global counterparts. By promoting international standards and harmonizing rules and protocols, Nacha aims to facilitate more streamlined and secure cross-border transaction processes, promoting trade and economic growth.

Furthermore, Nacha is committed to fostering innovation and collaboration within the banking industry. The organization actively engages with financial institutions, businesses, and technology providers to identify emerging trends, share best practices, and promote dialogue. This collaboration leads to the development of new technologies, services, and business models that drive further advancements in electronic payment processing.

As part of its future goals, Nacha will continue to prioritize education and training for banking professionals. By providing resources, workshops, and seminars, Nacha equips industry professionals with the knowledge and skills necessary to navigate the ever-changing landscape of electronic payment processing. This empowers financial institutions to deliver secure, efficient, and innovative payment solutions to their customers.

In summary, the future of Nacha in banking will involve a continued focus on faster payments, enhanced security measures, adoption of emerging payment channels, global interoperability, and fostering collaboration and innovation. By staying at the forefront of technological advancements, Nacha is well-positioned to shape the future of electronic payment processing and drive positive change within the banking industry.

Conclusion

Nacha, the National Automated Clearing House Association, plays a crucial role in the banking industry as it oversees the operation of the ACH (Automated Clearing House) network in the United States. By establishing rules, guidelines, and standards for electronic payment processing, Nacha ensures the secure, efficient, and standardized movement of funds between financial institutions and businesses.

Throughout this article, we have explored the various functions and benefits of Nacha in banking. From its role in overseeing the ACH network to the establishment of rules and regulations, Nacha provides a reliable infrastructure for electronic funds transfer. Its efforts promote trust, transparency, and accountability within the banking industry.

Nacha enables financial institutions and businesses to adopt innovative payment solutions while maintaining security and efficiency. By adhering to Nacha’s rules, participants in the ACH network can process transactions quickly, accurately, and cost-effectively. This promotes economic growth and stability while delivering enhanced convenience to consumers and businesses.

The future of Nacha in banking holds exciting opportunities for further advancements in electronic payment processing. From faster payment options and enhanced security measures to embracing emerging technologies and expanding global interoperability, Nacha is poised to shape the future of banking and meet the evolving needs of the digital economy.

In conclusion, Nacha’s role in the banking industry is vital for the smooth operation of electronic payments. It provides a trusted framework for secure and efficient funds transfer, ensures compliance with regulations, and fosters innovation and collaboration. By leveraging Nacha’s services and adhering to its rules, financial institutions and businesses can optimize their payment processes, deliver better experiences to their customers, and contribute to the continued growth and innovation of the banking industry.