Introduction

Welcome to the world of banking and finance, where acronyms and abbreviations are aplenty. If you have ever come across the term “ACH” in the context of banking, you may have wondered what it stands for and what it entails. Well, fear not, as we are here to demystify this acronym for you.

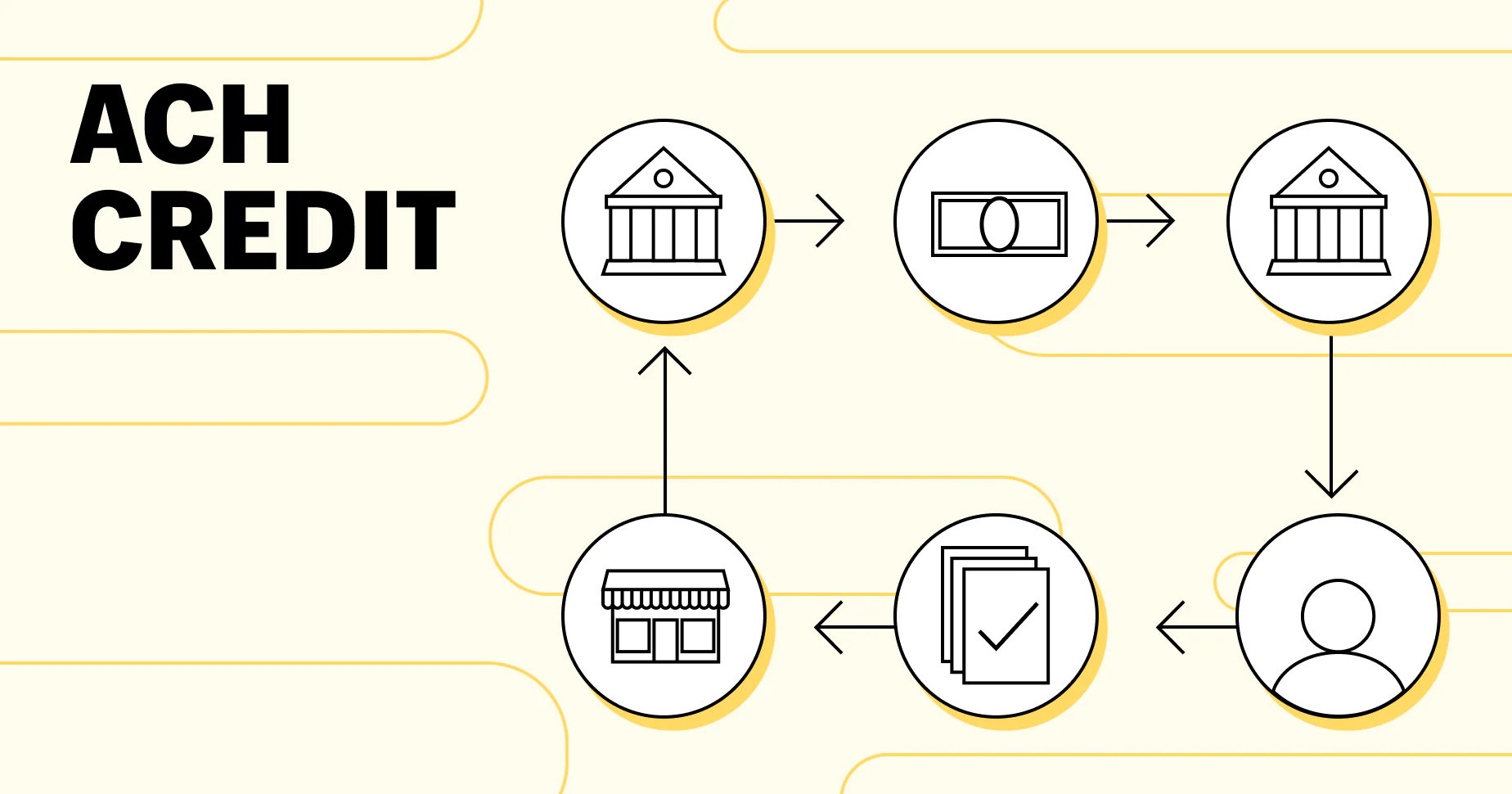

ACH stands for “Automated Clearing House,” and it is an electronic payment system used for the secure and efficient transfer of funds between different financial institutions. It serves as a backbone for various types of payment transactions, including direct deposits, bill payments, and business-to-business payments.

The ACH system enables the movement of funds from one bank account to another through an automated, batch processing system. It has become an integral part of the banking industry, revolutionizing the way payments are made and received.

In this article, we will delve deeper into what ACH stands for, how it works, and its benefits in the banking sector. We will also explore the key differences between ACH and other payment methods, as well as common use cases for ACH in daily banking transactions. Additionally, we will touch upon the security measures implemented to safeguard ACH transactions.

By the end of this article, you will have a comprehensive understanding of ACH and its significance in the world of banking. So, let’s begin our journey into the realm of ACH and explore the various facets of this essential payment system.

What does ACH stand for?

ACH stands for “Automated Clearing House.” It is an electronic payment system that allows for the secure and efficient transfer of funds between different banks and financial institutions. Instead of using paper checks or physical cash, ACH facilitates electronic transactions, making it quicker and more convenient for both businesses and individuals.

The ACH system operates as a batch processing system, which means that transactions are grouped together and processed in batches at specific times throughout the day. This automated process streamlines the movement of funds, reducing the time and effort required for manual processing.

ACH transactions typically involve the transfer of funds from one bank account to another, either for direct deposit purposes, bill payments, or business-to-business transactions. By utilizing the ACH network, businesses can effortlessly collect payments from their customers, and individuals can conveniently pay bills or make recurring payments.

The ACH system is governed by rules and regulations set forth by the National Automated Clearing House Association (NACHA), an organization that ensures the smooth operation and security of ACH transactions. These rules establish guidelines for creating, transmitting, and receiving ACH files, as well as securing the data and protecting the privacy of individuals involved.

Overall, ACH serves as the backbone of electronic payments in the banking industry, enabling seamless and secure transfer of funds between financial institutions. It has become an essential component of modern banking, replacing outdated paper-based payment methods and revolutionizing the way we handle financial transactions.

How does ACH work?

The Automated Clearing House (ACH) is a sophisticated, electronic payment system that facilitates the seamless transfer of funds between different banks and financial institutions. Let’s take a closer look at how ACH works:

1. Initiation: The ACH process begins when an entity, such as an employer or a business, initiates a payment or a collection request. This can be done through various channels, such as online banking platforms, financial software, or dedicated ACH service providers.

2. Data Entry: The initiator provides the necessary payment information, such as the recipient’s bank account number, routing number, and the payment amount. Additionally, any essential details related to the payment, such as invoice numbers or customer IDs, can be included in the transaction.

3. File Creation: The initiator compiles the payment requests into a standardized file format specified by NACHA. This file contains multiple entries, each representing an individual payment transaction. It also includes relevant details, like the originator’s identification and the payment’s purpose.

4. Transmission: Once the file is created, it is transmitted securely to an ACH operator. The ACH operator acts as an intermediary, facilitating the exchange of ACH files between financial institutions. This transmission can occur through dedicated secure networks or directly through the internet, depending on the participating parties’ infrastructure.

5. Batch Processing: The ACH operator receives the file and processes it in batches. The operator validates the entries, ensuring that the necessary data is present and accurate. It also performs security checks to mitigate the risk of fraudulent transactions.

6. Clearing and Settlement: The processed batches are then sent to the respective financial institutions involved in the transactions. The clearing process involves matching the payments with the recipients’ accounts and verifying the availability of funds.

7. Funds Transfer: Once the transactions are successfully cleared, the ACH system initiates the transfer of funds between the participating banks. The transfer takes place electronically, and the funds are typically made available within a specified time frame, depending on the recipient’s bank’s policies.

8. Confirmation and Reconciliation: Finally, the ACH system provides confirmation messages to the participating banks, notifying them of the completed transactions. The banks can reconcile these messages with their own records to ensure accuracy and mitigate any discrepancies.

This is a simplified overview of the ACH process. It is important to note that the actual implementation can vary between different financial institutions and systems. However, the underlying principles and workflow remain consistent, enabling the efficient and secure movement of funds using the ACH system.

Benefits of using ACH in banking

The adoption of the Automated Clearing House (ACH) system in the banking industry has brought about numerous benefits for both businesses and individuals. Let’s explore the advantages of using ACH for financial transactions:

1. Speed and Efficiency: ACH transactions are processed electronically, which significantly reduces the time compared to traditional paper-based methods. With ACH, payments can be initiated and processed quickly, resulting in faster fund transfers and quicker payment settlements.

2. Cost Savings: ACH transactions are generally more cost-effective than traditional payment methods. By eliminating the need for paper checks, envelopes, postage, and manual processing, businesses can save on printing and mailing expenses. Additionally, individuals can avoid fee charges associated with other payment alternatives, such as wire transfers.

3. Convenience: ACH offers convenience for both businesses and customers. Businesses can collect recurring payments electronically, such as monthly subscriptions or installment plans, without the hassle of manual invoicing and follow-up. On the other hand, individuals can conveniently pay bills online, set up automatic payments, and avoid the need for writing and mailing checks.

4. Security and Reliability: ACH transactions employ robust security measures to protect sensitive financial information. Encryption and authentication protocols ensure the safe transmission of data, reducing the risk of fraud or unauthorized access. Additionally, ACH payments are reliable, with a high success rate and low occurrence of errors compared to manual processing.

5. Enhanced Cash Flow Management: The predictability and consistency of ACH transactions allow businesses to better manage their cash flow. With scheduled payments and direct deposit capabilities, organizations can accurately forecast their revenue and expenses, reducing the uncertainties associated with manual payment processes.

6. Streamlined Operations: ACH integrates seamlessly with other automated financial systems, such as accounting software or enterprise resource planning (ERP) systems. This integration eliminates the need for manual data entry and reconciliation, reducing administrative efforts and improving overall operational efficiency.

7. Environmental Sustainability: By transitioning from paper-based payment methods to electronic transactions, ACH contributes to environmental sustainability. Reduced paper usage, lower carbon emissions from transportation, and minimized waste from the printing and disposal of checks all contribute to a greener and more eco-friendly banking industry.

These are just a few of the key benefits of utilizing the ACH system in banking. As technology continues to evolve, the advantages of ACH are likely to expand, making it an increasingly integral part of modern financial transactions.

ACH vs. other payment methods

When it comes to making financial transactions, there are various payment methods available, each with its own strengths and limitations. Let’s compare the Automated Clearing House (ACH) system with other commonly used payment methods:

1. ACH vs. Checks: ACH offers several advantages over traditional paper checks. While checks require manual preparation, printing, and mailing, ACH transactions are completed electronically, saving time and reducing costs. ACH is also more secure, as physical checks can be lost, stolen, or altered. Additionally, ACH offers faster processing and settlement times compared to the clearing period required for checks to be fully processed.

2. ACH vs. Wire Transfers: Wire transfers allow for immediate funds transfer between financial institutions, making them suitable for urgent and high-value transactions. However, wire transfers are generally more expensive and involve higher transaction fees compared to ACH. ACH offers a more cost-effective option for non-time-sensitive transfers, providing businesses and individuals with a cost-efficient alternative.

3. ACH vs. Credit/Debit Cards: Credit and debit cards provide convenience and widespread acceptance, making them popular payment methods. However, they typically involve transaction fees for merchants and may also incur fees for customers. ACH transactions, on the other hand, have lower costs, making them an attractive option for businesses that process large volumes of payments or recurring transactions.

4. ACH vs. Cash: Cash transactions are immediate and do not require any electronic processing. However, handling and storing physical cash can be cumbersome and present security risks. ACH offers a secure and convenient alternative, eliminating the need for physical cash while providing an electronic trail of the transaction.

5. ACH vs. Mobile Payment Apps: Mobile payment apps, such as Apple Pay or PayPal, have gained popularity for their ease of use and quick transactions. These apps often rely on credit or debit cards linked to the user’s account. ACH, on the other hand, offers a direct transfer of funds between bank accounts, bypassing the need for intermediaries or transaction fees associated with such apps.

Each payment method has its own set of advantages and considerations, depending on the specific requirements of businesses and individuals. ACH strikes a balance between cost-effectiveness, security, and convenience, making it a versatile option for a wide range of financial transactions.

Common uses of ACH in banking

The Automated Clearing House (ACH) system has revolutionized the way financial transactions are conducted, offering a wide range of applications in the banking industry. Let’s explore some of the common uses of ACH:

1. Direct Deposits: ACH is commonly utilized for direct deposit transactions, enabling the seamless transfer of funds from an employer’s account to an employee’s bank account. This convenient method eliminates the need for paper checks, expediting payroll processes and providing employees with quick access to their earnings.

2. Bill Payments: ACH is widely used for online bill payments, allowing individuals to pay their regular expenses, such as utility bills, mortgage payments, or credit card bills. By setting up automatic payments, customers can ensure timely payments without the need for manual intervention.

3. E-commerce Transactions: ACH is increasingly being integrated into e-commerce platforms to facilitate secure and efficient online transactions. Businesses can offer customers the option to make payments directly from their bank accounts, reducing the reliance on credit cards or other payment intermediaries.

4. Business-to-Business (B2B) Payments: ACH is an ideal solution for business-to-business payments, enabling organizations to easily transfer funds to suppliers, vendors, or other business partners. This method streamlines payment processes, reduces reliance on paper checks, and enhances cash flow management for both parties.

5. Monthly Subscriptions: With the rise of subscription-based services, ACH provides a convenient and recurring payment method. Customers can set up automatic payments, ensuring they never miss a subscription payment while avoiding the need for manual invoice processing or credit card updates.

6. Healthcare Payments: ACH is widely used in the healthcare industry for insurance claim reimbursements, medical bill payments, and premium collections. This offers an efficient and secure method for healthcare providers, insurers, and patients to handle financial transactions.

7. Government Payments: ACH serves as a trusted channel for various government transactions, such as tax refunds, social security benefits, or pension payments. By utilizing ACH, government agencies can reliably disburse funds to beneficiaries, reducing administrative costs and enhancing financial transparency.

8. Non-Profit Donations: ACH is increasingly utilized by non-profit organizations to collect donations efficiently. Instead of relying solely on checks or credit card payments, donors can contribute directly from their bank accounts, making it a user-friendly and cost-effective option for charitable giving.

These are just a few examples of the diverse applications of ACH in the banking sector. The versatility and convenience of ACH make it an essential payment system for individuals, businesses, and other organizations, simplifying financial transactions and enhancing operational efficiency.

Security measures in ACH transactions

With the increasing reliance on electronic transactions, ensuring the security and integrity of financial transactions is paramount. The Automated Clearing House (ACH) system incorporates various security measures to protect sensitive data and mitigate the risk of fraudulent activities. Let’s explore some of the security measures implemented in ACH transactions:

1. Secure Transmission: ACH transactions take place over secure networks or encrypted channels, protecting the data during transmission. Encryption algorithms, such as Secure Sockets Layer (SSL) or Transport Layer Security (TLS), are used to encrypt the information, ensuring that it remains confidential and protected from unauthorized access.

2. Authentication: ACH transactions employ robust authentication mechanisms to verify the identities of the participating entities. Authorized users are required to provide unique login credentials, such as usernames and passwords, before they can access and initiate transactions within the ACH system. In some cases, additional layers of authentication, such as multi-factor authentication, may be implemented for added security.

3. Role-Based Permissions: ACH systems implement role-based access controls, granting different levels of access and permissions based on the user’s role and responsibilities. This ensures that users can only perform actions that are relevant to their roles, reducing the risk of unauthorized transactions or data breaches.

4. Secure File Formats: The ACH system employs specific file formats to ensure the integrity of the data being transmitted. These formats include built-in error detection and verification mechanisms to flag any inconsistencies or tampering attempts. This helps protect against unauthorized modifications to the transaction data during transmission or processing.

5. Auditing and Monitoring: ACH transactions undergo extensive auditing and monitoring to detect any suspicious or fraudulent activities. Banks and financial institutions have internal controls in place to monitor transaction patterns and identify potential anomalies or unauthorized access. Regular audits are conducted to assess the effectiveness of the security measures and identify any vulnerabilities that need to be addressed.

6. Fraud Detection and Prevention: ACH systems employ advanced algorithms and fraud detection mechanisms to identify and prevent fraudulent transactions. These systems analyze transaction patterns, monitor for unusual activity, and flag suspicious transactions for further investigation. In case of any detected fraudulent activities, appropriate actions can be taken to mitigate the impact and protect the affected parties.

7. Compliance with Regulations: ACH transactions must adhere to strict regulatory guidelines and industry standards, such as those set forth by the National Automated Clearing House Association (NACHA). Compliance with these standards ensures that the necessary security measures are in place and that customer data is protected according to established protocols.

These security measures work collectively to protect ACH transactions and maintain the confidentiality, integrity, and availability of the data involved. By implementing these safeguards, the ACH system strives to provide a secure and reliable platform for financial transactions, fostering trust and confidence among users.

Conclusion

The Automated Clearing House (ACH) system has revolutionized the way financial transactions are conducted in the banking industry. Its electronic payment capabilities have brought about numerous benefits, including convenience, cost savings, and increased efficiency.

ACH facilitates secure fund transfers between different financial institutions, eliminating the need for paper checks and manual processes. It enables direct deposits, bill payments, business-to-business transactions, and more. The ACH system operates with speed, efficiency, and reliability, streamlining financial transactions for businesses and individuals alike.

Compared to other payment methods, ACH offers distinct advantages. It is cost-effective, environmentally friendly, and provides enhanced security measures to protect sensitive financial information. ACH transactions are seamless, allowing for efficient management of cash flow and convenient handling of recurring payments.

Additionally, ACH addresses the diverse needs of industries such as healthcare, government, and non-profit organizations, providing a secure and efficient platform for their unique payment requirements.

Security is a top priority in ACH transactions. Robust measures such as secure transmission channels, authentication protocols, role-based permissions, and fraud detection mechanisms help safeguard the integrity of data and mitigate the risk of fraudulent activities.

In conclusion, ACH has become an integral part of the banking industry, offering a reliable, secure, and efficient method for electronic transactions. Its widespread adoption has transformed the way businesses and individuals handle their financial transactions, promoting convenience, cost savings, and operational efficiency.

With continuous advancements in technology and ongoing efforts to enhance security measures, ACH will continue to play a crucial role in the ever-evolving landscape of banking and finance.