Introduction

Welcome to the world of banking, where numerous acronyms and terms are used to describe various financial transactions. One such term you may have come across is ACH. If you’ve ever wondered what ACH means in banking, you’re in the right place.

ACH stands for Automated Clearing House, which is an electronic network used for processing financial transactions in the United States. It allows individuals, businesses, and financial institutions to transfer funds securely and efficiently.

In this article, we will delve into the world of ACH and explore its inner workings, benefits, and common uses. Whether you are an avid online shopper, a business owner, or simply curious about the financial system, understanding ACH is essential.

Throughout the article, we will compare ACH transactions to other methods of transferring funds, highlight its presence in online banking, and discuss the processing time, risks, and security associated with ACH transactions. By the end, you will have a comprehensive understanding of ACH and how it impacts the world of banking.

So, let’s dive right in and demystify the concept of ACH in banking!

What is ACH?

ACH, which stands for Automated Clearing House, is an electronic payment network that facilitates the transfer of funds between different bank accounts. It serves as a central system for processing a wide range of transactions, including direct deposits, bill payments, business-to-business transactions, and person-to-person transfers.

The ACH network operates under the oversight of the National Automated Clearing House Association (NACHA), which establishes rules and regulations governing the movement of funds. NACHA ensures that all transactions carried out through ACH comply with industry standards and meet the required security protocols.

Unlike traditional methods of fund transfer, such as writing and depositing physical checks, ACH enables the quick and secure movement of funds electronically. By leveraging the power of technology, ACH eliminates the need for paper checks and physical cash, making transactions faster, more reliable, and more efficient.

When an ACH transaction is initiated, the funds are electronically debited from the sender’s account and then credited to the recipient’s account. This process typically takes one to two business days, depending on the timing and the participating financial institutions.

It’s important to note that ACH transactions can be initiated by individuals, businesses, or financial institutions. Whether you’re receiving your recurring paycheck through direct deposit, setting up automatic bill payments, or transferring funds between different accounts, ACH facilitates these transactions seamlessly.

Overall, ACH provides a cost-effective and convenient alternative to traditional payment methods. It provides a secure and efficient way to transfer funds electronically, making it a popular choice for individuals and businesses alike.

How Does ACH Work?

Understanding how ACH works is key to grasping the inner workings of this electronic payment network. The process begins with the initiator, who can be an individual or a business, authorizing an ACH transaction.

First, the initiator provides their bank account information, such as the account number and routing number, along with the recipient’s account details. This information is crucial for the ACH process to identify the relevant accounts and facilitate the transfer of funds.

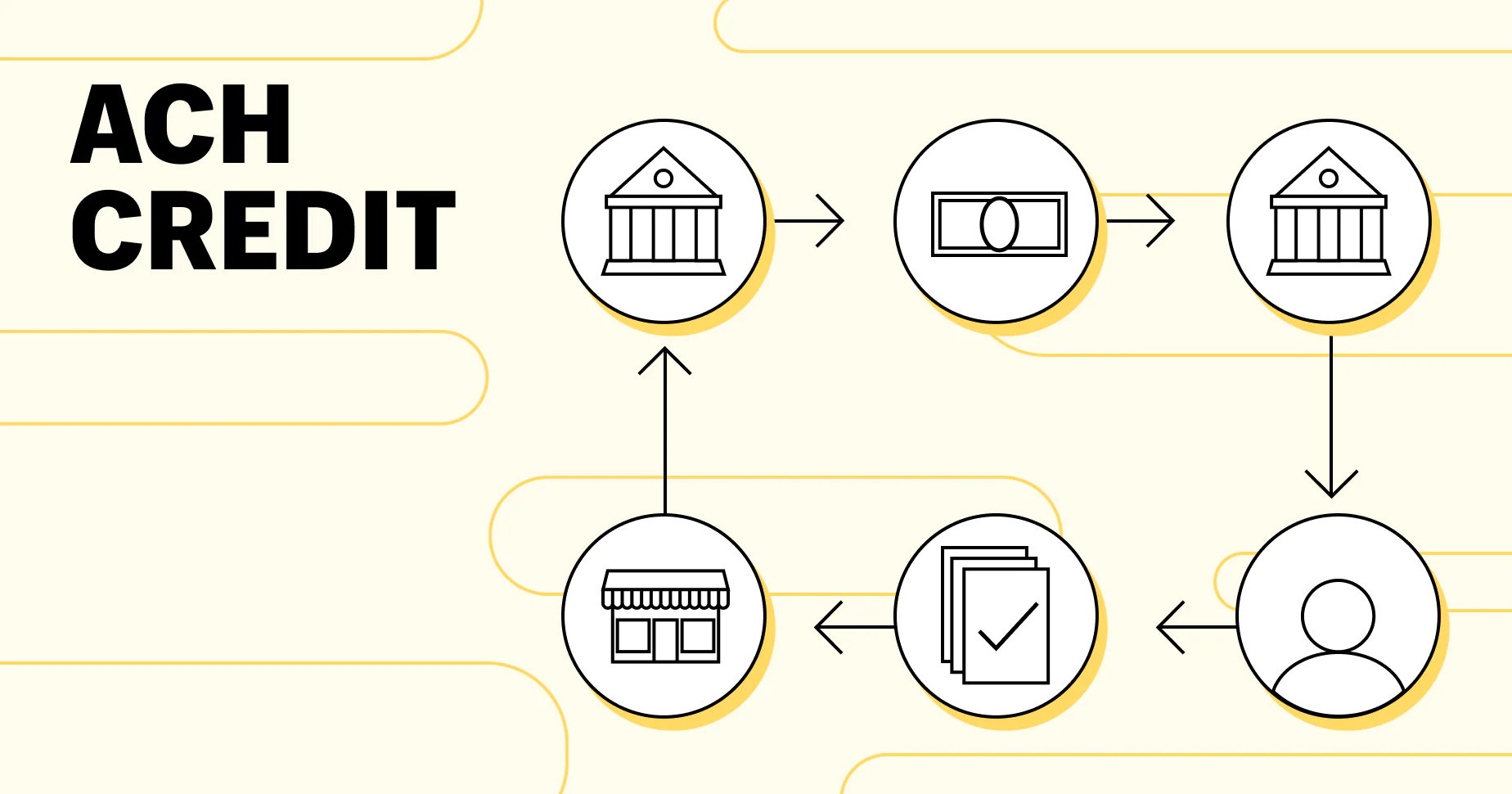

Next, the initiator’s bank, also known as the Originating Depository Financial Institution (ODFI), initiates the ACH transaction. The ODFI collects the transaction details and sends them to the ACH operator, which can be a Federal Reserve Bank or a private ACH operator. The ACH operator acts as a central clearinghouse, facilitating the transfer of funds between the ODFI and the recipient’s bank, known as the Receiving Depository Financial Institution (RFDI).

Once the transaction information reaches the RDFI, the funds are credited to the recipient’s account. This process typically occurs within one to two business days, depending on various factors, including the time of initiation and the processing time of the participating financial institutions.

It’s important to note that ACH transactions can be one-time or recurring. For example, if you set up automatic bill payments with your utility company, they may initiate a recurring ACH transaction to debit the funds from your account on a specified date each month. Similarly, if you receive your salary through direct deposit, your employer may initiate a recurring ACH transaction to credit your account on payday.

Security is of utmost importance in ACH transactions. The ACH network incorporates various security measures, including encryption and authentication protocols, to ensure the safety and confidentiality of transaction data. Additionally, NACHA establishes rules and guidelines that financial institutions and participants must adhere to, further enhancing the security of ACH transactions.

Overall, ACH simplifies the process of transferring funds electronically, offering a secure and streamlined solution for individuals and businesses. By leveraging the power of technology and a well-regulated network, ACH provides a reliable and efficient method for moving money between bank accounts.

Benefits of ACH

The use of ACH for financial transactions offers numerous benefits to both individuals and businesses. Let’s explore some of the key advantages of utilizing the ACH network:

1. Speed and Efficiency: ACH transactions are typically faster and more efficient than traditional paper-based methods. With ACH, funds can be transferred electronically between accounts within one to two business days, eliminating the need for physical checks and manual processing.

2. Cost Savings: ACH transactions are generally more cost-effective compared to alternatives like wire transfers or issuing checks. ACH transactions often have lower processing fees, making them a preferred choice for businesses and individuals looking to save on transaction costs.

3. Automation and Convenience: ACH allows for automated recurring payments, such as monthly utility bills or loan repayments. This automation helps individuals and businesses manage their finances more efficiently, ensuring timely payments without the need for manual intervention.

4. Security and Accuracy: ACH transactions comply with robust security measures and undergo multiple layers of validation during processing. This enhances the accuracy and reliability of the transactions, reducing the risk of errors or fraudulent activities.

5. Environmental Sustainability: ACH transactions significantly reduce paper consumption by replacing traditional check-based payments. By opting for electronic fund transfers instead of printed checks, individuals and businesses contribute to environmental sustainability by reducing their carbon footprint.

6. Accessibility: ACH transactions are widely accessible, allowing individuals and businesses to carry out financial transactions regardless of their physical location. This accessibility facilitates seamless online banking, enabling people to manage their finances from the comfort of their homes or offices.

7. Streamlined Cash Flow: For businesses, ACH helps optimize cash flow by expediting receivables and payables processing. The timely receipt of payments and efficient management of outgoing payments can help improve liquidity and financial stability.

These benefits make ACH an attractive choice for various financial transactions, from direct deposit of salaries and benefits to bill payments and vendor payments. Whether you’re an individual or a business, leveraging the ACH network can bring efficiency, cost savings, and convenience to your financial operations.

ACH Transactions vs. Wire Transfers

When it comes to transferring funds between bank accounts, two common methods are ACH transactions and wire transfers. While both serve the purpose of moving money, there are significant differences between the two. Let’s compare ACH transactions to wire transfers to understand these distinctions:

1. Speed and Timing: A key difference between ACH transactions and wire transfers lies in their speed and timing. ACH transactions typically take one to two business days for funds to be transferred, while wire transfers are almost instantaneous. Wire transfers offer faster availability of funds, making them suitable for urgent and time-sensitive payments.

2. Cost: Another significant difference is the cost associated with each method. ACH transactions are generally more affordable, with low or no fees for individuals and businesses. On the other hand, wire transfers often involve higher fees, especially for international transfers or expedited processing.

3. Transfer Limits: ACH transactions typically have higher transfer limits compared to wire transfers. ACH allows for larger transaction amounts, making it more suitable for businesses or individuals transferring significant sums of money.

4. Accessibility: ACH transactions are widely accessible and can be initiated through online banking platforms or authorized payment processors. Wire transfers, on the other hand, often require visiting a bank branch or contacting a bank representative to execute the transfer, making them slightly less accessible for individuals without direct access to a bank.

5. Use Cases: ACH is commonly used for various types of payments, including direct deposits, bill payments, and business-to-business transactions. Wire transfers are often preferred for large international transactions or when immediate availability of funds is crucial, such as purchasing real estate or making time-sensitive business payments.

6. Security: Both ACH transactions and wire transfers prioritize security. However, wire transfers are generally considered more secure due to their closed-loop nature and strict verification processes. ACH transactions, while secure, may have a slightly higher risk of unauthorized transactions due to the nature of the open ACH network.

Understanding these differences between ACH transactions and wire transfers allows individuals and businesses to select the most appropriate method based on their specific needs. Whether you prioritize speed, cost, transfer limits, or accessibility, both ACH transactions and wire transfers offer distinct advantages for transferring funds between bank accounts.

ACH vs. EFT

When it comes to electronic fund transfers, two commonly used terms are ACH and EFT. While they both involve the transfer of funds electronically, there are important distinctions to understand. Let’s compare ACH to EFT to clarify these differences:

1. Definition: ACH, as previously mentioned, stands for Automated Clearing House and refers to a specific electronic payment network that facilitates fund transfers between different bank accounts. On the other hand, EFT, or Electronic Funds Transfer, is a broader term that encompasses various electronic methods of transferring funds, including ACH.

2. Scope: ACH is a subset of EFT. EFT includes other electronic payment methods, such as wire transfers, debit card transactions, and digital wallet payments. ACH specifically refers to transactions processed through the ACH network, while EFT covers a wider range of electronic transactions.

3. Processing Time: ACH transactions typically take one to two business days for funds to be transferred between accounts, as they operate on a batch processing system. Conversely, other forms of EFT, such as wire transfers or debit card transactions, can often provide more immediate availability of funds, sometimes in real-time or near real-time.

4. Authorization: In ACH transactions, the sender typically provides authorization for the transfer to occur. This can be initiated by individuals, businesses, or financial institutions. In contrast, EFT can include transactions that are initiated automatically, such as recurring bill payments or direct deposit of salaries. EFT transactions can also be initiated manually, similar to ACH transactions.

5. Use Cases: ACH transactions are commonly used for a variety of purposes, such as direct deposits, bill payments, and business-to-business transactions. EFT encompasses a broader range of transactions, including ACH, wire transfers, card-based payments, and more. Therefore, EFT can be applied to various scenarios, including card-based purchases, electronic benefit payments, and online payment gateways.

6. Security Measures: Both ACH and EFT transactions prioritize security. They incorporate encryption protocols, authentication measures, and compliance with industry standards. NACHA establishes rules and guidelines for ACH transactions, while EFT transactions are subject to specific regulations based on the payment method employed.

Understanding the distinction between ACH and EFT allows individuals and businesses to navigate the world of electronic fund transfers more effectively. While ACH provides a specific framework for transferring funds through the ACH network, EFT encompasses a broader spectrum of electronic transactions, including ACH, wire transfers, and card-based payments.

ACH in Online Banking

As technology continues to advance, online banking has become increasingly popular for managing finances. ACH plays a significant role in the realm of online banking, facilitating seamless fund transfers and providing convenience to users. Let’s explore how ACH is integrated into online banking platforms:

1. Account Linking: Online banking platforms allow users to link their bank accounts to the platform, enabling easy access and management of multiple accounts in one place. By linking their accounts, users can initiate ACH transactions directly from their online banking interface.

2. Bill Payments: ACH is commonly used for online bill payments. Online banking platforms provide features that allow users to schedule recurring or one-time payments to pay bills electronically. These payments are processed using the ACH network, allowing for efficient and secure transactions.

3. Direct Deposits and Transfers: Online banking enables users to set up direct deposit of salaries, benefits, or other regular income. By providing their account details and authorizing ACH transactions, users can receive funds directly into their bank accounts without the need for physical checks.

4. Internal Transfers: ACH is utilized within online banking platforms to facilitate internal transfers between a user’s linked accounts. Users can easily transfer funds between their checking accounts, savings accounts, or other accounts held within the same financial institution, making it convenient to manage liquidity and allocate funds as needed.

5. Mobile Banking: With the rise of smartphones and mobile banking apps, users can now initiate ACH transactions directly from their mobile devices. Mobile banking apps often offer capabilities such as mobile check deposit, bill payments, and fund transfers, all powered by the ACH network.

6. Payment Platforms: Online banking platforms may integrate with payment platforms, such as PayPal or Venmo, which operate on the ACH network. By linking their online banking accounts to these payment platforms, users can easily transfer funds between accounts and make online purchases.

ACH integration in online banking platforms brings convenience, control, and accessibility to users’ financial management. By leveraging the capabilities of ACH, users can initiate various transactions, such as bill payments, direct deposits, and internal transfers, all from the comfort of their online banking interface or mobile banking app.

It’s important to note that different financial institutions may offer varying features and functionalities within their online banking platforms. However, ACH remains a common backbone for the secure and efficient movement of funds in the online banking landscape, providing users with the flexibility and convenience they need in managing their finances.

Common Uses of ACH

ACH, or Automated Clearing House, is widely used for various financial transactions, both by individuals and businesses. Let’s explore some of the common uses of ACH:

1. Direct Deposits: ACH is frequently used for direct deposits of salaries, pensions, Social Security benefits, and other forms of income. Employers, government agencies, and financial institutions can initiate ACH transactions to deposit funds directly into individuals’ bank accounts, eliminating the need for paper checks and ensuring prompt access to funds.

2. Recurring Payments: ACH is popular for setting up recurring payments such as monthly utility bills, mortgage payments, and membership dues. By authorizing ACH transactions, individuals and businesses can automate their payment processes, ensuring timely payments without the hassle of manual intervention.

3. Vendor Payments: Many businesses utilize ACH to make vendor payments. Instead of issuing physical checks, businesses can initiate ACH transactions to transfer funds electronically to their suppliers, contractors, and service providers. This streamlines the payment process, reduces administrative costs, and enhances efficiency.

4. Online Shopping: ACH is integrated into online shopping platforms, allowing customers to make payments using their bank account information securely. By selecting the ACH payment option at checkout, customers can authorize the transfer of funds directly from their bank accounts, providing an alternative to credit cards or other payment methods.

5. Loan Repayments: ACH is commonly used for loan repayments, including mortgages, auto loans, student loans, and personal loans. Borrowers can authorize their financial institutions or loan servicers to initiate ACH transactions to automatically deduct the loan payments from their bank accounts on designated dates each month.

6. Non-Profit Donations: ACH is an efficient way for individuals to make donations to non-profit organizations. By providing their bank account information, donors can authorize ACH transactions to transfer funds directly to their chosen charities, supporting causes they care about while minimizing administrative costs for the organizations.

7. Pre-Authorized Debits: ACH is used for pre-authorized debits, where individuals provide authorization to allow specific companies or organizations to automatically withdraw funds from their bank accounts. Examples include gym memberships, subscription services, and insurance premiums.

These are just a few examples of the common uses of ACH in various financial transactions. ACH provides a convenient and secure method for transferring funds electronically, offering individuals and businesses flexibility, efficiency, and ease of use.

ACH Processing Time

When it comes to ACH transactions, understanding the processing time is essential for individuals and businesses. The processing time for ACH transactions can vary based on several factors. Let’s take a closer look at the ACH processing time:

1. Initiation Time: The timing of when an ACH transaction is initiated plays a crucial role in the processing time. ACH transactions are typically processed on business days, excluding weekends and holidays. Transactions initiated outside of banking hours or on non-business days may experience a delay in processing.

2. Batch Processing: ACH transactions are processed in batches, meaning multiple transactions are grouped together for processing at specific intervals throughout the day. Financial institutions have cut-off times for submitting ACH transactions to be included in the next batch. Transactions initiated after the cut-off time may be processed in the next batch, leading to a slight delay in transfer time.

3. Settlement Period: ACH transactions involve the movement of funds between different financial institutions. Once the ACH transaction is initiated, the settlement process begins. Settlement refers to the final movement of funds from the originating bank to the recipient’s bank. This process typically takes one to two business days, but it can vary between financial institutions.

4. Receiving Financial Institution: The time it takes for the recipient’s financial institution, also known as the Receiving Depository Financial Institution (RDFI), to process and credit the funds can also impact the overall processing time. Different financial institutions may have varying internal processes and processing times, resulting in slight differences in the time it takes for funds to become available to the recipient.

5. Transaction Verification: As part of the ACH processing, transactions undergo verification and validation checks to ensure accuracy and security. Financial institutions verify the legitimacy of the transaction by confirming the account details, ensuring sufficient funds, and conducting fraud checks. These verification processes can contribute to the overall processing time of an ACH transaction.

Overall, ACH transactions typically take one to two business days for the funds to be transferred between bank accounts. However, it’s important to remember that timing can vary based on the factors mentioned above. To ensure timely delivery of funds, it’s advisable to initiate ACH transactions well in advance, especially for time-sensitive payments.

Additionally, it’s worth noting that some financial institutions offer expedited ACH processing for an additional fee. This option allows individuals and businesses to shorten the processing time and receive funds more quickly, making it a viable choice for urgent transactions.

Risks and Security of ACH Transactions

While ACH transactions offer convenience and efficiency, it’s important to be aware of the potential risks and the security measures in place to protect these transactions. Let’s explore the risks and security considerations associated with ACH transactions:

1. Unauthorized Transactions: One of the primary risks associated with ACH transactions is the potential for unauthorized transactions. It’s essential to safeguard your account information and be cautious of phishing attempts, fraudulent emails, or other forms of identity theft. Financial institutions implement security measures, such as multi-factor authentication and encryption, to mitigate these risks.

2. Fraudulent Activity: ACH transactions can be susceptible to fraudulent activity, including unauthorized withdrawals, unauthorized access to account information, or manipulation of transaction details. Financial institutions employ fraud monitoring systems and algorithms to detect suspicious activity and protect against fraud.

3. Account Compromise: In the event of an account compromise, unauthorized individuals may gain access to your account information and attempt fraudulent ACH transactions. It’s crucial to regularly monitor your account activity, report any suspicious transactions promptly, and notify your financial institution immediately in case of an account compromise.

4. Data Breaches: Data breaches pose a significant risk to the security of ACH transactions. If a financial institution’s or a payment processor’s data is compromised, it can lead to unauthorized access to account information. Financial institutions and payment processors have robust security protocols and compliance standards in place to protect against data breaches.

5. Compliance and Regulation: ACH transactions are subject to strict compliance and regulation to ensure security and protect the interests of both parties involved in the transaction. Financial institutions and payment processors adhere to guidelines set by regulatory bodies, such as NACHA, and implement measures to ensure compliance with industry standards.

6. Encryption and Secure Protocols: To mitigate the risks associated with ACH transactions, encryption and secure protocols are utilized to protect sensitive data during transmission. Financial institutions employ industry-standard encryption technologies to ensure the confidentiality and integrity of transaction data.

7. Customer Education and Awareness: Financial institutions play a critical role in educating their customers about the risks and security measures associated with ACH transactions. Customers are often provided with resources, guidelines, and best practices to enhance their awareness and protect against potential risks.

While the risks associated with ACH transactions exist, it’s important to note that financial institutions and payment processors take extensive measures to enhance the security and integrity of these transactions. By staying vigilant, keeping account information secure, and promptly reporting any suspicious activity, individuals can minimize the risks and confidently leverage the benefits offered by ACH transactions.

Conclusion

ACH, or Automated Clearing House, is a crucial electronic payment network that enables the seamless transfer of funds between bank accounts. Understanding the concept of ACH is essential for individuals and businesses looking to leverage this efficient and secure method of financial transactions.

In this article, we explored various aspects of ACH, including what it is, how it works, its benefits, and common uses. We compared ACH transactions to wire transfers and electronic funds transfers (EFT), highlighting their distinctions. We also discussed the role of ACH in online banking, emphasizing its integration into online platforms for convenient and secure financial management.

Furthermore, we delved into the factors that impact the processing time of ACH transactions, such as initiation time, batch processing, settlement periods, and verification processes. We also examined the risks associated with ACH transactions and the security measures implemented by financial institutions to safeguard against unauthorized transactions and fraud.

ACH provides individuals and businesses with a wide range of benefits, including speed, cost savings, convenience, security, accessibility, and streamlined cash flow. It facilitates recurring payments, direct deposits, vendor payments, online shopping, loan repayments, and more, making it a versatile option for various financial transactions.

While ACH transactions bring convenience, it’s important to remain vigilant and be aware of potential risks. By understanding common risks, such as unauthorized transactions or fraudulent activities, and adhering to security measures provided by financial institutions, individuals can mitigate risks and protect their financial information.

In conclusion, ACH is a valuable tool in the world of banking, offering individuals and businesses a secure, efficient, and cost-effective method of transferring funds electronically. By leveraging the benefits of ACH and remaining aware of the associated risks, individuals can confidently embrace this powerful financial transaction solution in their day-to-day activities.