Introduction

Welcome to the world of banking and finance, where numbers play a crucial role in ensuring smooth transactions. If you’ve ever come across the term “ACH number” and wondered what it means, you’ve come to the right place. In this article, we’ll explore the concept of an ACH number, how it relates to banking, and its significance in financial transactions.

The banking industry has evolved significantly over the years, with advancements in technology revolutionizing the way we handle our finances. The Automated Clearing House (ACH) system is one such innovation that has vastly improved the efficiency of electronic transfers.

Understanding the basics of an ACH number is essential for anyone who regularly deals with electronic payments, such as direct deposits, online bill payments, or automatic debits. Whether you’re an individual consumer or a business owner, having a grasp of this concept can help you navigate through the intricacies of the banking world more efficiently.

So, what exactly is an ACH number? How does it work, and what purpose does it serve? These questions will be answered in the subsequent sections as we delve into the fascinating world of ACH numbers in banking.

What is an ACH number?

An ACH number, also known as an ABA routing number or routing transit number (RTN), is a unique nine-digit code used to identify financial institutions within the United States. This number plays a vital role in facilitating electronic fund transfers, including direct deposits, bill payments, and other automated transactions.

The ACH number is assigned to each bank or credit union by the American Bankers Association (ABA) and serves as a means of identifying the institution in the vast network of financial entities. Just like a mailing address directs mail to the correct destination, an ACH number ensures that electronic transfers reach the intended bank or credit union.

While the ACH number might seem similar to other bank identifiers, such as an account number or a check number, it serves a different purpose. Unlike an account number, which identifies an individual’s or organization’s specific account, an ACH number identifies the financial institution itself.

Each bank and credit union in the United States has its unique ACH number, making it easy to differentiate between institutions. Whether you’re sending money to a friend, receiving your salary through direct deposit, or paying your bills online, the ACH number is crucial in determining where the funds are coming from or going to.

It’s essential to note that an ACH number is different from a SWIFT code, which is used for international money transfers. ACH numbers are used solely within the United States, while SWIFT codes are used internationally to ensure secure and accurate cross-border transactions.

Now that we have a basic understanding of what an ACH number is, let’s explore how the ACH system works as a whole and how the ACH number fits into the broader electronic payments landscape.

How does the ACH system work?

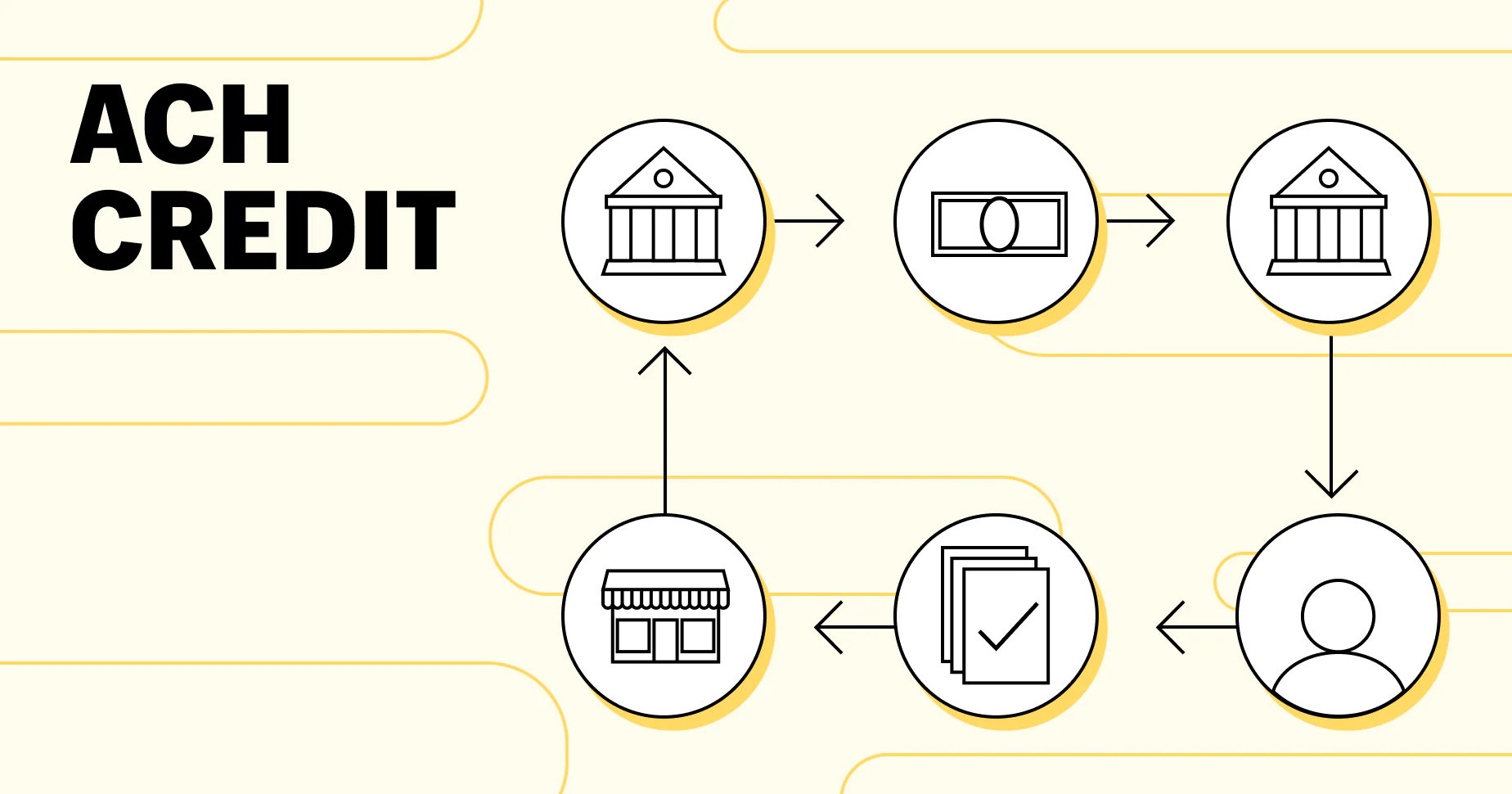

The ACH system is a sophisticated network that enables the efficient transfer of funds between banks and credit unions in the United States. It operates by electronically processing batches of transactions, resulting in a seamless transfer of funds from one account to another.

When a payment is initiated, whether it’s a direct deposit from an employer or an online bill payment, it follows a predefined path within the ACH system. Here’s a simplified breakdown of how the ACH system works:

- Initiation: The process begins with the originator, who could be an individual or an organization, initiating a payment transaction. This typically involves providing the necessary details, such as the recipient’s ACH number, account number, and the amount to be transferred.

- Originating Financial Institution: The originator’s bank, or the originating financial institution, receives the payment instructions and verifies the availability of funds in the originator’s account. Once the funds are confirmed, the originating financial institution prepares the transaction to be sent through the ACH system.

- ACH Operator: The originating financial institution submits the transaction to an ACH operator, which is typically a regional, private-sector organization that acts as an intermediary between financial institutions. The ACH operator processes and routes the transaction to the appropriate receiving financial institution.

- Receiving Financial Institution: The receiving financial institution, or the bank of the recipient, receives the transaction from the ACH operator. It verifies the recipient’s account details and ensures that the funds are properly credited to the correct account.

- Recipient: Finally, the funds are made available to the recipient, whether it’s an individual or an organization. The recipient can access the funds through their bank account and utilize them as needed.

The entire process, from initiation to the availability of funds, typically takes one to two business days. However, in some cases, the funds may be available on the same day, depending on the transaction type and the participating financial institutions.

The ACH system operates on a reliable and secure infrastructure, ensuring the confidentiality and integrity of electronic transactions. The use of ACH numbers in these transactions helps prevent errors and ensures that funds are properly directed to the correct financial institutions.

Now that we have a better understanding of how the ACH system works, let’s explore the concept of an ACH routing number and its importance in the overall process.

What is an ACH routing number?

An ACH routing number is a subset of the ACH number and plays a crucial role in the proper routing and processing of electronic transactions. It is a nine-digit code that identifies the specific bank or credit union within the ACH system.

Think of the ACH routing number as a unique identifier assigned to each financial institution to ensure accurate and timely transfers. Just like a postal code directs mail to the right region or city, an ACH routing number directs electronic payments to the correct banking institution.

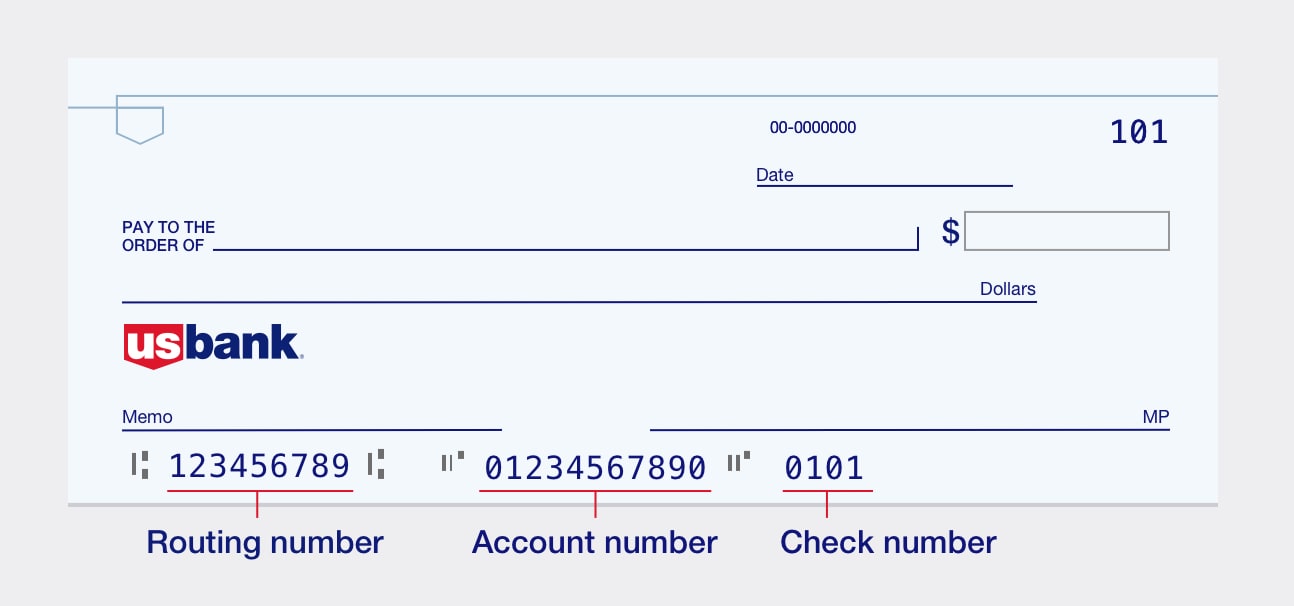

The ACH routing number is typically found on checks (usually at the bottom left corner) or on the bank’s website. It is important to note that not all nine-digit numbers found on a check are ACH routing numbers. The ACH routing number is specifically designated for processing electronic transactions and may differ from the check number or account number.

When initiating an electronic transaction, such as a direct deposit or an online payment, the ACH routing number plays an essential role in ensuring that the funds are correctly routed to the intended financial institution. It works hand-in-hand with other information, such as the recipient’s account number and the transaction amount, to facilitate a smooth transfer of funds.

It’s crucial to enter the ACH routing number accurately when setting up electronic payments to avoid any delays or misdirected funds. Even a small error in entering the routing number can result in the transaction being rejected or sent to the wrong institution.

It’s also worth mentioning that some financial institutions may have multiple ACH routing numbers due to mergers, acquisitions, or geographic locations. In such cases, it’s important to use the correct ACH routing number associated with the specific account or transaction to avoid any issues.

The ACH routing number is an essential component of the ACH system, working behind the scenes to ensure reliable and accurate electronic fund transfers. Knowing your bank’s ACH routing number can come in handy when setting up direct deposits, online bill payments, or any other automated transactions.

Now that we understand the purpose of an ACH routing number, let’s explore the significance of the ACH number as a whole and how it differs from a traditional check number.

What is the purpose of an ACH number?

The primary purpose of an ACH number is to facilitate the efficient and secure processing of electronic fund transfers within the Automated Clearing House (ACH) system. It serves as a unique identifier for each financial institution, allowing for accurate routing and delivery of funds from one account to another.

One of the key advantages of using an ACH number is the speed and convenience it offers in conducting various financial transactions. Whether it’s receiving your salary through direct deposit, making online bill payments, or setting up automatic debits, the ACH number ensures that these transactions occur smoothly and reliably.

Moreover, the ACH number enhances the accuracy of electronic transfers by eliminating the need for manual processing. With traditional paper checks, errors and delays can occur due to manual handling and routing. However, with the ACH system and its associated ACH numbers, transfers can be automated, reducing the risk of human error and expediting the movement of funds.

Furthermore, the ACH system and the use of ACH numbers significantly reduce the reliance on paper-based transactions, resulting in cost savings for both financial institutions and consumers. By digitizing the transfer process, there’s less need for physical checks, envelopes, and postage, making electronic transactions more environmentally friendly and cost-effective.

The ACH number also plays a crucial role in promoting financial inclusion and access to banking services. Many individuals and businesses who do not have access to traditional banking now rely on electronic payments to receive payments and make purchases. The use of ACH numbers allows these individuals to participate in the digital economy, giving them greater financial autonomy and opportunities.

Moreover, the ACH system and ACH numbers provide a secure platform for financial transactions. The system incorporates robust security measures to protect sensitive information and prevent fraudulent activity. By utilizing encryption, authentication mechanisms, and other security features, the ACH system ensures the confidentiality and integrity of electronic transfers.

Overall, the purpose of an ACH number is to streamline and enhance the efficiency of electronic fund transfers, providing individuals and businesses with a reliable and convenient method for conducting financial transactions. It promotes financial inclusion, reduces reliance on paper-based transactions, and fosters a secure environment for the movement of funds.

Now that we understand the purpose of an ACH number, let’s explore how to find your bank’s ACH number.

How to find your bank’s ACH number?

Finding your bank’s ACH number is a straightforward process that can be done using a few simple methods. Here are some ways to obtain your bank’s ACH number:

- Check your bank’s website: Many banks provide their ACH routing numbers on their website. Look for the “Routing Number” or “ABA Routing Number” section, which typically includes the ACH routing number along with other account-related information.

- Refer to your checkbook: If you have access to your physical checks, the ACH routing number is often printed on the bottom left corner of the check, followed by the account number and the check number. Make sure to differentiate the ACH routing number from other numbers on the check, such as the account number or the check number itself.

- Contact your bank: If you are unable to find the ACH routing number using the above methods or need further clarification, it is recommended to contact your bank directly. Reach out to their customer service helpline or visit a branch location to speak with a representative who can assist you in providing the correct ACH routing number.

It’s important to ensure the accuracy of the ACH routing number to prevent any issues with your transactions. Always double-check the number and verify that it matches the ACH routing number provided by your bank.

Additionally, keep in mind that if you have multiple accounts with the same bank, each account might have a unique ACH routing number associated with it. This is particularly relevant for businesses that may have separate accounts for different purposes. Ensure that you are using the correct ACH routing number specific to the account you intend to use for the transaction.

Finally, it’s worth noting that the same ACH routing number may be used by multiple branches of a bank, especially if they are under the same entity. This is because the ACH routing number is associated with the financial institution rather than the specific branch. Therefore, even if you change your branch location, the ACH routing number will typically remain the same.

By following these methods, you can easily find your bank’s ACH number and ensure the smooth processing of electronic transactions.

Now that we have explored how to find your bank’s ACH number, let’s distinguish the differences between an ACH number and a check number.

What are the differences between an ACH number and a check number?

While both an ACH number and a check number are associated with banking transactions, there are significant differences between them in terms of their purpose and usage. Here are the key distinctions:

Purpose:

An ACH number, also known as an ABA routing number or routing transit number, is used to identify the financial institution within the Automated Clearing House (ACH) system. It ensures accurate routing and delivery of electronic fund transfers. On the other hand, a check number is a unique identifier printed on a physical check and is primarily used for record-keeping and tracking purposes.

Usage:

The ACH number is used exclusively for electronic transactions, such as direct deposits, online bill payments, and automated transfers. It enables the secure and efficient movement of funds between financial institutions. In contrast, the check number is specific to physical checks and is used for referencing and organizing transactions. When writing a check, the check number is typically recorded to track the sequence of issued checks.

Format:

An ACH number is a nine-digit code, while a check number is typically a shorter numeric value, often ranging from three to six digits. The ACH number follows a standardized format, assigned by the American Bankers Association (ABA), which allows for easy identification and processing within the ACH system. The check number is assigned by the account holder’s bank, representing a unique number for each check issued.

Location:

The ACH number is primarily used in electronic transfers and is not typically visible on physical checks. It is usually found on bank statements or through online banking services. In contrast, the check number is prominently displayed on the bottom right corner of a physical check, along with other essential details such as the routing number and account number.

Function:

The primary function of an ACH number is to ensure accurate routing and delivery of electronic fund transfers, providing a fast and secure method for making payments and receiving funds. It is an integral part of the ACH system, enhancing efficiency and accuracy in financial transactions. On the other hand, the check number is used to track and record transactions made by physical checks, allowing for easy reconciliation and balancing of accounts.

By understanding the differences between an ACH number and a check number, you can navigate the world of electronic and paper-based transactions with greater clarity and confidence.

Now that we have explored the distinctions between an ACH number and a check number, let’s conclude our article.

Conclusion

In conclusion, understanding the concept of an ACH number is essential in today’s digital banking landscape. The ACH number serves as a unique identifier for financial institutions within the Automated Clearing House (ACH) system, facilitating secure and efficient electronic fund transfers.

We have learned that an ACH number is different from a check number, as it identifies the financial institution rather than individual accounts. It plays a vital role in accurate routing and delivery of funds, ensuring that transactions reach the intended recipient without delay or error.

The ACH system itself operates through a network of banks and credit unions, electronically processing batches of transactions and expediting the movement of funds. This digitized process offers convenience, speed, and cost savings for both financial institutions and consumers.

When it comes to finding your bank’s ACH number, options such as checking your bank’s website or referring to your checkbook can provide you with the necessary information. It is crucial to ensure the accuracy of the ACH routing number to avoid any disruptions in your electronic transactions.

Overall, the ACH number and its associated system play a crucial role in promoting financial inclusion, reducing reliance on paper-based transactions, and fostering a secure environment for electronic fund transfers. By understanding and utilizing the ACH number effectively, individuals and businesses can enjoy the convenience and efficiency of digital transactions.

So, the next time you encounter the term “ACH number” in the world of banking, you can confidently navigate through the complexities of electronic transfers, knowing that you have a solid understanding of its purpose and significance.

Thank you for joining us on this exploration of ACH numbers in banking. Should you have any further questions or require additional information, don’t hesitate to reach out to your financial institution for personalized guidance.