What Is a Banking Routing Number?

A banking routing number, also known as the routing transit number (RTN), is a unique identification number assigned to a financial institution. It serves as an address for processing electronic transactions, such as direct deposits, wire transfers, and automatic bill payments.

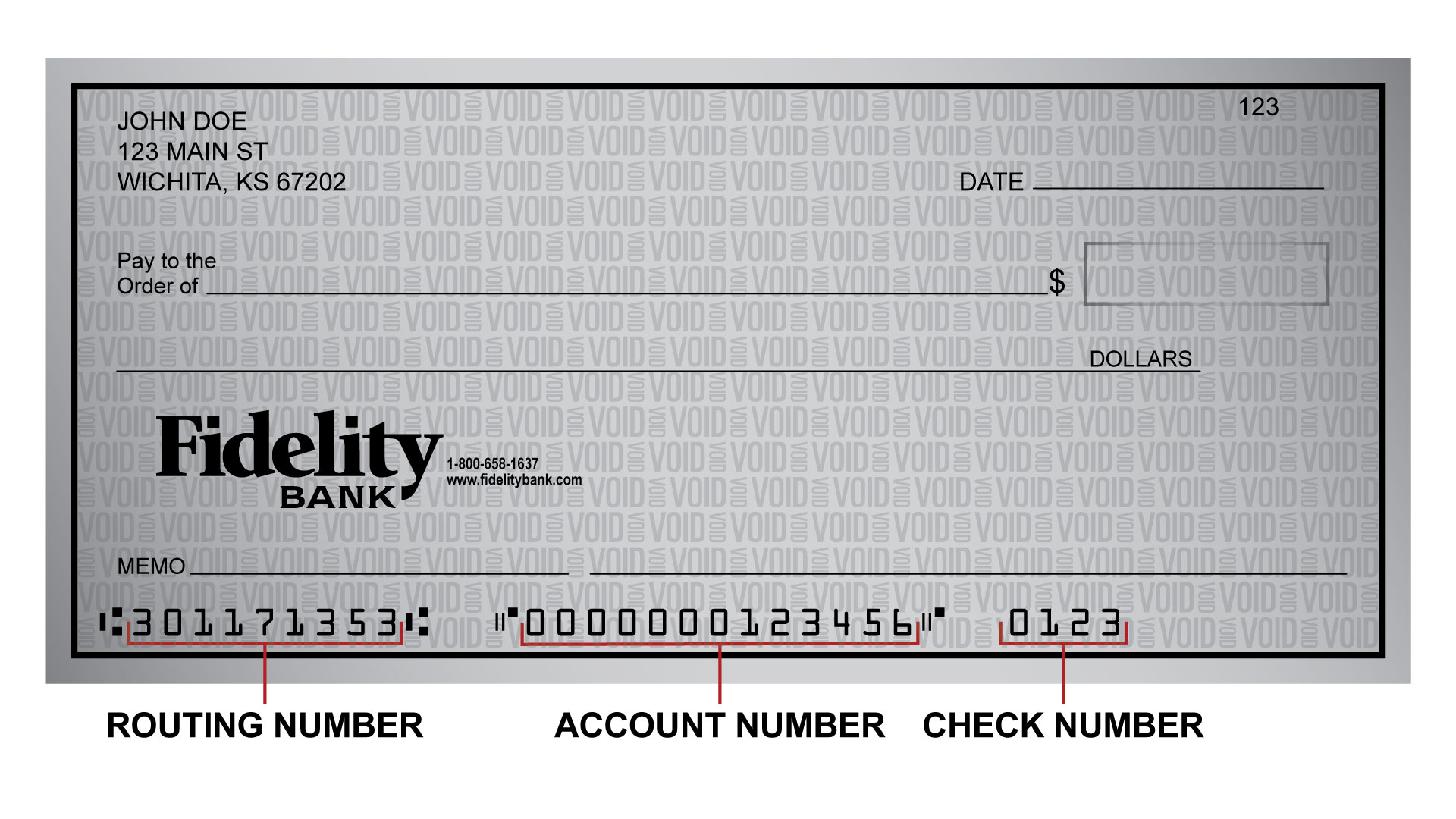

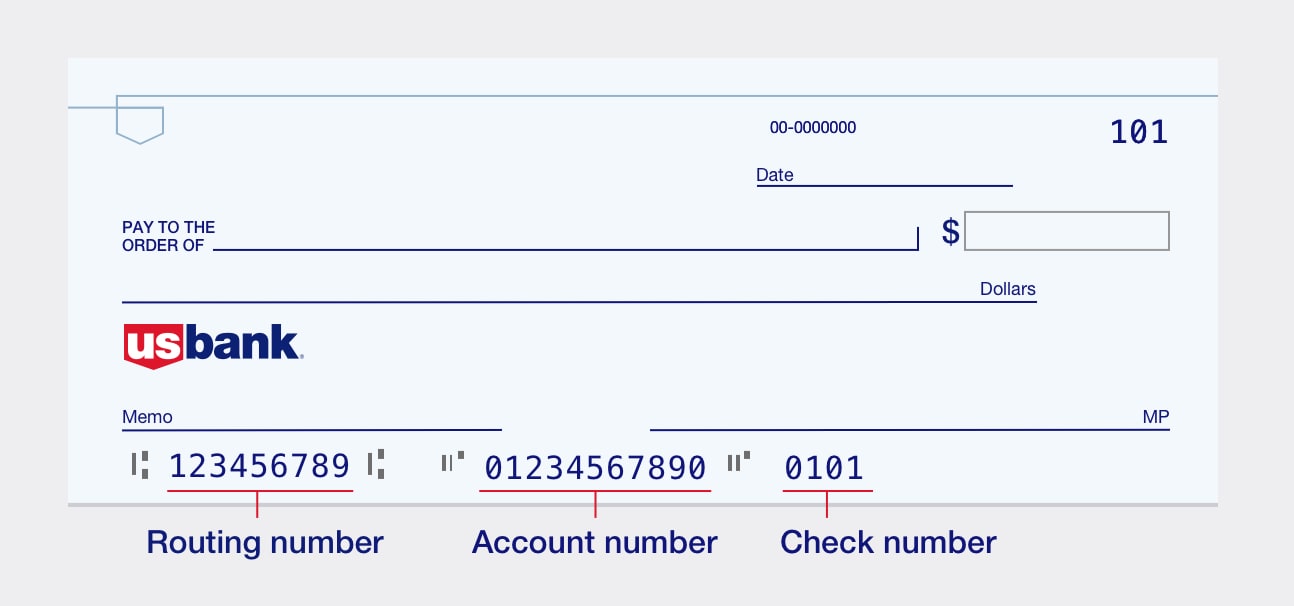

The routing number consists of 9 digits and is typically found at the bottom left-hand corner of personal checks issued by banks in the United States. It is essential for ensuring accurate and secure transfer of funds between different financial institutions.

Think of the routing number as a postal code that helps direct your financial transactions to the correct bank or credit union. Just like how a postal code would guide a letter to the appropriate destination, a routing number ensures that money transfers are directed to the right branch or specific account within a larger financial institution.

Each routing number is unique to a specific bank or credit union. It is like a digital fingerprint that distinguishes one financial institution from another. Therefore, it is important to provide the correct routing number when setting up direct deposits or making payments to ensure the seamless flow of funds.

While the routing number is primarily used for domestic transactions within the United States, some financial institutions may have separate routing numbers for international transfers. These international routing numbers, commonly referred to as SWIFT codes, are necessary for processing cross-border payments.

Moreover, it is worth noting that the routing number is not a secret or sensitive piece of information. Unlike account numbers or social security numbers, the routing number is publicly available and can be easily found online or by contacting the bank directly.

In summary, a banking routing number is a unique identification number assigned to a financial institution. It facilitates the secure and accurate transfer of funds for various transactions. Understanding the role of routing numbers can help ensure that your financial transactions are processed smoothly and efficiently.

Introduction

When it comes to managing our finances, there are various technical terms and concepts we come across. One such term is a banking routing number. If you’ve ever wondered what a routing number is and why it is important, you’ve come to the right place.

In this article, we will explore the fascinating world of routing numbers and uncover their significance in the banking industry. Whether you’re a seasoned banking professional or a curious individual looking to expand your financial knowledge, this article will provide you with a comprehensive understanding of what a routing number is and how it affects your financial transactions.

We’ll begin by explaining what a routing number actually is and how it functions in the banking system. We’ll then explore where you can find your routing number and the various types of routing numbers that exist. Understanding the purpose of a routing number and how it ensures the smooth transfer of funds will be the focus of our discussion.

It’s important to note that routing numbers are specific to the United States financial system, so our discussion will primarily revolve around the usage of routing numbers in the U.S. banking industry. However, the concepts and principles we cover can be applied to banking systems in other countries as well.

Whether you’re an individual looking to set up direct deposit for your paycheck or a business owner seeking to make electronic payments, understanding routing numbers is crucial. By the end of this article, you will have the knowledge and confidence to navigate the world of routing numbers and make informed financial decisions.

So, let’s delve into the topic and unravel the mystery of banking routing numbers.

What is a Routing Number?

A routing number, also known as a routing transit number (RTN), is a unique nine-digit identification number assigned to financial institutions in the United States. It serves as a vital piece of information for processing various electronic transactions, including direct deposits, wire transfers, and automatic bill payments.

Think of a routing number as an address that directs funds to the right bank or credit union. Similar to how a postal code ensures that mail is delivered to the correct location, a routing number ensures that funds are routed to the appropriate branch or account within a financial institution.

Routing numbers are printed on personal checks issued by banks and are usually located at the bottom left-hand corner. They are typically followed by the account number and the check number. However, routing numbers can also be obtained by contacting the bank directly or through their website or online banking platform.

Each routing number is unique to a specific financial institution, ensuring accurate and secure transfer of funds. For example, a bank’s routing number may vary from one branch to another, depending on its geographic location. This enables transactions to be efficiently processed within a vast network of banks and credit unions across the country.

It’s important to note that routing numbers facilitate domestic transactions within the United States. For international transfers, financial institutions often use a different set of codes known as Society for Worldwide Interbank Financial Telecommunication (SWIFT) codes. SWIFT codes are essential for processing cross-border payments and identifying the specific bank involved.

Furthermore, routing numbers are publicly available and not considered sensitive or confidential information. Unlike account numbers or social security numbers, which should be kept confidential, routing numbers can be freely shared when setting up direct deposits or making electronic payments.

In summary, a routing number is a unique identifier assigned to financial institutions in the United States. It acts as an address that ensures the accurate and secure transfer of funds between banks and credit unions.

How does a Routing Number Work?

Routing numbers play a crucial role in the efficient processing of financial transactions within the U.S. banking system. They act as a roadmap, guiding funds from the sender to the intended recipient’s financial institution. Understanding how routing numbers work can help demystify the process of electronic fund transfers.

When you initiate a transaction, such as a direct deposit or bill payment, the routing number acts as the key piece of information that instructs the funds to be transferred to the correct bank or credit union. It ensures that the money ends up in the correct account, whether it’s a checking, savings, or loan account.

Here’s a step-by-step breakdown of how a routing number works:

- Initiating the Transaction: When you provide your bank or employer with your routing number, you are giving them the necessary information to initiate the transaction. This could be setting up direct deposit for your paycheck, authorizing an automatic bill payment, or receiving a wire transfer.

- Request Processing: Once the transaction is initiated, the sender’s bank or financial institution processes the request. They will use the routing number to determine the destination bank’s identity and find the specific branch or account where the funds should be directed.

- Routing the Funds: The sender’s bank will send the transaction request to the Automated Clearing House (ACH) or an intermediary bank. The ACH or intermediary bank acts as a clearinghouse, managing the flow of funds between financial institutions.

- Verification and Processing: The receiving bank, using the routing number, verifies the transaction details and ensures that the funds are directed to the intended recipient’s account. They cross-reference the routing number with their internal database to match it with the appropriate branch or account.

- Completing the Transaction: Once the transaction is verified, the funds are transferred from the sender’s bank to the recipient’s bank. The routing number ensures that the transfer is accurate, secure, and reaches the correct account promptly.

By utilizing routing numbers, the U.S. banking system enables seamless and efficient transfer of funds between different financial institutions. It simplifies the complex process of directing funds, ensuring that transactions are processed accurately and securely.

It’s important to note that routing numbers are specific to the United States financial system. Other countries have their own unique systems and identifiers for routing funds. Therefore, when dealing with international transfers, it is essential to understand and use the appropriate codes, such as SWIFT codes.

In summary, routing numbers act as a roadmap, guiding funds from the sender to the recipient’s bank or credit union. They facilitate accurate and secure transfer of funds within the U.S. banking system, ensuring that transactions are processed smoothly and efficiently.

Where can I find my Routing Number?

If you need to find your routing number for a particular bank or credit union, there are several ways to obtain this information. Here are some common methods:

- Personal Checks: The most accessible place to find your routing number is on your personal checks. Typically, the routing number is located at the bottom left-hand corner of the check. It is a nine-digit number followed by your account number and the check number.

- Bank Statements: Your routing number can also be found on your bank statements. Many financial institutions include routing numbers on monthly statements along with other account information. If you receive paper statements, or if you can access electronic statements through online banking, you should be able to locate your routing number there.

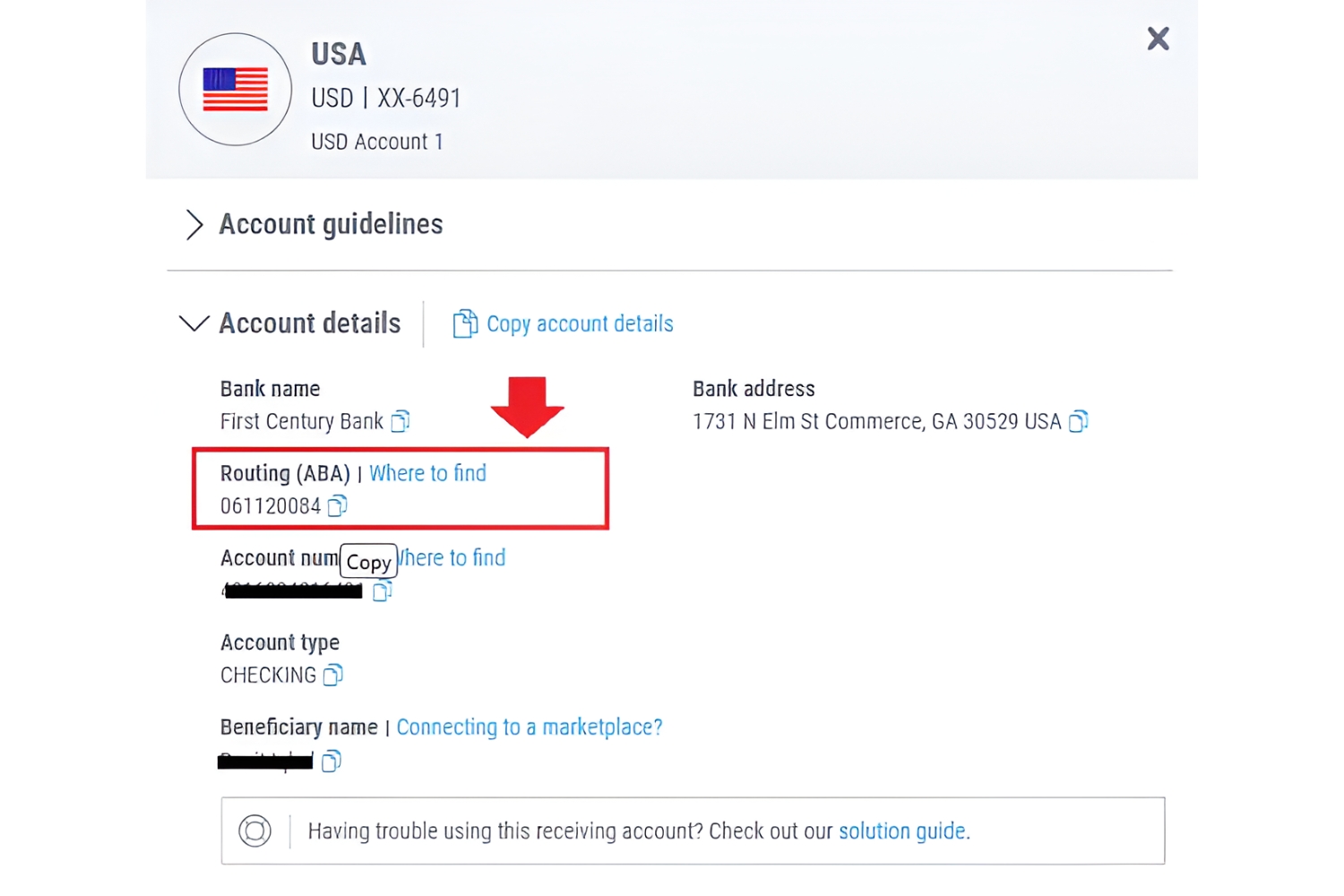

- Online Banking: If you have access to online banking, you can typically find your routing number by logging into your account. Once logged in, navigate to your account details or settings, where you will usually find a section displaying your routing number along with other account information. If you’re having trouble locating it, you can use the search function within the online banking platform or consult the bank’s FAQ section or customer support for assistance.

- Bank’s Website: Many banks provide their routing numbers on their official websites. Simply visit your bank’s website and search for “routing number.” The information should be readily available, often in the FAQ or customer support section. Some banks even have a dedicated page where you can search for routing numbers by entering your location or the bank’s name.

- Customer Support: If you’re unable to find your routing number through any of the above methods, you can always contact your bank’s customer support. They will be able to provide you with the correct routing number associated with your account. You can reach out to them via phone, email, or even through a live chat feature if available on the bank’s website.

It’s important to note that for different types of transactions, such as domestic or international wire transfers, the routing number required may differ. In such cases, it’s always advisable to double-check with your bank to ensure that you have the correct routing number for the specific transaction you wish to initiate.

Remember, a routing number is a public piece of information, so you can freely share it when setting up direct deposits, making payments, or providing it to employers or financial institutions. However, it’s essential to keep other sensitive account details, such as your account number and social security number, confidential.

In summary, you can find your routing number on your personal checks, bank statements, through online banking platforms, on the bank’s official website, or by contacting customer support. It’s important to have the correct routing number for specific transactions and to keep other sensitive account information private.

Different Types of Routing Numbers

Routing numbers can vary depending on the type of transaction and the location of the financial institution. While the basic format of a routing number remains the same (nine-digits), there are different types of routing numbers that serve specific purposes within the U.S. banking system. Let’s explore some of these variations:

- ACH Routing Numbers: Automated Clearing House (ACH) routing numbers are used for processing electronic transactions, such as direct deposits, electronic transfers, and automated bill payments. These routing numbers are specifically designed for transactions within the ACH network, which facilitates the transfer of funds between financial institutions. ACH routing numbers ensure the accurate and efficient routing of electronic payments.

- Wire Transfer Routing Numbers: Wire transfer routing numbers are used for initiating wire transfers, which involve the electronic transfer of funds between banks or credit unions. These routing numbers, also known as RTN/ABA numbers, are required for both domestic and international wire transfers. Wire transfer routing numbers are essential for identifying both the sending and receiving financial institutions and ensuring the smooth transfer of funds.

- Paper Transaction Routing Numbers: In the past, routing numbers were primarily used for paper-based transactions, such as writing checks or initiating manual fund transfers. These routing numbers were associated with the physical location of the bank branch where the transaction was being conducted. While paper-based transactions have become less common with the rise of electronic transfers, some financial institutions still maintain separate routing numbers for these purposes.

- International Routing Numbers: For international transactions, such as cross-border wire transfers, financial institutions often use a different set of codes known as Society for Worldwide Interbank Financial Telecommunication (SWIFT) codes. SWIFT codes are a standardized format used across the globe to identify specific banks or financial institutions involved in international transactions. These codes ensure that funds are directed to the correct international destination, regardless of the country or currency involved.

- Internal Routing Numbers: In some cases, larger financial institutions may use internal routing numbers for specific purposes within their organization. These internal routing numbers are used to route funds between different branches, departments, or accounts held within the same bank or credit union. They are unique to the financial institution and are not used for external transactions.

It’s important to note that the specific type of routing number needed for a transaction depends on the nature and destination of the funds being transferred. It’s always advisable to confirm with your bank or financial institution which particular routing number should be used for your specific transaction to ensure its smooth processing.

In summary, there are different types of routing numbers, including ACH routing numbers, wire transfer routing numbers, paper transaction routing numbers, international routing numbers (SWIFT codes), and internal routing numbers. Each type serves a specific purpose within the banking system and is used for different types of transactions.

What is the Purpose of a Routing Number?

The primary purpose of a routing number is to ensure the accurate and secure transfer of funds between financial institutions. It acts as a vital identifier that directs electronic transactions, such as direct deposits, wire transfers, and automatic bill payments, to the correct bank or credit union.

Here are some key purposes of a routing number:

- Transaction Routing: Routing numbers enable the routing of funds to the appropriate financial institution. Just like a postal code ensures that a letter is delivered to the correct address, a routing number directs transactions to the specific bank or credit union where the recipient’s account is held. This is a crucial step in ensuring that funds reach the intended destination accurately and efficiently.

- Account Identification: Routing numbers also play a role in account identification. By using a combination of the routing number and the account number, financial institutions can accurately identify the specific account within a bank or credit union that should receive the funds. This helps prevent any confusion or misrouting of funds.

- Secure and Efficient Fund Transfers: Routing numbers ensure secure and efficient fund transfers within the banking system. They provide a standardized method of directing transactions, reducing errors and delays in processing. With the use of routing numbers, financial institutions can reliably and securely transfer funds between accounts, enabling individuals and businesses to make timely payments and access their funds without complications.

- Network Connectivity: Routing numbers play a critical role in connecting financial institutions within the vast network of the U.S. banking system. They establish the necessary connections and pathways for the seamless transfer of funds between banks, credit unions, and other financial entities. This network connectivity ensures that funds can be transferred smoothly, regardless of the location of the sender and recipient.

- Compliance and Regulation: Routing numbers also have regulatory purposes. They help monitor and track financial transactions for regulatory compliance and anti-money laundering measures. By accurately identifying the sending and receiving institutions involved in a transaction, routing numbers assist in ensuring the integrity and legality of electronic funds transfers.

Ultimately, the purpose of a routing number is to facilitate secure, accurate, and efficient transfers of funds between financial institutions. It ensures that transactions are directed to the correct recipient’s account and that the transfer process complies with regulatory standards.

It’s important to have the correct routing number when setting up direct deposits, making electronic payments, or conducting other financial transactions. Using an incorrect routing number can result in delays or errors in fund transfers, which can cause inconvenience and potentially incur additional fees.

In summary, the purpose of a routing number is to facilitate the accurate and secure transfer of funds between financial institutions. It ensures that transactions are routed to the correct destination and comply with regulatory standards. Routing numbers play a vital role in connecting the vast network of the banking system and enable seamless fund transfers for individuals and businesses alike.

Can a Routing Number be Changed?

Routing numbers are unique identification numbers assigned to financial institutions, and they typically do not change. However, in certain circumstances, a routing number can be changed. Let’s explore the factors that can lead to a routing number change and how it can impact your banking transactions:

1. Merger or Acquisition: When two financial institutions merge or one institution acquires another, it can result in a change of routing number. This occurs to streamline operations and consolidate processes. In such cases, customers of the affected banks are notified of the routing number change well in advance. It’s important to update your routing number with any relevant payers or vendors to avoid disruptions in electronic transactions.

2. Reorganization or Restructuring: The reorganization or restructuring of a financial institution can also lead to a routing number change. This may include changes in the legal or operational structure of the bank, such as a change in ownership, name, or location. Again, customers are typically notified in advance, and it’s important to update your routing number to ensure smooth transactions.

3. System Upgrades or Conversions: Financial institutions occasionally upgrade their systems or convert to new processing platforms. During such upgrades or conversions, there may be a change in the routing number. This is done to ensure compatibility and efficiency with the updated systems. Customers are generally notified in advance, and the bank provides instructions on updating the routing number for any recurring transactions or direct deposits.

4. Geographic Relocation: In some cases, a financial institution may relocate its main office or branch to a different geographic location. This relocation can result in a change of routing number, especially if the move involves a different state or region. Customers are informed about the routing number change and are required to update their records accordingly.

It’s important to note that routing number changes are relatively rare and typically occur due to significant events, such as mergers, acquisitions, or system upgrades. Financial institutions strive to minimize disruptions and provide ample notice to customers to update their routing number information for a seamless transition.

If your bank undergoes a routing number change, it’s important to take the following steps:

- Contact the Bank: Reach out to your bank for detailed information about the routing number change and any necessary actions you need to take.

- Update Direct Deposits: Inform your employer, pension provider, or any other entities that make direct deposits into your account about the routing number change. Provide them with the updated routing number to ensure uninterrupted deposits.

- Notify Billers and Service Providers: Update the routing number with any billers or service providers who automatically deduct payments from your account to avoid any disruptions or missed payments.

- Update Personal Records: Update your personal records, including online banking profiles, payment apps, and any other platforms where your banking information is stored to reflect the new routing number.

By proactively updating your routing number information and notifying relevant parties, you can minimize any potential disruptions in your banking transactions resulting from a routing number change.

In summary, while routing numbers typically do not change, certain events such as mergers, reorganizations, system upgrades, or relocations can lead to a routing number change. Customers are typically notified in advance and are required to update their routing number information with employers, billers, and service providers to ensure uninterrupted electronic transactions.

Conclusion

Understanding banking routing numbers is essential for navigating the world of electronic transactions and ensuring the smooth flow of funds between financial institutions. In this article, we explored what a routing number is and why it is important in the banking system.

A routing number acts as a unique identification number assigned to financial institutions in the United States. It facilitates accurate and secure transfer of funds for various transactions, including direct deposits, wire transfers, and automatic bill payments. Routing numbers ensure that funds are directed to the correct bank or credit union and reach the intended recipient’s account promptly and efficiently.

Routing numbers can be found on personal checks, bank statements, online banking platforms, or by contacting your bank’s customer support. It’s important to have the correct routing number for specific transactions and to keep other sensitive account information private.

We also discussed different types of routing numbers, such as ACH routing numbers, wire transfer routing numbers, and international routing numbers, which serve specific purposes within the banking system. These variations ensure the accurate routing and processing of different types of transactions, both domestically and internationally.

In the event of a routing number change, which can occur due to mergers, acquisitions, system upgrades, or relocations, it’s important to stay informed and update your records accordingly. By promptly updating your routing number information with employers, billers, and service providers, you can avoid disruptions in your financial transactions.

In conclusion, routing numbers are fundamental to the efficient and secure transfer of funds in the banking industry. By understanding how routing numbers work, where to find them, and their various types, you can confidently manage your financial transactions and ensure that funds are accurately and seamlessly directed to their intended destinations.