What Is A BIC Number?

A Bank Identifier Code (BIC), also known as a SWIFT code, is a unique alphanumeric code used to identify a specific bank or financial institution globally. It is primarily used in international banking transactions to ensure accurate and efficient communication between banks.

The BIC number serves as a standardized identification code that facilitates secure and reliable communication between financial institutions. It is similar to a bank’s fingerprint, providing crucial information about the bank, such as its name, location, and branch. With the increasing globalization of the financial industry, BIC numbers have become an essential component of international transactions.

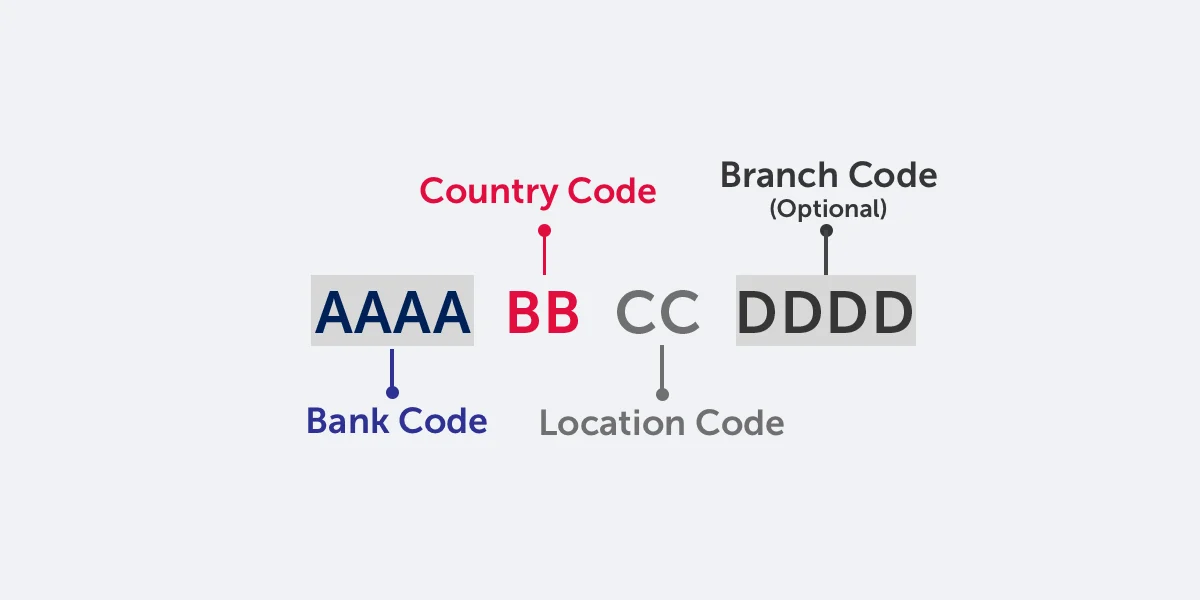

Each BIC code consists of a combination of letters and numbers and follows a standardized format. The structure of a BIC number includes a four-letter Bank Code, a two-letter Country Code representing the bank’s home country, a two-letter Location Code representing the bank’s specific location or branch, and an optional three-letter Branch Code to identify a particular branch within a location.

For example, a BIC number may appear as: ABCDUS33XXX, where “ABCD” represents the Bank Code, “US” represents the Country Code (United States), “33” represents the Location Code, and “XXX” represents the optional Branch Code.

The BIC number plays a vital role in ensuring accurate and secure transmission of information during international money transfers, payments, and other cross-border financial transactions. It helps banks identify each other, verify the authenticity of transactions, and prevent errors or delays by ensuring the funds are directed to the correct recipient institution.

Understanding the structure and importance of BIC numbers is crucial for individuals and businesses involved in international transactions. These alphanumeric codes enable efficient and error-free communication between banks, ensuring the smooth flow of funds across borders.

In the next section, we will explore how BIC numbers are used in banking and the significance they hold in facilitating seamless international transactions.

How is a BIC Number Used in Banking?

BIC numbers play a significant role in international banking by facilitating efficient and secure communication between financial institutions. Here are some key ways in which BIC numbers are used in banking:

1. Identification of Banks: BIC numbers are primarily used to identify banks and financial institutions worldwide. When initiating an international money transfer or transaction, the BIC number ensures that the funds are directed to the correct bank and branch.

2. Secure Communication: BIC numbers enable secure communication between banks during international transactions. By including the BIC number in transaction messages, banks can authenticate the message sender, ensuring that the communication is legitimate and authorized.

3. Swift Network Integration: The Society for Worldwide Interbank Financial Telecommunication (SWIFT) is the global network used by financial institutions to send and receive financial messages. BIC numbers are an integral part of the SWIFT network, allowing banks to locate and communicate with each other seamlessly.

4. Cross-Border Payments: BIC numbers are especially important in cross-border payments, including international wire transfers and electronic fund transfers. When sending money overseas, the sending bank includes the BIC number of the recipient bank to ensure the correct routing and crediting of the funds.

5. Confirmation of Bank Details: BIC numbers provide a way to verify the authenticity of bank details. Before initiating any transaction with a foreign bank, individuals and businesses can use BIC numbers to ensure they are dealing with a legitimate and authorized institution.

6. Compliance with Regulatory Requirements: BIC numbers are essential for banks to comply with regulatory requirements, such as anti-money laundering (AML) and know-your-customer (KYC) regulations. These codes assist in maintaining accurate records and audit trails for international transactions.

7. International Trade and Commerce: BIC numbers facilitate international trade and commerce by ensuring smooth and efficient payment transfers between buyers and sellers. They play a crucial role in ensuring that funds are transferred accurately and promptly, reducing delays and mitigating risks.

In summary, BIC numbers are extensively used in banking to identify banks, facilitate secure communication, ensure compliance with regulatory requirements, and streamline international transactions. Understanding the importance of BIC numbers is essential for individuals and businesses engaged in cross-border financial activities.

Understanding the Structure of a BIC Number

The structure of a Bank Identifier Code (BIC) or SWIFT code follows a standardized format that consists of a combination of letters and numbers. Each part of the BIC number serves a specific purpose in identifying a bank or financial institution. Let’s break down the structure of a BIC number:

1. Bank Code: The Bank Code is a four-letter code that represents the bank or financial institution itself. It is assigned by the Society for Worldwide Interbank Financial Telecommunication (SWIFT) and uniquely identifies the bank within the global financial network.

2. Country Code: The Country Code is a two-letter code that represents the home country of the bank. It follows the standard ISO 3166-1 alpha-2 country code format. For example, “US” represents the United States, “GB” represents the United Kingdom, and “DE” represents Germany. This code helps in identifying the country where the bank is located.

3. Location Code: The Location Code is also a two-letter code that represents the specific location or branch of the bank within its home country. It could indicate a city or a specific area within a city. For example, “NY” represents New York, “LON” represents London, and “SYD” represents Sydney. This code helps in narrowing down the bank’s location.

4. Branch Code (optional): Some BIC numbers may have an optional three-letter Branch Code. This code helps in identifying a specific branch of a bank within a location. It is not always included in the BIC number, but when present, it provides more specific information about the bank’s branch.

When all the components are combined, the BIC number forms a unique identification code for a bank. For example, a BIC number may appear as: ABCDUS33XXX, where “ABCD” represents the Bank Code, “US” represents the Country Code, “33” represents the Location Code, and “XXX” represents the optional Branch Code.

Understanding the structure of a BIC number is crucial for correctly identifying and communicating with a bank or financial institution during international transactions. It ensures that the funds are directed to the correct bank and branch, minimizing errors and delays.

In the next section, we will explore the difference between BIC numbers and International Bank Account Numbers (IBAN) and their respective roles in banking.

Difference Between BIC and IBAN

While both Bank Identifier Codes (BIC) and International Bank Account Numbers (IBAN) are important components of international banking, they serve different purposes. Here are the key differences between BIC and IBAN:

1. Purpose: BIC: The primary purpose of a BIC (also known as a SWIFT code) is to identify a specific bank or financial institution globally. It ensures accurate and secure communication during international transactions. IBAN: On the other hand, an IBAN is used to identify individual bank accounts within a particular country. It provides standardized account information to facilitate domestic and international fund transfers.

2. Information Encoded: BIC: The BIC code contains information about the bank’s name, location, and branch. It helps in identifying and routing transactions to the correct bank and branch. IBAN: The IBAN, on the other hand, includes information about the specific bank and branch, as well as the customer’s account number.

3. Structure: BIC: The structure of a BIC code consists of a four-letter Bank Code, a two-letter Country Code, a two-letter Location Code, and an optional three-letter Branch Code. IBAN: The structure of an IBAN varies depending on the country but typically includes a two-letter Country Code, two check digits, and a country-specific combination of alphanumeric characters that represent the bank and account details.

4. Usage: BIC: BIC codes are used primarily in international transactions, such as wire transfers, to ensure accurate routing and communication between banks. IBAN: IBANs are used for both domestic and international transactions. They are mandatory within the European Union and some other countries and are required for cross-border payments.

5. Coverage: BIC: BIC codes are globally recognized and used by banks and financial institutions worldwide, regardless of their country of operation. IBAN: IBANs are used mainly in countries that have adopted the IBAN standard. Not all countries use the IBAN system, so its usage can vary.

6. Verification: BIC: BIC codes can be verified using SWIFT’s online directory or by contacting the recipient bank directly. IBAN: IBANs undergo a series of validation checks, including mathematical calculations and country-specific algorithms, to ensure their accuracy and integrity.

While BIC codes and IBANs serve different purposes, they often work together to facilitate secure and efficient international transactions. The BIC code helps identify and route transactions to the correct bank, while the IBAN ensures accurate crediting of funds to the specific account.

In the next section, we will discuss how to find your bank’s BIC number.

How to Find Your Bank’s BIC Number

When conducting international transactions or setting up cross-border payments, it is essential to have the correct Bank Identifier Code (BIC), also known as a SWIFT code, for your bank. Here are some ways to find your bank’s BIC number:

1. Bank’s Website: Visit your bank’s official website and search for the BIC or SWIFT code. Most banks provide this information on their website, either in the “Contact” or “Support” section. Look for any sections related to international banking or wire transfers, as the BIC code is usually mentioned there.

2. Online BIC Directories: Several online directories provide comprehensive BIC information for banks worldwide. One popular directory is SWIFT’s online BIC directory, which allows you to search for BIC codes by bank name, country, or branch location. Other third-party websites specializing in bank codes and identifiers may also provide the information you need.

3. Contact Customer Service: Reach out to your bank’s customer service department for assistance. They can provide you with the correct BIC code for your bank and any additional information you may need. Be sure to have your account details and purpose of the BIC code request ready for verification purposes.

4. Consult Your Bank Statement: Check your bank statement, particularly for international transactions or wire transfers. The BIC code is often included in the transaction details section, helping you identify the specific BIC associated with your bank.

5. Visit the Bank Branch: If all else fails, you can visit your bank’s local branch and inquire about the BIC code in person. The bank staff should be able to assist you and provide the necessary information.

It is important to ensure that you have the most up-to-date and accurate BIC number for your bank. BIC codes can change over time, especially if banks go through mergers, acquisitions, or rebranding. Double-check the validity of the BIC number before initiating any international transactions.

Having the correct BIC number is crucial for the smooth processing of international transactions, avoiding delays or misdirected funds. Take the time to verify and obtain the accurate BIC code for your bank to ensure seamless cross-border banking activities.

In the next section, we will discuss the importance of BIC numbers in international transactions.

Importance of BIC Numbers in International Transactions

BIC numbers, also known as Bank Identifier Codes or SWIFT codes, play a crucial role in facilitating smooth and secure international transactions. Here are some key reasons why BIC numbers are essential in international banking:

1. Accurate Identification of Banks: BIC numbers ensure accurate identification of banks and financial institutions involved in international transactions. They provide a standardized code that uniquely identifies each bank, minimizing the risk of errors or confusion in the transfer of funds.

2. Secure Communication: BIC numbers enable secure communication between banks during international transactions. By including the BIC code in transaction messages, banks can verify the authenticity of the sender and ensure that the communication is authorized, preventing fraud and unauthorized access.

3. Routing of Funds: BIC numbers are crucial for routing funds to the correct bank and branch. When initiating an international payment or wire transfer, the sender includes the recipient’s BIC code to ensure that the funds are directed accurately, avoiding delays and misdirected transfers.

4. Compliance with International Standards: BIC numbers are part of the SWIFT network, which is a globally recognized standard for financial messaging. Using BIC codes ensures that banks adhere to international standards and protocols, promoting consistency and interoperability in cross-border transactions.

5. Verification of Bank Details: BIC numbers provide a reliable way to verify the authenticity of bank details. Individuals and businesses can cross-check BIC codes to ensure they are dealing with legitimate and authorized financial institutions, reducing the risk of scams or fraudulent activities.

6. Integration with International Payment Systems: BIC numbers are essential for the smooth functioning of international payment systems. They enable interoperability between banks and facilitate the transfer of funds across borders, supporting global trade, investments, and financial activities.

7. Transparency and Tracking: BIC numbers help maintain transparency and tracking of international transactions. They provide a unique identifier that can be used to trace the flow of funds, supporting regulatory compliance, and audit requirements.

Overall, BIC numbers are of utmost importance in international transactions, ensuring accurate identification of banks, secure communication, and efficient routing of funds. They are an essential component of the global financial infrastructure, promoting trust, reliability, and transparency in cross-border banking activities.

In the next section, we will discuss the benefits of using BIC numbers in banking.

Benefits of Using BIC Numbers in Banking

BIC numbers, also known as Bank Identifier Codes or SWIFT codes, provide several benefits when it comes to conducting international transactions and cross-border banking. Here are some key advantages of using BIC numbers:

1. Accurate and Efficient Transactions: By including the correct BIC number in international transactions, banks can ensure accurate and efficient routing of funds. This minimizes errors, delays, and the risk of funds being sent to the wrong recipient.

2. Secure Communication: BIC codes play a vital role in secure communication between financial institutions during international transactions. Banks can verify and authenticate messages by validating the BIC code, ensuring that only authorized parties can access sensitive financial information.

3. Global Standardization: BIC numbers follow a standardized format recognized globally. Using BIC codes promotes consistency and uniformity in international banking, enabling seamless communication and cooperation between banks across countries and regions.

4. Verification of Bank Authenticity: BIC numbers provide a reliable means of verifying the authenticity of banks and financial institutions. Individuals and businesses can cross-check BIC codes to ensure they are dealing with legitimate and authorized entities before initiating international transactions.

5. Efficient International Payments: BIC numbers are crucial for processing international payments and wire transfers. They ensure that funds are routed correctly to the intended recipient’s bank, facilitating timely and accurate crediting of funds.

6. Compliance with Regulatory Requirements: BIC numbers play a role in regulatory compliance, such as anti-money laundering (AML) and know-your-customer (KYC) regulations. By using BIC codes, banks can maintain accurate records and fulfill their obligations in preventing financial crimes.

7. Seamless Integration with International Networks: BIC numbers are an integral part of the global SWIFT network. By using BIC codes, banks can seamlessly integrate into this network and benefit from the extensive connectivity it offers, enabling efficient and secure international financial transactions.

8. Enhanced Transparency and Tracking: BIC numbers provide a unique identifier for each bank, allowing for enhanced transparency and tracking of international transactions. This promotes accountability, auditability, and compliance with reporting requirements.

Overall, the use of BIC numbers in banking offers numerous benefits, including accurate and efficient transactions, secure communication, global standardization, enhanced verification of bank authenticity, compliance with regulations, seamless integration with international networks, and improved transparency and tracking capabilities.

In the next section, we will address some common FAQs about BIC numbers to provide further clarity.

Common FAQs about BIC Numbers

Here are some frequently asked questions about Bank Identifier Codes (BIC), also known as SWIFT codes:

1. What is the difference between BIC and SWIFT code?

The terms BIC and SWIFT code are used interchangeably and refer to the same concept. BIC stands for Bank Identifier Code, while SWIFT stands for Society for Worldwide Interbank Financial Telecommunication, the organization responsible for assigning BIC codes to banks.

2. Are BIC numbers the same for all branches of a bank?

No, the Bank Code and the Location Code of a BIC number are the same for all branches of a particular bank. However, the optional Branch Code may differ between branches, allowing for identification of specific branches within a location.

3. Can I use any bank’s BIC number for international transactions?

No, you should use the BIC number specific to the bank you are conducting the transaction with. Using the correct BIC ensures that the funds are directed to the correct recipient bank and branch.

4. What if I don’t have a BIC number for a specific bank?

If you don’t have the BIC number for a specific bank, there are several options. You can visit the bank’s website, contact their customer service, consult your bank statement for past international transactions involving that bank, or check online BIC directories.

5. Can a BIC number be used to identify an individual account?

No, a BIC number is used to identify the bank or financial institution, not individual accounts. To identify a specific bank account, you would need the appropriate account number or International Bank Account Number (IBAN).

6. Are BIC numbers required for domestic transactions?

No, BIC numbers are primarily used for international transactions. For domestic transactions, banks usually rely on other identification methods, such as routing numbers or internal codes specific to the country’s banking system.

7. What is the length of a BIC number?

A standard BIC number consists of either 8 or 11 characters, depending on whether or not a Branch Code is included. However, some countries may have variations in BIC length, so it’s essential to consult the specific BIC format for the corresponding country or bank.

These are some common questions regarding BIC numbers. Understanding how BIC codes work and their significance in international transactions can help ensure smooth and accurate cross-border banking activities.

Now that we have addressed common FAQs, let’s summarize the key points before concluding.

Conclusion

Bank Identifier Codes (BIC), also known as SWIFT codes, are essential in international banking for accurate identification, secure communication, and seamless transactions. BIC numbers serve as unique identification codes for banks and financial institutions globally, ensuring the efficient routing of funds and adherence to international standards.

In this article, we discussed the purpose and structure of BIC numbers, as well as their significance in international transactions. BIC numbers play a crucial role in secure communication, accurate routing of funds, compliance with regulatory requirements, and verification of bank authenticity. They enable efficient international payments, integration with global networks, and enhanced transparency and tracking capabilities. Together with International Bank Account Numbers (IBAN), BIC numbers facilitate smooth cross-border banking activities.

When conducting international transactions, it is important to have the correct BIC number for your bank. You can find this information on your bank’s website, through online directories, by contacting customer service, or by checking your bank statement. Using the accurate BIC number ensures that your funds are transferred to the intended recipient smoothly and securely.

Understanding the importance of BIC numbers and how they are used in banking can help individuals and businesses navigate the complexities of international transactions. Whether you are sending or receiving funds across borders, having the correct BIC number is crucial for seamless cross-border banking activities.

By adhering to the standardized structure and utilizing BIC numbers correctly, banks and individuals can ensure efficient communication, accurate routing, and secure transactions in the global financial landscape.