What is a Banking Swift Code?

A banking Swift code, also known as a Bank Identifier Code (BIC), is a unique alphanumeric code that is used to identify a specific bank during international transactions. Swift codes are widely used in the banking industry and play a crucial role in facilitating secure and efficient money transfers between banks globally.

The Swift code is used to identify not only the bank but also the specific branch of the institution. It consists of a combination of letters and numbers that provide essential information about the bank, such as its country, city, and branch. This standardized code ensures accuracy and reduces the risk of errors when processing international transactions.

With the ever-increasing globalization of the financial sector, Swift codes have become a vital component of international banking. They enable banks from different countries to communicate and transfer funds securely, ensuring that the money reaches the intended recipient in a timely manner.

Each bank has its own unique Swift code, which is assigned by the Society for Worldwide Interbank Financial Telecommunication (SWIFT) network. SWIFT is a global cooperative organization that oversees the messaging system used by banks for cross-border transactions.

It is important to note that Swift codes are not the same as International Bank Account Numbers (IBANs). While Swift codes identify the bank, IBANs serve as a standardized format for identifying individual bank accounts. Both codes work together to facilitate smooth international transactions, ensuring that funds are routed correctly.

In summary, a banking Swift code is a unique identifier that allows international banks to communicate and transfer funds securely. It plays a vital role in ensuring the accuracy and efficiency of cross-border transactions, making it an invaluable tool for the global banking industry.

Understanding the Basics

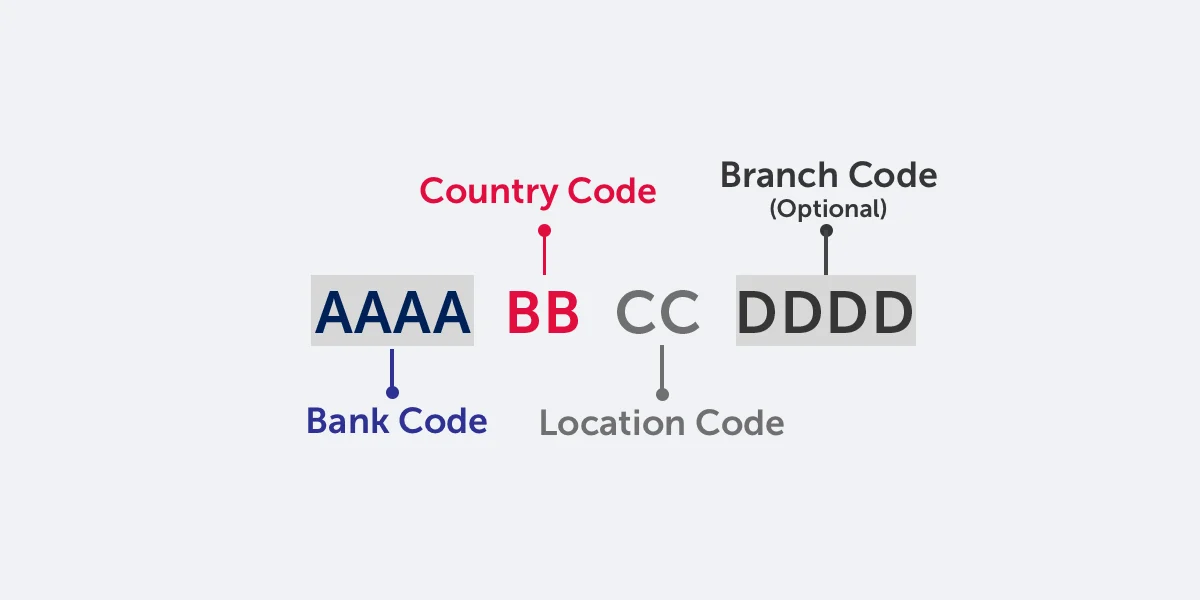

To comprehend the significance of a banking Swift code, it is important to understand its basic elements and structure. A Swift code consists of either 8 or 11 characters, divided into four components: bank code, country code, location code, and branch code.

The first four characters represent the bank code, which is unique to each financial institution. This code is assigned by the SWIFT network and helps identify the exact bank involved in the transaction. It is important to note that some banks have multiple Swift codes to distinguish between different branches or divisions.

The next two characters represent the country code and indicate the country in which the bank is located. These two letters are based on the International Organization for Standardization (ISO) 3166-1 alpha-2 country codes. For example, “US” represents the United States, while “GB” represents the United Kingdom.

The following two characters represent the location code, which provides information about the bank’s city or region. This helps further pinpoint the exact location of the bank within a specific country. The location code is also based on the ISO 3166-1 alpha-2 country codes.

If the Swift code is 11 characters long, the last three characters represent the branch code. This code provides additional details regarding the specific branch of the bank. However, not all banks use this three-letter branch code, as some may only have an 8-character Swift code.

When initiating an international transfer, it is crucial to provide the correct Swift code to ensure the funds are correctly routed to the intended recipient. A minor error in the Swift code can lead to delays or even the failure of the transaction. It is therefore important to verify the Swift code with the bank or recipient before making any international transfers.

In summary, a banking Swift code consists of a bank code, country code, location code, and branch code (if applicable). Understanding these basic elements is essential for accurately identifying the recipient bank during international transfers.

How Does a Swift Code Work?

A Swift code functions as a unique identifier for banks during international transactions. It serves as a communication tool between financial institutions, ensuring that funds are transferred securely and accurately.

When initiating an international transfer, the sender’s bank uses the Swift code to identify the recipient’s bank. The Swift code is included in the transfer instructions and acts as a routing number, directing the funds to the correct bank and branch.

Once the sender’s bank has the Swift code, it uses the SWIFT network to send the transfer instructions to the recipient’s bank. The SWIFT network acts as a secure messaging system that facilitates the exchange of information between banks worldwide.

Upon receiving the transfer instructions, the recipient’s bank uses the Swift code to identify the correct branch or division where the funds should be credited. This ensures that the money reaches the intended recipient’s account without any delays or errors.

It is important to note that Swift codes are used primarily for international transfers and do not apply to domestic payments within a country. For domestic transfers, local systems such as Automated Clearing House (ACH) or National Electronic Fund Transfer (NEFT) are used.

Swift codes are also instrumental in providing transparency and accountability in the international banking system. As Swift codes are unique to each bank, they enable regulators and auditors to track and monitor cross-border transactions, ensuring compliance with relevant laws and regulations.

Furthermore, Swift codes play a vital role in reducing errors and facilitating faster transfer processing. By using a standardized and universally recognized code, banks can streamline their operations and minimize the risk of funds being misdirected or delayed.

In summary, a banking Swift code acts as a routing number, ensuring that international transfers are directed to the correct bank and branch. It serves as a vital communication tool between financial institutions, facilitating secure and efficient money transfers globally.

Why Do Banks Use Swift Codes?

Banks use Swift codes for several reasons, primarily to ensure the smooth and secure processing of international transactions. Let’s explore the key reasons why banks rely on Swift codes:

1. Identification: Swift codes provide a unique identifier for each bank and its branches. This helps banks accurately identify the recipient bank during international transfers, reducing the risk of errors and ensuring that funds are routed to the correct account.

2. Standardization: Swift codes follow a standardized format, making them universally recognizable and accepted by banks worldwide. This standardization streamlines the processing of international transfers and promotes consistency in the global banking system.

3. Efficiency: By using Swift codes, banks can expedite the transfer process, as the code contains essential information about the recipient bank. This reduces the need for manual intervention, minimizes processing time, and improves overall efficiency.

4. Compliance: Swift codes facilitate compliance with regulatory requirements. As banks are required to report cross-border transactions to regulatory authorities, the use of Swift codes enables efficient tracking and monitoring of these transactions, ensuring compliance with anti-money laundering (AML) and know your customer (KYC) regulations.

5. Global Reach: Swift codes allow banks to connect and communicate with financial institutions worldwide. They enable seamless transfer of funds across borders, ensuring that banking services are accessible globally and fostering international trade and commerce.

6. Accuracy: Using Swift codes reduces the risk of errors during international transfers. Banks can rely on the standardized code to ensure that the funds reach the correct recipient without delays or misrouting, enhancing the overall reliability and accuracy of cross-border transactions.

In summary, banks utilize Swift codes to enhance the efficiency, accuracy, and security of international transactions. These codes provide a unique identification system, streamline the transfer process, promote compliance with regulations, and enable seamless global connectivity among financial institutions.

How to Find a Bank’s Swift Code?

Locating a bank’s Swift code is essential when initiating international transfers. Here are several ways to find a bank’s Swift code:

1. Bank’s Website: The most reliable and convenient way to find a bank’s Swift code is by visiting their official website. Most banks provide this information on their website, often under the “Contact” or “International Services” section. Look for a page specifically dedicated to Swift codes or international wire transfers.

2. Online Swift Code Directories: Numerous online directories specialize in providing Swift codes for various banks worldwide. These directories allow you to search for a specific bank and retrieve its Swift code instantly. Examples of such directories include swiftcodes.org, theswiftcodes.com, and bank-codes.com.

3. Contacting the Bank: If you’re unable to find the Swift code online, contacting the bank’s customer service or international banking department is another option. They will be able to provide you with the correct Swift code for the specific branch or division you need.

4. Mobile Banking App: Many banks offer mobile banking apps that provide access to account information, transfer services, and international payment details. Check the app’s functionalities to see if it includes a Swift code lookup feature.

5. Consultation with a Bank Representative: If you have a personal relationship with a bank representative or financial advisor, they can assist you in finding the Swift code. They have access to internal resources and can provide accurate and up-to-date information.

When searching for a bank’s Swift code, ensure that you have the correct details, such as the bank’s name, branch, and country. Swift codes can vary based on these factors, so being specific will help you find the accurate code.

It is crucial to verify the Swift code provided by any source to avoid errors. Inaccurate or outdated Swift codes can result in delays or misrouting of funds. Always double-check the Swift code with the bank or recipient before initiating an international transfer.

In summary, finding a bank’s Swift code can be done through various methods, including checking the bank’s website, using online directories, contacting the bank directly, utilizing mobile banking apps, or consulting with a bank representative. Always ensure the accuracy of the Swift code to facilitate seamless international transfers.

Common Mistakes to Avoid When Using a Swift Code

When using a Swift code for international transactions, it is crucial to be mindful of common mistakes to ensure a smooth and successful transfer. Here are some key mistakes to avoid:

1. Incorrect Swift Code: One of the most common errors is entering an incorrect Swift code. Even a single incorrect character can lead to misrouting or failure of the transaction. Always double-check and verify the Swift code with the recipient or their bank to ensure accuracy.

2. Outdated Swift Code: Swift codes can change over time due to mergers, acquisitions, or rebranding. Using an outdated Swift code can result in delays or rejection of the transfer. Regularly update your records or confirm with the recipient’s bank to ensure you have the most up-to-date Swift code.

3. Confusing Swift Code with IBAN: Swift codes and International Bank Account Numbers (IBANs) serve different purposes. Some people make the mistake of using a Swift code where an IBAN is required, or vice versa. Understand the specific requirements of the transfer and provide the correct code accordingly.

4. Ignoring Branch Code: In cases where a bank has multiple branches, including the branch code in the Swift code is crucial. Ignoring or omitting the branch code can result in the funds being misdirected to the wrong branch. Ensure you have the correct Swift code, including the branch code if applicable.

5. Lack of Verification: Failing to verify the Swift code before initiating the transfer can be a costly mistake. Always confirm the accuracy of the Swift code directly with the recipient or their bank to avoid any errors or delays.

6. Assuming Universal Swift Codes: Although Swift codes are widely used, not all banks have the same code for all their branches. It is essential to remember that each branch might have a unique Swift code. Do not assume that a single Swift code applies to all branches of a bank.

7. Neglecting to Include Additional Information: Some international transfers require additional information along with the Swift code, such as the recipient’s account number or reference. Neglecting to provide the required details can lead to processing delays or rejection of the transfer. Review the transfer instructions carefully and include all necessary information.

By avoiding these common mistakes, you can ensure that your international transfers are processed accurately and efficiently, minimizing the risk of delays or errors.

In summary, being aware of the potential mistakes when using a Swift code is crucial. Double-checking the accuracy of the code, keeping it up-to-date, understanding the specific requirements of the transfer, and verifying all necessary information can contribute to successful and error-free international transactions.

Alternatives to Swift Codes

While Swift codes have been the traditional method for identifying banks during international transactions, several alternative systems have emerged in recent years. These alternatives aim to provide faster, more efficient, and cost-effective solutions for cross-border transfers. Here are a few notable alternatives to Swift codes:

1. Ripple (XRP): Ripple utilizes a digital payment protocol and cryptocurrency called XRP. It offers real-time gross settlement, low fees, and instantaneous cross-border transfers. Ripple’s network enables banks and financial institutions to connect directly, eliminating the need for intermediaries and reducing transaction costs.

2. TransferWise: TransferWise is a peer-to-peer money transfer service that utilizes local bank accounts to facilitate international transfers. It offers competitive exchange rates and transparent fees, making it a popular alternative to traditional banks. TransferWise operates in multiple currencies and often provides transfers at a fraction of the cost charged by banks.

3. Blockchain Technology: Blockchain technology, the foundation of cryptocurrencies like Bitcoin and Ethereum, is increasingly being used for cross-border transfers. Blockchain offers decentralization, transparency, and enhanced security, eliminating the need for intermediaries like banks. Startups and financial institutions are exploring the potential of blockchain to revolutionize the international payments industry.

4. International Bank Account Numbers (IBANs): While IBANs are not direct alternatives to Swift codes, they are often used in conjunction with Swift codes to ensure accurate identification of individual bank accounts. IBANs are standardized formats that help identify individual bank accounts within specific countries, making international bank transfers more efficient and accurate.

5. Central Bank-led Payment Systems: Some countries have developed central bank-led payment systems to streamline domestic and cross-border transfers. For example, the Eurozone has the Single Euro Payments Area (SEPA) system, which allows for quick and low-cost Euro transfers within member countries.

6. Payment Service Providers (PSPs): Payment service providers like PayPal and Payoneer offer online payment solutions that allow businesses and individuals to send and receive money across borders. These services often offer convenience, quick transfers, and competitive exchange rates.

While these alternatives continue to gain traction, Swift codes remain the most widely used method of identifying banks in international transactions. However, as technology advances and financial systems evolve, these alternatives have the potential to provide more efficient and cost-effective solutions for cross-border transfers.

In summary, several alternatives to traditional Swift codes have emerged, including Ripple, TransferWise, blockchain technology, IBANs, central bank-led payment systems, and payment service providers. These alternatives offer faster, more cost-effective, and technologically advanced solutions for international transfers, transforming the global payments landscape.

Conclusion

Banking Swift codes are essential in facilitating secure and efficient international transactions. They serve as unique identifiers for banks and their branches, allowing for accurate routing of funds across borders. With their standardized format, Swift codes provide a universal language for communication between financial institutions worldwide.

Understanding the basics of Swift codes, including their structure and purpose, is crucial for both individuals and businesses engaged in cross-border transactions. By ensuring the accuracy of Swift codes and avoiding common mistakes, such as entering incorrect codes or neglecting branch codes, one can minimize the risk of errors and delays in international transfers.

Although Swift codes have long been the standard in the global banking industry, alternative systems have emerged in recent years. Technologies like blockchain, digital payment protocols, and payment service providers offer novel ways to make international transfers faster, cheaper, and more secure. These alternatives are challenging the traditional banking system and providing innovative solutions for global financial transactions.

However, despite the emergence of these alternatives, Swift codes remain the predominant method for identifying banks during international transfers. Their widespread adoption, standardization, and compatibility make them crucial in ensuring reliable and accurate cross-border funds transfer.

In conclusion, banking Swift codes are integral to the international banking system. They play a vital role in ensuring the smooth processing of cross-border transactions, providing transparency and efficiency. While alternative systems may offer new possibilities, Swift codes continue to be the primary method for identifying banks and branches during international transfers. Staying informed about Swift codes and their proper usage is essential for individuals and businesses involved in global finance.