Introduction

The world of banking and financial transactions can sometimes be confusing, with various acronyms and terms that are unfamiliar to many people. One such term is ACH credit. If you’ve ever come across this term and wondered what it means, you’re in the right place. In this article, we’ll explore the definition, workings, benefits, drawbacks, and examples of ACH credit transactions.

ACH, or Automated Clearing House, is an electronic network used for financial transactions in the United States. It allows for the transfer of funds between different banks or financial institutions seamlessly and efficiently. ACH credit refers to a transaction where funds are electronically deposited into a recipient’s account. This can include various types of payments, such as direct deposits, payroll payments, vendor payments, and tax refunds.

ACH credit works by utilizing the ACH network to transfer funds from the sender’s account to the recipient’s account. The sender initiates the transaction, usually through their bank or a third-party payment processor. The necessary information, such as the recipient’s account number and bank routing number, is provided to ensure accurate delivery.

What is ACH Credit?

ACH credit is a type of electronic payment that allows funds to be electronically deposited into a recipient’s bank account. ACH, which stands for Automated Clearing House, is a network that enables the transfer of funds between different banks or financial institutions.

In an ACH credit transaction, the sender initiates the payment and authorizes their bank or a third-party payment processor to transfer the funds to the recipient’s account. This can be done for various purposes, such as direct deposits, payroll payments, vendor payments, tax refunds, and more.

ACH credit transactions offer a convenient and efficient way to transfer funds, eliminating the need for physical checks or cash. Instead, the transaction takes place electronically, allowing for faster processing times and reducing the risk of loss or theft associated with paper-based payments.

One of the key elements of an ACH credit transaction is the use of the recipient’s bank account information, including the account number and bank routing number. This information ensures that the funds are deposited into the correct recipient’s account.

It’s important to note that ACH credit transactions can be one-time payments or recurring payments, depending on the nature of the transaction. For example, an employer may use ACH credit to deposit employees’ salaries directly into their bank accounts on a regular basis.

It’s worth mentioning that ACH credit transactions are subject to certain rules and regulations to ensure the security and integrity of the system. These rules govern the process of initiating, verifying, and approving ACH transactions, providing a level of protection for both the sender and the recipient.

In the next section, we’ll delve into how ACH credit transactions work and their benefits in more detail.

How Does ACH Credit Work?

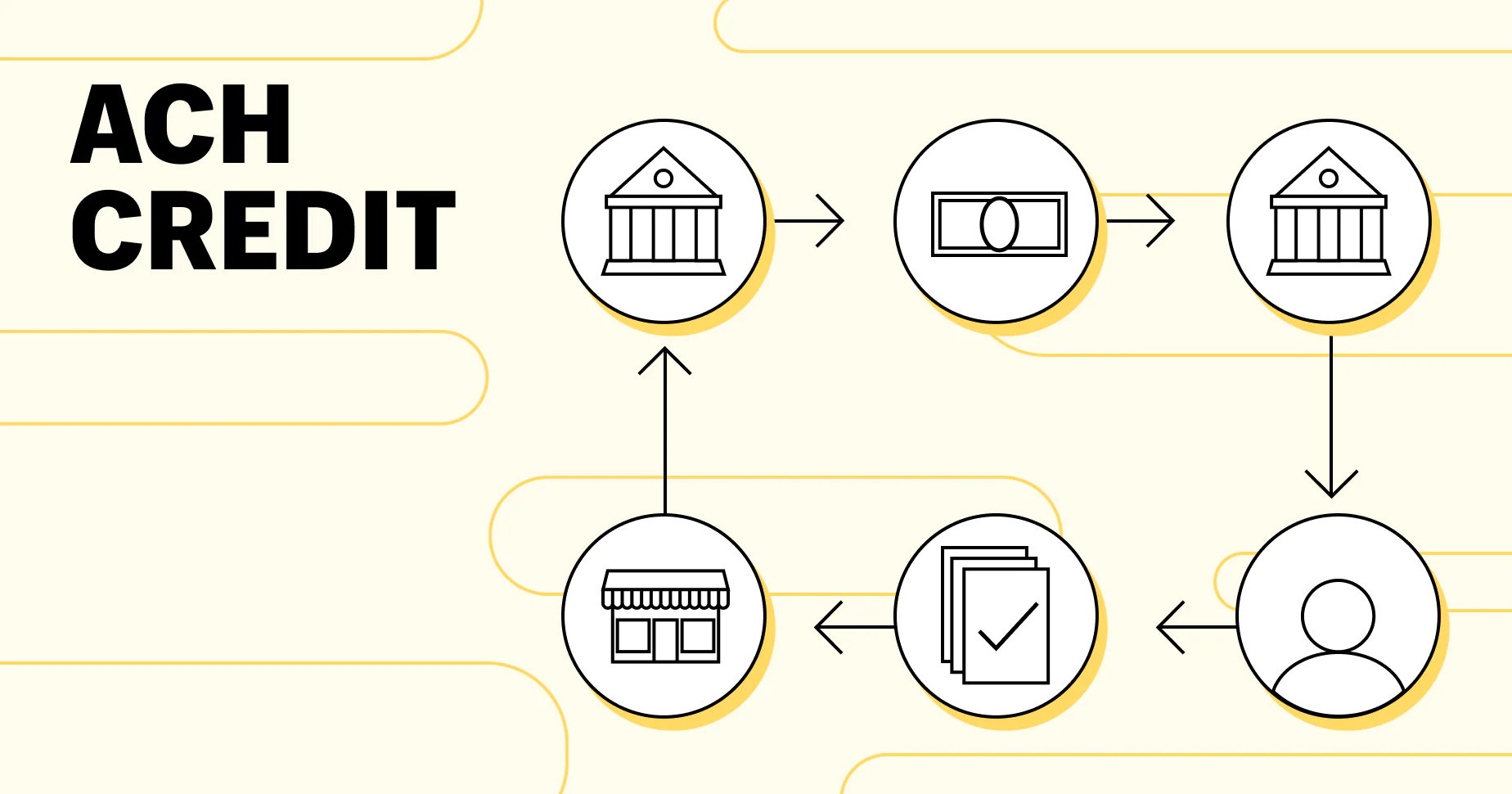

ACH credit transactions involve a series of steps that facilitate the transfer of funds from the sender to the recipient. Let’s take a closer look at how ACH credit works:

- The sender initiates the ACH credit transaction by providing their bank or a third-party payment processor with the necessary information, including the recipient’s bank account number and routing number.

- The sender’s financial institution or payment processor verifies the information provided and ensures that the sender has sufficient funds to cover the transaction.

- Once the verification is complete, the sender’s bank debits the funds from the sender’s account and initiates the transfer using the ACH network.

- The ACH network then processes the transaction and routes it to the recipient’s bank.

- The recipient’s bank receives the funds and credits them to the recipient’s account.

- The recipient can access the funds in their account, either by withdrawing cash, making purchases, or transferring the funds to another account.

It’s important to note that ACH credit transactions are not instantaneous. The timing of the transfer depends on various factors, including the processing times of the sender’s and recipient’s banks. Typically, ACH credit transactions are completed within a few business days, although it can vary.

ACH credit transactions offer several benefits to both the sender and the recipient, which we’ll explore in the next section.

Benefits of ACH Credit

ACH credit transactions provide numerous advantages for both the sender and the recipient. Let’s explore some of the key benefits:

- Efficiency: ACH credit transactions offer a more efficient way to transfer funds compared to traditional methods like writing and mailing physical checks. The funds are electronically deposited into the recipient’s bank account, eliminating the need for manual processing and reducing the risk of errors.

- Cost Savings: ACH credit transactions are typically more cost-effective than other payment methods. They often involve lower fees and eliminate expenses associated with paper checks, such as printing, postage, and check processing fees.

- Security: ACH credit transactions provide a secure way to transfer funds. By eliminating the use of physical checks, which can be lost or stolen, the risk of fraudulent activity is reduced. Additionally, ACH transactions are subject to strict regulations and encryption protocols, ensuring the safety of sensitive financial information.

- Convenience: Both the sender and the recipient benefit from the convenience of ACH credit transactions. For the sender, there is no need to write and mail checks or visit a bank. The recipient enjoys the ease of receiving funds directly into their bank account, without the hassle of depositing physical checks.

- Timely Payments: ACH credit transactions can be processed quickly, ensuring timely payments. This is particularly beneficial for recurring payments, such as employee salaries or monthly bill payments, where funds need to be transferred on a regular basis.

- Recordkeeping: ACH credit transactions provide a digital record of the payment, making it easier for both parties to track and reconcile transactions. This simplifies accounting processes and reduces paperwork.

Overall, ACH credit transactions offer a secure, efficient, and cost-effective method of transferring funds, benefiting both the sender and the recipient. In the next section, we’ll discuss some of the potential drawbacks of ACH credit.

Drawbacks of ACH Credit

While ACH credit transactions offer numerous benefits, there are also a few drawbacks to consider:

- Processing Time: ACH credit transactions are not instantaneous and can take a few business days to complete. This delay may not be suitable for time-sensitive transactions or situations where immediate access to funds is necessary.

- Reversal Limitations: Once an ACH credit transaction is initiated, it can be challenging to reverse or cancel the payment. This lack of flexibility can be problematic if the need for a refund or reversal arises.

- Authorization Disputes: In some cases, disputes may arise regarding the authorization of an ACH credit transaction. This can lead to delays in resolving the issue and potentially impacting the relationship between the sender and the recipient.

- Fee Structure: While ACH credit transactions typically have lower fees compared to other payment methods, some financial institutions may still charge a fee for initiating or receiving ACH credits. It’s important to be aware of any applicable fees when engaging in such transactions.

- Technology Reliance: ACH credit transactions rely heavily on technology and the availability of electronic systems. Technical issues or system outages can impact the processing and timing of the transaction, causing disruptions or delays.

- Security Considerations: While ACH credit transactions are generally secure, there is still a risk of unauthorized access or fraud. It is crucial for both the sender and the recipient to maintain strong security practices, such as secure online banking and protection of account information.

Despite these drawbacks, ACH credit transactions remain a popular and widely-used method for transferring funds due to their convenience and efficiency. In the next section, we’ll provide some examples of common ACH credit transactions to further illustrate their usage.

Examples of ACH Credit Transactions

ACH credit transactions are used for a variety of purposes and can be found in various aspects of our daily lives. Here are some examples of common ACH credit transactions:

- Direct Deposits: Many individuals receive their salaries through direct deposit. Employers use ACH credit to deposit employees’ wages directly into their bank accounts, eliminating the need for paper checks.

- Vendor Payments: Businesses often make vendor payments using ACH credit. This can include payments to suppliers, contractors, or service providers, streamlining the payment process and improving cash flow management.

- Tax Refunds: When individuals file their tax returns and are entitled to a refund, the funds are often transferred through ACH credit. This allows for faster and more efficient delivery of tax refunds.

- Online Bill Payments: Many individuals and businesses opt for online bill payment, where funds are electronically transferred to pay bills such as utilities, rent, mortgage, and credit card payments.

- Charitable Donations: Nonprofit organizations often accept donations through ACH credit. This enables donors to contribute funds conveniently and securely, supporting various causes.

- Government Benefits: Government agencies use ACH credit to disburse benefits such as social security, retirement pensions, veterans’ benefits, and unemployment payments to eligible recipients.

- Expense Reimbursements: Companies may use ACH credit to reimburse employees for business-related expenses, such as travel expenses or employee reimbursements.

- Loan Payments: Borrowers often set up ACH credit transactions for loan payments, allowing automatic deduction of loan installments from their bank accounts on specific dates.

These examples demonstrate the wide-ranging applications of ACH credit transactions across different industries and sectors. While each transaction serves a specific purpose, they all utilize the ACH network to facilitate efficient and secure fund transfers.

Next, we’ll explore the difference between ACH credit and ACH debit transactions.

ACH Credit vs. ACH Debit

While both ACH credit and ACH debit are electronic payment methods that utilize the ACH network, there are some key differences between the two:

- Direction of Funds: ACH credit transactions move funds in the direction of the recipient, where funds are deposited into their account. On the other hand, ACH debit transactions move funds in the direction of the sender, where funds are withdrawn from the sender’s account to make a payment.

- Initiator of the Transaction: In ACH credit transactions, the sender initiates the payment, authorizing the transfer of funds to the recipient. With ACH debit transactions, the recipient or payee usually initiates the transaction, seeking authorization to withdraw funds from the sender’s account.

- Authorization Requirements: ACH credit transactions typically require the explicit consent and authorization of the sender. The sender needs to provide the recipient’s bank account and routing number, along with their own bank account information. ACH debit transactions, on the other hand, usually require the sender to provide their bank account details to the recipient or payee, allowing them to initiate the withdrawal.

- Use Cases: ACH credit transactions are commonly used for direct deposits, payroll payments, vendor payments, and reimbursements. ACH debit transactions are often used for bill payments, loan repayments, insurance premiums, and subscription payments.

- Risk and Liability: With ACH credit transactions, the sender has more control over the transfer of funds, as they initiate the payment and provide the necessary information. However, with ACH debit transactions, the risk and liability may be higher for the sender, as they authorize the recipient to withdraw funds directly from their account.

It’s important to note that both ACH credit and ACH debit transactions offer benefits in terms of security, efficiency, and convenience, depending on the specific use case and individual preferences.

In the next section, we’ll discuss how to initiate an ACH credit transaction.

How to Initiate an ACH Credit

Initiating an ACH credit transaction is a relatively straightforward process. Here are the general steps to follow:

- Ensure Authorization: Obtain proper authorization from the recipient to transfer funds into their bank account. This may involve obtaining their bank account information, such as the account number and routing number.

- Select Method of Initiation: Determine how you want to initiate the ACH credit transaction. You can choose to work directly with your bank, utilize a third-party payment processor, or leverage online banking services offered by financial institutions.

- Gather Information: Collect the necessary information for the ACH credit transaction, including the recipient’s bank account and routing numbers, as well as your own account details.

- Complete Transaction Details: Provide the required information, such as the amount to be transferred, the purpose of the payment, and any additional details requested by your bank or payment processor.

- Submit Request: Submit the ACH credit request to your bank or payment processor. This can typically be done online through a secure portal or by contacting the relevant department or representative directly.

- Verification and Processing: Your bank or payment processor will verify the transaction details, including the accuracy of the recipient’s banking information and the availability of funds in your account. Once verified, the ACH credit transaction will be processed and initiated.

- Confirmation and Recordkeeping: After the ACH credit transaction has been processed, you will receive confirmation, either through an online notification or a receipt provided by your bank or payment processor. It’s important to keep a record of the transaction for future reference or accounting purposes.

It’s worth noting that the exact process and requirements may vary depending on your bank or payment processor. It’s advisable to consult with your financial institution or refer to their documentation for specific guidelines on initiating ACH credit transactions.

In the next section, we’ll discuss the security aspects of ACH credit transactions.

ACH Credit Security

Security is a crucial aspect of ACH credit transactions to ensure the protection of sensitive financial information and prevent unauthorized access or fraudulent activity. Here are some key measures and considerations regarding ACH credit security:

- Encryption and Secure Communication: Financial institutions and payment processors utilize encryption protocols, such as Secure Socket Layer (SSL) or Transport Layer Security (TLS), to secure the transmission of data during ACH credit transactions. This ensures that the information exchanged between parties is protected from interception.

- Authentication and Authorization: ACH credit transactions require proper authentication and authorization to ensure that only authorized individuals or entities can initiate and process transactions. This can involve the use of secure login credentials, multi-factor authentication, and personalized security questions.

- Verification and Validation: Financial institutions and payment processors have mechanisms in place to verify and validate the accuracy and legitimacy of ACH credit transactions. This includes verifying account information, confirming sufficient funds, and reviewing transaction details for potential red flags or suspicious activity.

- Regulatory Compliance: ACH credit transactions are subject to various rules and regulations set forth by regulatory bodies such as the National Automated Clearing House Association (NACHA). These regulations ensure the integrity of the ACH network and promote secure and reliable transactions.

- Education and Awareness: It’s important for both senders and recipients of ACH credit transactions to stay informed and educated about security best practices. This includes safeguarding personal banking information, regularly monitoring account activity, and being cautious of phishing attempts or fraudulent communication.

- Dispute Resolution: In the event of unauthorized or fraudulent ACH credit transactions, it’s vital to have processes in place for dispute resolution. Financial institutions provide mechanisms for reporting and investigating such incidents, potentially leading to the reversal or resolution of fraudulent transactions.

By adhering to these security measures and practices, individuals and organizations can mitigate the risk associated with ACH credit transactions and ensure the safe and reliable transfer of funds.

In summary, ACH credit transactions provide a secure and efficient method of transferring funds. However, it’s essential for both senders and recipients to remain vigilant and proactive in maintaining the security of their financial information.

Conclusion

ACH credit transactions have revolutionized the way funds are transferred in the banking industry. By leveraging the Automated Clearing House network, individuals and businesses can enjoy the benefits of secure, efficient, and cost-effective electronic payments.

In this article, we explored the concept of ACH credit and how it works. We discussed the advantages of using ACH credit, such as improved efficiency, cost savings, security, convenience, timely payments, and streamlined recordkeeping. Alongside the benefits, we also discussed some drawbacks, including processing times, limited reversibility, and potential fees.

We compared ACH credit and ACH debit transactions, highlighting the differences in direction of funds, initiation processes, authorization requirements, and use cases. We also provided insights into how to initiate an ACH credit transaction, emphasizing the importance of proper authorization and accurate information.

Security considerations were addressed, with a focus on encryption, authentication, verification, regulatory compliance, and education. By adhering to these security measures, individuals and businesses can mitigate the risks associated with ACH credit transactions.

In conclusion, ACH credit transactions have transformed the way we handle payments, offering a secure, efficient, and cost-effective alternative to traditional payment methods. Whether it’s receiving salaries, paying vendors, or making charitable donations, ACH credit transactions provide convenience and peace of mind. By understanding how ACH credit works and following best practices, individuals and businesses can harness the benefits of this electronic payment method.