Introduction

Welcome to the world of Open Banking, where technology and innovation are reshaping the financial industry. In this digital age, traditional banking methods are giving way to a more connected and streamlined approach. At the heart of this transformation is the use of Application Programming Interfaces (APIs) – a key component of Open Banking.

APIs have revolutionized the way businesses and consumers interact with financial services, allowing for seamless integration and data sharing between various applications. In the realm of Open Banking, APIs play a crucial role in granting secure access to financial information, facilitating transactions, and driving innovation.

By leveraging APIs, banks and financial institutions can offer a wide range of services and products to their customers, while also creating opportunities for third-party developers to build innovative applications on top of their infrastructure. This democratization of banking services has the potential to enhance customer experiences, foster competition, and drive financial inclusion.

However, understanding the intricacies of APIs and their role in Open Banking requires a closer look at the concept itself. In this article, we will explore what Open Banking is, delve into the world of APIs, and understand how they work in the context of Open Banking. We will also examine the benefits and challenges associated with API implementation in Open Banking, and provide examples of APIs that are driving innovation in the financial industry.

What is Open Banking?

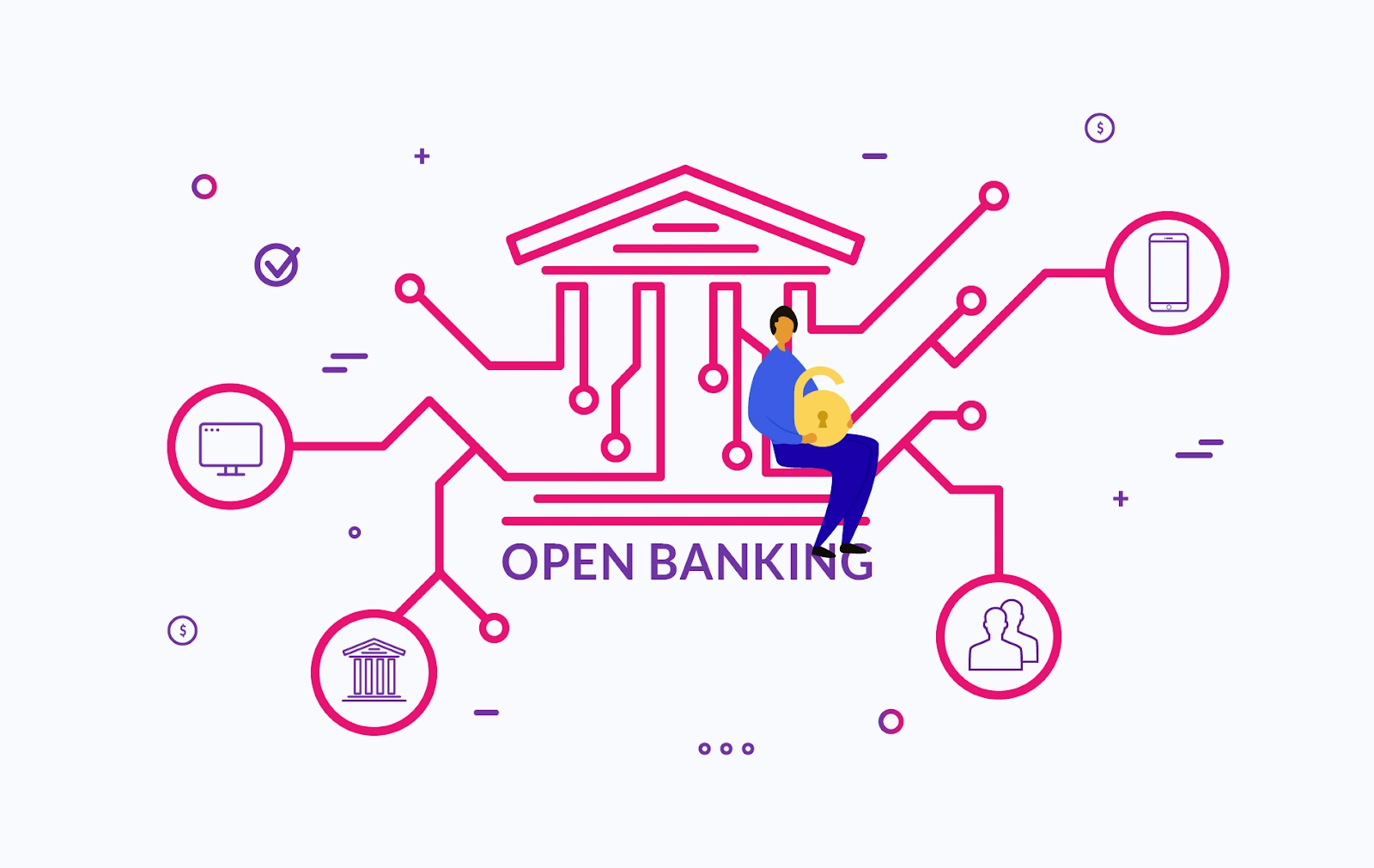

Open Banking is a concept that refers to the secure sharing of financial data between different financial institutions and authorized third-party providers through the use of APIs. It aims to empower consumers by giving them greater control over their financial information and providing them with more choices when it comes to banking services.

Traditionally, banks have been the primary custodians of customers’ financial data, holding information about their accounts, transactions, and spending habits. However, with the emergence of Open Banking, customers now have the ability to grant third-party providers access to their financial data, enabling them to access a wider range of personalized banking services.

Open Banking is facilitated by regulatory initiatives, such as the Revised Payment Services Directive (PSD2) in Europe and the Consumer Data Right (CDR) in Australia. These regulations require banks to open up their systems and provide secure access to customer data, allowing authorized third-party providers to develop innovative financial applications and services.

By embracing Open Banking, consumers can benefit from a range of services such as account aggregation, where they can view and manage multiple bank accounts in one place. They can also access personalized financial advice, compare products from different providers, and initiate payments directly from their accounts using third-party applications. Open Banking has the potential to revolutionize how consumers interact with their finances, offering them greater convenience, transparency, and choice.

For financial institutions, Open Banking presents both opportunities and challenges. By opening up their APIs, banks can collaborate with fintech startups and other third-party providers to innovate and enhance their product offerings. They can also leverage the wealth of customer data available through Open Banking to gain valuable insights and offer more personalized services.

However, implementing Open Banking requires careful consideration of security and data privacy. Banks need to ensure that customer data is protected and only accessed by authorized parties. They must also comply with relevant regulations and standards to maintain trust with their customers.

In summary, Open Banking is a transformative concept that empowers consumers by giving them greater control over their financial data and access to a wider range of personalized banking services. It opens up opportunities for collaboration and innovation within the financial industry, while also posing challenges related to security and data privacy.

What is an API?

An Application Programming Interface, or API, is a set of rules and protocols that allows different software applications to communicate and interact with each other. It acts as a bridge, enabling the exchange of data and functionality between different systems, regardless of their underlying technologies or programming languages.

Think of an API as a waiter in a restaurant. The waiter serves as an intermediary between the customer and the kitchen, taking the customer’s order, relaying it to the kitchen, and delivering the food back to the customer. Similarly, an API facilitates the exchange of information and services between applications, acting as a mediator and enabling seamless integration.

APIs consist of a collection of predefined commands, protocols, and tools that developers use to access specific features or data of a software application or platform. These commands, known as API endpoints, define how requests and responses should be formatted and structured. They specify the functions and capabilities available for interaction.

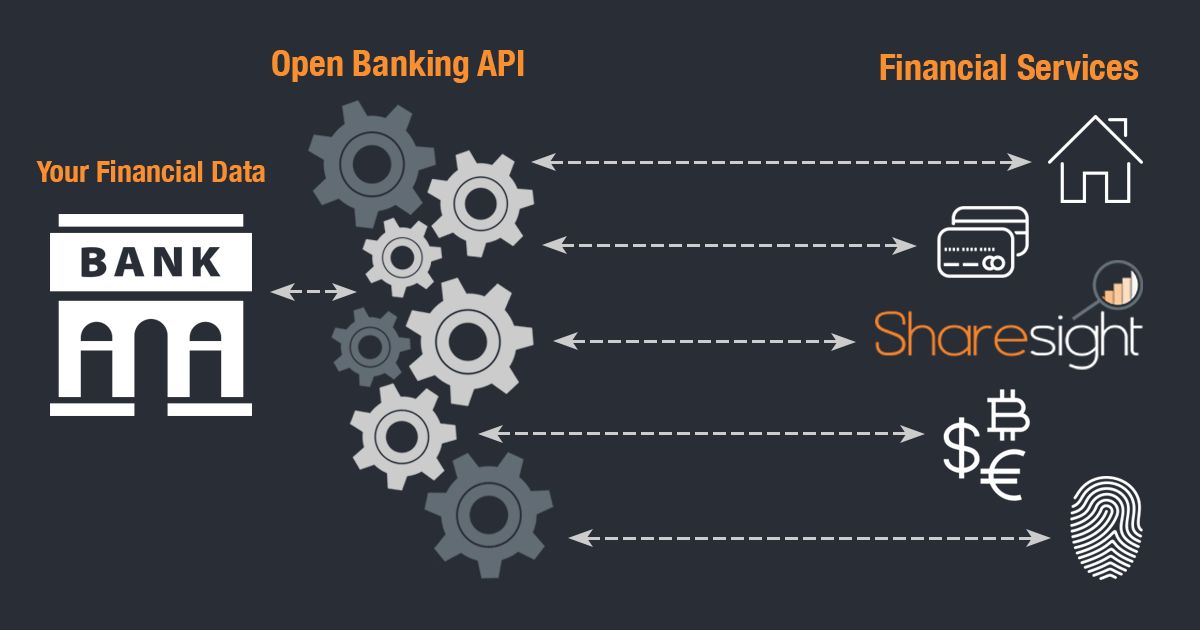

In the context of Open Banking, APIs are used to securely share financial data and services among different financial institutions and third-party providers. They enable authorized third-party developers to access and retrieve specific pieces of information, such as account balances, transaction histories, and payment initiation, from banks and other financial institutions.

APIs in Open Banking follow specific standards and protocols to ensure secure and standardized communication. For example, the REST (Representational State Transfer) architecture is commonly used, which leverages HTTPS (Hypertext Transfer Protocol Secure) for encryption and authentication.

APIs have become an essential component of the modern digital landscape. They enable developers to build sophisticated applications by leveraging the existing functionality and data of other systems. They facilitate integration, reduce development time and resources, and promote innovation by allowing developers to focus on building unique features rather than reinventing the wheel.

APIs can be public or private, depending on their intended use. Public APIs are openly available to developers and allow them to access specified functionalities of an application or platform. Private APIs, on the other hand, are restricted to specific partners or internal use within an organization.

In summary, an API is a set of rules and protocols that enable different software applications to communicate and interact with each other. In the context of Open Banking, APIs facilitate the secure sharing of financial data between financial institutions and third-party providers, driving innovation and providing consumers with access to a broader range of services.

How API works in Open Banking

In the realm of Open Banking, APIs play a crucial role in enabling secure and standardized communication between financial institutions and third-party providers. Let’s explore how APIs work in the context of Open Banking:

1. Authentication and Authorization:

When a third-party application wants to access a user’s financial data or initiate a transaction, it needs to authenticate itself with the relevant financial institution. This is typically done through a process called OAuth (Open Authorization). The user is prompted to grant explicit permission to the third-party application, which then receives an access token to authenticate subsequent API requests.

2. Data Retrieval:

Once the third-party application has obtained the necessary authentication, it can make API requests to retrieve specific data from the financial institution. This could include retrieving account balances, transaction history, and other relevant financial information. The API endpoints define the structure and format of these requests and responses, ensuring consistent communication.

3. Payment Initiation:

In addition to data retrieval, APIs in Open Banking also enable third-party applications to initiate payments on behalf of the user. For example, a user could use a budgeting app to transfer funds from their bank account to a savings account or make a payment to a merchant. APIs provide a secure and standardized way for these payment instructions to be passed to the financial institution.

4. Consent Management:

Consent management is a critical component of Open Banking APIs. It ensures that users have full control over the sharing of their financial data. The APIs facilitate the management of user consent, allowing them to grant, revoke, or modify permissions for third-party applications to access their data. This consent is usually time-limited and can be managed through consent management APIs provided by financial institutions.

5. Real-Time Updates:

APIs also enable real-time updates of financial data. This means that when a user makes a transaction or an account balance changes, the third-party application can be notified immediately. This real-time data access provides users with up-to-date information and enhances the accuracy and timeliness of financial management applications.

Overall, APIs play a vital role in facilitating secure and standardized communication between financial institutions and third-party providers in Open Banking. They enable data retrieval, payment initiation, consent management, and real-time updates, giving consumers greater control over their financial information and access to a wider range of personalized banking services.

Benefits of APIs in Open Banking

The implementation of APIs in Open Banking brings forth a multitude of benefits for various stakeholders, including financial institutions, third-party providers, and, most importantly, consumers. Let’s explore some of the key advantages:

1. Enhanced Customer Experience:

APIs enable seamless integration between different financial services, allowing customers to access a wide range of banking services and products through a single platform. This unified experience enhances convenience, simplifies financial management, and provides a more holistic view of a customer’s financial situation.

2. Increased Competition and Innovation:

APIs open up a level playing field for third-party providers, allowing them to compete with traditional banks and offer innovative solutions. This increased competition fosters innovation, as new players can bring fresh ideas and more personalized services to the market. Ultimately, consumers benefit from a broader range of options and improved financial offerings.

3. Improved Financial Access and Inclusion:

Open Banking APIs have the potential to promote financial inclusion by granting access to previously underserved individuals and businesses. Third-party providers can leverage APIs to build applications tailored to specific customer segments, making financial services more accessible, affordable, and relevant to their needs.

4. Personalized Services:

APIs provide access to valuable customer data, allowing financial institutions and third-party providers to deliver more personalized services. By leveraging insights from transaction history, spending patterns, and other financial data, institutions can offer tailored recommendations, customized products, and targeted financial advice to their customers.

5. Seamless Integration and Collaboration:

APIs facilitate seamless integration between different systems and applications, enabling financial institutions to collaborate with third-party providers more effectively. This collaboration can lead to the creation of innovative financial products and services that combine the strengths of multiple stakeholders, enhancing the overall banking ecosystem.

6. Efficiency and Cost-Savings:

APIs streamline processes and automate data exchange between financial institutions and third-party providers. This automation reduces manual effort and paperwork, resulting in improved operational efficiency and significant cost savings for both banks and their partners.

7. Security and Control:

APIs in Open Banking prioritize security and data privacy, enforcing strict access controls and encryption protocols. Customers retain control over their data and must provide explicit consent for access, ensuring that their sensitive financial information is protected.

In summary, the implementation of APIs in Open Banking brings numerous benefits, including enhanced customer experiences, increased competition and innovation, improved financial access and inclusion, personalized services, seamless integration and collaboration, efficiency and cost-savings, as well as enhanced security and control over data.

Challenges of APIs in Open Banking

While APIs have revolutionized the financial industry and brought significant benefits to Open Banking, their implementation also poses certain challenges that need to be addressed. Let’s explore some of the key challenges:

1. Security and Data Privacy:

One of the primary concerns associated with Open Banking APIs is the security and privacy of customer data. Financial institutions must ensure robust authentication and encryption mechanisms to protect sensitive information and prevent unauthorized access. Compliance with data protection regulations, such as GDPR, is crucial to maintaining consumer trust and confidence in the Open Banking ecosystem.

2. Standardization and Interoperability:

With multiple financial institutions and third-party providers involved, ensuring standardization and interoperability of APIs becomes a challenge. Different organizations may adopt varying standards, making it difficult for developers to build applications that work seamlessly across various platforms. Collaborative efforts and industry-wide initiatives are essential to establish common API standards and promote interoperability.

3. Technical Complexity:

Developing and maintaining APIs can be technically complex, especially when integrating with legacy systems or dealing with diverse data formats and structures. Financial institutions may face challenges in modernizing their infrastructure and ensuring compatibility with newer API technologies. Robust documentation, developer support, and effective API management strategies are necessary to overcome these complexities.

4. Regulatory Compliance:

Open Banking initiatives are often governed by stringent regulatory frameworks. Financial institutions and third-party providers must adhere to these regulations to ensure legal compliance and protect consumer interests. Compliance with regulations such as PSD2 in Europe and CDR in Australia involves significant investments in technology, governance, and process changes.

5. Liability and Responsibility:

With the sharing of financial data and financial transactions through APIs, issues related to liability and responsibility can arise. Determining who is responsible in case of errors, disputes, or fraudulent activities can become complex in a multi-party ecosystem. Clear contractual agreements, well-defined roles and responsibilities, and dispute resolution mechanisms are important to address these challenges.

6. Consumer Awareness and Trust:

Open Banking relies on the trust and consent of consumers to share their financial data with third-party providers. Ensuring that consumers are aware of the benefits, risks, and rights associated with Open Banking is crucial. Educating consumers about their data privacy rights, security measures, and the control they have over their data is necessary to build trust and wider adoption of Open Banking services.

In summary, while APIs in Open Banking offer immense opportunities, they also present challenges related to security, standardization, technical complexity, regulatory compliance, liability, and consumer trust. Overcoming these challenges requires collaboration, industry-wide standards, and continuous efforts to ensure a secure and transparent Open Banking ecosystem.

Examples of APIs in Open Banking

The implementation of APIs in Open Banking has sparked innovation and led to the development of numerous applications and services that enhance the banking experience for consumers. Let’s explore some examples of APIs that are driving innovation in the realm of Open Banking:

1. Payment Initiation Services (PIS) APIs:

PIS APIs enable third-party providers to initiate payments directly from a customer’s bank account. These APIs facilitate secure and convenient payment services, such as making online purchases or transferring funds between accounts. PIS APIs adhere to regulatory requirements and provide seamless integration with a customer’s banking infrastructure.

2. Account Information Services (AIS) APIs:

AIS APIs allow third-party providers to access and retrieve account-related information, including balance, transaction history, and customer details. With AIS APIs, customers can aggregate their financial information from multiple accounts and get a holistic view of their financial situation through a single application or platform.

3. Know Your Customer (KYC) APIs:

KYC APIs play a critical role in customer onboarding and verification processes. These APIs enable financial institutions and third-party providers to access customer identity and verification data to comply with regulatory requirements. KYC APIs streamline the customer onboarding process and enhance customer due diligence.

4. Data Enrichment APIs:

Data enrichment APIs provide third-party providers access to additional data sources that can enhance the analysis and understanding of customer financial information. By enriching the available data with external sources, financial institutions and third-party providers can offer more personalized recommendations, better risk assessment, and improved credit scoring to customers.

5. Fraud Prevention APIs:

Fraud prevention APIs help financial institutions and third-party providers detect and prevent fraudulent activities. These APIs analyze transactional data in real-time to identify suspicious patterns and behaviors, alerting customers and institutions to potential fraud attempts. By leveraging fraud prevention APIs, financial institutions can enhance security and protect their customers against fraudulent activities.

6. Open Data APIs:

Open Data APIs promote transparency and financial innovation by providing access to anonymized and aggregated financial data. These APIs enable developers and researchers to gain insights into market trends, consumer behavior, and economic indicators. Open Data APIs can drive innovation and foster the development of new financial applications and services.

These are just a few examples of the wide array of APIs utilized in Open Banking. The adoption of APIs in Open Banking has paved the way for continuous innovation and collaboration among financial institutions, fintech startups, and other third-party providers, resulting in a more diverse and customer-centric banking ecosystem.

Conclusion

Open Banking, powered by APIs, is revolutionizing the financial industry by enabling secure data sharing, fostering innovation, and offering personalized banking experiences. APIs have become the backbone of Open Banking, providing a standardized and secure way for financial institutions and third-party providers to exchange information and services.

By embracing Open Banking APIs, financial institutions can enhance their product offerings, collaborate with fintech startups, and deliver more personalized services to their customers. APIs enable seamless integration, real-time updates, and secure authentication and authorization processes, resulting in enhanced customer experiences and increased competition in the industry.

However, the implementation of APIs in Open Banking also comes with challenges, such as ensuring data security and privacy, achieving standardization and interoperability, addressing technical complexities, navigating regulatory compliance, and building consumer trust. These challenges require collaborative efforts, industry-wide initiatives, and continuous evaluation to maintain a secure and transparent Open Banking ecosystem.

Despite the challenges, the benefits of APIs in Open Banking are significant. APIs promote financial inclusion, foster innovation, provide personalized services, streamline operations, and empower consumers with more control over their financial data and choices. The adoption of APIs in Open Banking has paved the way for a more connected, convenient, and customer-centric financial ecosystem.

In conclusion, APIs have transformed Open Banking into a dynamic, innovative, and consumer-focused landscape. They have redefined the way financial institutions and third-party providers collaborate, share data, and deliver services. As technology continues to evolve, APIs will play an increasingly critical role in shaping the future of Open Banking, driving further innovation, and creating more value for both the industry and consumers.