Introduction

Technology has revolutionized the banking industry, offering new and efficient ways to manage finances. One of the remarkable innovations in this digital era is the Application Programming Interface, commonly known as API. APIs have become an integral part of the banking landscape, transforming how financial institutions interact with customers, partners, and even with each other.

An API, in simple terms, is a set of rules and protocols that allows software applications to communicate and interact with each other. In the context of banking, APIs provide a bridge between various systems and enable secure and seamless exchange of data and functionality.

APIs have opened up a plethora of opportunities for banks to enhance their digital capabilities and offer innovative services to customers. With the help of APIs, traditional banking functions, such as payments, account information, and transfers, can be easily accessed and integrated into third-party applications, bringing convenience and flexibility to customers.

Furthermore, APIs enable banks to collaborate with fintech startups and other businesses, fostering a vibrant ecosystem. This collaboration allows for the development of innovative financial products and services that cater to the ever-evolving needs of customers.

In this article, we will explore the concept of APIs in banking, their working principles, the benefits they bring, and the challenges that financial institutions may face in implementing API strategies. We will also discuss the security considerations that are crucial to safeguard the integrity and privacy of customer data. Finally, we will delve into the future of APIs in banking and the potential they hold in shaping the industry’s landscape.

What is an API?

An API, short for Application Programming Interface, is a set of rules and protocols that allows different software applications to communicate and interact with each other. APIs define the methods and data formats that applications should use to exchange information, making it easier for developers to leverage existing functionalities and build new applications quickly.

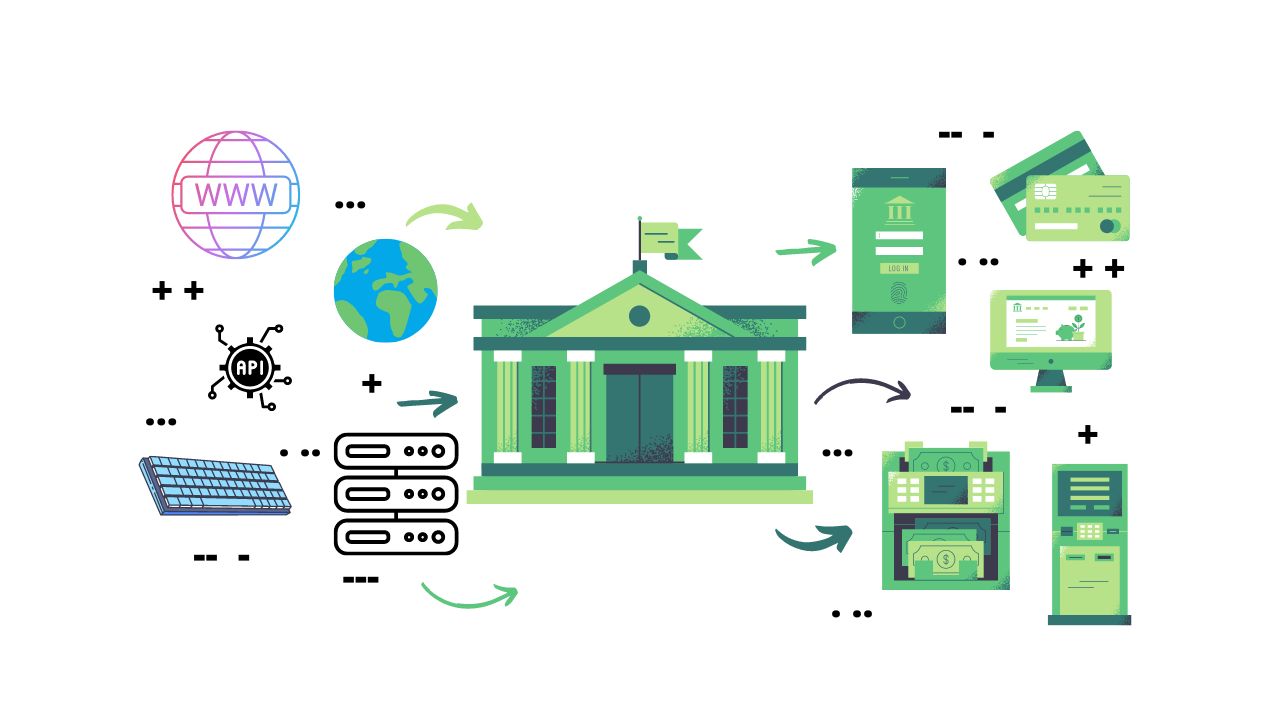

In the context of the banking industry, APIs serve as a bridge between various systems, allowing banks to expose their services and data to third-party developers. This enables seamless integration of banking functionalities into external applications such as mobile banking apps, personal finance management tools, and payment gateways.

APIs are designed to be language-agnostic, meaning they can be implemented in any programming language and used on different platforms. They operate in a standardized manner, ensuring compatibility and interoperability between systems.

APIs can be categorized into different types based on their purpose and functionality. Some common types of APIs in banking include:

- Payment APIs: These APIs facilitate secure and efficient payment transactions between banking systems and merchant applications. They enable users to initiate payments, check transaction status, and retrieve payment history.

- Account Information APIs: These APIs provide access to account-related information, including balances, transaction history, and account details. They enable users to view their account information without having to log in to the banking system.

- Transfer APIs: These APIs allow users to initiate fund transfers between different accounts, both within the same bank and across different banks. They streamline the transfer process and provide real-time confirmation of successful transactions.

- Authentication APIs: These APIs handle the authentication and authorization process for users accessing banking services. They verify user identities, validate login credentials, and grant access permissions based on user roles and privileges.

APIs provide a standardized and secure way for developers to access and utilize banking services and data. By leveraging APIs, developers can focus on creating unique user experiences and innovative applications, without having to worry about the underlying complexities of banking systems.

Overall, APIs play a vital role in enabling digital transformation in the banking industry. They foster collaboration between banks and external stakeholders, drive innovation, and enhance customer experiences by bringing banking services closer to the users in a seamless and integrated manner.

How does API work in banking?

APIs serve as the backbone of modern banking systems, enabling seamless integration and communication between different applications and systems. In the banking context, APIs work by exposing specific functionalities and data to authorized developers, allowing them to build innovative applications and services that leverage the power of banking systems.

Here is a high-level overview of how APIs work in banking:

- API Documentation: Banks provide comprehensive documentation that outlines the available APIs, their functionalities, and the required authentication and authorization mechanisms. This documentation serves as a guide for developers who want to utilize the bank’s API services.

- API Key and Authorization: Developers who intend to access a bank’s APIs need to obtain an API key or token. This key, along with other necessary authorization credentials, ensures that only authorized applications and developers can interface with the bank’s systems.

- API Calls: Once authorized, developers can make API calls to access specific banking services and data. These API calls are made using HTTP requests, and the requested data is typically returned in a standardized format, such as JSON or XML.

- Data Exchange: The API call triggers the exchange of data between the bank’s systems and the external application. For example, a payment API call initiates a transaction between the user’s bank account and the designated recipient, while an account information API call retrieves the user’s account details from the banking system.

- Response Handling: The bank’s API returns a response to the developer’s API call, indicating the success or failure of the requested action. This response may include relevant data, error messages, or status updates.

APIs in banking leverage secure and encrypted communication protocols, such as HTTPS, to ensure that sensitive data is exchanged securely between applications. Additionally, banks often implement rate limiting and authentication mechanisms to prevent unauthorized access and protect user privacy.

By leveraging APIs, banks enable developers to create innovative applications that extend the functionality of traditional banking systems. For instance, a personal finance management app may use APIs to access account information and transaction data, providing users with real-time insights into their financial health.

Furthermore, APIs enable banks to collaborate with third-party service providers and fintech startups, allowing for the integration of complementary services. This collaboration enhances the overall customer experience by providing a seamless and comprehensive suite of financial services.

Overall, APIs play a vital role in enhancing the flexibility, accessibility, and interoperability of banking systems. They enable the development of customer-centric applications, foster innovation, and drive digital transformation within the banking industry.

Benefits of API in banking

The utilization of APIs in the banking industry brings forth numerous benefits for both financial institutions and customers. These benefits contribute to improved efficiency, enhanced customer experiences, and the overall advancement of the banking landscape.

Here are some key benefits of API in banking:

- Streamlined Processes: APIs allow banks to streamline their processes by automating various tasks and integrating their systems with third-party applications. This automation reduces manual intervention, increases operational efficiency, and speeds up service delivery.

- Enhanced Customer Experience: APIs enable the development of customer-centric applications that provide seamless access to banking services. Customers can easily manage their accounts, make payments, and transfer funds directly from their preferred applications, resulting in a frictionless and convenient banking experience.

- Expanded Service Offerings: APIs allow banks to extend their service offerings beyond traditional banking functions. By collaborating with third-party vendors and fintech startups, banks can integrate additional services, such as personal finance management tools, digital wallets, and investment platforms, into their ecosystem.

- Improved Accessibility: APIs make banking services more accessible by allowing users to interact with their accounts through various channels, including mobile apps, websites, and voice assistants. This multi-channel approach ensures that customers have flexibility in choosing how they engage with their financial institutions.

- Increased Innovation: APIs foster innovation by enabling developers to create new and creative applications that leverage banking services. This encourages experimentation and the development of innovative solutions that address specific customer needs and preferences.

- Efficient Collaboration: APIs facilitate collaboration between banks and external partners, including fintech companies and software developers. This collaborative environment promotes the creation of new financial products and services, leading to a more dynamic and competitive industry.

- Personalized Offerings: APIs provide access to customer data, allowing banks to analyze user behavior and preferences. This data-driven approach enables banks to offer personalized recommendations, tailored promotions, and targeted marketing campaigns, enhancing customer satisfaction and loyalty.

The benefits of API in banking are not limited to the examples above. As the industry continues to evolve, APIs will play a crucial role in driving further innovation, opening up new opportunities, and reshaping the way financial services are delivered.

Use cases of API in banking

The integration of APIs has opened up a world of possibilities in the banking industry, enabling the development of innovative applications and services. Here are some key use cases of API in banking:

- Mobile Banking: APIs have revolutionized the mobile banking experience, allowing customers to access their accounts, make transactions, and manage finances directly from their smartphones. Mobile banking apps utilize APIs to secure real-time data on balances, transaction history, and account information, providing users with seamless control over their financial affairs.

- Payment Aggregators: APIs enable payment aggregators to consolidate multiple payment gateways into a single platform, making it convenient for users to make payments from different accounts and sources. By integrating with banking APIs, these aggregators offer a wide range of payment options and ensure secure and efficient transactions.

- Personal Finance Management: APIs facilitate the development of personal finance management tools that aggregate transaction data from multiple banks and financial institutions. These tools use APIs to fetch account information and categorize transactions, providing users with insights into their spending habits, budgeting, and financial goals.

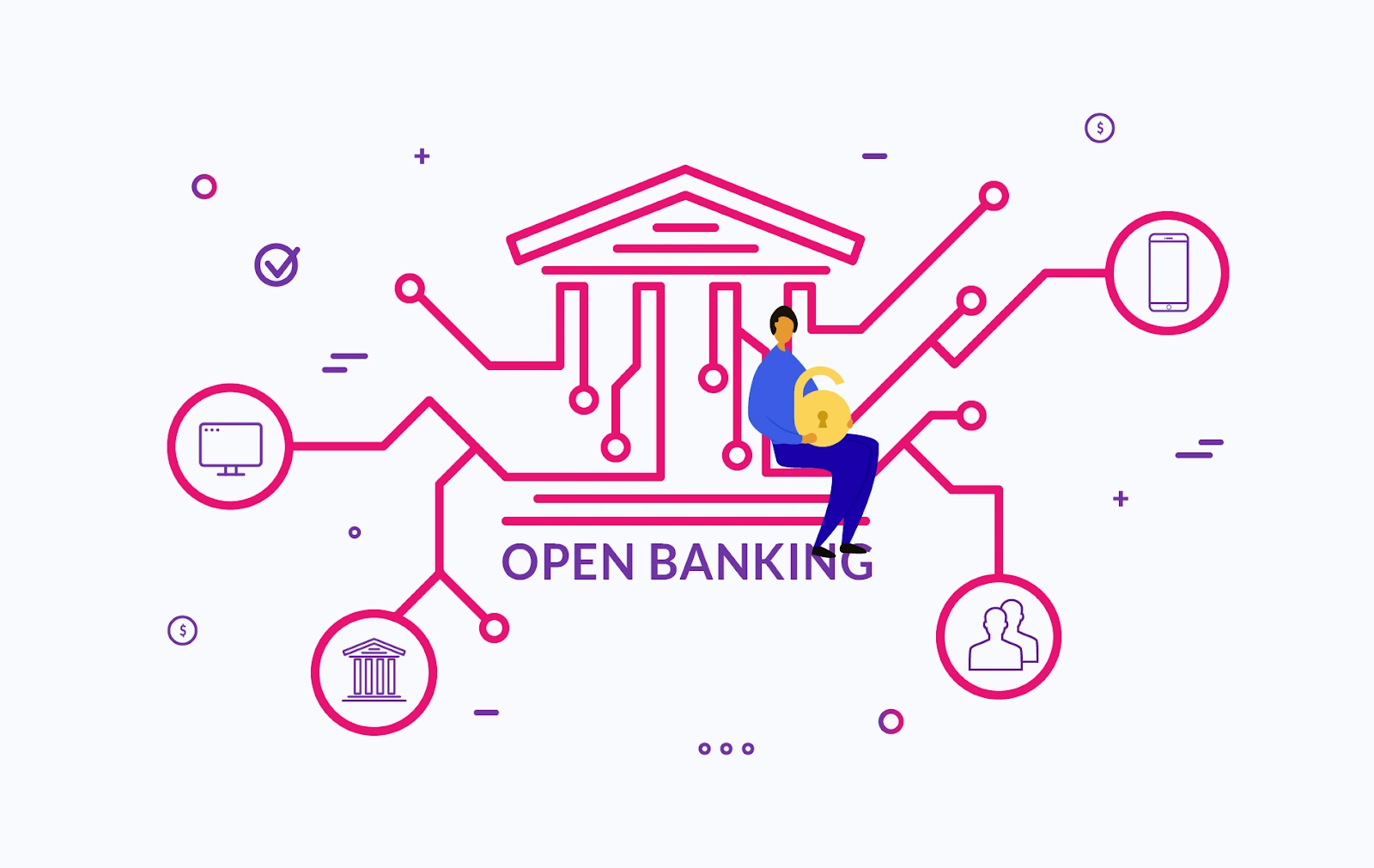

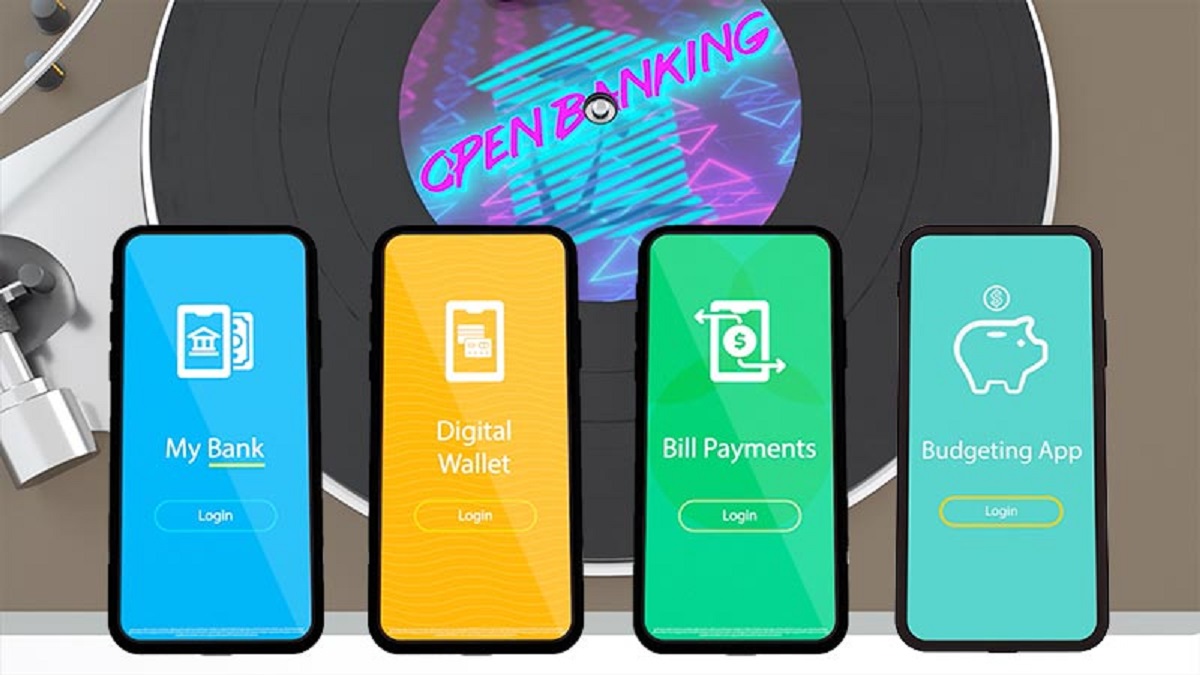

- Open Banking: API-based open banking initiatives allow customers to authorize third-party applications to access their banking data. This empowers users to share their financial information securely with fintech companies, enabling personalized recommendations, loan approvals, and other innovative services.

- Digital Wallets: APIs play a crucial role in the functionality of digital wallets by securely integrating banking services with mobile payment platforms. With the help of APIs, users can link their bank accounts and cards to digital wallets, enabling seamless transactions, contactless payments, and peer-to-peer transfers.

- Account Aggregation: APIs enable account aggregation services to consolidate financial data from multiple institutions into a single platform. These services use APIs to fetch transactional information, balances, and other account details, providing users with a comprehensive view of their financial holdings.

- API Marketplaces: Banks can create API marketplaces, allowing developers and businesses to access and utilize their APIs. These marketplaces promote collaboration and innovation by providing a platform for creating new applications and services that leverage banking functionalities.

These use cases illustrate how APIs are transforming traditional banking services, bringing convenience, efficiency, and enhanced functionality to customers. The integration of APIs in banking continues to expand, with new use cases continually emerging as technology advances and customer demands evolve.

Challenges of API in banking

While APIs bring numerous benefits and opportunities to the banking industry, their implementation is not without challenges. These challenges need to be addressed to ensure the smooth and secure functioning of API-driven banking systems. Here are some key challenges of API in banking:

- Security Concerns: APIs expose banking systems to potential security risks, as they involve the exchange of sensitive customer data. Banks must implement robust security measures, such as encryption, authentication, and access controls, to protect customer information and prevent unauthorized access.

- Compliance and Regulations: The integration of APIs in banking must comply with various regulatory frameworks, such as data privacy laws and financial regulations. Banks must ensure that their API implementations adhere to these regulations to maintain legal and ethical standards.

- Legacy System Integration: Many banks have complex legacy systems that may not be designed to seamlessly integrate with modern APIs. Integrating APIs with these legacy systems can be challenging and may require significant updates and modifications to ensure compatibility.

- Standardization: APIs in the banking industry lack standardization in terms of data formats, protocols, and authentication mechanisms. This lack of standardization can create interoperability issues when integrating different APIs from multiple banks or when collaborating with external partners.

- Reliability and Resilience: APIs need to be highly reliable and resilient to ensure uninterrupted service availability. Banks must implement robust API management solutions and infrastructure to handle high volumes of requests, prevent downtime, and manage API traffic efficiently.

- Data Integrity and Privacy: As APIs involve the exchange of customer data, ensuring data integrity and privacy is crucial. Banks must implement measures like data encryption, secure transmission protocols, and consent management to protect customer data from unauthorized access and data breaches.

- API Documentation and Support: Clear and comprehensive documentation is essential for developers to understand and utilize banking APIs effectively. Banks need to provide extensive documentation and reliable developer support to assist developers in integrating and utilizing their APIs.

- Dependency on Third-Party Providers: Banks often rely on third-party providers for API integration and management. This dependency can introduce potential risks, such as service disruptions, data breaches, or vendor lock-in. Banks must carefully evaluate and select reliable and trusted third-party providers to mitigate these risks.

Addressing these challenges requires a proactive and comprehensive approach by banks. By prioritizing security, compliance, and technical robustness, banks can overcome these challenges and harness the full potential of APIs in the banking industry.

Security Considerations for API in banking

As APIs become increasingly prevalent in the banking industry, ensuring the security of API-driven systems becomes paramount. The exchange of sensitive customer data and integration with third-party applications require strict security measures to protect against data breaches and unauthorized access. Here are some important security considerations for API in banking:

- Authentication and Access Control: Implement robust authentication mechanisms such as OAuth or JSON Web Tokens (JWT) to verify the identity of users and applications accessing the API. Use strong access control mechanisms to ensure that only authorized entities can access specific API functions and data.

- Encryption: Data transmitted between the API and client applications should be encrypted using secure cryptographic protocols (e.g., HTTPS). Encryption ensures that data exchanged remains confidential and protected from eavesdropping and tampering.

- API Key Management: Secure the issuance and management of API keys to prevent unauthorized access. Employ mechanisms to rotate and revoke API keys as needed to maintain control over API access and mitigate the risk of compromised keys.

- Secure Data Transmission: Use secure channels for transmitting sensitive data like account details and personal information. Implement Transport Layer Security (TLS) protocols to ensure the integrity and confidentiality of data during transmission.

- Input Validation and Sanitization: Apply strict input validation and data sanitization techniques to prevent common vulnerabilities such as Cross-Site Scripting (XSS) and SQL injection attacks. Validate and sanitize user input to mitigate the risk of malicious code execution or unauthorized access to backend systems.

- Security Testing: Conduct regular security testing, including threat modeling, vulnerability scanning, and penetration testing, to identify and address potential security weaknesses in the API ecosystem. This helps ensure that security vulnerabilities are proactively identified and remediated.

- Throttling and Rate Limiting: Implement throttling and rate limiting mechanisms to prevent abuse and denial-of-service attacks. Enforce usage limits on API calls to protect the API infrastructure from excessive traffic or malicious activities.

- Access Logging and Monitoring: Implement comprehensive logging and monitoring systems to track and monitor API usage. Monitor API traffic, analyze logs, and employ anomaly detection techniques to identify suspicious activities or potential security breaches in real-time.

- Secure Integration with Third-Party Services: When integrating with third-party services or vendors, conduct thorough security assessments of their APIs and ensure they adhere to industry best practices for security and compliance.

Addressing these security considerations is crucial to protect customer data, maintain trust, and adhere to regulatory requirements. By adopting a robust and comprehensive security framework, banks can ensure the secure implementation and operation of APIs in the banking ecosystem.

Future of API in banking

The future of APIs in banking holds tremendous potential for reshaping the industry and driving further innovation. As technology continues to evolve, the role of APIs is expected to expand, offering new opportunities and transforming the way financial services are delivered. Here are some key aspects that define the future of API in banking:

- Advancing Open Banking: Open banking initiatives, powered by APIs, will continue to gain traction. Customers will have more control over their financial data, allowing them to securely share information with trusted third-party providers to access personalized services, improved financial management tools, and customized offerings.

- Artificial Intelligence and APIs: APIs will play a crucial role in facilitating the integration of artificial intelligence (AI) technologies in banking. APIs will enable AI-powered applications, such as chatbots and virtual assistants, to provide personalized and context-aware customer experiences, seamless authentication, and enhanced fraud detection.

- Blockchain and Distributed Ledger Technology: APIs will enable banks to harness the potential of blockchain and distributed ledger technology. Banks can leverage APIs to securely integrate with decentralized networks, enabling real-time settlement, smart contracts, and transparent transaction tracking.

- Internet of Things (IoT): APIs will facilitate the integration of banking services with IoT devices. APIs will enable secure connections between smart devices, such as wearables, connected cars, and smart homes, allowing for frictionless payments, personalized offers, and contextual financial services.

- Embedded Banking: APIs will power the expansion of embedded banking, where banking services are seamlessly embedded within non-financial applications and platforms. APIs will enable customers to access banking functionalities, such as payments, transfers, and account management, directly within their favorite apps, websites, or even social media platforms.

- Data Collaboration and Analytics: APIs will enhance data collaboration and analytics capabilities for banks. APIs will allow banks to securely share and analyze data with partners, fintech startups, and other financial institutions, promoting the development of innovative products and services based on comprehensive data insights.

- Robotic Process Automation (RPA): APIs will integrate with RPA technologies to automate routine banking processes. APIs will enable efficient and secure communication between systems and bots, streamlining activities like customer onboarding, loan processing, and compliance checks.

- API Marketplaces: Banks will continue to evolve their API marketplaces, providing developers with a broader range of APIs to build innovative applications and services. API marketplaces will foster collaboration, drive competition, and spur the development of next-generation banking solutions.

The future of API in banking is marked by the convergence of technologies, collaboration, and customer-centricity. APIs will empower banks to deliver personalized experiences, leverage emerging technologies, and expand their offerings beyond traditional banking boundaries.

As the industry evolves, it is essential for banks to remain agile, adaptive, and prepared to embrace the synergies between APIs and emerging technologies to stay competitive and meet the ever-changing needs of their customers.

Conclusion

APIs have revolutionized the banking industry, enabling seamless integration, collaboration, and innovation. They have transformed how banks interact with customers, partners, and third-party developers. By providing secure and standardized ways to access banking functionalities and data, APIs have enhanced the efficiency, accessibility, and customer experience in the banking landscape.

The evolution of APIs in banking has brought forth numerous benefits. Banks can streamline processes, offer personalized services, and expand their offerings by integrating with external applications and collaborating with fintech startups. Customers now have greater control and convenience, accessing banking services anytime, anywhere, through various channels and devices.

However, the implementation of API-driven systems in banking comes with its set of challenges. Security considerations, compliance with regulations, legacy system integration, and standardization remain key focus areas for banks. Addressing these challenges is crucial to ensure the secure and scalable implementation of APIs and protect customer data.

The future of APIs in banking is promising. As technology advances, APIs will continue to drive digital transformation in the industry. Open banking, artificial intelligence, blockchain, IoT, and embedded banking are just a few areas where APIs will play a vital role in shaping the future of banking services.

In conclusion, APIs have become the catalyst for innovation and collaboration in the banking sector, transforming traditional banking practices and creating new opportunities. By harnessing the power of APIs, banks can navigate the ever-changing landscape, provide exceptional customer experiences, and deliver innovative solutions that meet the evolving demands of the digital age.