Introduction

Welcome to the world of 401(k) investments! As an employee, you have the opportunity to contribute to your 401(k) retirement plan and make investment decisions that can help grow your savings for the future. Understanding how to effectively manage your 401(k) investments is essential for achieving your financial goals and ensuring a secure retirement.

A 401(k) is a tax-advantaged retirement savings plan offered by many employers. It allows you to contribute a portion of your salary to a retirement account, and in some cases, your employer may match a certain percentage of your contributions. The money you contribute to your 401(k) is typically invested in a range of mutual funds, stocks, and bonds.

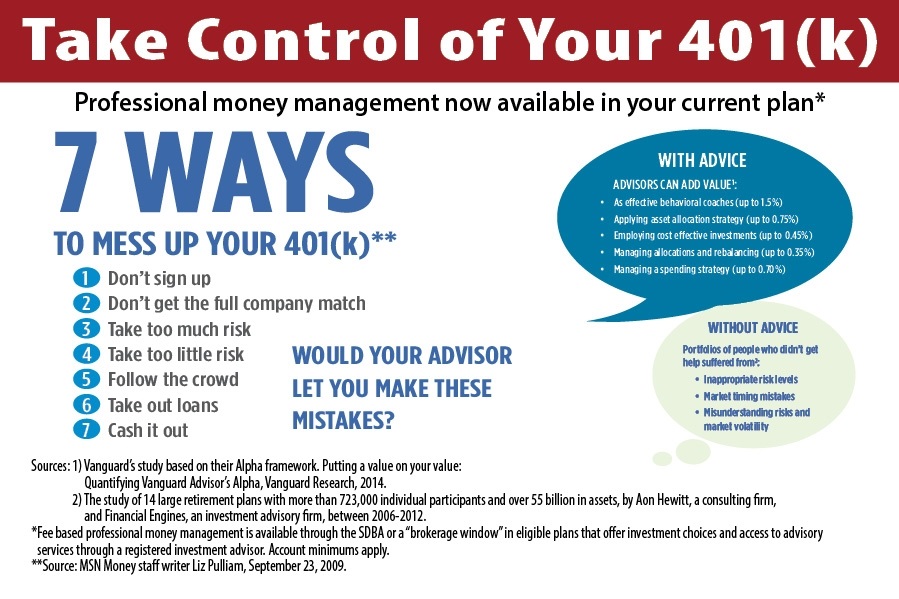

Managing your 401(k) investments involves making key decisions about asset allocation, risk tolerance, and portfolio diversification. These decisions can have a significant impact on the growth of your retirement savings over time. By taking an active role in managing your investments, you can maximize the potential returns and minimize the risks associated with your 401(k) account.

Throughout this guide, we will explore various aspects of managing your 401(k) investments, providing you with valuable insights and strategies to make informed decisions. From understanding different investment options to evaluating performance and adjusting your investments over time, we will cover the essential steps to help you navigate the complexities of 401(k) management.

Keep in mind that everyone’s financial situation and goals are unique, and there is no one-size-fits-all approach to managing a 401(k). The information presented here is intended to serve as a general guide, and we encourage you to consult with a financial advisor or investment professional before making any specific investment decisions.

So, let’s dive into the world of 401(k) investments and discover how you can take control of your financial future!

Understanding Your 401(k)

Before you can effectively manage your 401(k) investments, it’s crucial to have a clear understanding of how your plan works. A 401(k) is a retirement savings plan offered by employers, allowing employees to save and invest a portion of their salary for the future.

When you enroll in a 401(k) plan, you’ll typically have the option to contribute a percentage of your pre-tax income. Some employers also offer a matching contribution, where they will contribute a portion of the employee’s salary to the account. This matching contribution can be a significant benefit, as it provides an additional boost to your retirement savings.

Contributions made to your 401(k) are usually invested in a selection of mutual funds, stocks, and bonds. The specific investment options available to you will depend on the plan offered by your employer. It’s important to review and understand the investment options provided, as they will determine the potential returns and risks associated with your account.

One key advantage of a 401(k) is the tax benefits it offers. Your contributions are made on a pre-tax basis, meaning they are deducted from your paycheck before any taxes are withheld. This reduces your taxable income for the year, potentially lowering your overall tax liability. Additionally, the earnings on your investments grow tax-deferred, meaning you won’t pay taxes on them until you withdraw the funds in retirement.

It’s essential to be aware of the restrictions and regulations governing 401(k) accounts. Typically, you won’t be able to withdraw funds from your account until you reach the age of 59 1/2, except under certain circumstances, such as financial hardship. Withdrawing funds before this age can result in penalties and taxes.

To stay informed about your 401(k) plan, you will receive periodic statements that detail your contributions, investment returns, and account balance. It’s crucial to review these statements regularly to ensure your investments align with your financial goals and risk tolerance.

Understanding the basic principles and mechanics of your 401(k) plan is the first step towards effective management of your investments. In the next section, we will explore how to choose the right investments for your portfolio based on your risk tolerance and financial objectives.

Choosing Your Investments

When it comes to managing your 401(k) investments, one of the key decisions you’ll need to make is selecting the right investments for your portfolio. The investment options available in your 401(k) plan may include mutual funds, target-date funds, individual stocks, and bonds.

Before diving into the different investment options, it’s essential to assess your risk tolerance and investment goals. Risk tolerance refers to how comfortable you are with the potential ups and downs of the market. If you’re more risk-averse, you may lean towards more conservative investments, while those with a higher risk tolerance may opt for more aggressive investments.

Mutual funds are a common investment option in 401(k) plans. They pool money from multiple investors to invest in a diversified portfolio of stocks, bonds, or a combination of both. These funds are managed by professional fund managers who make investment decisions on behalf of the investors.

Another popular choice is target-date funds. These funds automatically adjust the asset allocation as you approach your target retirement date. They typically start with a higher allocation to stocks when you’re younger and gradually shift towards more conservative investments as you near retirement.

If you prefer a hands-on approach to investing, you may consider investing in individual stocks or bonds. Individual stocks allow you to purchase shares of specific companies, while bonds represent loans made to governments or corporations.

When selecting investments, it’s important to diversify your portfolio. Diversification helps to spread out your risk by investing in a variety of asset classes and sectors. By diversifying, you avoid putting all your eggs in one basket and reduce the impact of any single investment performing poorly.

Take the time to research and understand the investment options available in your 401(k) plan. Read the fund prospectuses, which provide essential information about the fund’s objectives, past performance, and fees. Additionally, consider consulting with a financial advisor who can provide personalized advice based on your unique circumstances.

Remember, your investment choices should align with your risk tolerance, time horizon, and financial goals. It’s crucial to periodically review your portfolio and make adjustments as needed. In the next section, we will discuss how to assess the performance of your investments to ensure they meet your expectations.

Assessing Your Risk Tolerance

When it comes to managing your 401(k) investments, understanding your risk tolerance is crucial. Risk tolerance refers to your willingness and ability to endure fluctuations in the value of your investments. It’s important to assess your risk tolerance to determine the appropriate asset allocation for your portfolio.

There are several factors to consider when assessing your risk tolerance. Firstly, consider your investment goals and time horizon. If you have a long time until retirement, you may be able to tolerate more risk as you have a greater opportunity to recover from market downturns. However, if you’re nearing retirement, you may want to adopt a more conservative approach to protect your accumulated savings.

Next, assess your financial circumstances, including your income, expenses, and existing savings. Evaluate how comfortable you are with potential losses in your investments. If you have a stable income and a substantial emergency fund, you may be more willing to take on higher-risk investments. On the other hand, if you have limited savings and depend on your 401(k) for retirement, you may prefer more conservative investments to protect your future income.

Consider also your emotional attitude towards risk. Some individuals have a higher tolerance for volatility and are comfortable with market fluctuations. Others may be more risk-averse and prefer the stability of conservative investments. Understanding your emotional response to risk is important to ensure you can stick to your investment strategy during periods of market turbulence.

To get a better understanding of your risk tolerance, you can also utilize risk assessment tools and questionnaires provided by financial institutions or consult with a financial advisor. These tools ask a series of questions and provide an assessment of your risk tolerance based on your responses. They can be a helpful starting point for determining your ideal investment strategy.

Once you have assessed your risk tolerance, it’s important to align your asset allocation accordingly. A more risk-tolerant investor may opt for a higher allocation to stocks to potentially achieve higher returns. On the other hand, a more conservative investor may favor a larger allocation to bonds or cash equivalents for more stability.

Remember that risk tolerance may change over time. It’s important to periodically reassess your risk tolerance, particularly as you approach retirement or experience significant life events. Regularly reviewing and rebalancing your portfolio will help ensure that your investments remain aligned with your risk tolerance and financial goals.

In the next section, we will delve into the importance of diversifying your portfolio to further manage risk.

Diversifying Your Portfolio

When it comes to managing your 401(k) investments, one of the most effective strategies for reducing risk is diversifying your portfolio. Diversification involves spreading your investments across different asset classes, sectors, and geographical regions. By diversifying, you aim to minimize the impact of any single investment performing poorly and increase the potential for positive returns.

The key principle of diversification is the old adage: “Don’t put all your eggs in one basket.” Instead of investing all your money in a single stock or asset, allocate your investments across a mix of stocks, bonds, and other investment vehicles.

By diversifying across asset classes, you can benefit from the differing performance characteristics of each. For example, during economic downturns, bonds may offer more stability while stocks may experience greater volatility. By holding both stocks and bonds, you can potentially offset losses in one asset class with gains in the other, thus reducing the impact of market fluctuations.

Furthermore, diversification involves investing in various sectors and industries. Different sectors perform differently based on market conditions and economic factors. By spreading your investments across sectors such as technology, healthcare, finance, and energy, you reduce the risk of being overly exposed to any one sector’s performance.

Geographical diversification is another aspect to consider. Global economies and markets can have varying levels of growth and stability. Investing in international stocks and funds allows you to access investment opportunities beyond your home country and potentially benefit from different economic cycles and trends.

It’s important to note that diversification does not guarantee profits or protect against losses. However, it can help reduce the impact of market volatility and mitigate risk. It’s crucial to regularly monitor your portfolio and rebalance if necessary to maintain your desired diversification levels.

While diversification is a key strategy for risk management, it’s also important to consider your investment goals and risk tolerance when determining your diversification approach. Balancing your risk level with your desired returns is essential to achieve your financial objectives.

To implement diversification effectively, review the investment options available in your 401(k) plan and consider asset allocation strategies that align with your risk tolerance and financial goals. If you are uncertain about how to diversify your portfolio, consulting with a financial advisor can provide valuable guidance based on your specific circumstances.

In the next section, we will explore how to evaluate the performance of your investments to ensure they are meeting your expectations.

Evaluating Investment Performance

Regularly assessing the performance of your 401(k) investments is essential to ensure they are meeting your expectations and aligning with your financial goals. Evaluating investment performance allows you to make informed decisions about whether to maintain or adjust your portfolio. Here are some key factors to consider when evaluating investment performance:

Return on Investment (ROI): One of the primary indicators of investment performance is the return you have generated over a specific period. ROI measures the percentage increase or decrease in the value of your investment. Compare the ROI of your investments to relevant benchmarks, such as market indices or industry averages, to assess how well your investments are performing relative to the broader market.

Risk-adjusted returns: It’s important to consider the level of risk associated with your investments when evaluating performance. Some investments may generate higher returns, but they may also carry higher levels of risk. Assessing risk-adjusted returns allows you to determine if the potential rewards are commensurate with the risks taken.

Consistency: Assessing the consistency of an investment’s performance over time is crucial. Look beyond short-term fluctuations and focus on the long-term trend. Consistent performance is an important quality to consider when evaluating the strength of an investment.

Comparison to Investment Objectives: Evaluate how your investments are performing relative to your investment objectives. Are they meeting your desired growth rate or income targets? If they are falling short, it may be necessary to re-evaluate your investment strategy and consider adjustments to your portfolio.

Fees and Expenses: Take into account the fees and expenses associated with your investments. High fees can eat into your returns and impact your overall investment performance. Compare the fees of different investment options and assess whether the potential returns justify the costs incurred.

Market Conditions: Consider the broader market conditions when evaluating investment performance. Market fluctuations and economic factors can impact the performance of your investments. It’s important to distinguish between underperformance due to individual investments versus overall market conditions.

To evaluate the performance of your investments effectively, regularly review your account statements, which provide details on returns, fees, and overall portfolio performance. Some 401(k) platforms also provide online tools and calculators to track and analyze your investments.

While evaluating investment performance is important, it’s crucial to keep a long-term perspective and avoid making impulsive decisions based on short-term fluctuations. Investing is a marathon, not a sprint, and it’s important to stay focused on your overall investment strategy and financial goals.

In the next section, we will delve into the importance of monitoring investment expenses and how they can impact your overall returns.

Monitoring Investment Expenses

When managing your 401(k) investments, it’s crucial to keep a close eye on the expenses associated with your investments. Monitoring investment expenses is essential because high fees and costs can erode your overall investment returns over time. By understanding and controlling these expenses, you can optimize your portfolio’s performance and maximize your long-term savings.

There are several types of investment expenses you should be aware of:

- Management Fees: These fees are charged by the fund manager or company overseeing your investments. They cover the cost of managing and operating the fund. Management fees can have a significant impact on your overall returns, so it’s important to compare the fees of different investment options within your 401(k) plan.

- Expense Ratios: The expense ratio represents the percentage of a fund’s assets that goes toward covering operating expenses. This includes administrative fees, transaction costs, and management fees. Lower expense ratios generally translate to higher net investment returns, so it’s important to select funds with low expense ratios when possible.

- Transaction Costs: These costs are associated with buying and selling investments within your portfolio. They include brokerage fees, commissions, and other charges. Frequent trading or excessive turnover can substantially increase transaction costs, so it’s important to consider the impact of these expenses on your overall returns.

- Individual Service Fees: Some 401(k) plans may charge individual service fees for specific services, such as taking out a loan against your account or processing a hardship withdrawal. These fees vary depending on the plan and can add up over time, so it’s important to be aware of them and assess if the benefits outweigh the costs.

To monitor investment expenses effectively, thoroughly review the prospectuses and disclosure documents provided for each investment option. These documents provide detailed information about the fees and expenses associated with each fund or investment vehicle.

When selecting investments, compare expense ratios, management fees, and other relevant costs to find investments with competitive pricing. Over the long term, even seemingly small differences in expense ratios can significantly impact your investment returns.

It’s worth noting that while minimizing investment expenses is important, it’s equally crucial to consider the overall quality and performance of the investment options. Sometimes, investments with higher expense ratios may provide better long-term returns, so it’s important to strike a balance between expenses and performance.

Regularly monitoring investment expenses and assessing the impact on your overall returns will help you make informed decisions about your portfolio. By opting for lower-cost investments and managing transaction costs, you can effectively enhance your investment returns and maximize your 401(k) savings.

In the next section, we will explore the concept of portfolio rebalancing and its importance in maintaining a well-diversified and optimized investment strategy.

Rebalancing Your Portfolio

Rebalancing your portfolio is a vital step in managing your 401(k) investments and ensuring that your asset allocation remains aligned with your investment goals. Over time, changes in the market can cause your portfolio to deviate from your target asset allocation. Rebalancing involves adjusting the mix of investments in your portfolio back to your desired allocation percentages.

Why is rebalancing important? Asset classes perform differently at various times, meaning that the value of your investments may fluctuate and upset your original asset allocation. For example, if stocks have performed well and represent a larger percentage of your portfolio than intended, you may be taking on more risk than you are comfortable with. By rebalancing, you bring your portfolio back in line with your desired risk profile.

There are a few methods to consider when rebalancing your portfolio:

- Calendar-based: With this method, you rebalance your portfolio on a set schedule, such as annually or semi-annually. This approach provides a disciplined approach to ensure that your asset allocation remains on track. However, it may not take into account changes in market conditions or the performance of specific investments.

- Threshold-based: This method involves rebalancing your portfolio when the asset allocation deviates beyond a predetermined threshold. For example, if your target allocation for stocks is 60% and it exceeds 65%, you would rebalance to bring it back in line. This approach allows for flexibility and accounts for changes in market conditions.

- Band-based: With this method, you set upper and lower percentage limits for each asset class. When an asset class exceeds or falls below these thresholds, you rebalance to bring it back within the targeted band. This approach allows for more flexibility and reduces the need for frequent rebalancing.

When rebalancing, it’s important to consider the impact of taxes and transaction costs. Selling investments to rebalance your portfolio could result in capital gains taxes and transaction fees. To minimize taxes, you can focus on rebalancing within tax-advantaged accounts, such as your 401(k), where capital gains taxes are typically deferred until you withdraw the funds in retirement.

Additionally, as part of the rebalancing process, take the opportunity to reassess your investment strategy. Review your financial goals, risk tolerance, and time horizon to ensure they are still aligned with your current life circumstances. Consider making any necessary adjustments to your long-term investment plan.

Remember, rebalancing should not be based solely on short-term market trends or the desire to chase past performance. It’s a disciplined approach to maintain a well-diversified portfolio that aligns with your investment objectives.

Monitoring your portfolio regularly and rebalancing when appropriate helps you stay in control of your investment strategy. By keeping your asset allocation in check, you can potentially minimize the impact of market volatility and maintain a consistent approach to reaching your financial goals.

In the final section of this guide, we will discuss the importance of adjusting your investments over time to reflect changes in your financial situation and goals.

Adjusting Your Investments Over Time

As you progress through different stages of life, it’s important to periodically assess and adjust your 401(k) investments to ensure they align with your evolving financial situations and goals. Life events such as changes in income, age, and risk tolerance may warrant adjustments to your investment strategy. Here are some key considerations when adjusting your investments over time:

Changing risk tolerance: As you age, your risk tolerance may change. Younger investors typically have a longer time horizon and may be more comfortable with higher-risk investments such as stocks. However, as you approach retirement, you may want to gradually shift to more conservative investments to preserve capital and reduce exposure to market volatility. Reassess your risk tolerance periodically and adjust your asset allocation accordingly.

Life events: Significant life events, such as getting married, having children, or buying a home, can impact your financial priorities and goals. Consider how these changes may influence your risk tolerance, time horizon, and long-term objectives. Adjust your investment strategy to accommodate these new financial circumstances and ensure your portfolio reflects your updated goals.

Income changes: Changes in your income, such as a promotion or job loss, may necessitate adjustments to your investment contributions. If you have the capacity to save more, consider increasing your contributions to take advantage of potential tax benefits and accelerated growth of your retirement savings. Conversely, a decrease in income may require you to reduce your contributions temporarily until your financial situation stabilizes.

Reevaluating investment options: As the investment landscape evolves, new investment options may become available or existing options may undergo changes. It’s important to regularly evaluate the investment options offered by your 401(k) plan and assess their performance, fees, and alignment with your investment objectives. Consider if there are any new funds, target-date funds, or other investment vehicles that better suit your needs.

Regular monitoring: Continuously monitor the performance of your investments and review your portfolio’s asset allocation. Ensure that your investments are consistently aligned with your desired mix of asset classes and financial goals. Regular portfolio check-ups will help identify any areas requiring adjustment and allow you to take proactive steps to optimize your portfolio’s performance.

It’s worth noting that adjusting your investments should be done thoughtfully and with careful consideration. Avoid making knee-jerk reactions based on short-term market fluctuations and seek professional advice if you are unsure about making significant adjustments to your investments.

Remember, successfully managing your 401(k) investments is an ongoing process that requires periodic evaluation and adjustment. By actively monitoring and adjusting your investments over time, you can ensure that your portfolio remains aligned with your financial goals and provides you with the best opportunity to achieve a secure and comfortable retirement.

Seek Professional Advice if Needed

Managing your 401(k) investments can be a complex task, and it’s perfectly okay to seek professional advice if you feel overwhelmed or uncertain about making important investment decisions. While you can take an active role in managing your investments, consulting with a financial advisor or investment professional can provide you with valuable guidance and expertise.

A financial advisor can offer personalized advice based on your individual circumstances, risk tolerance, and financial goals. They can help you develop a comprehensive investment plan that aligns with your long-term objectives. They have access to research, tools, and resources that can assist in identifying appropriate investment opportunities and constructing a well-diversified portfolio.

When choosing a financial advisor, consider their credentials, experience, and area of expertise. Look for professionals who are experienced in retirement planning and have a deep understanding of 401(k) investments. Additionally, ensure that the advisor works as a fiduciary, meaning they are legally obligated to act in your best interest.

If you’re not able to work with a financial advisor directly, consider utilizing robo-advisors or online investment platforms. These digital investment platforms use algorithms to construct and manage portfolios based on your risk tolerance and goals. While they may not offer the personalized guidance of a human advisor, they can provide low-cost investment solutions and automated portfolio rebalancing.

Remember that seeking professional advice should not replace your own understanding and involvement in managing your 401(k) investments. Use the guidance of professionals to enhance your knowledge and make informed decisions, but ultimately, take ownership of your financial future.

Continually educate yourself about investing and take advantage of available resources. Take the time to understand the investment options within your 401(k) plan, review fund prospectuses, and stay informed about market trends and economic news. The more you know, the better equipped you will be to make smart investment choices.

By seeking professional advice when needed and actively engaging in the management of your 401(k) investments, you can create a solid foundation for building long-term wealth and achieving your retirement goals.

That concludes our guide on managing 401(k) investments. Remember, everyone’s financial situation is unique, and it’s important to tailor your investment strategy to your individual circumstances. May your journey towards a secure and prosperous retirement be successful!