Introduction

Welcome to WePay, a convenient and secure online payment processing platform. Whether you are running an e-commerce store, organizing a fundraising event, or collecting payments for your services, WePay makes it easy to handle transactions efficiently. Before you dive into using WePay, it’s important to understand how the platform works and the fees you may encounter along the way.

Founded in 2008, WePay is trusted by millions of individuals and businesses worldwide to handle their payment processing needs. With its robust features and user-friendly interface, WePay offers a seamless payment experience for both merchants and customers. By integrating WePay into your website or application, you can provide a convenient and secure way for users to make online payments.

In this article, we will delve into the various fees associated with WePay and discuss when and how you may be charged. Additionally, we will explore strategies to minimize fees and provide tips on understanding chargebacks and other fees that may be incurred.

It’s important to note that WePay is not a bank and does not offer traditional banking services. Instead, it acts as a payment facilitator, enabling businesses and individuals to accept payments from their customers. By partnering with major financial institutions, WePay ensures that transactions are processed securely and efficiently.

How does WePay work?

WePay simplifies the process of accepting online payments by providing merchants with an easy-to-use platform. Here’s a breakdown of how WePay works:

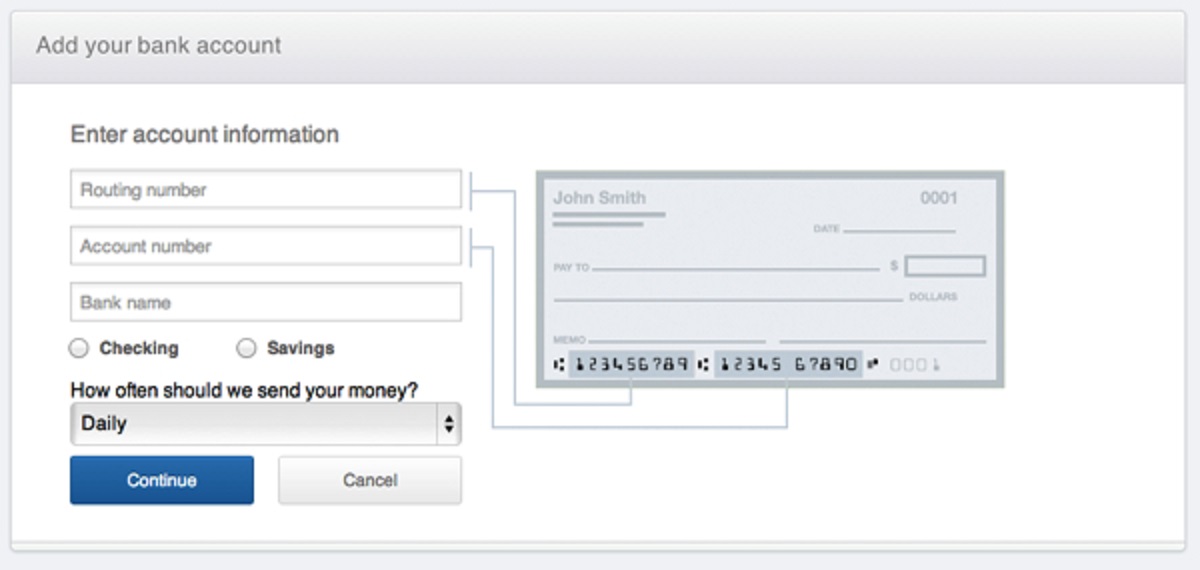

- Account Setup: To get started, you need to create a WePay account. During the registration process, you will provide basic information about your business, such as your business name, contact details, and bank account information.

- Integration: Once your account is set up, you can integrate WePay into your website or application using their robust API. This allows you to seamlessly embed WePay’s payment functionality into your platform for a smooth user experience.

- Payment Collection: When a customer makes a purchase or payment on your website, WePay securely processes the transaction. Customers can make payments using major credit cards, as well as popular digital payment methods like Apple Pay and Google Pay. WePay supports both one-time payments and recurring subscriptions, giving you flexibility in how you collect payments.

- Funds Transfer: After a successful transaction, WePay holds the funds in your account for a period of time to mitigate the risk of chargebacks or fraudulent activity. Once the hold period is over, WePay transfers the funds directly to your linked bank account, usually within a few business days.

- Reporting and Analytics: WePay provides merchants with robust reporting and analytics tools to track their payment activity. You can access detailed transaction records, view payment trends, and generate custom reports to gain valuable insights into your business’s financial performance.

Overall, WePay streamlines the payment process, ensuring that transactions are secure, reliable, and hassle-free. By leveraging its intuitive interface and comprehensive features, merchants can focus on growing their business while leaving the payment processing to WePay.

Types of fees charged by WePay

When using WePay, it’s important to understand the different types of fees that may be charged. Here are the main fees associated with WePay:

- Transaction Fees: WePay charges a fee for each transaction processed through their platform. This fee is typically a percentage of the transaction amount, although the exact rate may vary depending on factors such as your business type and transaction volume. It’s important to review WePay’s fee schedule to determine the specific transaction fee applicable to your account.

- ACH Transfer Fees: If you choose to transfer funds from your WePay account to your linked bank account using Automated Clearing House (ACH) transfers, you may incur additional fees. These fees are usually a fixed amount per transfer and can vary based on the destination bank.

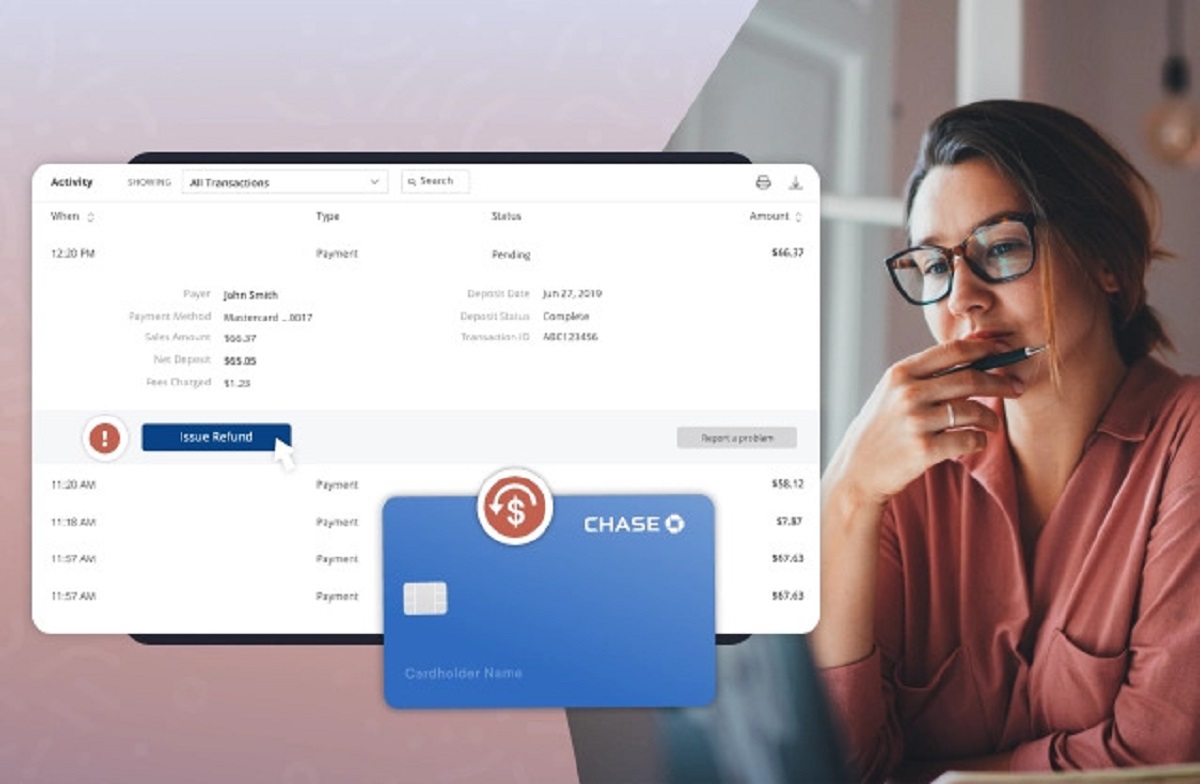

- Chargeback Fees: In the event of a chargeback, where a customer disputes a transaction and requests a refund, WePay may charge a fee to cover the administrative costs associated with resolving the dispute. Chargeback fees are typically applied per occurrence and can range from a nominal amount to a higher fee for more complex cases.

- Refund Fees: While WePay doesn’t typically charge fees for processing refunds, it’s important to note that refund transactions may still incur the original transaction fee. This means that even if you refund a customer’s payment in full, you may still be responsible for the original transaction fee associated with that payment.

It’s important to check WePay’s fee schedule and terms of service regularly, as fees may be subject to change. By understanding the different types of fees charged, you can accurately assess the costs associated with using WePay and make informed decisions about your payment processing strategies.

When are you charged for a transaction?

When using WePay, you are typically charged for a transaction at the time of processing. Here’s a breakdown of when you can expect to be charged for a transaction:

- Online Payments: For online transactions, such as purchases made on your e-commerce store or donations received through your website, the transaction fee is typically deducted immediately when the payment is processed. WePay automatically calculates and deducts the fee based on the percentage specified in their fee schedule, leaving you with the net amount.

- In-person Payments: If you are accepting payments in-person using WePay’s POS (Point of Sale) solution, the transaction fees are immediately processed at the time of the transaction. This allows you to provide a seamless checkout experience for your customers, ensuring that the payment is securely processed and the fee is deducted promptly.

- Recurring Payments: If you have set up recurring payments or subscriptions using WePay, the transaction fee will be charged for each recurring payment as it occurs. This ensures that you are billed for the fee proportionally to the revenue generated by the recurring payment on an ongoing basis.

- Hold Period: It’s important to note that WePay may place a hold on the funds for a specific duration before they are transferred to your linked bank account. This hold period is to mitigate the risk of chargebacks or fraudulent activity. During this hold period, the funds remain in your WePay account but are not accessible for immediate withdrawal.

By understanding when you will be charged for a transaction, you can anticipate the associated fees and plan your finances accordingly. It’s recommended to review your WePay account dashboard or transaction reports to stay informed about the fees deducted for each transaction and track your payment processing costs effectively.

Can you avoid fees or lower them?

While fees are an inevitable part of using any payment processing platform, there are strategies you can employ to minimize or lower the fees associated with WePay. Here are a few ways you can potentially reduce the impact of fees:

- Compare Fee Structures: Before choosing WePay or any other payment processor, it’s essential to compare fee structures and pricing options. Different processors may have varying fee rates or offer special pricing plans for specific industries or transaction volumes. By doing thorough research and comparing options, you can find a payment provider that offers competitive rates and fits your business needs.

- Optimize your Pricing Strategy: Consider adjusting your product or service pricing to factor in the transaction fees. This can help you ensure that your profit margins remain intact after deducting the fees. You can also evaluate if it makes sense to pass on a portion of the transaction fee to your customers by adjusting your pricing strategy accordingly.

- Explore Volume Discounts: If your business processes a high volume of transactions, it may be worthwhile to inquire about volume discounts with WePay. Many payment processors offer discounted rates or customized pricing plans for businesses with significant transaction volumes. Reach out to WePay’s customer support or account management team to discuss the possibility of negotiating lower fees based on your transaction volume.

- Encourage Lower-Cost Payment Methods: Some payment methods, such as bank transfers or ACH payments, may have lower processing fees compared to credit cards or digital wallets. Encourage your customers to use these lower-cost payment methods whenever possible. You can highlight the benefits of using these methods, such as faster fund availability or potential cost savings, to motivate customers to choose them.

- Monitor and Resolve Chargebacks: Chargebacks can result in additional fees, so it’s crucial to be proactive in monitoring and resolving any customer disputes or issues. By providing clear communication, exceptional customer service, and promptly addressing any concerns, you can minimize the occurrence of chargebacks and the associated fees.

- Stay Informed: Keep yourself updated on WePay’s fee schedule and any changes that may occur. By staying informed, you can adapt your strategies and pricing accordingly to optimize your fee management.

Remember that while you can take steps to minimize fees, it’s essential to strike a balance between reducing costs and providing a seamless payment experience for your customers. Finding the right balance will ensure that your revenue is maximized while maintaining professionalism and convenience for those making payments.

Understanding chargebacks and associated fees

Chargebacks can be a challenging aspect of payment processing, and it’s essential to understand how they work and the fees that may be associated with them. Here’s a breakdown of chargebacks and the potential fees involved:

When a customer disputes a transaction and requests a refund directly from their financial institution, it initiates a chargeback process. The customer may claim various reasons for the dispute, such as unauthorized charges, goods not received, or dissatisfaction with the product or service.

When a chargeback occurs, WePay is responsible for investigating the dispute on your behalf and resolving the issue. However, chargebacks can result in additional fees to cover the administrative costs associated with resolving the dispute.

The specific chargeback fees charged by WePay can vary, depending on the complexity of the case and the resources involved in resolving the dispute. It’s important to review WePay’s fee schedule to understand the potential charges you may incur for each chargeback occurrence.

To effectively manage and minimize chargebacks, consider the following strategies:

- Clear Communication: Ensure that your product or service descriptions are accurate and clearly communicate what customers can expect. By setting realistic expectations, you can minimize the likelihood of chargebacks due to misunderstandings or dissatisfaction.

- Provide Excellent Customer Service: Promptly address any customer concerns or issues to prevent them from escalating to chargebacks. Respond to inquiries in a timely manner and strive to resolve disputes amicably. Excellent customer service can go a long way in reducing the chances of chargebacks.

- Keep Detailed Records: Maintain comprehensive records of all transactions, including customer communications, order details, tracking information, and delivery confirmations. These records can serve as valuable evidence in case of a chargeback and help you provide a strong defense against disputed transactions.

- Monitor Transactions for Suspicious Activity: Regularly review your transactions for any signs of fraudulent activity. Look for unusual purchasing patterns or orders that raise suspicion. Implement fraud detection measures, such as address verification systems and IP verification, to mitigate the risk of fraudulent transactions.

- Respond to Chargebacks Promptly: When you receive a notification of a chargeback, respond promptly within the specified timeframe. Provide any necessary evidence or supporting documentation to back your case. A timely and well-documented response can improve your chances of winning the dispute and avoid additional chargeback fees.

By understanding chargebacks and implementing proactive measures to prevent them, you can minimize both the financial impact and the associated fees. It’s important to stay vigilant, educate yourself on chargeback processes, and take steps to provide a positive customer experience that reduces the likelihood of disputes and chargebacks.

Additional fees to be aware of

While WePay’s main fees are transaction fees and chargeback fees, there are a few additional fees that you should be aware of when using the platform. These fees may apply in specific situations, and understanding them will help you manage your payment processing costs effectively. Here are some of the additional fees to keep in mind:

- ACH Transfer Fees: If you choose to transfer funds from your WePay account to your linked bank account using ACH transfers, you may incur additional fees. These fees are typically a fixed amount per transfer and vary depending on the destination bank. It’s important to review the fee schedule for ACH transfers to understand the cost implications of withdrawing funds to your bank account via this method.

- Customized Pricing: Depending on your business size, industry, and specific requirements, you may opt for a customized pricing plan with WePay. While customized pricing plans offer flexibility, it’s crucial to review the terms and conditions to understand any additional fees or charges associated with these plans. Discuss the details with the WePay team to ensure you have a clear understanding of the costs involved.

- Foreign Transaction Fees: If you process payments or receive funds in a different currency than your WePay account’s default currency, additional fees may apply. These fees are usually associated with currency conversion and can vary based on the exchange rates and the specific terms outlined in WePay’s fee schedule. It’s important to consider these fees when dealing with international transactions.

- Dispute Resolution Fees: In rare cases, if a dispute or mediation process arises between you and WePay, there may be dispute resolution fees involved. These fees cover the costs associated with resolving the dispute through a third-party mediator or arbitration service.

- Additional Services: WePay offers various additional services and integrations that can enhance your payment processing capabilities. While some of these services may come at an additional cost, they can provide value-added features tailored to your business needs. It’s important to review the pricing details for any additional services you choose to leverage.

Understanding these additional fees and considering them in your overall payment processing strategy will help you accurately calculate costs and plan your finances. It’s crucial to familiarize yourself with WePay’s fee schedule, terms of service, and any updates or changes they may communicate to ensure transparency and effective management of fees.

Conclusion

WePay offers a convenient and reliable payment processing solution for businesses and individuals. By understanding how WePay works and the fees involved, you can effectively manage your payment processing costs while providing a seamless experience for your customers.

In this article, we explored the various fees charged by WePay, including transaction fees, ACH transfer fees, chargeback fees, and refund fees. We discussed strategies for avoiding or lowering fees, such as comparing fee structures, optimizing pricing strategies, exploring volume discounts, and encouraging lower-cost payment methods.

We also highlighted the importance of understanding chargebacks and associated fees, providing tips on preventing chargebacks through clear communication, excellent customer service, and record-keeping. Additionally, we mentioned the additional fees to be aware of, such as ACH transfer fees, customized pricing fees, foreign transaction fees, dispute resolution fees, and fees for additional services.

By staying informed, monitoring your transactions, and proactively managing your payment processing, you can effectively navigate WePay’s fees and ensure that your revenue and customer experiences remain at the forefront. Always consult WePay’s official fee schedule and terms of service for the most up-to-date information on fees.

Remember, WePay is committed to providing a secure and reliable payment platform, and understanding the fees associated with their services will help you make informed decisions and optimize your payment processing experience. By using WePay strategically, you can focus on growing your business while ensuring efficient and seamless payment transactions.