Introduction

Managing your bank balance and QuickBooks balance effectively is crucial for the financial health of your business. However, it is not uncommon to encounter discrepancies between these two balances. This discrepancy can cause confusion and make it challenging to keep accurate track of your financial records.

Understanding why your bank balance may differ from your QuickBooks balance is essential for resolving any issues and maintaining accurate financial records. In this article, we will explore the common causes of discrepancies between your bank balance and QuickBooks balance and provide tips to help you resolve them.

It is important to note that while QuickBooks is a powerful accounting software, it relies on accurate and up-to-date data. Therefore, discrepancies can arise due to various factors such as outstanding checks, deposits in transit, reconciliation errors, bank fees, data entry errors, uncleared transactions, and even fraudulent activity. By understanding these causes and implementing proper strategies, you can ensure that your bank balance aligns with your QuickBooks balance and maintain accurate financial records.

Now, let’s dive into the main causes of differences between your bank balance and QuickBooks balance.

Causes of Difference between Bank Balance and QuickBooks Balance

There are several factors that can contribute to a difference between your bank balance and QuickBooks balance. Let’s examine each of these causes in detail:

- Outstanding Checks: When you write a check and it hasn’t been cashed or processed by the bank, it creates a discrepancy between your bank balance and QuickBooks balance. These outstanding checks need to be accounted for and reconciled to ensure accuracy.

- Deposits in Transit: Similar to outstanding checks, deposits in transit refer to funds that you’ve deposited but haven’t been cleared by the bank. These deposits can cause a difference between your bank balance and QuickBooks balance until they are processed and reflected in your bank account.

- Reconciliation Errors: Mistakes during the reconciliation process can also lead to discrepancies. It’s important to double-check the reconciliation reports and ensure that all transactions are properly marked as cleared or unreconciled.

- Bank Fees and Service Charges: Your bank may charge fees or deduct service charges, which can impact your bank balance. If these fees are not recorded in QuickBooks, it can result in a difference between the two balances.

- Uncleared Transactions: Transactions that are recorded in QuickBooks but have not yet cleared the bank can cause a discrepancy. This can include checks or electronic payments that are still in transit or pending clearance.

- Data Entry Errors: Human error during data entry can lead to discrepancies between your bank balance and QuickBooks balance. It’s essential to review and double-check all transactions entered into QuickBooks to ensure accuracy.

- Fraudulent Activity or Unauthorized Transactions: Unfortunately, fraudulent activity or unauthorized transactions can occur, causing a difference between your bank balance and QuickBooks balance. It’s crucial to monitor your accounts regularly for any suspicious activity and report it to your bank immediately.

Identifying these causes can help you uncover the root of the discrepancy and take appropriate steps to reconcile the two balances. In the next section, we will explore practical tips to resolve any differences between your bank balance and QuickBooks balance.

Outstanding Checks

Outstanding checks refer to checks that you have issued, but the recipient has not yet cashed or deposited. These checks can create a discrepancy between your bank balance and QuickBooks balance since the funds have not been deducted from your account.

To address outstanding checks, follow these steps:

- Review your outstanding checks report in QuickBooks to identify any checks that have not been cleared.

- Contact the recipients of these outstanding checks to inquire about the status and remind them to deposit or cash the checks.

- Once the checks have been cleared by the bank, update your QuickBooks records to mark them as reconciled.

- Regularly reconcile your bank accounts in QuickBooks to ensure that all outstanding checks are accounted for and properly reflected in your balance.

By taking these steps, you can ensure that outstanding checks are properly addressed, and the discrepancy between your bank balance and QuickBooks balance is resolved.

Deposits in Transit

Deposits in transit are funds that you have deposited but have not yet been credited to your bank account. These deposits can cause a difference between your bank balance and QuickBooks balance, as the funds are still in transit and haven’t been processed by the bank.

To address deposits in transit, follow these steps:

- Access your bank statement and compare it to your records in QuickBooks to identify any deposits that have not yet cleared.

- Contact your bank to inquire about the status of these deposits and when they are expected to be credited to your account.

- Once the deposits have been credited and cleared by the bank, update your QuickBooks records to reflect the cleared deposits.

- Regularly reconcile your bank accounts in QuickBooks to ensure that all deposits in transit are properly accounted for and reflected in your balance.

By addressing deposits in transit promptly and ensuring they are properly credited to your account, you can reconcile the difference between your bank balance and QuickBooks balance.

Reconciliation Errors

Reconciliation errors can occur during the process of comparing transactions in your bank statement to the entries in your QuickBooks account. These errors can lead to discrepancies between your bank balance and QuickBooks balance if the reconciliation is not completed accurately.

To address reconciliation errors, follow these steps:

- Review your bank reconciliation report in QuickBooks to identify any discrepancies or errors.

- Carefully compare the transactions in your bank statement with the entries in QuickBooks to ensure they match.

- If you identify any errors or discrepancies, correct them in QuickBooks by adjusting the transactions or reclassifying them if necessary.

- Reconcile your bank accounts in QuickBooks again to ensure that all transactions are accurately marked as cleared or unreconciled.

Regularly reviewing and correcting reconciliation errors will help ensure that your bank balance aligns with your QuickBooks balance. By maintaining accurate reconciliation records, you can prevent future discrepancies and have more confidence in the accuracy of your financial records.

Bank Fees and Service Charges

Bank fees and service charges are common expenses that can impact your bank balance. If these fees and charges are not properly recorded in QuickBooks, it can result in a discrepancy between your bank balance and QuickBooks balance.

To address bank fees and service charges, follow these steps:

- Review your bank statements and identify any fees or service charges deducted by your bank.

- Create appropriate expense transactions in QuickBooks to record these fees and charges. Make sure to categorize them correctly to reflect the nature of the expense.

- Regularly reconcile your bank accounts in QuickBooks to ensure that all bank fees and service charges are accurately recorded and reconciled.

- If you notice any discrepancies between the fees charged by the bank and those recorded in QuickBooks, investigate and resolve the issue by adjusting the transactions accordingly.

By accurately recording and reconciling bank fees and service charges in QuickBooks, you can ensure that your bank balance and QuickBooks balance align. This will provide a clearer picture of your financial status and help you make informed business decisions.

Uncleared Transactions

Uncleared transactions are transactions that have been recorded in QuickBooks but have not yet cleared your bank. These transactions, such as checks or electronic payments, can cause a discrepancy between your bank balance and QuickBooks balance until they are processed and reflected in your bank account.

To address uncleared transactions, follow these steps:

- Review your bank statement and compare it to the transactions in QuickBooks to identify any uncleared transactions.

- Contact your bank to inquire about the status of these transactions and when they are expected to clear.

- Once the transactions have cleared the bank, update your QuickBooks records to mark them as cleared.

- Regularly reconcile your bank accounts in QuickBooks to ensure that all uncleared transactions are properly accounted for and reflected in your balance.

By addressing uncleared transactions promptly and ensuring they are properly reflected in your QuickBooks records, you can reconcile the difference between your bank balance and QuickBooks balance and maintain accurate financial records.

Data Entry Errors

Data entry errors can occur when manually entering transactions into QuickBooks. These errors can lead to discrepancies between your bank balance and QuickBooks balance if the incorrect information is recorded.

To address data entry errors, follow these steps:

- Regularly review your transactions in QuickBooks to identify any potential data entry errors.

- Compare the transactions in QuickBooks to your supporting documentation, such as bank statements or receipts, to ensure accuracy.

- If you discover any data entry errors, correct them in QuickBooks by editing the respective transactions.

- Reconcile your bank accounts in QuickBooks to ensure that the corrected transactions are properly reflected in your balance.

By being diligent in reviewing and correcting data entry errors, you can ensure that your bank balance aligns with your QuickBooks balance. Accurate data entry is essential for maintaining reliable financial records and making informed business decisions.

Fraudulent Activity or Unauthorized Transactions

Unfortunately, fraudulent activity or unauthorized transactions can occur, leading to a difference between your bank balance and QuickBooks balance. These actions can result in unauthorized withdrawals or charges that are not reflected in your QuickBooks records.

To address fraudulent activity or unauthorized transactions, follow these steps:

- Regularly monitor your bank accounts for any suspicious or unauthorized transactions. If you notice any discrepancies, contact your bank immediately to report the fraudulent activity.

- Work with your bank to investigate the unauthorized transactions and take the necessary steps to secure your account.

- Once the fraudulent transactions have been resolved with your bank, reconcile your bank accounts in QuickBooks to ensure that your QuickBooks balance reflects the corrected transactions.

- Consider implementing additional security measures such as using two-factor authentication, regularly updating passwords, and monitoring account activity to prevent future fraudulent activity.

By promptly addressing and reporting fraudulent activity or unauthorized transactions, you can minimize the impact on your bank balance and maintain the accuracy of your QuickBooks records. Staying vigilant and taking preventive measures will help safeguard your financial information and protect your business from fraudulent activities.

Tips to Resolve Difference between Bank Balance and QuickBooks Balance

Resolving the difference between your bank balance and QuickBooks balance is essential for accurate financial management. Here are some tips to help you address and reconcile the discrepancies:

- Reconcile Accounts Regularly: Make it a habit to reconcile your bank accounts in QuickBooks regularly. This process involves comparing your bank statement transactions to the entries in QuickBooks and ensuring they match. Regular reconciliation will help identify and resolve discrepancies in a timely manner.

- Review and Correct Reconciliation Errors: Carefully review your bank reconciliation reports in QuickBooks to identify any errors or discrepancies. If you find any, promptly correct them by adjusting the transactions or reclassifying them correctly.

- Update and Sync Bank Feeds: Keep your bank feeds updated in QuickBooks by syncing your accounts regularly. This ensures that your QuickBooks records are up to date and reflect the latest transactions in your bank account.

- Audit and Verify Uncleared Transactions: Pay close attention to uncleared transactions in QuickBooks, such as outstanding checks or deposits in transit. Timely follow-up with the relevant parties or your bank to ensure these transactions are properly cleared and reflected in your balance.

- Double-Check Data Entry and Categorization: Accurate data entry is crucial to avoid discrepancies. Take the time to double-check the entered transactions in QuickBooks, ensuring that the amounts, dates, and categories are entered correctly.

- Monitor and Report Fraudulent Activities: Regularly monitor your bank accounts for any suspicious or unauthorized transactions. If you notice any fraudulent activity, promptly report it to your bank and take the necessary steps to secure your accounts.

By implementing these tips, you can effectively resolve the difference between your bank balance and QuickBooks balance. Maintaining accurate records and addressing discrepancies promptly will provide you with a reliable financial picture and help you make informed business decisions.

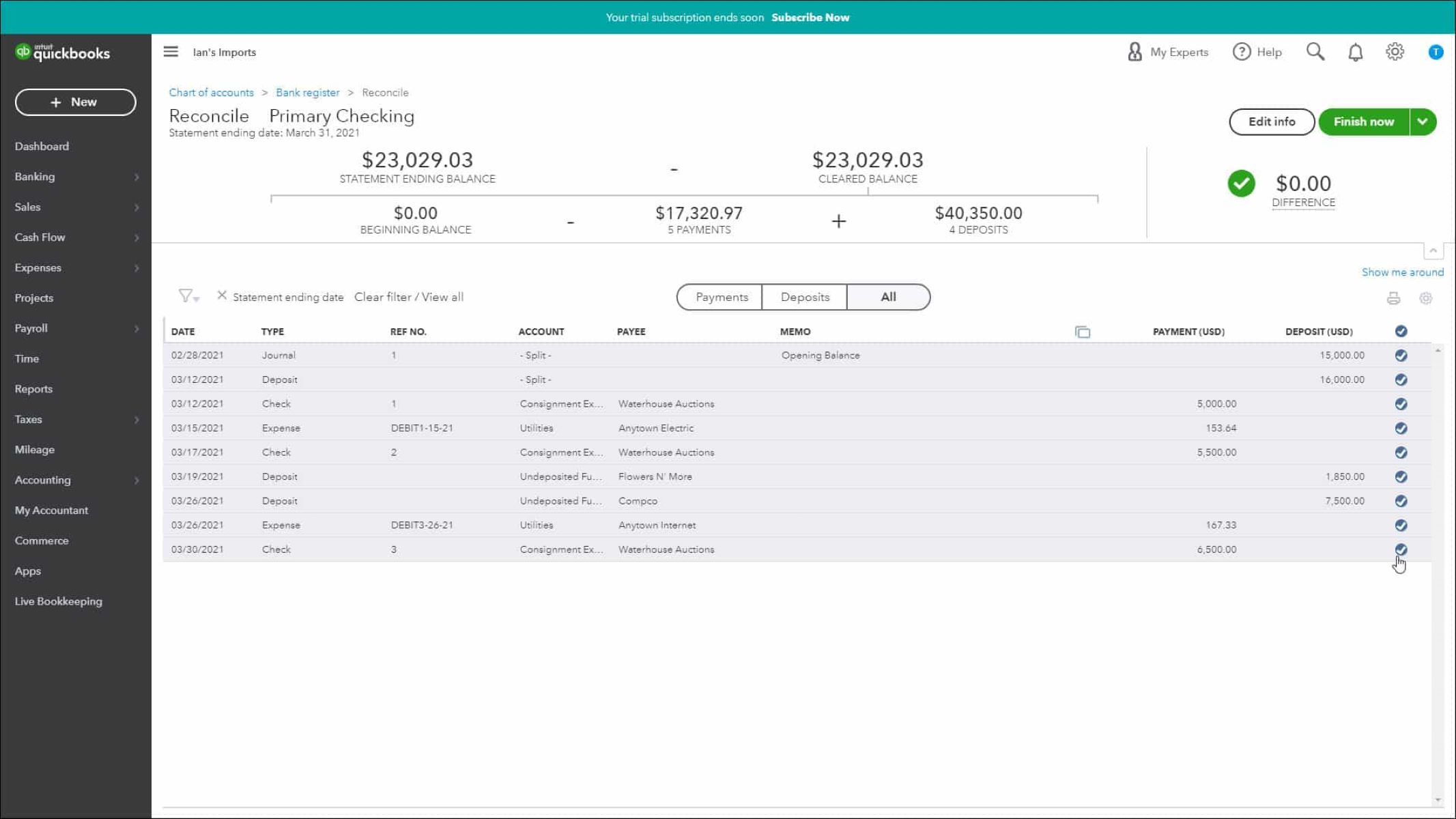

Reconcile Accounts Regularly

One of the most important steps to resolve the difference between your bank balance and QuickBooks balance is to reconcile your accounts regularly. Reconciliation is the process of comparing your bank statement transactions to the entries in QuickBooks and ensuring they match. Regular reconciliation helps identify and rectify any discrepancies in a timely manner.

Here are some key points to consider when reconciling your accounts:

- Establish a Reconciliation Schedule: Set a specific schedule for reconciling your bank accounts in QuickBooks. This could be monthly, quarterly, or even more frequently, depending on the volume of transactions and the complexity of your business.

- Gather Your Bank Statements: Collect all the bank statements for the period you are reconciling. This includes both paper statements and electronic statements, such as PDFs or online banking records.

- Compare Transactions: Go through each transaction listed in your bank statement and compare it to the corresponding entry in QuickBooks. Check for any discrepancies or omissions.

- Mark Cleared Transactions: Once you have verified that a transaction in your bank statement matches the one in QuickBooks, mark it as cleared in your QuickBooks account. This indicates that the transaction has been accounted for and matches the bank records.

- Reconcile Discrepancies: If you come across any discrepancies between your bank statement and QuickBooks, investigate the cause of the discrepancy. This could be due to an error in data entry, an uncaptured transaction, or a timing difference. Rectify the discrepancy by adjusting the transaction or adding the missing entry in QuickBooks.

- Finalize the Reconciliation: Once you have completed the reconciliation process and rectified any discrepancies, finalize the reconciliation in QuickBooks. This ensures that the reconciled transactions are marked as complete and helps maintain an accurate balance going forward.

By reconciling your accounts regularly, you can identify and address any differences between your bank balance and QuickBooks balance. This practice not only promotes accuracy in your financial records but also provides a clear picture of your business’s financial health.

Review and Correct Reconciliation Errors

During the reconciliation process, it’s essential to review your bank reconciliation reports in QuickBooks and address any errors or discrepancies. It is not uncommon for mistakes to occur, such as data entry errors or mismatches between bank records and QuickBooks transactions. By promptly identifying and correcting reconciliation errors, you can ensure that your bank balance aligns with your QuickBooks balance.

Here are some steps to help you review and correct reconciliation errors:

- Review Bank Reconciliation Reports: Access your bank reconciliation reports in QuickBooks and carefully examine each transaction listed. Pay attention to any discrepancies or errors that need to be addressed.

- Compare Bank Statements and QuickBooks Entries: Take your bank statements for the reconciliation period and cross-reference them with the corresponding entries in QuickBooks. Verify that the amounts, dates, and transaction details match accurately.

- Identify Reconciliation Errors: If you discover any discrepancies between the bank statement and QuickBooks, highlight them as potential reconciliation errors. Common errors include missed transactions, incorrect amounts, or improperly categorized entries.

- Correct the Errors: Once you have identified the reconciliation errors, take the necessary steps to correct them. Depending on the nature of the error, you may need to adjust the transaction amount, edit the transaction details, or reclassify the entry to the correct account.

- Reconcile Again: After making the corrections, reconcile your bank accounts in QuickBooks once more to ensure that the adjustment has been incorporated accurately. This allows you to verify that the corrected transactions are now correctly reflected in the reconciliation process.

- Maintain Accurate Records: As you rectify reconciliation errors, make sure to keep detailed documentation of the changes you’ve made. This will help you maintain accurate records and provide a clear audit trail if needed in the future.

By diligently reviewing and correcting reconciliation errors, you can ensure that the difference between your bank balance and QuickBooks balance is resolved. Taking these steps will help you maintain accurate financial records, strengthen the integrity of your accounting system, and make more informed business decisions.

Update and Sync Bank Feeds

Keeping your bank feeds updated in QuickBooks is crucial to ensure that your financial records accurately reflect your bank transactions. The process of updating and syncing bank feeds involves retrieving and importing the latest transaction data from your bank into QuickBooks. By regularly updating and syncing your bank feeds, you can reduce discrepancies between your bank balance and QuickBooks balance.

Here are some steps to help you update and sync bank feeds:

- Connect your Bank Account: Connect your bank account to QuickBooks by providing the necessary login credentials and granting permission for QuickBooks to access your account information securely.

- Set up Automatic Updates: Take advantage of QuickBooks’ automatic update feature to schedule regular updates of your bank feeds. This ensures that your transaction data stays up to date without requiring manual intervention.

- Manually Sync Bank Feeds: If you prefer manual control over updating bank feeds, you can initiate the sync manually. Navigate to the banking section in QuickBooks and select the option to manually update your bank feeds.

- Review and Categorize Transactions: Once your bank feeds are updated, review the imported transactions in QuickBooks. Ensure that they are correctly categorized, match the purpose of the transaction, and align with your accounting practices.

- Reconcile Bank Transactions: As you review and categorize the updated bank transactions, cross-check them with your bank statements. Reconcile any discrepancies between the imported transactions and the statement records.

- Resolve Sync Errors: If you encounter any errors during the syncing process or notice missing transactions, take the necessary steps to address them. This might involve troubleshooting connectivity issues, reaching out to your bank’s support, or seeking assistance from QuickBooks customer support.

By ensuring that your bank feeds are regularly updated and accurately synchronized with QuickBooks, you can minimize discrepancies and maintain a reliable record of your financial transactions. This helps to improve the accuracy of your bank balance and QuickBooks balance, providing a clear and up-to-date view of your business’s financial health.

Audit and Verify Uncleared Transactions

Uncleared transactions, such as outstanding checks or deposits in transit, can contribute to the difference between your bank balance and QuickBooks balance. It’s crucial to regularly audit and verify these transactions to ensure accuracy in your financial records and reconcile the discrepancy.

Here are the steps to audit and verify uncleared transactions:

- Review Uncleared Transactions: Access your QuickBooks account and navigate to the uncleared transactions section. This will provide you with a list of transactions that have not yet been cleared by the bank.

- Retrieve Supporting Documentation: Gather the necessary supporting documentation for these uncleared transactions. This may include copies of checks, deposit slips, or other relevant records that confirm the existence and validity of these transactions.

- Contact the Bank: Reach out to your bank to inquire about the status of these transactions. Confirm if they have been processed or if there are any issues delaying their clearance.

- Update Cleared Transactions: Once the transactions have been confirmed as cleared by the bank, update your QuickBooks records accordingly. Mark these transactions as cleared to reflect them accurately in your QuickBooks balance.

- Reconcile Again: After updating the cleared transactions, reconcile your bank accounts in QuickBooks to ensure that all uncleared transactions are now properly accounted for and the discrepancy between your bank balance and QuickBooks balance is resolved.

- Investigate Discrepancies: If any discrepancies or issues arise during the audit and verification process, thoroughly investigate the cause. This might involve tracing missing transactions, validating the accuracy of data entry, or reconciling timing differences.

By conducting regular audits and verifying uncleared transactions, you can ensure that your financial records are accurate and up to date. This helps prevent the discrepancy between your bank balance and QuickBooks balance, providing a clear picture of your business’s financial position.

Double-Check Data Entry and Categorization

Data entry errors and incorrect categorization can contribute to differences between your bank balance and QuickBooks balance. It is crucial to double-check the accuracy of data entry and ensure the proper categorization of transactions to maintain reliable financial records and reconcile the discrepancy.

Here are some steps to help you double-check data entry and categorization:

- Verify Transaction Details: When entering transactions into QuickBooks, ensure that all the details, such as dates, amounts, and payees, are entered accurately. Take an extra moment to review the information before saving the transaction.

- Compare to Source Documents: Cross-reference the entered transactions in QuickBooks with their corresponding source documents, such as receipts or bank statements. Verify that the information matches and accurately represents the original transaction.

- Review Account Categorization: Double-check the categorization of each transaction to ensure that it is assigned to the correct account in QuickBooks. Mis-categorized transactions can contribute to discrepancies between your bank balance and QuickBooks balance.

- Use Appropriate Labels and Descriptions: Provide clear and descriptive labels or descriptions for each transaction. This can help you easily identify and review transactions, reducing the chance of mistakes in data entry or categorization.

- Reconcile Regularly: Reconcile your bank accounts in QuickBooks on a regular basis to catch any data entry errors or categorization mistakes. The reconciliation process allows you to compare your bank statement transactions with the corresponding entries in QuickBooks, increasing the likelihood of identifying and rectifying any discrepancies.

- Perform Periodic Reviews: Set aside time regularly to perform reviews of your transaction data in QuickBooks. This helps identify any potential errors or inconsistencies that may have been overlooked during the initial data entry.

By taking the time to double-check data entry and categorization, you can significantly reduce the chances of errors and discrepancies between your bank balance and QuickBooks balance. Accurate data entry and categorization contribute to reliable financial records, helping you make informed business decisions based on accurate financial information.

Monitor and Report Fraudulent Activities

Monitoring your bank accounts for fraudulent activities is crucial to protect your financial records and prevent discrepancies between your bank balance and QuickBooks balance. Unfortunately, fraudulent activities, such as unauthorized transactions or identity theft, can occur. Being vigilant and proactive in detecting and reporting fraudulent activities can help minimize the impact on your accounts and maintain accurate financial records.

Here are some steps to help you monitor and report fraudulent activities:

- Regularly Review Account Activity: Monitor your bank accounts regularly for any suspicious or unauthorized transactions. Keep an eye out for unfamiliar payees, unexpected withdrawals, or any other activity that doesn’t align with your usual banking patterns.

- Set Up Fraud Alerts: Take advantage of your bank’s fraud alert system. Many banks offer options to receive alerts via text message or email for any suspicious activity on your account. Enable these alerts to stay informed about any potential fraudulent activities.

- Report Suspected Fraud: If you notice any fraudulent or unauthorized transactions, immediately report them to your bank. Contact your bank’s fraud department, provide them with the details of the suspicious activity, and follow their instructions to resolve the issue.

- Secure Your Accounts: Strengthen the security measures for your bank accounts. Use strong and unique passwords, enable two-factor authentication, and regularly update your login credentials. These measures can make it more difficult for unauthorized individuals to access your accounts.

- Keep Documentation: Maintain detailed documentation of any suspected fraudulent activities. This documentation can include transaction details, correspondence with your bank, and any other relevant information. Having thorough records will assist in the investigation and resolution process.

- Report to Law Enforcement: If the fraudulent activities are significant or involve identity theft, consider filing a report with your local law enforcement agency. Provide them with all the necessary information and cooperate with their investigation.

By monitoring your bank accounts regularly and promptly reporting any suspected fraudulent activities, you can take proactive steps to safeguard your financial records. This helps minimize discrepancies between your bank balance and QuickBooks balance and maintains the integrity of your financial data.

Conclusion

Resolving the difference between your bank balance and QuickBooks balance is crucial for accurate financial management. Understanding the causes of these discrepancies and implementing the appropriate steps can help you maintain reliable financial records and make informed business decisions.

In this article, we explored several common causes of differences between your bank balance and QuickBooks balance. These include outstanding checks, deposits in transit, reconciliation errors, bank fees and service charges, uncleared transactions, data entry errors, and fraudulent activities. By identifying these causes, you can take targeted actions to reconcile the discrepancies and ensure the accuracy of your financial records.

We provided practical tips to help you resolve the difference between your bank balance and QuickBooks balance. These tips include reconciling accounts regularly, reviewing and correcting reconciliation errors, updating and syncing bank feeds, auditing and verifying uncleared transactions, double-checking data entry and categorization, and monitoring and reporting fraudulent activities.

By following these tips and maintaining diligence in your financial management practices, you can improve the accuracy of your bank balance and ensure it aligns with your QuickBooks balance. This, in turn, allows you to have an up-to-date and clear view of your business’s financial health.

Remember, regularly reconciling your accounts, double-checking data entry, monitoring your bank accounts for fraudulent activities, and promptly reporting any discrepancies are essential steps in maintaining accurate financial records and safeguarding your business’s financial well-being.

By implementing these strategies, you can maintain financial accuracy, make informed decisions, and ensure the smooth operation of your business.