Introduction

Reconciliation is an essential process for businesses to ensure the accuracy of their financial records. It involves comparing and matching transactions between a company’s bank statements and its accounting software, such as QuickBooks Online. By reconciling these accounts, businesses can identify any discrepancies or errors and take the necessary steps to correct them.

Accurate financial records are crucial for making informed business decisions, preparing financial statements, and ensuring compliance with tax regulations. Without proper reconciliation, errors or missing transactions can go unnoticed, leading to inaccurate financial reporting, potential cash flow problems, and even legal consequences.

In this article, we will discuss the importance of reconciliation and provide a step-by-step guide on how to reconcile your QuickBooks Online account. Whether you are a small business owner, a bookkeeper, or an accountant, mastering the process of reconciliation will help you maintain accurate financial records and gain a clear understanding of your company’s financial health.

Throughout the article, we will provide practical tips and insights to help you streamline the reconciliation process and avoid common pitfalls. So, let’s dive in and learn how to effectively reconcile your QuickBooks Online account!

What is Reconciliation

Reconciliation is the process of comparing and matching financial transactions between your bank statements and your accounting software, such as QuickBooks Online. It ensures that the records in your accounting system accurately reflect the transactions recorded by your bank. Reconciliation involves verifying the accuracy and completeness of both sets of records and resolving any discrepancies or errors that may arise.

During the reconciliation process, you will compare the transactions listed on your bank statement to the ones recorded in QuickBooks Online to ensure they match. This includes comparing deposits, withdrawals, checks, and any other transactions. The goal is to identify any discrepancies or missing transactions that may occur due to timing differences or errors in data entry.

Reconciliation is not just about matching numbers; it’s about ensuring the overall accuracy of your financial records. It helps you catch errors or fraudulent activities, such as unauthorized transactions or duplicate entries, that may affect your financial statements or cash flow. By regularly reconciling your accounts, you can spot and rectify these issues promptly.

Additionally, reconciliation provides businesses with a clear and up-to-date picture of their financial health. It allows you to analyze your cash flow, track expenses, and monitor income. This information is crucial for making informed business decisions, identifying potential risks or opportunities, and maintaining financial stability.

Besides bank reconciliation, there are other types of reconciliation that businesses may need to perform. These include credit card reconciliation, merchant account reconciliation, and accounts receivable reconciliation. Each type has its own unique challenges and requirements, but the underlying goal is always to ensure accuracy and consistency in financial records.

In the next section, we will explore the importance of reconciliation and how it can benefit your business.

Why is Reconciliation Important

Reconciliation plays a crucial role in maintaining accurate financial records and ensuring the overall financial health of your business. Here are several reasons why reconciliation is important:

1. Accuracy of Financial Records: Reconciliation helps ensure the accuracy and integrity of your financial records. By comparing and matching transactions between your bank statements and accounting software, you can identify any discrepancies or errors that might have occurred. This ensures that your financial statements, such as your balance sheet and income statement, reflect the true financial position of your business.

2. Fraud Detection: Regular reconciliation can help you detect and prevent fraudulent activities, such as unauthorized transactions or duplicate entries. By carefully reviewing and comparing your bank statements and accounting records, you can identify any suspicious or unusual transactions that may indicate fraudulent behavior. Prompt detection of fraud can minimize financial losses and protect the financial well-being of your business.

3. Cash Flow Management: Reconciliation allows you to track and manage your cash flow effectively. By comparing your bank statements to your accounting records, you can monitor incoming and outgoing cash, identify any discrepancies, and take necessary actions to improve cash flow. This helps you ensure that you have sufficient funds to cover expenses, pay vendors, and meet other financial obligations.

4. Decision-Making: Accurate and up-to-date financial records are essential for making informed business decisions. Reconciliation provides you with a clear understanding of your revenue, expenses, and overall financial position. With this information at hand, you can make strategic decisions related to budgeting, forecasting, and investment. Reconciliation also helps you measure the effectiveness of your business strategies and identify areas where you can improve efficiency and profitability.

5. Compliance and Auditing: Reconciliation is crucial for compliance with regulatory requirements and tax obligations. By maintaining accurate financial records through regular reconciliation, you can ensure that your business remains compliant with relevant rules and regulations. In addition, if you are audited by tax authorities or undergo a financial review, having well-reconciled records will simplify the process and demonstrate your commitment to financial transparency.

6. Building Credibility: Accurate and reconciled financial records enhance your business’s credibility and trustworthiness. When dealing with investors, lenders, or potential partners, having reliable financial information demonstrates your commitment to sound financial management. This can help you secure financing, negotiate favorable terms, and build strong business relationships.

Overall, reconciliation is a critical process that ensures the accuracy, integrity, and reliability of your financial records. It enables you to make informed decisions, detect fraud, manage cash flow effectively, meet compliance requirements, and build credibility for your business.

Step 1: Gather the necessary information

Before you begin the reconciliation process in QuickBooks Online, it’s essential to gather all the necessary information and documents. This step will ensure that you have everything you need to reconcile your accounts accurately. Here’s what you’ll need:

1. Bank statements: Obtain your bank statements for the period you wish to reconcile. This may include monthly statements or statements covering a specific timeframe, such as a quarter or a year. Make sure you have the most recent statement available.

2. QuickBooks Online access: Ensure you have access to your QuickBooks Online account. This includes having your username and password ready. If you are using the services of a bookkeeper or an accountant, coordinate with them to ensure access to the relevant QuickBooks Online account.

3. List of transactions: Compile a list of transactions recorded in QuickBooks Online for the period you are reconciling. This includes deposits, withdrawals, checks, and any other transactions that were recorded during that time frame.

4. Supporting documents: Gather any supporting documents, such as receipts, invoices, and bank statements, that correspond to the transactions recorded in QuickBooks Online. These documents can serve as evidence and help in case of any discrepancies or irregularities.

5. Notebook or spreadsheet: Keep a notebook or use a spreadsheet to jot down notes, record calculations, and track your progress throughout the reconciliation process. This will help you stay organized and document any issues or adjustments that need to be made.

6. Clear understanding of reconciliation process: Familiarize yourself with the reconciliation process in QuickBooks Online. Make sure you understand the steps involved and any specific features or functions that the software offers for this process. This will help you navigate through the reconciliation process smoothly.

7. Dedicated time and focus: Set aside dedicated time for the reconciliation process. Choose a time when you can focus without distractions and give your full attention to the task at hand. Reconciliation requires concentration and precision, so allocate enough time to complete the process thoroughly.

Gathering all the necessary information and documents before starting the reconciliation process will streamline the process and help you avoid unnecessary delays or errors. Once you have everything you need, you can move on to the next step: reviewing and comparing your bank statements and QuickBooks Online transactions.

Step 2: Review and compare bank statements and QuickBooks Online

Once you have gathered all the necessary information, it’s time to review and compare your bank statements with the transactions recorded in QuickBooks Online. This step is crucial to identify any discrepancies or errors that may have occurred. Follow these steps to review and compare the two sets of records:

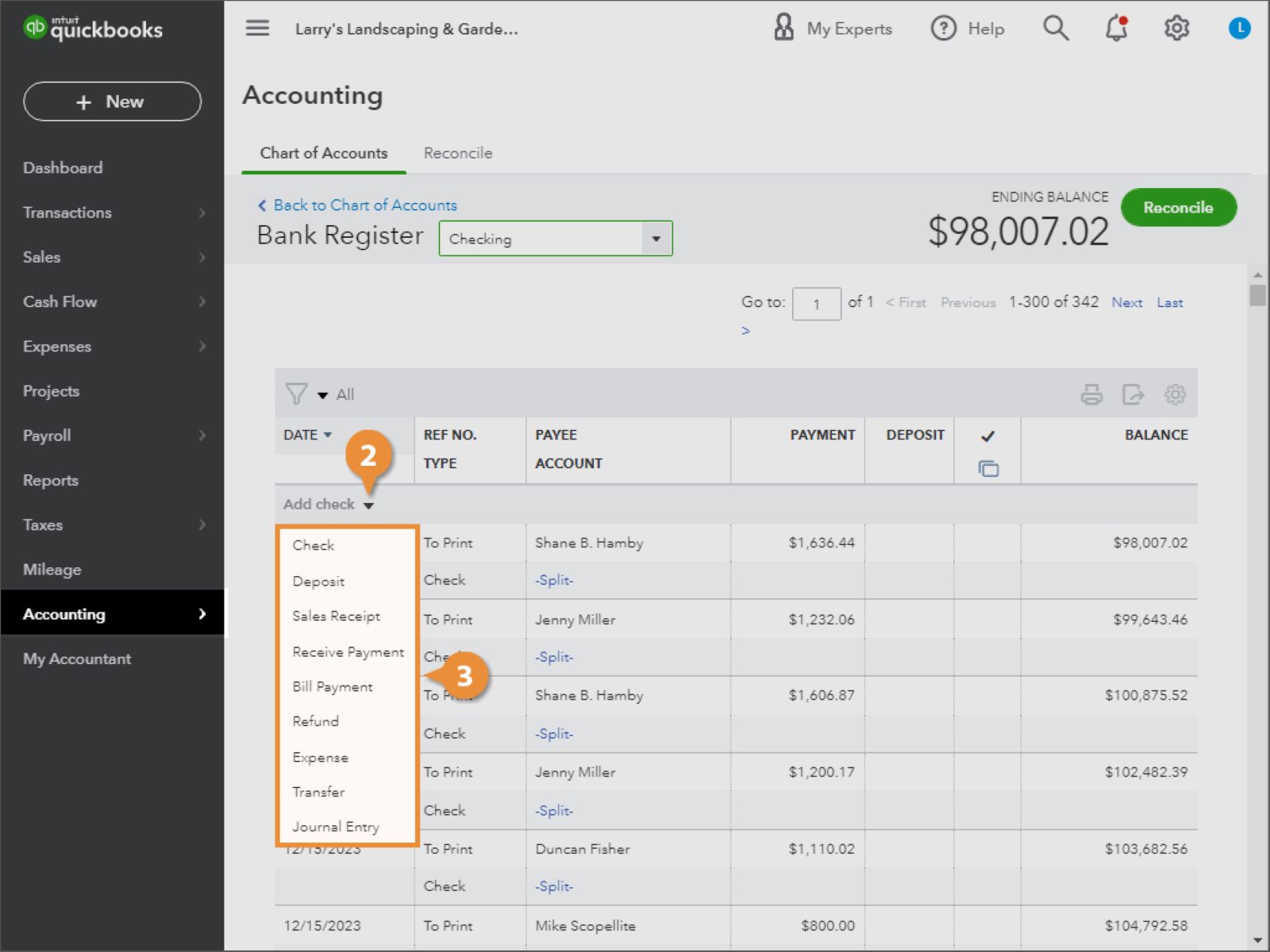

1. Open QuickBooks Online: Log in to your QuickBooks Online account using your credentials. Navigate to the Banking or Transactions section, where you can access the transactions recorded in the software.

2. Retrieve the bank statements: Open the bank statements for the period you are reconciling. Ensure you have the most recent statement available. This can be in the form of a paper statement, a PDF download, or an electronic statement provided by your bank.

3. Check for matching transactions: Start by comparing the transactions listed on your bank statement with the transactions recorded in QuickBooks Online. Look for matching amounts, dates, and descriptions. Be consistent and meticulous in your comparisons to ensure accurate reconciliation.

4. Note any discrepancies: As you review the transactions, make note of any discrepancies or inconsistencies between the bank statement and QuickBooks Online records. These may include missing transactions, different amounts, or discrepancies in the dates or descriptions. Note any discrepancies in your notebook or spreadsheet for future reference.

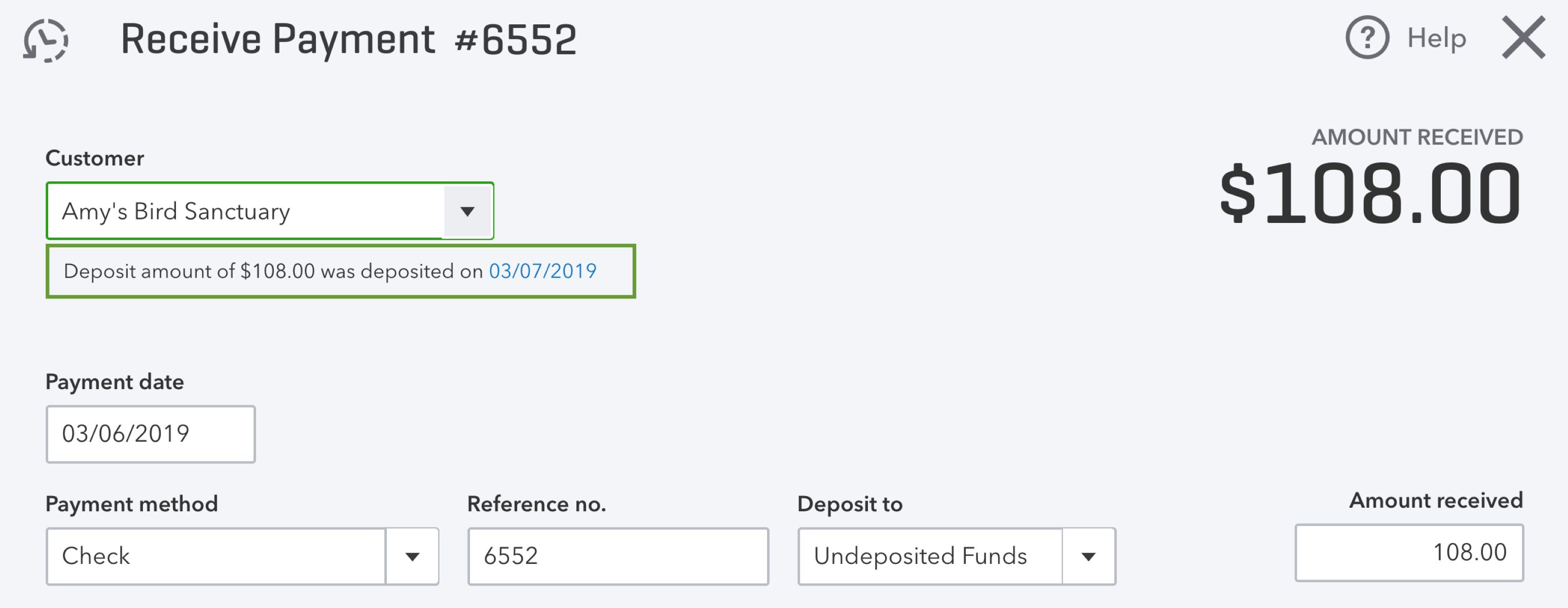

5. Reconcile cleared transactions: Mark the transactions that have cleared the bank, meaning they appear on both the bank statement and in QuickBooks Online, as reconciled or cleared in the software. This will help you keep track of which transactions have been accounted for during the reconciliation process.

6. Pay attention to timing differences: Take note of any timing differences that may cause transactions to appear on one record but not the other. This is common with transactions that have not yet cleared the bank or have been recorded in QuickBooks Online but have not yet been reflected in the bank statement. These timing differences should be accounted for in subsequent steps.

7. Verify beginning and ending balances: Ensure that the beginning balance on your bank statement matches the beginning balance entered in QuickBooks Online for the reconciliation period. Likewise, verify that the ending balance on the bank statement matches the ending balance calculated based on the reconciled transactions in QuickBooks Online.

8. Keep an eye out for bank fees or interest: Be sure to account for any bank fees or interest earned that may not be included in your QuickBooks Online transactions. These amounts should be recorded separately in the software to ensure accurate reconciliation.

Reviewing and comparing your bank statements with the transactions recorded in QuickBooks Online is a critical step in the reconciliation process. By meticulously comparing the two sets of records and noting any discrepancies, you can move on to the next step: identifying and resolving any discrepancies that you have found.

Step 3: Identify and Resolve Discrepancies

After reviewing and comparing your bank statements with the transactions recorded in QuickBooks Online, it’s time to identify and resolve any discrepancies that you have found. Discrepancies can include missing transactions, different amounts, or discrepancies in dates or descriptions. Follow these steps to address and resolve the discrepancies:

1. Double-check data entry: Start by reviewing the data entry in QuickBooks Online for any errors or typos. Verify that the amounts, dates, and descriptions match the corresponding transactions on your bank statement. Even a small error in data entry can lead to significant discrepancies, so ensure accuracy at this stage.

2. Investigate missing transactions: If you come across any missing transactions on either the bank statement or in QuickBooks Online, investigate further. Check your supporting documents, such as receipts or invoices, to ensure you have recorded all the transactions accurately. If you find any missing transactions, enter them in QuickBooks Online, making sure to input the correct details.

3. Check for timing differences: Timing differences can occur when transactions have been recorded in QuickBooks Online but have not yet cleared the bank. Review these timing differences and decide how to handle them. If the item has already appeared on the bank statement of a subsequent period, you may need to adjust your reconciliation accordingly.

4. Reconcile discrepancies: For any discrepancies in amounts, dates, or descriptions, carefully compare the information on your bank statement with the records in QuickBooks Online. Look for any potential errors or mismatches and correct them accordingly. If the discrepancy cannot be resolved immediately, make note of it for further investigation.

5. Seek assistance if needed: If you encounter complex discrepancies or are unsure how to resolve certain issues, consider reaching out to a bookkeeper, accountant, or QuickBooks Online support for guidance. They can offer expert advice and help ensure that your reconciliation is accurate and complete.

6. Maintain clear documentation: Throughout the resolution process, maintain clear documentation of the discrepancies you have encountered and the actions taken to address them. This will serve as a reference in case of any future questions or audits, providing transparency and supporting the accuracy of your reconciliation.

7. Make necessary adjustments: As you address and resolve discrepancies, make the necessary adjustments in QuickBooks Online. This may involve modifying amounts, dates, or descriptions to match the information on your bank statement. Ensure that your adjustments are accurate and properly recorded to maintain the integrity of your financial records.

By carefully identifying and resolving discrepancies, you ensure that your bank statement and transaction records in QuickBooks Online are aligned. This brings you closer to completing the reconciliation process and moving on to the next step: making necessary adjustments in QuickBooks Online.

Step 4: Make Necessary Adjustments in QuickBooks Online

Once you have identified and resolved discrepancies between your bank statements and QuickBooks Online records, it’s time to make any necessary adjustments in the software. This step ensures that your QuickBooks Online account accurately reflects the transactions and balances from your bank statements. Follow these steps to make the necessary adjustments:

1. Edit or add missing transactions: If you discovered missing transactions during the reconciliation process, edit or add them in QuickBooks Online. Ensure that the transaction details match the information on your bank statement, such as the date, amount, and description. Aim to recreate the transaction exactly to maintain accuracy.

2. Correct amounts or descriptions: If you noticed discrepancies in amounts or descriptions, edit the corresponding transactions in QuickBooks Online to match the information on your bank statement. Double-check the accuracy of the adjustments to ensure that they align with the actual transactions.

3. Create adjusting entries: In some cases, you may need to make adjusting entries to account for timing differences or other reconciling items. Adjusting entries are journal entries that correct errors or allocate transactions to the appropriate accounts. Consult with an accountant or bookkeeper if you are unsure about the required adjustments.

4. Reconcile cleared transactions: Once you have made the necessary adjustments, reconcile the cleared transactions in QuickBooks Online. Mark them as reconciled or cleared, indicating that they have been accounted for in the reconciliation process. This step helps you keep track of completed reconciliations and ensures accuracy in your financial records.

5. Review beginning and ending balances: Verify that the beginning and ending balances in QuickBooks Online match the corresponding balances on your bank statement after making the necessary adjustments. If there is still a discrepancy, investigate further to identify any issues that may have been missed during the reconciliation process.

6. Retain supporting documentation: Throughout the adjustment process, maintain clear and organized documentation of any changes made. This includes receipts, invoices, and any other supporting documents that verify the accuracy of the adjustments. Proper documentation ensures transparency and provides evidence of the adjustments made.

7. Reconcile additional accounts: Depending on your business’s complexity, you may need to reconcile other accounts, such as credit cards or merchant accounts. Repeat the steps of reviewing, comparing, identifying discrepancies, and making adjustments for these accounts while following the same reconciliation process.

Making necessary adjustments in QuickBooks Online brings your financial records in line with the information on your bank statement. This step ensures accurate and up-to-date records, which are essential for financial reporting, decision-making, and maintaining the overall health of your business’s finances.

Step 5: Reconcile and Finalize the Process

After making the necessary adjustments in QuickBooks Online, you are ready to reconcile your accounts and finalize the process. This final step ensures that the balances in your QuickBooks Online account match the balances on your bank statement. Follow these steps to reconcile and finalize the reconciliation process:

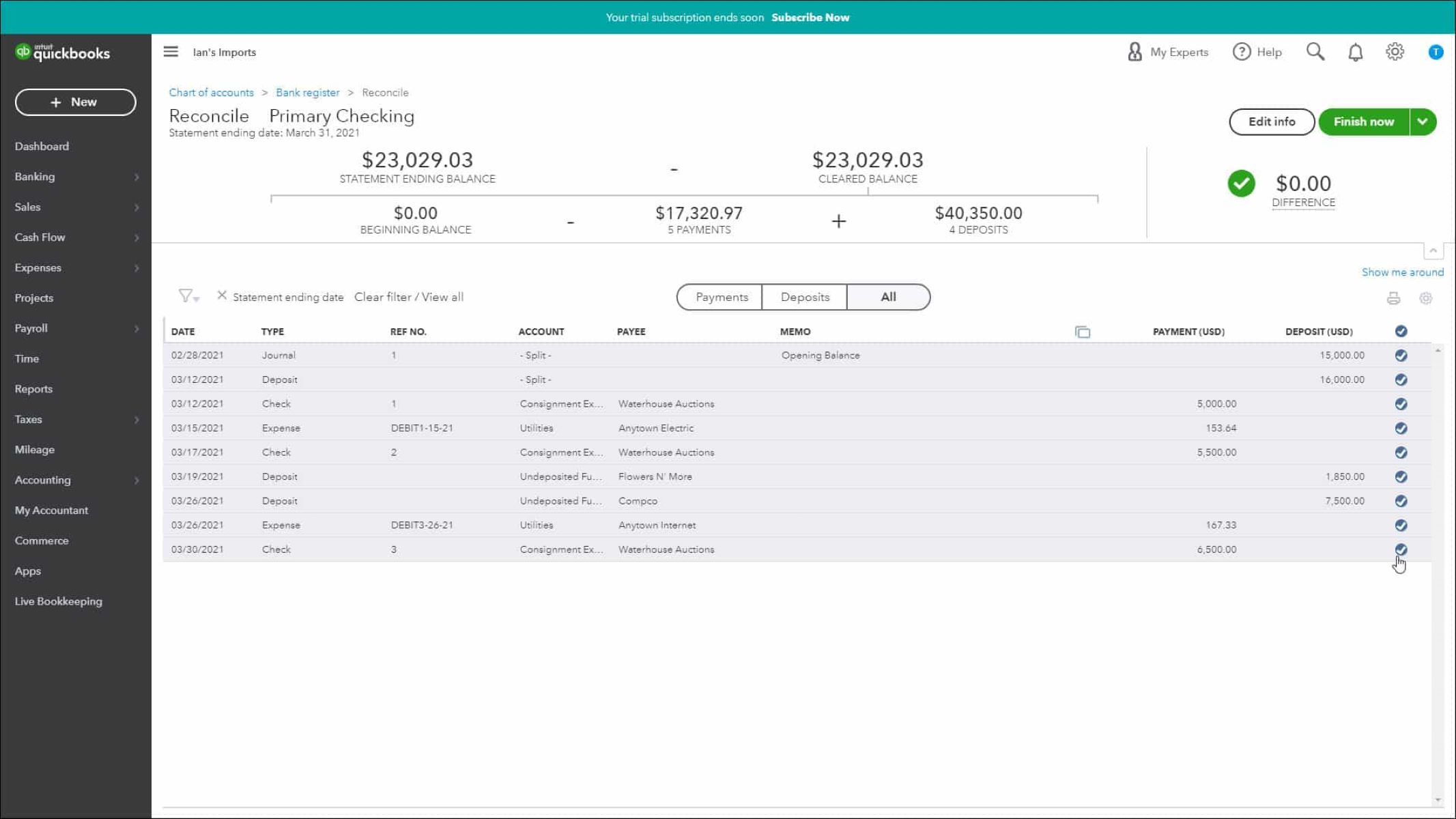

1. Initiate the reconciliation: In QuickBooks Online, go to the Banking or Reconciliation section and select the account you want to reconcile. Enter the statement date and ending balance from your bank statement. QuickBooks Online will automatically populate the cleared transactions based on your previous steps.

2. Verify cleared transactions: Review the list of cleared transactions in QuickBooks Online and compare it to the transactions on your bank statement to ensure that they match. Confirm that all the adjustments you made during the previous steps are reflected in the reconciliation process.

3. Reconcile any remaining items: If there are any remaining items that have not been cleared or matched, investigate and resolve them before proceeding further. Double-check the accuracy of these items and make any necessary adjustments or corrections in QuickBooks Online.

4. Verify ending balance: Ensure that the ending balance in QuickBooks Online matches the ending balance on your bank statement after reconciling all the transactions. If the balances do not match, retrace your steps and review the adjustments and transactions made during the reconciliation process.

5. Review reconciliation summary: QuickBooks Online will provide a reconciliation summary that outlines the details of the reconciliation process, including the statement date, beginning and ending balances, and any adjustments. Carefully review this summary to ensure accuracy before proceeding.

6. Finalize the reconciliation: Once you have reviewed and confirmed the reconciliation summary, finalize the reconciliation process in QuickBooks Online. This action marks the reconciliation as complete and locks the reconciliation period, preventing accidental changes to the reconciled transactions.

7. Retain documentation: Keep a copy of the reconciliation summary and any supporting documents as part of your financial records. These documents serve as evidence of the completed reconciliation and can be referenced for future audits or reviews.

By reconciling and finalizing the process, you can be confident that your bank statement balances match the balances reflected in QuickBooks Online. This synchronization ensures accurate financial reporting and provides a reliable snapshot of your business’s financial health.

Conclusion

Reconciling your QuickBooks Online account is a vital part of maintaining accurate financial records for your business. By following the step-by-step process outlined in this guide, you can ensure that your bank statements and QuickBooks Online transactions are aligned, thereby providing a clear picture of your financial health.

Throughout the reconciliation process, it is crucial to gather all the necessary information, review and compare your bank statements and QuickBooks Online transactions, identify and resolve any discrepancies, make adjustments as needed, and finalize the reconciliation. Each step plays a significant role in ensuring the accuracy and integrity of your financial records.

Reconciliation offers numerous benefits, including ensuring the accuracy of your financial statements, detecting and preventing fraudulent activities, managing cash flow effectively, aiding in decision-making, complying with regulations, and building credibility for your business.

Remember to maintain clear documentation throughout the reconciliation process. This documentation serves as evidence of the steps you have taken and the adjustments made, providing transparency and supporting the accuracy of your financial records.

Regularly reconciling your QuickBooks Online account is a best practice that should be performed on a monthly basis. This ensures that your records are up to date and accurate. Additionally, by reconciling frequently, you can identify and resolve discrepancies promptly, reducing the risk of errors impacting your financial reporting and decision-making processes.

Ultimately, effective reconciliation in QuickBooks Online fosters financial transparency, enables better financial management, and positions your business for success. By dedicating time and attention to this process, you can maintain the integrity of your financial records and make informed business decisions based on accurate and reliable information.

Implement the steps outlined in this guide and prioritize regular reconciliation in your financial routine. With diligent effort and attention to detail, you can reconcile your QuickBooks Online account effectively, leading to more accurate financial records and increased confidence in your business’s financial position.