Introduction

A general ledger is a crucial component of any accounting system, including QuickBooks. It serves as a centralized record-keeping system for tracking and organizing financial transactions within a business. In QuickBooks, the general ledger provides a comprehensive view of all financial activities, ensuring accuracy and facilitating financial analysis.

With QuickBooks’ user-friendly interface and powerful features, businesses of all sizes can easily create and maintain a general ledger. From recording daily transactions to generating useful reports, QuickBooks simplifies the accounting process and helps businesses stay organized.

In this article, we will explore the importance of the general ledger in QuickBooks and how it can benefit your business. We will also provide step-by-step guidance on creating and customizing the general ledger, entering transactions, reconciling records, and generating reports. Additionally, we will share some valuable tips for maintaining an accurate general ledger in QuickBooks.

Whether you’re a small business owner or a seasoned accountant, understanding the general ledger and how to effectively use it in QuickBooks is essential for managing financial information and making informed business decisions.

What is a General Ledger?

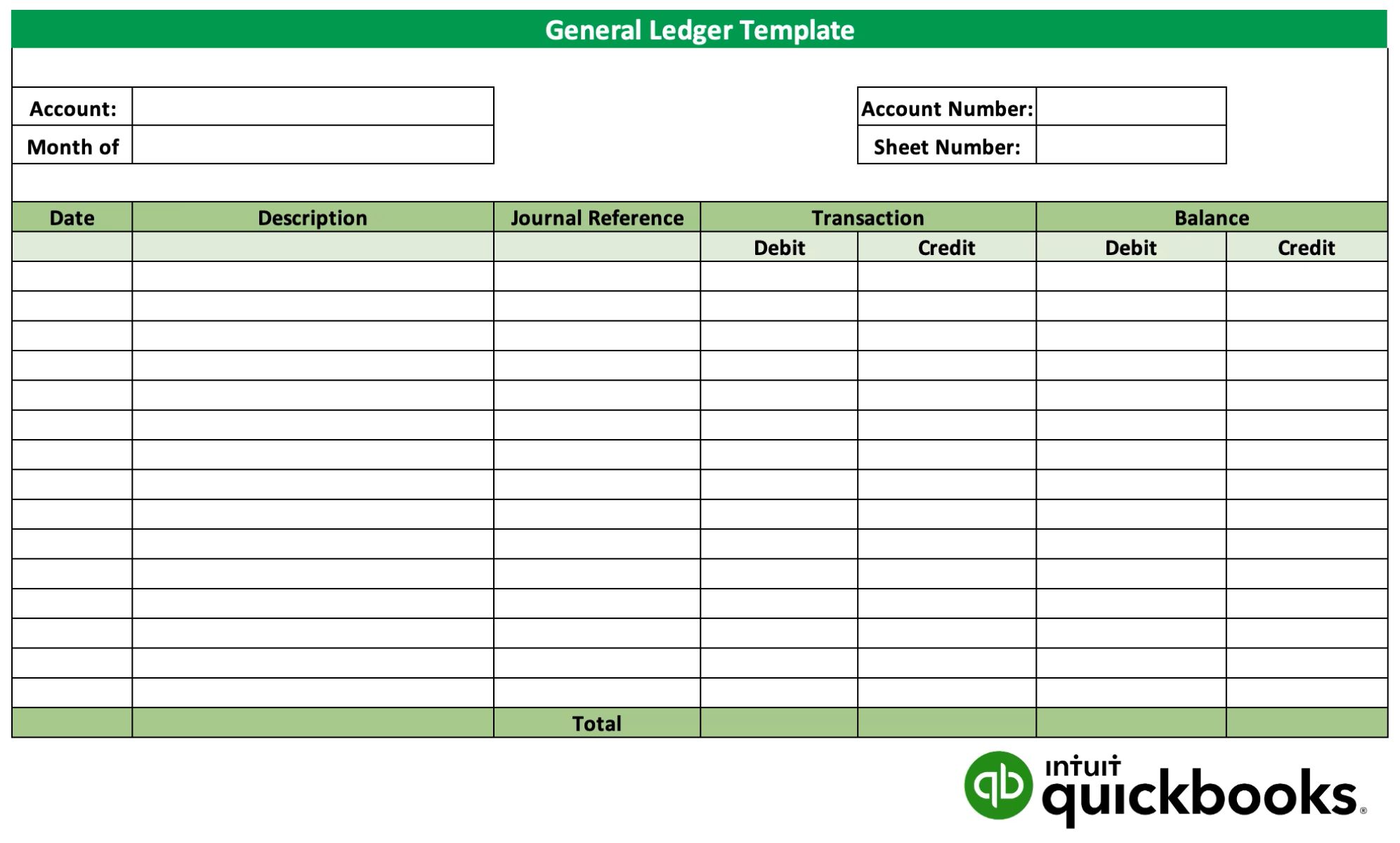

A general ledger is a financial record that contains all the detailed accounts and transactions of a business. It serves as the central repository for recording and summarizing financial information, allowing businesses to monitor their financial health, analyze trends, and make informed decisions.

In simple terms, the general ledger is like a big ledger book where all financial transactions are recorded. It provides a complete picture of the company’s financial activities, including income, expenses, assets, liabilities, and equity.

The general ledger consists of individual accounts referred to as “ledger accounts” or “T-accounts.” Each account represents a specific financial category, such as cash, accounts receivable, accounts payable, inventory, sales, and expenses. These accounts are structured using a chart of accounts, which organizes them into logical groups.

Every transaction that occurs within the business, such as sales, purchases, and payments, is recorded in the appropriate ledger account. These transactions are usually classified as either debit or credit entries, following double-entry bookkeeping principles.

The general ledger provides a detailed historical record of all financial activities, making it easier to track and reconcile transactions. It also serves as the basis for creating financial statements, such as the balance sheet, income statement, and cash flow statement.

In QuickBooks, the general ledger is automatically updated whenever a transaction is entered, ensuring accuracy and saving time compared to manual ledger books. With QuickBooks’ built-in reporting capabilities, businesses can easily generate financial statements and gain valuable insights into their financial performance.

The general ledger is a fundamental tool for businesses of all sizes, as it provides a comprehensive view of the company’s financial position and helps ensure compliance with accounting standards and regulations.

Benefits of Using a General Ledger in QuickBooks

Utilizing a general ledger in QuickBooks offers several key benefits for businesses. Let’s explore some of these advantages:

- Accurate Financial Tracking: The general ledger in QuickBooks ensures accurate tracking of financial transactions. It captures all debits and credits, providing a complete record of financial activities, which is crucial for monitoring cash flow, reconciling accounts, and preparing financial statements.

- Better Financial Analysis: QuickBooks’ general ledger allows for easy analysis of financial data. By generating reports from the ledger, businesses can gain insights into their income, expenses, assets, and liabilities. This enables informed decision-making and helps identify areas that require improvement or adjustment.

- Streamlined Reporting: With the general ledger in QuickBooks, generating financial reports becomes quick and straightforward. QuickBooks offers a wide range of pre-built reports, such as profit and loss statements, balance sheets, and cash flow statements. These reports can be customized to suit specific business needs, making it easier to assess financial performance.

- Improved Audit Trail: The general ledger acts as an audit trail, providing a detailed history of financial transactions. QuickBooks maintains a chronological record of all entries, making it easier to trace and verify transactions during audits or tax preparations. This helps ensure compliance with regulatory requirements.

- Enhanced Budgeting and Forecasting: QuickBooks’ general ledger aids in budgeting and forecasting. By analyzing historical data from the ledger, businesses can make more accurate financial projections and set realistic budgets. This enables effective financial planning and helps businesses stay on track towards their goals.

Overall, using a general ledger in QuickBooks offers businesses the advantage of organized and efficient financial management. It provides a comprehensive view of financial data, facilitates analysis and reporting, and ensures compliance with accounting standards.

Next, we will discuss how to create and set up a general ledger in QuickBooks.

Creating a General Ledger in QuickBooks

To create a general ledger in QuickBooks, follow these steps:

- Set up a Chart of Accounts: The Chart of Accounts is the foundation of the general ledger in QuickBooks. It categorizes accounts into groups such as assets, liabilities, equity, income, and expenses. Customize the Chart of Accounts to match your business’s specific needs and industry requirements.

- Add Accounts: Once the Chart of Accounts is set up, add individual accounts to represent different financial categories. For example, you may have separate accounts for cash, accounts receivable, accounts payable, inventory, and various expense categories. Ensure that each account is properly classified under the appropriate group in the Chart of Accounts.

- Enter Opening Balances: If you are starting to use QuickBooks in the middle of a financial year, you may need to enter opening balances for existing accounts. This step ensures that your general ledger reflects the accurate financial position at the beginning of your QuickBooks usage.

- Set Up Users and Permissions: Determine who will have access to the general ledger in QuickBooks and set up their user accounts with appropriate permissions. This helps maintain data security and ensures that only authorized individuals can view or make changes to the ledger.

- Explore Integration Options: QuickBooks integrates with various financial applications and services, offering additional features and functionalities. Research and consider integrating relevant tools to enhance the capabilities of your general ledger and streamline accounting processes.

- Configure Automatic Transaction Feeds: QuickBooks allows you to connect bank accounts and credit cards for automatic transaction feeds. This feature simplifies the process of recording transactions in the general ledger and reduces the risk of errors or omissions.

Once the general ledger is set up in QuickBooks, it’s essential to regularly review and update it with new transactions. This ensures that your financial records are accurate and up to date.

The next section will discuss the importance of the Chart of Accounts in QuickBooks and how it relates to the general ledger.

Understanding Chart of Accounts in QuickBooks

The Chart of Accounts is a crucial element of the general ledger in QuickBooks. It serves as a framework for organizing and classifying financial transactions. Understanding the Chart of Accounts is essential to effectively track and manage your business’s finances in QuickBooks.

Here are the key aspects of the Chart of Accounts in QuickBooks:

- Account Types: The Chart of Accounts in QuickBooks consists of different account types, such as assets, liabilities, equity, income, and expenses. Each account type represents a specific financial category, and transactions are recorded under these categories. QuickBooks provides default account types, but you can also customize them to match your business’s unique needs.

- Account Numbers: QuickBooks allows you to assign account numbers to each account in the Chart of Accounts. Account numbers provide a logical way to organize and identify accounts. They can follow a specific numbering system, such as sequential or hierarchical, depending on your preference and the complexity of your business.

- Account Names and Descriptions: Each account in the Chart of Accounts should have a clear and descriptive name. The account name should accurately represent the financial category it belongs to. Additionally, you can provide additional details or explanations in the account description to ensure clarity and comprehension.

- Subaccounts: QuickBooks allows the creation of subaccounts within the Chart of Accounts. Subaccounts provide a way to further categorize and organize transactions. For example, under the Expense account category, you can have subaccounts for different expense types like rent, utilities, and office supplies. This hierarchical structure adds flexibility and granular reporting capabilities.

- Parent Accounts: Parent accounts are used to group related subaccounts in the Chart of Accounts. They help create a logical hierarchy and make it easier to navigate and analyze financial data. For example, an Income parent account can have subaccounts for sales revenue, interest income, and other income sources.

Properly setting up and maintaining the Chart of Accounts ensures the accuracy and effectiveness of your general ledger in QuickBooks. It allows for easier data entry, faster reporting, and improved financial analysis.

In the next section, we will discuss how to enter transactions in the general ledger in QuickBooks.

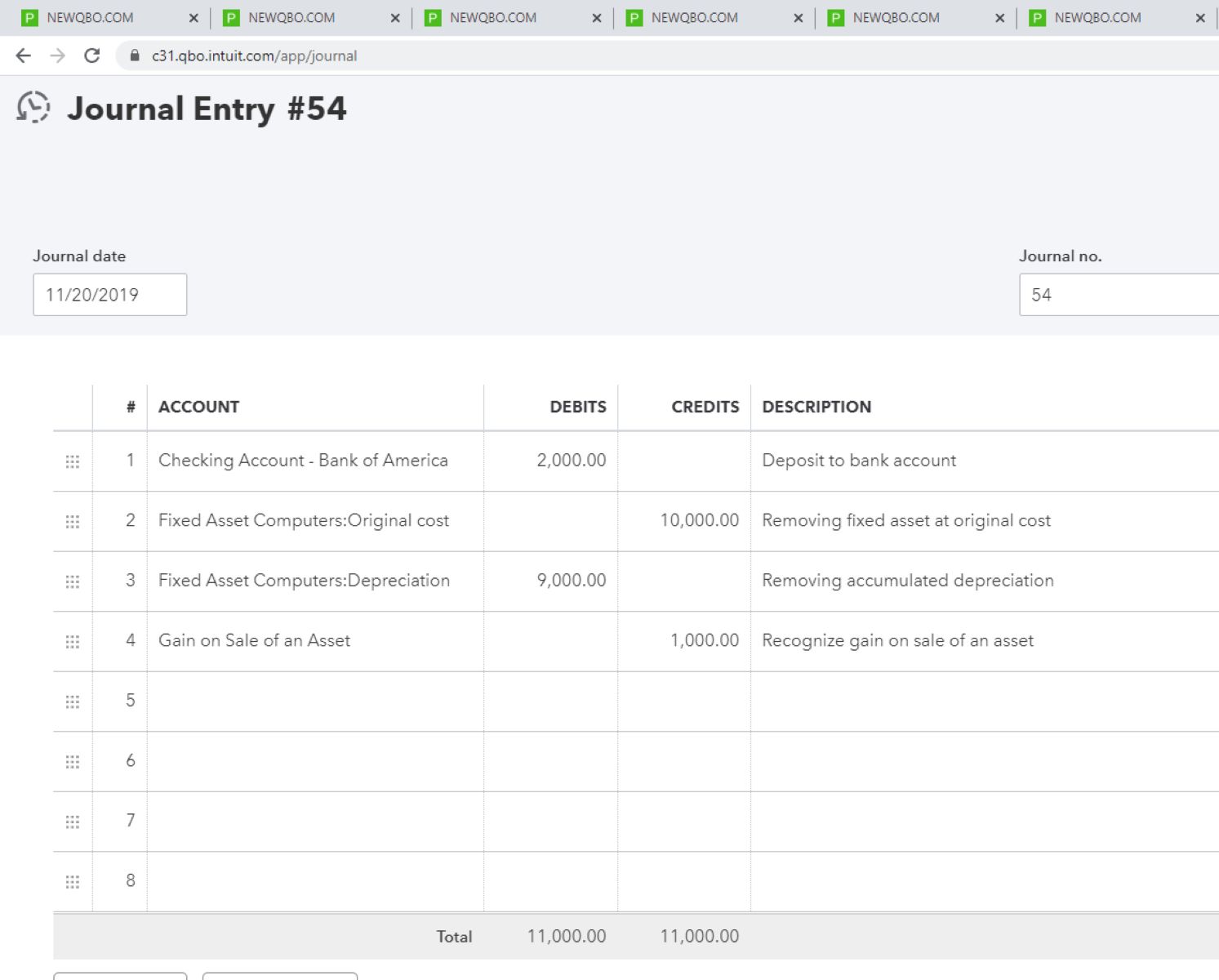

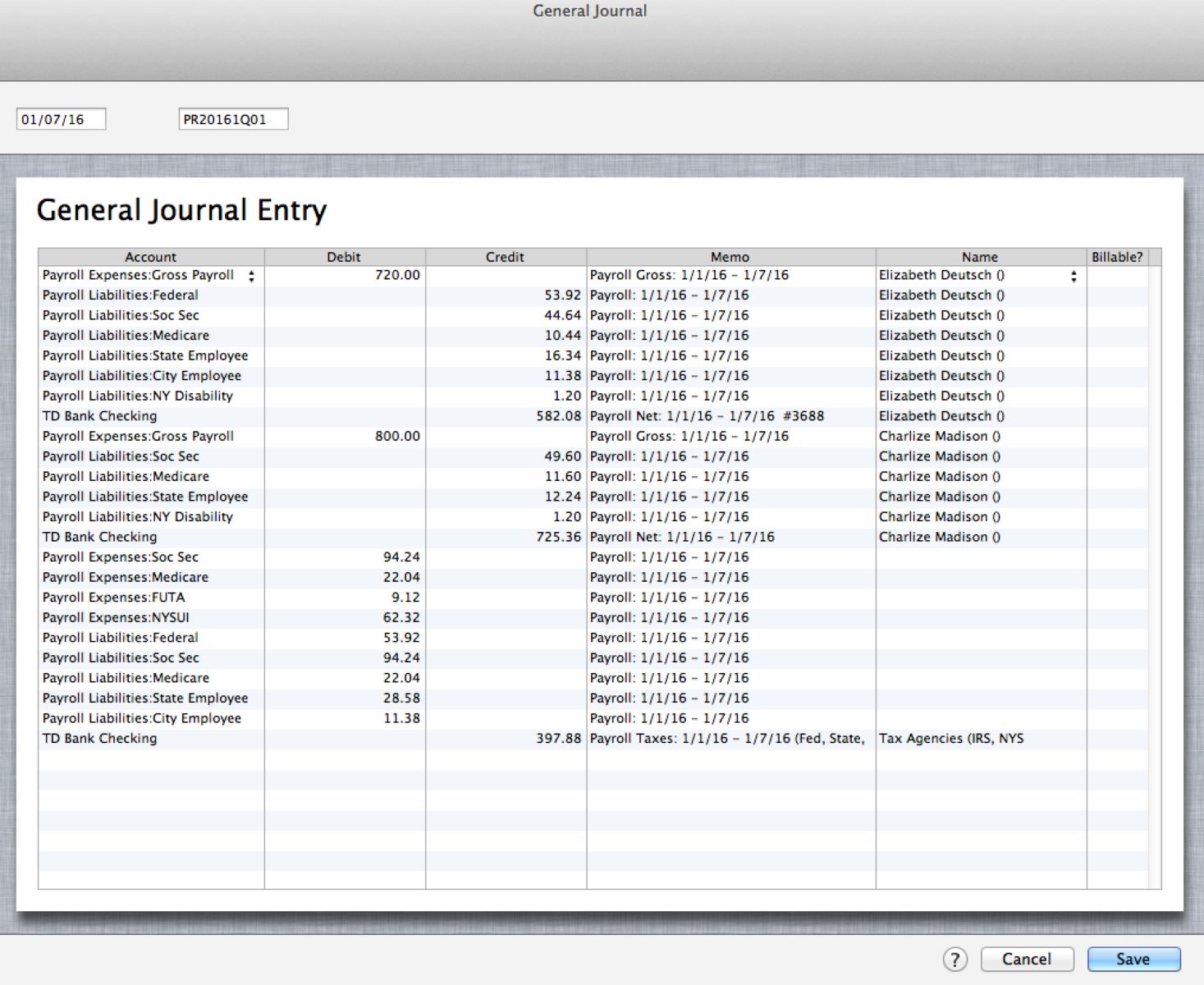

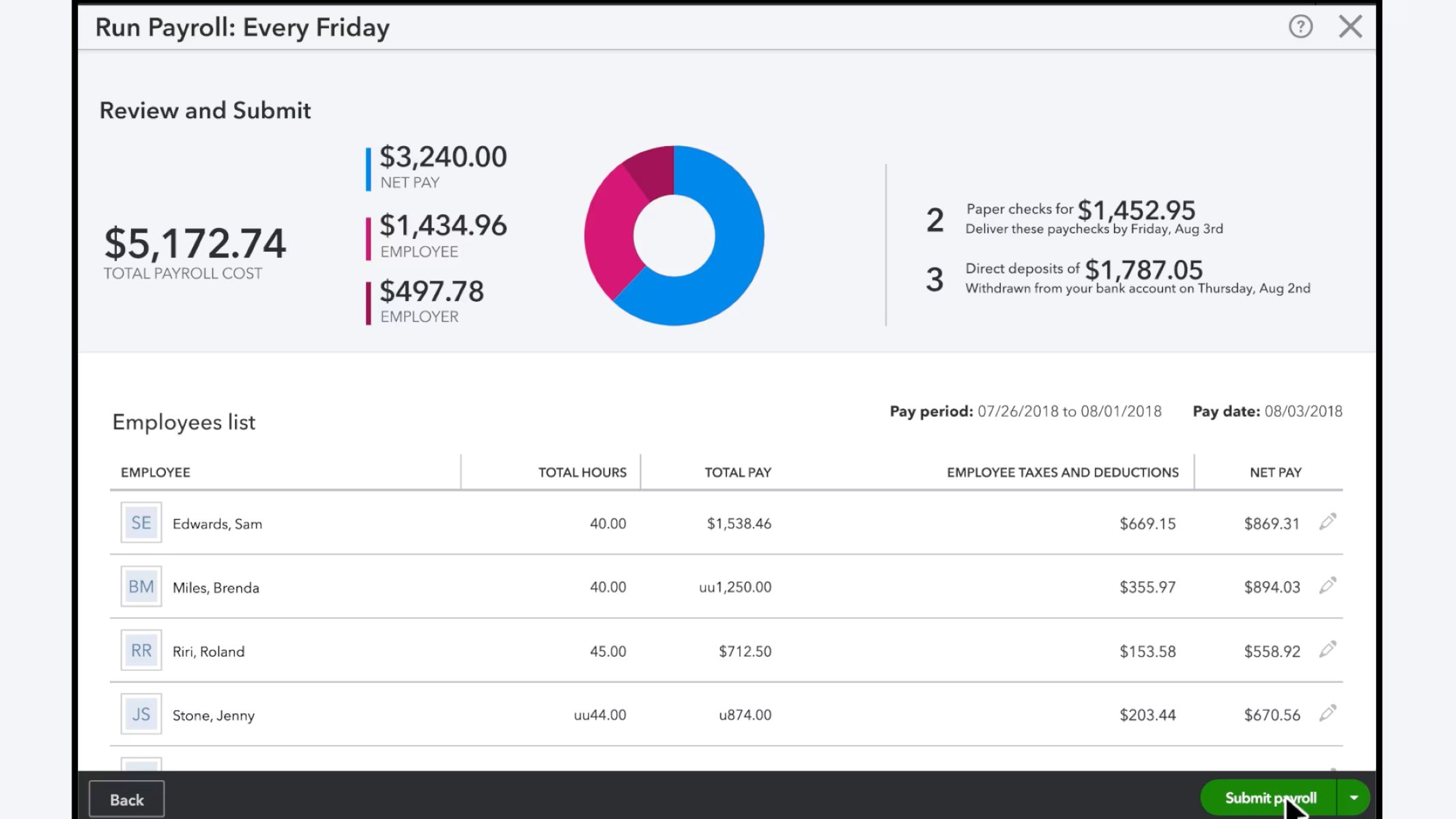

Entering Transactions in the General Ledger

Entering transactions in the general ledger is a crucial step in maintaining accurate financial records in QuickBooks. It allows businesses to keep track of income, expenses, assets, and liabilities effectively. Here’s how to enter transactions in the general ledger:

- Select the Correct Account: When entering a transaction, ensure that you select the appropriate account from the Chart of Accounts that best represents the nature of the transaction. For example, if you receive payment from a customer, select the accounts receivable account.

- Enter Transaction Details: Provide the necessary details of the transaction, including the date, amount, and any additional information required. For sales transactions, include the customer’s name and the items or services sold.

- Choose the Transaction Type: QuickBooks offers various transaction types, such as sales receipts, invoices, bills, payments, and journal entries. Select the relevant transaction type that aligns with the nature of the transaction you are entering.

- Ensure Balanced Entries: QuickBooks follows the double-entry bookkeeping method, meaning each transaction must have balanced debit and credit entries. The total debits must equal the total credits. Verify the amounts entered in each account to ensure accuracy.

- Attach Supporting Documents: It’s good practice to attach supporting documents to transactions, such as invoices, receipts, or bills, as it enables easier reference and verification in the future.

- Review and Save: Before finalizing the transaction, review all the details entered to ensure accuracy. Once satisfied, save the transaction in QuickBooks, and it will be automatically recorded in the general ledger.

Regularly entering transactions in the general ledger is essential to maintain up-to-date and organized financial records in QuickBooks. It enables accurate financial reporting and analysis, contributes to better decision-making, and simplifies the process of reconciling accounts.

The next section will cover how to reconcile the general ledger in QuickBooks to ensure the accuracy of your financial records.

Reconciling the General Ledger in QuickBooks

Reconciling the general ledger in QuickBooks is a critical task that ensures the accuracy and integrity of your financial records. This process involves comparing your business’s financial transactions with external documents, such as bank statements, to identify and resolve any discrepancies. Here’s how to reconcile the general ledger in QuickBooks:

- Gather Bank Statements and Records: Collect the latest bank statements, credit card statements, and other relevant financial documents that show the transactions made during the reconciliation period.

- Access the Reconciliation Feature: In QuickBooks, navigate to the Reconcile section found in the Banking menu. Select the account you want to reconcile, such as your bank account or credit card account.

- Enter Statement Information: Provide the opening and closing balances stated on the bank statement. QuickBooks will automatically compare these balances with your general ledger’s opening and closing balances.

- Compare Transactions: Go through each transaction listed on the bank statement and compare them with the corresponding entries in your general ledger. Check for any discrepancies, such as missing transactions, duplicate entries, or incorrect amounts.

- Make Adjustments: If you find any discrepancies, make the necessary adjustments in QuickBooks. This may involve adding missing transactions, deleting duplicates, or correcting erroneous entries. Ensure that the ending balances on both the bank statement and in QuickBooks match.

- Reconcile and Complete the Process: Once all discrepancies are resolved, reconcile the account in QuickBooks. This confirms that the transactions in your general ledger align with the bank statement and ensures the accuracy of your financial records.

Reconciling the general ledger in QuickBooks on a regular basis is crucial for accurate financial reporting, identifying errors or fraud, and maintaining the integrity of your financial records.

In the next section, we will explore how to generate valuable reports from the general ledger in QuickBooks to gain insights into your business’s financial performance.

Generating Reports from the General Ledger

One of the significant advantages of using the general ledger in QuickBooks is the ability to generate various reports that provide valuable insights into your business’s financial performance. These reports help you analyze trends, make informed decisions, and monitor the overall health of your business. Here’s how you can generate reports from the general ledger in QuickBooks:

- Access the Reports Menu: In QuickBooks, navigate to the Reports menu, where you will find a wide range of pre-built report templates categorized by financial aspects, such as profit and loss, balance sheet, cash flow, sales, and expenses.

- Select the Desired Report: Choose the specific report that aligns with the information you want to review. For example, if you want to assess your business’s profitability, select the profit and loss report.

- Customize the Report: QuickBooks allows you to customize reports to fit your needs. You can modify the date range, add or remove columns, adjust the layout, and apply filters to focus on specific accounts or transaction types.

- Review the Generated Report: Once you have customized the report parameters, review the generated report on-screen. Analyze the numbers, look for trends, and identify areas that require attention or improvement.

- Export or Print the Report: If needed, you can export the report to a spreadsheet or PDF format for further analysis or sharing with stakeholders. Alternatively, you can directly print the report for physical documentation purposes.

- Save Report Customizations: Save any customized reports that you plan to generate regularly. This saves time and effort in recreating the reports with the same settings in the future.

By generating reports from the general ledger in QuickBooks, you can gain insights into your business’s financial performance, monitor key metrics, and make data-driven decisions. Regularly reviewing and analyzing these reports will help you identify trends, address issues, and drive business growth.

In the next section, we will discuss how to customize the general ledger in QuickBooks to suit your business’s specific needs.

Customizing the General Ledger in QuickBooks

QuickBooks offers flexibility in customizing the general ledger to fit your business’s specific needs and preferences. Customization allows you to organize and present financial information in a way that is most useful and relevant to your business. Here are some ways to customize the general ledger in QuickBooks:

- Chart of Accounts Customization: Review and modify the Chart of Accounts to align with your business’s financial structure and reporting requirements. Add new accounts, edit account names, reorganize account hierarchies, and ensure that each account is correctly classified under the appropriate account type.

- Add Custom Fields: QuickBooks allows you to add custom fields to the general ledger to capture additional information that is relevant to your business. For example, you can create custom fields to track customer or project-specific details, cost centers, or special tracking categories.

- Custom Reporting: Take advantage of QuickBooks’ advanced reporting features to create customized reports that focus on specific accounts, time periods, or transaction types. Tailor the reports to present the information you need for better financial analysis and decision-making.

- Personalize User Interface: QuickBooks allows you to customize the user interface to match your preferences. Adjust settings related to display, font, colors, and form layouts to create a personalized user experience when working with the general ledger.

- Integration with Third-Party Apps: QuickBooks integrates with a wide range of third-party applications and services. Explore these integrations to enhance the capabilities of your general ledger. For example, you can integrate with data visualization tools to create interactive dashboards or connect with expense tracking apps for seamless expense management.

- Automated Workflows: QuickBooks provides automation features that can simplify general ledger processes. Set up automated workflows, such as recurring transactions or scheduled reports, to save time and ensure consistency in recording and reporting financial information.

By customizing the general ledger in QuickBooks, you can tailor the system to meet your business’s unique requirements. This enables efficient financial management, better analysis, and improved decision-making.

In the next section, we will discuss some essential tips for maintaining an accurate general ledger in QuickBooks.

Tips for Maintaining an Accurate General Ledger in QuickBooks

Maintaining an accurate general ledger in QuickBooks is essential for efficient financial management and informed decision-making. Follow these tips to ensure the integrity and accuracy of your general ledger:

- Consistent Data Entry: Enter all transactions into QuickBooks consistently and promptly. This ensures that your general ledger reflects the most recent and accurate financial information, enabling better tracking and reporting.

- Regular Reconciliation: Reconcile your bank accounts, credit card accounts, and other financial accounts on a regular basis. This process helps identify and resolve any discrepancies between your general ledger and external statements, minimizing errors and ensuring accurate financial records.

- Monitor and Review: Regularly review your general ledger for any unusual or unexpected entries. Pay attention to account balances, transaction details, and any abnormalities that may require investigation. Timely detection and correction of errors can prevent larger issues down the line.

- Implement Internal Controls: Establish internal controls to safeguard your general ledger from fraud or unauthorized transactions. Limit access to sensitive financial information, regularly change passwords, and conduct periodic audits to ensure compliance and maintain data integrity.

- Backup and Secure Data: Regularly backup your QuickBooks data to prevent data loss. Store backups securely and, if possible, consider using cloud-based backup options for added protection. Implement security measures, such as user access restrictions and secure passwords, to prevent unauthorized access to your general ledger.

- Stay Updated with QuickBooks: Keep your QuickBooks software up to date by installing updates and patches. New updates often include bug fixes, security enhancements, and new features that can optimize the performance and reliability of your general ledger.

- Training and Support: Invest in training for yourself and your team to understand the proper use of QuickBooks and the general ledger. This ensures that everyone is proficient in data entry, reporting, and troubleshooting, reducing the likelihood of errors.

- Consult with an Accountant: If you’re uncertain about any aspects of maintaining your general ledger, seek guidance from an accountant with expertise in QuickBooks. They can provide valuable insights, assist with complex transactions, and ensure compliance with accounting standards.

By following these tips, you can maintain an accurate and reliable general ledger in QuickBooks, enabling effective financial management and confident decision-making.

Next, we will conclude this article by summarizing the key points discussed.

Conclusion

In conclusion, the general ledger is a vital component of QuickBooks that allows businesses to track and manage their financial transactions accurately. It serves as a centralized record-keeping system, providing a comprehensive view of income, expenses, assets, liabilities, and equity.

Through the use of QuickBooks’ user-friendly interface and powerful features, businesses can easily create and customize their general ledger. This enables them to enter transactions, reconcile accounts, generate reports, and make informed decisions based on accurate financial data.

We discussed the benefits of using a general ledger in QuickBooks, including accurate financial tracking, better financial analysis, streamlined reporting, improved audit trails, and enhanced budgeting and forecasting.

Furthermore, we explored the process of creating a general ledger, understanding the Chart of Accounts, entering transactions, reconciling accounts, and generating reports. Each step is essential for maintaining an accurate and organized general ledger.

We also provided tips for ensuring the integrity of your general ledger, such as consistent data entry, regular reconciliations, monitoring and reviewing, implementing internal controls, backing up data, staying updated with QuickBooks, and seeking professional advice when needed.

By following these guidelines, businesses can maintain an accurate general ledger in QuickBooks, enabling them to make informed financial decisions, meet regulatory requirements, and drive overall business success.

Remember, the general ledger is not just a record-keeping tool; it is a powerful resource that provides valuable insights into your business’s financial health. Embrace its potential, customize it to suit your needs, and leverage its features to optimize your financial management processes.

So, go ahead and utilize the power of the general ledger in QuickBooks to take your financial management to the next level!