Introduction

Planning for retirement is an important financial goal that requires careful consideration and strategic decision-making. One of the key factors to consider is how much you should have in investments in order to retire comfortably. While there is no one-size-fits-all answer to this question, it depends on various factors such as your age, retirement goals, expected expenses, and existing sources of retirement income.

Retirement is a time when individuals can finally enjoy the fruits of their labor and have the freedom to pursue their passions and interests. However, it is essential to have a solid financial foundation to support your desired lifestyle during this phase of life.

In this article, we will explore the factors that need to be considered when determining how much you should have in investments for retirement. Understanding these factors will help you make informed decisions and create a financial plan that aligns with your retirement goals.

It’s important to note that the information provided in this article is for general guidance purposes only. It is always recommended to consult with a financial advisor who can assess your specific circumstances and provide personalized advice.

Now, let’s dive into the factors you should consider when determining your investment needs for a comfortable retirement.

Factors to Consider

When determining how much you should have in investments in order to retire, there are several key factors that you should take into account. These factors will help you assess your current financial situation, evaluate your retirement goals, and make informed decisions about your investment strategy.

Age and Retirement Goals: Your age plays a significant role in determining how much you should have in investments for retirement. If you are younger, you have a longer time horizon to save and invest, which allows for more aggressive investment strategies. On the other hand, if you are closer to retirement, you may need to focus on preserving capital and generating income rather than seeking high returns. Additionally, consider your retirement goals – whether it’s traveling, starting a second career, or simply enjoying a comfortable lifestyle – as this will impact how much you need to save.

Expected Retirement Expenses: Estimating your retirement expenses is crucial in determining how much you should have in investments. Consider your housing costs, healthcare expenses, travel plans, and any other lifestyle choices you anticipate. It’s essential to be realistic and factor in potential inflation and unexpected expenses that may arise.

Sources of Retirement Income: Take into account your expected sources of retirement income, such as social security benefits, company pension plans, and other investments. Understanding the potential income streams you will have in retirement will help you gauge how much you will need to supplement from your investments.

Social Security Benefits: Determine your eligibility and expected benefits from the social security system. Social security benefits can provide a valuable base income during retirement, but they may not cover all of your expenses. Make sure to factor this into your investment planning.

Company Pension Plans: If you have a company pension plan, understand the benefits it will provide during retirement. Some plans offer a fixed monthly income, while others may have a lump sum payout option. Assessing and understanding the terms of your pension plan will give you a clearer picture of how much you need to save independently.

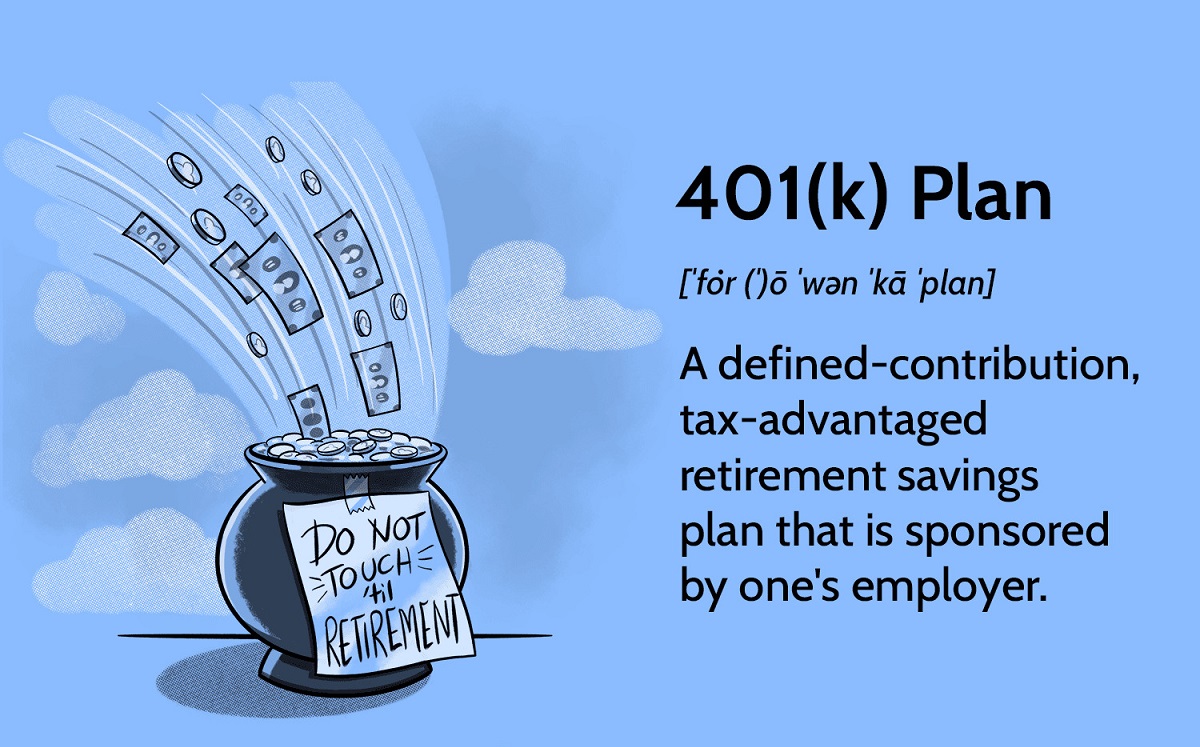

Personal Savings and Investments: Your personal savings and investments will play a critical role in supporting your retirement lifestyle. Consider your current savings and investment portfolio, including any retirement accounts like 401(k)s or IRAs. Assess your risk tolerance and determine if adjustments need to be made to your investment strategy.

By considering these factors, you can create a more accurate assessment of how much you should have in investments in order to retire comfortably. Remember, everyone’s financial situation and goals are unique, so it’s crucial to tailor your retirement plan accordingly.

Age and Retirement Goals

One of the fundamental factors to consider when determining how much you should have in investments for retirement is your age and retirement goals. These two aspects go hand in hand and play a significant role in shaping your investment strategy and the amount you need to save.

If you are younger and have many years until retirement, you have the advantage of time. This means you can take advantage of compounding returns by investing in assets that have higher growth potential, such as stocks or equity-based funds. The longer your investment horizon, the more risk you can afford to take on to potentially earn higher returns. However, it’s important to strike a balance between risk and reward and diversify your investments to minimize potential losses.

Conversely, if you are closer to retirement age, your investment strategy may shift towards capital preservation and generating income. At this stage, the focus is on protecting your accumulated savings and ensuring a consistent cash flow during retirement. This may involve reallocating a portion of your portfolio to more stable and income-generating assets, such as bonds, dividend-paying stocks, or real estate investment trusts (REITs).

Another factor to consider alongside age is your retirement goals. What do you envision for your retirement? Do you plan to travel frequently, start a small business, or simply enjoy a comfortable lifestyle? The answer to these questions can significantly impact how much you need to have in investments.

If your retirement goals involve expensive hobbies or extensive travel, you may need a larger investment portfolio to support those aspirations. On the other hand, if your goals are more modest and you plan to live a simpler lifestyle, you may be able to get by with a smaller investment portfolio.

It’s crucial to have a clear understanding of your retirement goals and revisit them periodically as they may evolve over time. This will allow you to adjust your investment strategy and savings accordingly.

Remember, the key to successfully determining how much you should have in investments for retirement lies in aligning your age, retirement goals, and investment strategy. Regularly reassessing your financial situation and consulting with a financial advisor can help you stay on track and make the necessary adjustments to achieve the retirement you desire.

Expected Retirement Expenses

When calculating how much you should have in investments for retirement, it is essential to consider your expected retirement expenses. Estimating your expenses accurately will help you determine the amount of income you will need and, consequently, the size of your investment portfolio.

Consider all aspects of your daily living and lifestyle during retirement. Start by looking at your current expenses and identifying any areas that may change once you retire. For example, you may no longer have commuting or work-related expenses, but you may have additional healthcare, travel, or leisure expenses.

Housing costs are often a significant part of retirement expenses. Are you planning to downsize to a smaller home or relocate to an area with a lower cost of living? Do you have a mortgage or plan to rent? Assess your housing needs and factor in associated costs, such as property taxes, maintenance, and utilities.

Healthcare expenses are another crucial consideration. As we age, our healthcare needs tend to increase. Account for costs related to health insurance, Medicare premiums, prescription medications, and potential out-of-pocket expenses for medical treatments or long-term care.

Travel and leisure are often top priorities for retirees. Consider your travel aspirations and hobbies, and estimate the associated costs. Do you plan to take frequent vacations, explore new destinations, or indulge in expensive hobbies? These expenses should be factored into your retirement budget accordingly.

It’s also important to keep inflation in mind when estimating your retirement expenses. Over time, the cost of goods and services tends to rise. Considering an inflation rate of 2-3% per year can help you project your future expenses more accurately.

Lastly, don’t forget to plan for unexpected expenses and emergencies. It’s wise to have a contingency fund set aside to cover unexpected medical bills, home repairs, or any unforeseen financial challenges that may arise during retirement.

By carefully assessing your anticipated retirement expenses, you can better determine how much you need to have in investments to cover these costs. Remember to revisit your budget periodically and adjust your investment strategy accordingly to ensure your financial security during retirement.

Sources of Retirement Income

When considering how much you should have in investments for retirement, it’s crucial to examine the various sources of retirement income that will contribute to your financial well-being. By understanding these income sources, you can determine how much additional income you will need from your investments.

Social Security Benefits: Social Security benefits are an important source of income for many retirees. The amount you receive depends on several factors, including your earnings history and the age at which you start collecting benefits. To estimate your Social Security benefits, you can use the Social Security Administration’s online calculators or consult with a financial advisor.

Company Pension Plans: If you are fortunate enough to have a company pension plan, this can provide a significant portion of your retirement income. Pension plans vary in terms of their structure and benefits. Some provide a fixed monthly income, while others offer a lump-sum payout option. Review your pension plan documentation and consult with your HR department or pension administrator to understand the benefits it will provide during retirement.

Personal Savings and Investments: Personal savings and investments are a crucial piece of the retirement income puzzle. This includes your savings accounts, individual retirement accounts (IRAs), and other investment vehicles like stocks, bonds, and mutual funds. The goal is to accumulate enough savings and investments to generate a regular income stream during retirement.

It’s important to assess your current savings and investment portfolio and determine if it aligns with your retirement goals. Consider factors such as your risk tolerance, time horizon, and desired retirement lifestyle when determining the appropriate investment strategy.

Other Retirement Accounts: In addition to personal savings and investments, you may have other retirement accounts, such as 401(k)s or 403(b)s from previous employers. These accounts can also contribute to your retirement income. Evaluate the balance in these accounts and explore any potential rollover or consolidation options to streamline your retirement savings.

Part-Time Work or Side Hustles: Some individuals choose to continue working on a part-time basis or pursue side hustles during retirement. This can provide an additional income stream and help offset any gaps between your retirement income sources and expenses. Consider your skills, interests, and potential opportunities for part-time work or self-employment during retirement.

By analyzing these sources of income, you can assess how much you will receive from each and determine the additional income required from your investments to maintain your desired retirement lifestyle. Remember to factor in potential changes in income sources over time and regularly evaluate and adjust your investment strategy as needed.

Social Security Benefits

When planning for retirement and determining how much you should have in investments, it is essential to understand and factor in your expected Social Security benefits. Social Security is a government program that provides retirement income to eligible individuals based on their earnings history and the age at which they choose to start collecting benefits.

Estimating your Social Security benefits requires consideration of several factors. Your primary insurance amount (PIA), which is the basis for determining your benefit amount, is calculated based on your average indexed monthly earnings during your highest-earning years.

The age at which you choose to start collecting benefits also affects the amount you receive. You can start collecting benefits as early as age 62, but your benefit will be permanently reduced if you claim before your full retirement age (FRA). On the other hand, if you delay claiming benefits past your FRA, your benefit will increase until age 70.

It’s important to note that the full retirement age varies depending on the year you were born. For individuals born between 1943 and 1954, the full retirement age is 66. It gradually increases to age 67 for those born in 1960 or later.

One key decision to make when it comes to Social Security benefits is whether to claim early or delay. Claiming early, although reducing your monthly benefit, may make sense in certain situations, such as if you need the income to cover expenses or have concerns about your health and life expectancy.

Delaying benefits, on the other hand, can result in a higher monthly benefit, which can be advantageous if you have a longer life expectancy, sufficient alternative income sources, or simply want to maximize your retirement income.

Understanding your Social Security benefits can help you better calculate how much additional income you will need from your investments. The Social Security Administration provides online calculators that can assist you in estimating your benefits based on different claiming scenarios.

Keep in mind that while Social Security benefits can form a crucial part of your retirement income, they may not be sufficient to cover all of your expenses. It’s important to evaluate other income sources, such as pensions, personal savings, and investments, to ensure a comfortable retirement.

Consulting with a financial advisor who specializes in retirement planning can provide valuable insights into optimizing your Social Security benefits and integrating them into your overall investment strategy.

Company Pension Plans

Company pension plans can be a significant source of retirement income for individuals who are fortunate enough to have access to them. Understanding how your company pension plan works and the benefits it provides is crucial when determining how much you should have in investments for retirement.

Pension plans vary in structure and benefits, so it’s essential to review the details of your specific plan. Some pension plans offer a defined benefit (DB) plan, where the retirement income is predetermined based on factors such as your salary and years of service. With a DB plan, you can typically expect a fixed monthly income during retirement.

Other pension plans may offer a defined contribution (DC) plan, such as a 401(k). With a DC plan, your employer and/or you contribute to the account, and the value of the account grows based on investment performance. The income you receive during retirement from a DC plan depends on the accumulated contributions and investment returns.

If you have a DB plan, it’s crucial to understand the benefits it will provide during retirement. Review the plan’s documentation and consult with your HR department or pension administrator to determine how the benefits are calculated and when you can begin receiving them. Some DB plans may have specific eligibility criteria or early retirement provisions, which can affect the timing and amount of benefits you receive.

In the case of a DC plan, take into account the balance of your account and your employer’s matching contributions, if applicable. Assess the investment performance and consider if there are any opportunities to maximize the growth of your account. Additionally, determine whether a lump-sum payout or an annuity option is available at retirement.

When evaluating your company pension plan, it’s important to consider how it complements your other retirement income sources. Assess how the benefits from your pension plan, along with Social Security benefits and personal savings, will contribute to your retirement income needs.

If you have multiple pensions from different employers, it may also be beneficial to explore potential consolidation options. Consolidating your pension funds into a single account can simplify your retirement planning and provide a clearer picture of your overall retirement income.

Finally, keep in mind that company pension plans are subject to rules and regulations, and the benefits you receive may be impacted by various factors. Changes in the company’s financial situation or the pension plan’s funding status may affect the amount of benefits you ultimately receive.

Consulting with a financial advisor who specializes in retirement planning can help you navigate your company pension plan and make decisions that align with your retirement goals. They can provide guidance on optimizing your pension benefits and integrating them into your overall investment strategy.

Personal Savings and Investments

Personal savings and investments are a critical component when determining how much you should have in investments for retirement. These assets will play a significant role in supporting your desired lifestyle during your golden years.

Assessing your current savings and investment portfolio is the first step in understanding how much you have earmarked for retirement. This includes evaluating your savings accounts, individual retirement accounts (IRAs), and other investment vehicles such as stocks, bonds, and mutual funds.

Consider your risk tolerance, time horizon until retirement, and desired retirement lifestyle when determining the appropriate investment strategy. A diversified portfolio that aligns with your goals can provide a balance between growth and stability.

It’s important to regularly contribute to your retirement savings. Setting aside a portion of your income each month to save and invest can help you build a substantial nest egg over time. Automating these contributions can ensure consistency and make it easier to stay committed to your long-term financial objectives.

Maximizing tax-advantaged accounts, such as 401(k)s or IRAs, can also be beneficial. These accounts offer tax benefits, such as tax-deferred growth or tax-free withdrawals in retirement, depending on the account type. Take advantage of employer matching contributions if available, as they can significantly boost your overall savings.

Assessing your risk tolerance is crucial when determining the allocation of your investments. Younger individuals with a longer time horizon until retirement may be more comfortable taking on higher risk investments, such as stocks, which have the potential for higher returns. As you approach retirement, you may want to consider shifting towards more conservative investments, such as bonds, to help preserve capital.

Regularly monitoring and adjusting your investment portfolio is essential. Rebalancing your portfolio periodically ensures that it stays aligned with your risk tolerance and long-term objectives. Economic conditions, market fluctuations, and personal circumstances may warrant adjustments to maintain a well-diversified and balanced portfolio.

Keep in mind that personal savings and investments are tools to supplement other sources of retirement income, such as Social Security benefits or company pension plans. Evaluating your overall retirement income picture is crucial to ensure that you’re on track to meet your financial goals.

Consulting with a financial advisor who specializes in retirement planning can help you develop a personalized strategy for your personal savings and investments. They can provide guidance on asset allocation, investment options, and help you stay on track to achieve a financially secure retirement.

Types of Investments for Retirement

When planning for retirement, it’s important to consider the various types of investments that can help you grow your savings and generate income. Diversifying your investment portfolio is crucial to mitigate risk and maximize returns over the long term.

Stocks: Investing in stocks allows you to become a partial owner of a company and benefit from its growth and success. Stocks offer the potential for higher returns but also come with higher volatility. Long-term investors who can tolerate market fluctuations may choose to include stocks in their retirement portfolio to capture capital appreciation.

Bonds: Bonds are fixed-income investments where you lend money to a government or corporation in exchange for regular interest payments and the return of the principal amount when the bond matures. Bonds provide more stable returns compared to stocks and can be an excellent addition to a retirement portfolio for income generation and capital preservation.

Mutual Funds: Mutual funds pool money from multiple investors to invest in a diversified portfolio of stocks, bonds, or other assets. These professionally managed funds offer instant diversification and are suitable for individuals who prefer a hands-off approach to investing. They can be a convenient option for retirement savings, providing exposure to a range of investments with varying risk levels.

Real Estate: Real estate investments, such as rental properties or real estate investment trusts (REITs), can provide steady income and potential appreciation over time. Real estate can be an attractive addition to a retirement portfolio for individuals seeking alternative sources of income and diversification beyond traditional stocks and bonds.

Exchange-Traded Funds (ETFs): ETFs are similar to mutual funds but trade on stock exchanges like individual stocks. Like mutual funds, ETFs offer diversified investment options, but they provide the flexibility of trading throughout the day. ETFs can be an effective tool for building a well-rounded retirement portfolio.

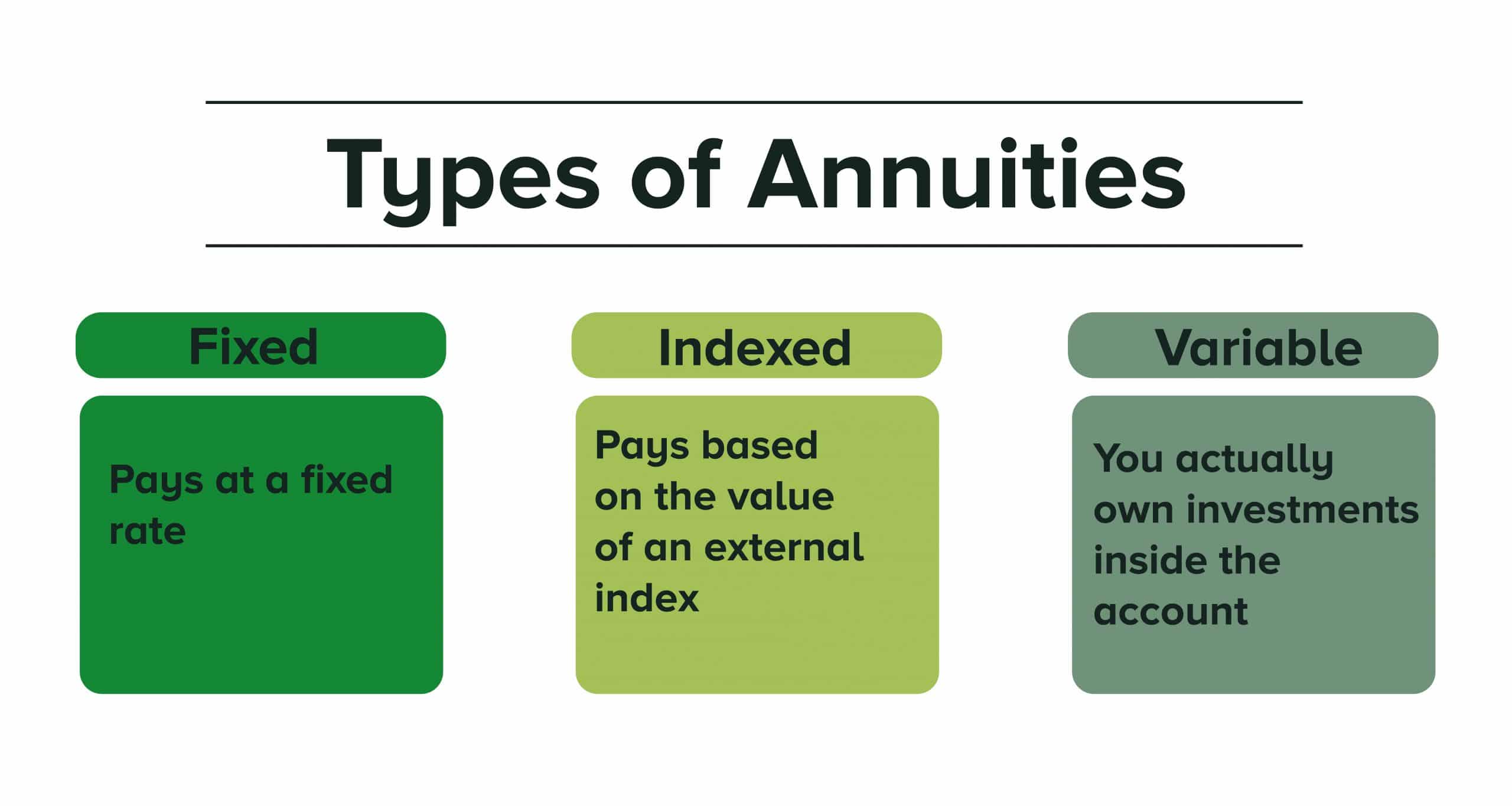

Annuities: Annuities are insurance products that provide a guaranteed income stream during retirement. They can be immediate, where you start receiving payments right away, or deferred, allowing for the accumulation of funds until a later date. Annuities can provide a sense of security and stability to your retirement income but may come with fees and restrictions, so thorough research and consideration are essential.

Index Funds: Index funds aim to replicate the performance of a specific market index, such as the S&P 500. These funds passively invest in a diversified portfolio of assets, offering broad market exposure and low fees. Index funds can be a cost-effective option for long-term investments and are often favored by individuals seeking to match market returns.

Cash and Cash Equivalents: Cash, savings accounts, and money market funds are considered low-risk, liquid investments. While they offer minimal returns, they provide stability and immediate access to funds. Maintaining an emergency fund and having some cash on hand can provide peace of mind during retirement.

Every individual’s retirement investment strategy will differ based on their risk tolerance, financial goals, and time horizon. It’s important to consult with a financial advisor who can help you determine the most suitable mix of investments for your retirement needs.

Assessing Risk Tolerance

Assessing your risk tolerance is a crucial step in determining how much you should have in investments for retirement. Your risk tolerance reflects your ability to handle fluctuations in the value of your investments and can help guide your investment decisions.

Risk tolerance varies from person to person and is influenced by several factors, including your age, financial goals, time horizon until retirement, and comfort with market volatility. It’s important to understand your risk tolerance to ensure that your investment strategy aligns with your comfort level and long-term objectives.

One way to assess your risk tolerance is to consider your reaction to market fluctuations. If you find yourself getting anxious or losing sleep when the value of your investments declines, you may have a lower risk tolerance. In contrast, if you are unfazed by short-term market volatility and understand that markets tend to recover over the long term, you may have a higher risk tolerance.

Another factor to consider is your financial goals and time horizon. If you have many years until retirement, you may have a higher risk tolerance as you have more time to recover from market downturns. However, if you are nearing retirement, capital preservation and stable income may take precedence, leading to a lower risk tolerance.

It’s important to note that risk tolerance is not a one-size-fits-all concept. Each individual has their own unique financial situation, objectives, and comfort level with risk. What might be an acceptable level of risk for one person may be too conservative or aggressive for another.

It’s also important to differentiate between emotional risk tolerance and financial risk tolerance. Emotional risk tolerance refers to how you emotionally react to market fluctuations, whereas financial risk tolerance pertains to your financial capacity to take on risk based on your income, expenses, and overall financial situation.

When assessing your risk tolerance, it can be helpful to work with a financial advisor. They can help you evaluate your financial goals, analyze your current financial situation, and develop an investment strategy that aligns with your risk tolerance.

A balanced approach is often recommended, involving a diversified portfolio that includes a mix of asset classes suited to your risk tolerance. By diversifying your investments, you can potentially mitigate the impact of market fluctuations and reduce the overall risk of your portfolio.

Remember, risk tolerance is not a static measurement and may change over time. Regularly reassessing your risk tolerance and adjusting your investment strategy as needed can help ensure that your investments align with your changing circumstances and long-term goals.

Determining an Investment Strategy

When planning for retirement, determining an investment strategy is crucial to ensure that you are on track to meet your financial goals. An investment strategy outlines how you will allocate your assets, manage risk, and maximize returns over the long term. Here are key considerations to help you determine the right investment strategy for your retirement:

Financial Goals: Clearly define your financial goals for retirement. Do you want to maintain your current lifestyle, travel extensively, or leave a financial legacy for your loved ones? Understand your goals and prioritize them to guide your investment decisions.

Time Horizon: Consider the number of years until your retirement. A longer time horizon allows for a more aggressive investment approach, as there is more time to recover from short-term market fluctuations. Conversely, a shorter time horizon may require a more conservative strategy to protect accumulated capital.

Risk Tolerance: Assess your risk tolerance, which reflects your ability to handle fluctuations in the value of your investments. Consider your comfort level with market volatility and how much risk you can afford to take based on your financial situation, goals, and emotional resilience.

Diversification: Diversify your investment portfolio by allocating your assets across different asset classes, such as stocks, bonds, real estate, and cash equivalents. Diversification helps reduce the overall risk of your portfolio and provides potential sources of income and growth.

Asset Allocation: Determine the appropriate mix of assets based on your risk tolerance and financial goals. This involves deciding how much of your portfolio should be allocated to each asset class. A balanced approach that aligns with your risk tolerance and time horizon is typically recommended.

Rebalancing: Regularly review and rebalance your investment portfolio to maintain your desired asset allocation. Over time, certain investments may outperform or underperform, causing your asset allocation to drift. Rebalancing ensures that you stay aligned with your predetermined strategy.

Costs and Fees: Consider the costs and fees associated with your investments. High fees can eat into your returns over time. Look for low-cost investment options, such as index funds or exchange-traded funds (ETFs), that offer broad market exposure at a lower cost.

Stay Informed: Stay updated on market trends, economic indicators, and changes in tax laws or retirement regulations. The investment landscape is constantly evolving, and it’s important to stay informed to make informed decisions and adapt your strategy as needed.

It’s important to note that determining an investment strategy is not a one-time activity but an ongoing process. Regularly review and assess your investments, financial goals, and risk tolerance to ensure that your strategy evolves with your changing circumstances and objectives.

Working with a financial advisor can provide invaluable guidance in determining an investment strategy tailored to your needs. They can help evaluate your risk tolerance, develop a customized plan, and provide ongoing support to keep you on track towards a secured retirement.

Working with a Financial Advisor

When planning for retirement and determining how much you should have in investments, working with a financial advisor can provide valuable expertise and guidance. A financial advisor can help you navigate the complexities of retirement planning, develop a personalized strategy, and make informed investment decisions. Here’s how working with a financial advisor can benefit you:

Expert Advice: Financial advisors have specialized knowledge in retirement planning, investment management, and wealth preservation. They can assess your unique financial situation, understand your goals, and provide tailored recommendations to help you achieve a financially secure retirement.

Objective Perspective: Emotions and biases can often cloud financial decisions. A financial advisor provides an objective viewpoint and helps you make rational investment decisions based on your long-term objectives rather than short-term market trends or emotions.

Risk Management: Assessing risk tolerance and managing risk is a critical aspect of retirement planning. A financial advisor can help you understand and navigate different types of risk, develop a diversified investment portfolio, and mitigate potential losses.

Portfolio Management: Building and managing a retirement investment portfolio can be complex. A financial advisor can help you determine an appropriate asset allocation, select suitable investments, and regularly monitor and adjust your portfolio based on changing market conditions and your risk tolerance.

Financial Planning: Retirement planning involves more than just investments. A financial advisor can assist with comprehensive financial planning that encompasses budgeting, tax planning, estate planning, and insurance to ensure all aspects of your financial well-being are considered.

Maximizing Retirement Benefits: Financial advisors can provide guidance on maximizing retirement benefits from sources such as Social Security and company pension plans. They can help you understand the implications of different claiming strategies and make decisions that optimize your retirement income.

Education and Empowerment: Working with a financial advisor provides an opportunity to educate yourself about various investment options and retirement strategies. Advisors can explain complex financial concepts, answer your questions, and empower you to make informed decisions about your financial future.

Long-Term Partnership: Building a relationship with a financial advisor means having a trusted partner who can provide ongoing support and advice throughout your retirement journey. Regular meetings and reviews ensure that your financial plan remains aligned with your goals and adjusts to any changes in your circumstances.

It’s important to choose a reputable and qualified financial advisor who has expertise in retirement planning and a fiduciary duty to act in your best interest. Consider credentials, experience, and client reviews when selecting an advisor to ensure a good fit for your specific needs.

Remember, while working with a financial advisor is valuable, it does not absolve you of your own responsibility to stay informed and actively participate in the decision-making process. Collaboration with your advisor can lead to a more confident and successful retirement strategy.

Frequently Asked Questions

1. How much should I have in investments for retirement?

The amount needed for retirement varies based on individual circumstances, goals, and expected expenses. It is recommended to consult with a financial advisor who can assess your specific situation and help determine a target savings goal.

2. What is the ideal age to start saving for retirement?

The earlier you start saving for retirement, the better. Starting in your twenties or thirties allows you to take advantage of compounding returns and have a longer time horizon to build a substantial nest egg. However, it’s never too late to start saving and investing, even if you are closer to retirement age.

3. Should I prioritize paying off debt or saving for retirement?

It’s generally advisable to strike a balance between paying off high-interest debt and saving for retirement. High-interest debt can eat into your savings, so it’s important to address it. However, it’s also crucial to start saving for retirement early to take advantage of compounding returns over time.

4. How do I determine my risk tolerance?

Assessing your risk tolerance involves evaluating your comfort level with market volatility, financial goals, time horizon until retirement, and overall financial situation. Understanding your risk tolerance helps shape your investment strategy and asset allocation.

5. What is the role of Social Security in retirement?

Social Security provides a base income for many retirees. The amount you receive depends on your earnings history and the age at which you start collecting benefits. It’s important to consider Social Security benefits along with other retirement income sources to plan for a secure retirement.

6. Do I need a financial advisor for retirement planning?

While not mandatory, a financial advisor can provide valuable expertise, guidance, and support in retirement planning. They can help you navigate complex financial decisions, develop a personalized strategy, and keep your retirement plan on track.

7. How often should I review my retirement investments?

Regularly reviewing your retirement investments is important to ensure that they align with your goals and risk tolerance. Annual reviews or reviews during significant life events can help you make any necessary adjustments to your investment strategy.

8. What is the best way to diversify my retirement portfolio?

Diversification involves spreading your investments across different asset classes, such as stocks, bonds, real estate, and cash equivalents. Allocating your assets based on your risk tolerance and investment goals can help mitigate risk and maximize returns.

9. Can I make changes to my retirement plan as I approach retirement?

Absolutely! As you approach retirement, it’s important to reassess your retirement plan and make any necessary adjustments. This may involve adjusting your asset allocation, evaluating your retirement income sources, and ensuring your investments align with your desired retirement lifestyle.

10. How can I optimize my retirement savings and investments?

Optimizing your retirement savings and investments involves careful planning, regular contributions, diversification, and adjusting your investment strategy when needed. Working with a financial advisor can provide personalized assistance and expertise in maximizing your retirement assets.

Conclusion

Planning for retirement and determining how much to have in investments is a critical aspect of achieving financial security in your golden years. By considering factors such as age, retirement goals, expected expenses, and sources of retirement income, you can develop a comprehensive retirement strategy.

Assessing your risk tolerance and determining an appropriate investment strategy are key components of successful retirement planning. It’s important to work with a financial advisor who can provide guidance, expertise, and insights tailored to your specific financial situation and goals.

Remember that retirement planning is an ongoing process. Regularly review your investments, adjust your strategy if necessary, and stay informed about changes in the financial landscape. Revisiting your retirement plan periodically will help ensure that it remains aligned with your evolving circumstances and objectives.

Finally, while there are general guidelines and recommendations, each individual’s retirement journey is unique. It’s essential to personalize your retirement plan based on your individual needs, preferences, and financial goals.

By taking the time to plan, seek expert advice, and make informed decisions, you can secure a comfortable and enjoyable retirement. Start early, stay disciplined, and remember that the actions you take today will shape your financial future for years to come.