What Are Investments?

Investments refer to the allocation of money or resources with the expectation of generating a return or profit over time. In simple terms, it is the act of putting your money to work in order to make more money. By investing, individuals can potentially grow their wealth and achieve financial goals.

There are various forms of investments that people can choose from, including stocks, bonds, mutual funds, real estate, and even starting a business. Each investment option carries its own level of risk and potential returns.

When you invest in stocks, you are buying shares of ownership in a company. The value of those shares can fluctuate based on the performance of the company and market conditions. Bonds, on the other hand, are debt instruments issued by governments or companies. Investors lend money to the issuer and receive interest payments until the bond matures.

Mutual funds are investment vehicles that pool money from multiple investors to invest in a diversified portfolio of stocks, bonds, or other assets. Real estate investments involve buying properties, such as houses or commercial buildings, with the goal of renting them out or selling them at a higher price in the future. Starting a business is another form of investment where individuals invest their time, money, and effort in the hopes of generating profits.

Regardless of the type of investment, the ultimate goal is to generate a positive return on the initial investment. This return can come in the form of capital gains, where the value of the investment increases, or through dividends or interest payments.

Investing is not without risks. The value of investments can go down as well as up, and there is always a possibility of losing some or all of the initial investment. It is important to assess your risk tolerance and conduct thorough research before making any investment decisions.

Overall, investments provide individuals with an opportunity to grow their wealth, generate passive income, and achieve long-term financial stability. Whether through stocks, bonds, real estate, or starting a business, investing can be a powerful tool in building a secure financial future.

Why Should You Invest?

Investing is a crucial step towards securing your financial future and achieving your long-term goals. Here are several reasons why you should consider investing:

1. Wealth Accumulation: Investing allows your money to work for you and potentially grow over time. By earning returns on your investments, you can accumulate wealth and increase your overall net worth. This can provide financial security and open up opportunities for a comfortable retirement or the pursuit of your dreams.

2. Beat Inflation: Inflation erodes the purchasing power of your money over time. By investing, you have the opportunity to earn returns that outpace inflation, ensuring that your money retains its value and can afford you the same lifestyle in the future as it does today.

3. Passive Income: Certain investments, such as rental properties or dividend-paying stocks, can generate regular income without requiring active involvement. This passive income can supplement your primary source of earnings and provide financial stability.

4. Retirement Planning: Investing is a crucial component of retirement planning. By starting early and consistently investing, you can build a substantial retirement portfolio that will support you during your golden years. The power of compounding returns can significantly accelerate your savings, allowing you to maintain your desired lifestyle after retirement.

5. Achieve Financial Goals: Investing provides a pathway to achieving specific financial goals. Whether it’s buying a home, funding your child’s education, or starting a business, investing can help you accumulate the necessary funds over time. By setting clear goals and aligning your investment strategy accordingly, you can work towards realizing your aspirations.

6. Diversification: Investing in different asset classes helps spread the risk and reduces the impact of any single investment’s performance. Diversification safeguards your portfolio against market volatility and boosts the potential for consistent returns. A diversified investment strategy enables you to balance potential gains and losses, preserving your wealth for the long term.

7. Take Advantage of Compound Interest: Compound interest is the concept of earning interest on both the initial investment and the accumulated interest over time. By investing early and allowing the power of compounding to take effect, your returns can multiply exponentially, significantly enhancing your investment’s value in the long run.

Investing is not without risks, and it’s important to conduct thorough research and seek professional advice. However, by understanding the potential benefits and taking a disciplined approach, investing can position you for financial success and help you fulfill your aspirations.

Types of Investments

When it comes to investing, there are various options available to individuals, each with its own characteristics and potential returns. Here are some common types of investments:

1. Stocks: Investing in stocks involves buying shares of ownership in a publicly traded company. Stock prices can fluctuate based on the company’s performance, market conditions, and investor sentiment. Stocks offer the potential for capital appreciation and may also pay dividends.

2. Bonds: Bonds are debt instruments issued by governments, municipalities, or corporations. When you buy a bond, you are essentially lending money to the issuer in exchange for regular interest payments and the return of the principal at maturity.

3. Mutual Funds: Mutual funds pool money from multiple investors to invest in a diversified portfolio of stocks, bonds, or other assets. They are managed by professional investment firms and offer investors the opportunity to access a wide range of investments without the need for extensive knowledge or time commitment.

4. Exchange-Traded Funds (ETFs): Similar to mutual funds, ETFs are investment funds that own assets such as stocks, bonds, or commodities. However, unlike mutual funds, ETFs trade on stock exchanges like individual stocks and can be bought or sold throughout the trading day at market prices.

5. Real Estate: Investing in real estate involves purchasing properties with the goal of generating rental income or profiting from property appreciation. Real estate investments can include residential properties, commercial buildings, or even real estate investment trusts (REITs) that allow you to invest in real estate indirectly.

6. Commodities: Commodities are raw materials or primary agricultural products that can be bought and sold, such as gold, oil, or agricultural products. Investing in commodities can provide diversification to a portfolio and act as a hedge against inflation.

7. Cryptocurrencies: Cryptocurrencies, such as Bitcoin or Ethereum, have gained popularity as an investment option. These digital currencies operate on decentralized networks and offer potential returns through price appreciation. However, they also carry significant volatility and risk.

8. Retirement Accounts: Retirement accounts, such as 401(k)s or Individual Retirement Accounts (IRAs), are special investment vehicles designed to help individuals save for retirement. These accounts offer tax advantages and can include a variety of investment options, such as stocks, bonds, or mutual funds.

It’s important to note that each investment type carries its own level of risk and potential return. It’s essential to consider factors such as your risk tolerance, investment goals, and time horizon when deciding on the appropriate mix of investments for your portfolio.

Additionally, diversification is key to managing risk and maximizing potential returns. By diversifying your investments across different asset classes and investment types, you can help ensure that your portfolio is not overly reliant on the performance of a single investment.

Remember to conduct thorough research, seek professional advice, and stay informed about market trends and economic conditions when making investment decisions.

How Much Does the Average American Have in Investments?

The amount of investments held by the average American can vary significantly depending on factors such as age, income level, education, and regional differences. While it’s challenging to pinpoint an exact figure, we can look at some general trends and statistics to understand the landscape.

1. Net Worth: According to the Federal Reserve’s Survey of Consumer Finances, the median net worth of American households was $121,700 in 2019. This figure includes all assets, such as investments, real estate, and savings, minus any liabilities.

2. Investment Allocation: Investments typically constitute a portion of an individual’s overall net worth. The allocation between different types of investments varies based on personal preference and financial goals. Common investment categories include stocks, bonds, mutual funds, real estate, and retirement accounts.

3. Stock Ownership: A Gallup poll conducted in 2020 found that approximately 55% of Americans reported owning stocks, either individually or through an investment account like a 401(k) or IRA. This indicates that a significant portion of the population has exposure to the stock market.

4. Retirement Accounts: Retirement accounts play a critical role in Americans’ investment portfolios. The Employee Benefit Research Institute reports that as of 2018, the median IRA and 401(k) account balance for individuals aged 35-64 was around $60,000, with higher amounts for those closer to retirement age.

5. Regional Differences: Investment amounts can vary depending on geographical location. Urban areas with higher costs of living and more affluent populations tend to have larger average investment holdings compared to rural or less affluent areas.

6. Wealth Disparity: It’s important to acknowledge that investment holdings are not distributed evenly across the population. There is a significant wealth disparity in the United States, with a small percentage of individuals holding a large portion of the total wealth. This skews the average investment figures higher for those at the top end of the wealth spectrum.

It’s worth noting that the average investment amount is just a general indicator and may not reflect an individual’s specific financial situation. Factors such as personal goals, risk tolerance, and available income to invest all contribute to the investment amounts held by different individuals.

To increase their investment holdings, individuals can employ strategies such as saving a portion of their income, maximizing contributions to retirement accounts, diversifying their investment portfolio, and seeking guidance from financial advisors.

Ultimately, it’s important for individuals to assess their own financial goals and take steps towards building an investment portfolio that aligns with their objectives and risk tolerance.

Factors That Affect Investment Amounts

Several factors can influence the amount of investments held by individuals. Understanding these factors can provide insights into why investment amounts vary among different individuals and households. Here are some key factors that can affect investment amounts:

1. Age: Age plays a significant role in investment amounts. Younger individuals generally have fewer accumulated assets and may have limited financial resources available for investments. As individuals progress through their careers and accumulate wealth, they tend to have a higher capacity to invest.

2. Income Level: Income level is a critical factor in determining investment amounts. Individuals with higher incomes often have more disposable income available to allocate towards investments. This enables them to save and invest larger amounts compared to those with lower incomes.

3. Education: Education level can impact investment amounts in several ways. Higher education can lead to better job prospects and higher incomes, providing individuals with more financial resources to allocate towards investments. Additionally, individuals with higher levels of education may have a better understanding of investing and the importance of long-term financial planning.

4. Financial Literacy: Financial literacy plays a crucial role in investment decisions. Individuals with a higher level of financial literacy are more likely to be aware of the benefits of investing and make informed investment choices. They may have a better understanding of risk management and asset allocation, leading to larger investment amounts.

5. Risk Tolerance: Risk tolerance varies among individuals. Those with a higher risk tolerance may be more willing to invest larger amounts in higher-risk assets, such as stocks or real estate. On the other hand, individuals with a lower risk tolerance may prefer safer investments, such as bonds or savings accounts, resulting in potentially lower investment amounts.

6. Financial Goals: Financial goals have a significant impact on investment amounts. Individuals with ambitious financial goals, such as early retirement or funding a child’s education, may be motivated to invest larger amounts. Clear and achievable financial goals can provide the necessary motivation to allocate a significant portion of income towards investments.

7. Access to Investment Options: Accessibility to various investment options can influence investment amounts. Some investment opportunities, such as certain stocks or private equity, may require higher minimum investments, limiting the participation of individuals with lower investment amounts.

8. Economic Conditions: Economic conditions can impact investment amounts. During periods of economic uncertainty or recession, individuals may have a lower appetite for investing larger amounts due to concerns about market volatility and a desire to preserve cash. Conversely, during economic booms or periods of optimism, individuals may be more inclined to invest larger amounts in hopes of higher returns.

It’s essential to note that these factors tend to work together, and the influence of each factor can vary from person to person. Ultimately, personal circumstances and financial goals will determine the investment amounts that individuals are comfortable with.

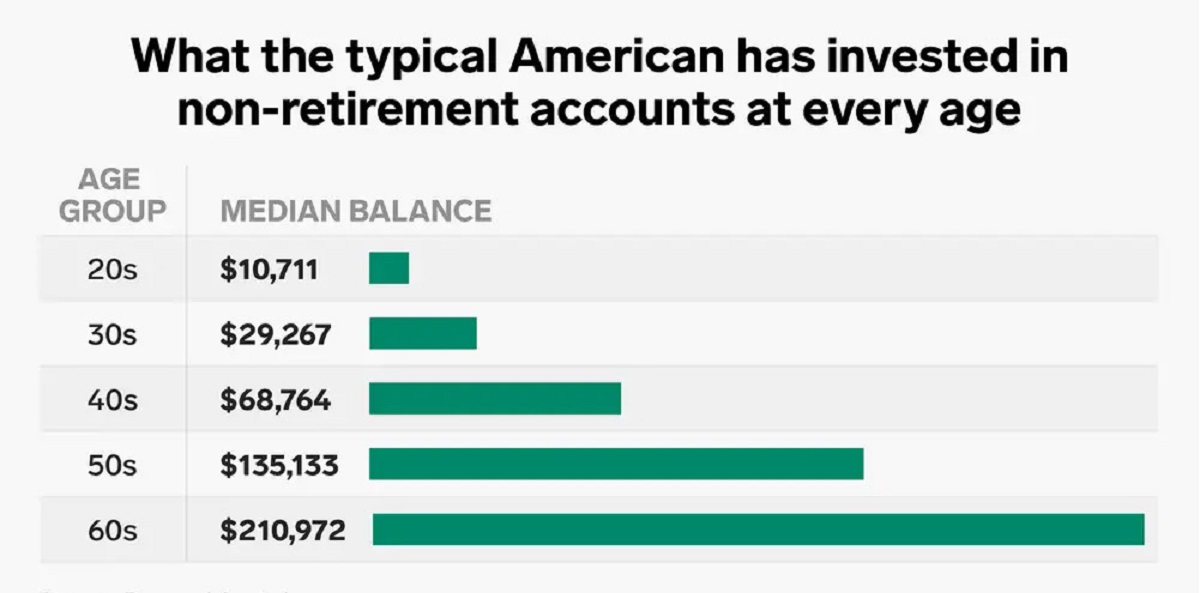

Age and Investments

Age is a significant factor that influences investment decisions and strategies. As individuals progress through different stages of life, their investment goals, risk tolerance, and financial circumstances typically evolve. Here’s a closer look at how age impacts investments:

1. Younger Individuals: Younger individuals, such as those in their 20s and 30s, often have a longer time horizon for their investment goals, such as retirement. They can afford to take on more risk and may focus on long-term growth investments, such as stocks or equity-focused mutual funds. They have the advantage of compounding returns over time, allowing their investments to potentially grow significantly.

2. Middle-Aged Individuals:Middle-aged individuals, typically in their 40s and 50s, often have increased financial responsibilities, such as paying off mortgages, funding their children’s education, or supporting aging parents. At this stage, their investment focus may shift towards a more balanced approach, aiming for a mix of growth and income-generating investments. They may also prioritize diversification and risk management to safeguard their accumulated wealth.

3. Pre-Retirement Individuals: Pre-retirement individuals, usually in their late 50s and early 60s, begin to focus more on capital preservation and income generation. They may rebalance their investment portfolio to include a higher percentage of fixed-income assets, such as bonds or dividend-paying stocks. As retirement draws nearer, they tend to become more risk-averse and prioritize preserving their accumulated wealth for a steady stream of income during retirement.

4. Retirees: Retirees, typically aged 65 and older, often transition from accumulating wealth to deploying their savings to generate income during retirement. With a lower risk capacity, they may shift towards more conservative investments, such as bonds, certificates of deposit (CDs), or annuities. Some retirees may also use a portion of their savings to purchase immediate or deferred annuities, providing a guaranteed income stream for life.

It’s important to note that these age-related investment patterns are generalizations, and individual circumstances play a critical role in determining investment strategies. Personal factors like risk tolerance, financial health, and specific financial goals can differ significantly among individuals within the same age group.

Regardless of age, key investment principles such as diversification, regular savings, and periodic review of investment goals remain relevant. Periodically reassessing investment strategies and seeking professional advice can help individuals optimize their portfolios based on their changing needs and life stages.

Furthermore, with increasing life expectancy and changing retirement dynamics, many individuals are now extending their investment horizon well into their retirement years. This extended time horizon calls for continued growth investments to combat inflation and sustain retirement income for a longer duration.

In summary, age is closely intertwined with investment decisions. Understanding the investment needs and risks associated with each life stage can help individuals make informed choices and develop appropriate investment strategies to meet their long-term financial goals.

Income Level and Investments

Income level is a significant factor that influences an individual’s ability to invest and the amount they can allocate towards investment activities. Here’s a closer look at how income level impacts investments:

1. Investment Capacity: Higher income levels generally provide individuals with greater capacity to invest. With a larger disposable income, individuals can allocate a larger portion of their earnings towards investments. This enables them to build a more substantial investment portfolio and potentially benefit from higher returns.

2. Investment Options: Higher income levels can open doors to a broader range of investment options. Certain types of investments, such as private equity or hedge funds, may have higher minimum investment requirements that are more attainable for individuals with higher incomes. This allows them to diversify their portfolio and potentially access higher potential returns.

3. Risk Appetite: Income level can also influence an individual’s risk tolerance. Those with higher incomes may be more willing to take on higher-risk investments, such as stocks or real estate, in pursuit of higher returns. Conversely, individuals with lower incomes may have a more conservative approach to investing, opting for safer investments like bonds or savings accounts.

4. Retirement Planning: Income level plays a crucial role in retirement planning and the ability to build a sufficient nest egg. Higher income earners may have more financial resources available to contribute to retirement accounts, such as 401(k)s or IRAs, and take advantage of matching contributions from employers. This provides them with a stronger foundation for retirement and the potential for a more comfortable lifestyle in their golden years.

5. Access to Financial Advice: Individuals with higher incomes may have greater access to professional financial advice. Financial advisors can provide guidance on investment strategies, portfolio diversification, and wealth management. Having access to expert advice can assist individuals in making more informed investment decisions and potentially optimizing their investment returns.

6. Lifestyle Considerations: Income level can also impact an individual’s lifestyle choices, which can, in turn, affect their ability to invest. Higher-income individuals may have greater flexibility and financial freedom, allowing them to allocate more funds towards investment activities. Conversely, individuals with lower incomes may face budgetary constraints and have less disposable income available for investments.

While higher income levels can provide advantages in terms of investment capacity and options, it’s important to note that investing is not exclusively for high-income individuals. Individuals with lower incomes can still engage in investing by starting small and gradually increasing their investment contributions over time.

Investing is a tool that can help individuals, regardless of income level, build wealth, secure their financial future, and achieve their long-term goals. It requires careful planning, research, and a disciplined approach to ensure investment objectives are met.

Ultimately, it’s crucial for individuals of all income levels to prioritize financial education, set realistic investment goals, and seek professional advice when needed. This holistic approach can empower individuals to make informed investment decisions and maximize their investment potential.

Education and Investments

Education level is a factor that can significantly influence an individual’s approach to investing and their investment outcomes. Here’s a closer look at how education impacts investments:

1. Financial Literacy: Education plays a crucial role in developing financial literacy, which is the knowledge and understanding of financial concepts and strategies. Individuals with higher levels of education tend to have a better grasp of investment principles, risk management, and the importance of long-term financial planning. This financial literacy empowers them to make informed investment decisions.

2. Understanding Investment Options: Higher education levels often provide individuals with a deeper understanding of investment options available to them. They may have knowledge of different investment vehicles, such as stocks, bonds, mutual funds, or real estate, and understand how these options align with their financial goals and risk tolerance. This knowledge enables them to make educated choices when it comes to constructing their investment portfolio.

3. Research Abilities: Education fosters critical thinking and research skills, which can benefit investment decisions. Individuals with higher levels of education may be more adept at conducting thorough research on investment opportunities, analyzing financial statements, and evaluating market trends. These skills can contribute to more informed investment selections and potentially superior investment returns.

4. Risk Appetite: Education level can influence an individual’s risk appetite. Those with higher levels of education may be more open to taking calculated risks, understanding the potential rewards and pitfalls of their investment decisions. They may be more comfortable with investments that have higher volatility or longer investment horizons, potentially increasing their overall return potential.

5. Access to Financial Resources: Higher education often leads to higher income potential and access to better job opportunities. This can provide individuals with greater financial resources to allocate towards investments. With more disposable income, they can contribute larger amounts to their investment portfolios, accelerating their wealth-building potential.

6. Entrepreneurship and Business Ventures: Education can also foster an entrepreneurial mindset. Individuals with higher education levels may be more inclined to start their own businesses or engage in entrepreneurial ventures. This can introduce additional investment opportunities and potential higher returns, albeit with increased risk.

It’s important to remember that while higher education can provide advantages in terms of financial literacy and investment know-how, anyone can learn and improve their investment knowledge regardless of their educational background. Resources such as books, online courses, and financial literacy programs can help individuals at any education level bolster their understanding of investment fundamentals.

Regardless of educational background, it’s crucial for individuals to continuously seek knowledge, expand their financial literacy, and stay informed about changing market dynamics. Regularly reassessing investment strategies and seeking professional advice when needed can contribute to improved investment outcomes.

While education can provide a solid foundation, successful investing requires a combination of knowledge, experience, and a disciplined approach. By continuously learning and adapting, individuals can enhance their investment decision-making and work towards achieving their financial goals.

Regional Differences in Investment Amounts

Investment amounts can vary significantly based on geographical location, as regional factors impact individuals’ financial situations and investment behaviors. Here’s a look at some of the key regional differences in investment amounts:

1. Cost of Living: The cost of living varies across different regions, which directly affects individuals’ discretionary income and capacity to invest. In areas with higher living costs, individuals may have less money available to allocate towards investments, resulting in potentially lower investment amounts compared to regions with lower living costs.

2. Economic Development: Regions with stronger economic development tend to have higher average investment amounts. Robust economies create more job opportunities and higher income levels, providing individuals with greater financial resources to invest. Stronger economic development also attracts investors and businesses, creating investment opportunities and potentially contributing to higher investment amounts within those regions.

3. Real Estate Market: Real estate markets vary regionally, and investment amounts can be influenced by property prices and rental potential. In areas with high property values, individuals may need more significant investment amounts to purchase properties. Higher rental income potential may encourage individuals to invest more in real estate, particularly in regions with higher demand for rental properties.

4. Access to Investment Opportunities: Access to investment opportunities can vary geographically. Some areas may have more robust financial markets, providing residents with a broader range of investment options. On the other hand, remote or underserved regions may have limited investment opportunities, potentially resulting in lower investment amounts.

5. Cultural Factors: Cultural factors can influence investment behaviors within different regions. Some cultures may prioritize savings or investments, leading to higher investment amounts even in regions with lower average income levels. Conversely, cultures that focus more on immediate consumption or have lower risk tolerance may reflect lower investment amounts.

6. Government Policies and Incentives: Government policies and incentives can impact investment amounts regionally. Some regions may offer tax incentives or investment-friendly policies that encourage residents to invest more. These incentives can drive higher investment activity and potentially increase investment amounts within those regions.

It’s important to note that while regional differences exist, investment amounts are not solely determined by geography. Individual circumstances, such as income level, financial goals, and risk tolerance, also play a significant role in investment decisions irrespective of regional factors.

Regardless of the region, individuals can work towards increasing their investment amounts by focusing on financial planning, building their income streams, and making informed investment decisions. Seeking guidance from financial advisors and staying informed about investment trends and opportunities can help individuals maximize their investment potential regardless of their location.

Ultimately, individuals should consider their own unique circumstances, financial goals, and risk tolerance when determining their investment amounts, regardless of regional differences.

How to Increase Your Investments

Increasing your investments is an essential step towards building wealth and achieving your financial goals. Here are some strategies to help you boost your investment portfolio:

1. Increase Your Savings: One of the simplest ways to increase your investments is to save more. Review your budget and identify areas where you can cut expenses, then redirect that money towards your investment accounts. Set up automatic transfers from your paycheck or bank account to ensure consistent savings each month.

2. Maximize Your Retirement Contributions: If you have access to a retirement account such as a 401(k) or an Individual Retirement Account (IRA), strive to contribute the maximum allowed amount. These accounts offer tax advantages and potential employer matching contributions, allowing your investments to grow more rapidly.

3. Diversify Your Investments: Consider diversifying your investment portfolio to spread the risk and potentially increase returns. Allocate your investments across various asset classes, such as stocks, bonds, real estate, and commodities. Diversification helps protect your portfolio from market volatility and ensures you have exposure to different investment opportunities.

4. Automate Your Investments: Set up automated investment contributions to take advantage of dollar-cost averaging. By automatically investing a fixed amount at regular intervals, you can buy more shares when prices are lower and fewer shares when prices are higher. This strategy helps even out market fluctuations over time.

5. Reinvest Dividends and Capital Gains: If you receive dividends or capital gains from your investments, consider reinvesting them instead of cashing them out. Reinvesting these earnings allows your investment to compound over time, potentially accelerating your portfolio growth.

6. Educate Yourself: Continuously educate yourself about investing to make informed decisions. Read books, attend seminars, and follow reputable financial websites to enhance your knowledge. Understanding investment strategies and staying informed about market trends can empower you to make smarter investment choices.

7. Seek Professional Advice: Consider working with a qualified financial advisor to help you develop a personalized investment plan. A financial advisor can assess your financial situation, risk tolerance, and goals to provide tailored investment recommendations. They can also provide guidance during market volatility or changes in your circumstances.

8. Take Advantage of Employer Benefits: If your employer offers investment-related benefits, such as a matching contribution to a retirement plan or stock purchase plans, make sure you take full advantage of these offerings. Employer benefits can significantly boost your investment amounts without requiring additional personal contributions.

9. Stay Disciplined and Stay the Course: Investing requires discipline and a long-term perspective. Stick to your investment plan, avoid making impulsive decisions based on short-term market fluctuations, and resist the temptation to time the market. Consistent contributions and a patient approach can yield significant results over time.

10. Review and Adjust Your Portfolio: Regularly review your investment portfolio to ensure it aligns with your goals and risk tolerance. Rebalance your portfolio periodically by adjusting the allocation of your investments based on your investment strategy and market conditions.

Remember, increasing your investments is a gradual process. It requires commitment, patience, and a proactive approach to saving and investing. By implementing these strategies and monitoring your progress, you can steadily increase your investments and work towards achieving your long-term financial objectives.

Conclusion

Investing is a powerful tool that can help individuals build wealth, secure their financial future, and achieve their goals. Whether you’re just starting or looking to grow your existing investments, understanding the factors that influence investment amounts and implementing strategies to increase your investments is crucial.

Factors such as age, income level, education, and region can impact the amount individuals are able to invest. Younger individuals may focus on growth investments, while those nearing retirement tend to prioritize capital preservation and income generation. Higher income levels provide individuals with greater investment capacity, access to a broader range of investment options, and potentially higher risk tolerance. Education, financial literacy, and access to resources play a pivotal role in making informed investment decisions.

To increase your investments, consider strategies such as increasing your savings, maximizing contributions to retirement accounts, diversifying your portfolio, and automating your investments. Educate yourself about investing and seek professional advice to make well-informed choices. Take full advantage of employer benefits and continuously monitor and adjust your portfolio to stay on track with your goals.

Investing is a long-term endeavor that requires discipline, patience, and a commitment to your financial well-being. By implementing these strategies and remaining focused on your investment objectives, you can steadily increase your investments and work towards financial security and the attainment of your aspirations.

Remember, everyone’s investment journey is unique, and it’s crucial to align your investment strategy with your individual circumstances, risk tolerance, and long-term goals. Regularly assess your progress, stay informed, and adapt your strategies as needed to stay on the path to financial success.