Introduction

Living off investments is a financial goal that many people aspire to achieve. It involves generating enough income from your investment portfolio to cover your everyday expenses, without relying on traditional employment or a fixed income. This concept has gained popularity as individuals seek financial independence and the freedom to pursue their passions and live life on their own terms.

By strategically allocating your assets and making wise investment decisions, you can potentially create a passive income stream that allows you to sustain your desired lifestyle. However, determining how much you need to live off investments requires careful planning and consideration of various factors.

In this article, we will explore the key aspects of living off investments and provide insights into calculating the portfolio size required. We will discuss evaluating your current expenses, considering your desired lifestyle, estimating your annual expenses, and understanding the 4% rule – a widely accepted guideline used for retirement planning. We will also delve into the factors that can impact your investment needs, such as inflation, market conditions, and unforeseen expenses.

Additionally, we will touch upon managing investment risks, monitoring and adjusting your investment strategy, and ensuring your portfolio remains aligned with your goals. Whether you are planning for retirement, seeking financial independence, or simply curious about living off investments, this article aims to provide you with a comprehensive overview to help you make informed decisions and navigate the journey towards financial freedom.

What is living off investments?

Living off investments refers to the ability to generate enough income from your investment portfolio to cover your living expenses and sustain your desired lifestyle. It is an alternative to relying solely on traditional employment or a fixed income source. By strategically investing your money in a diverse range of assets, such as stocks, bonds, real estate, and other investment vehicles, you can potentially generate a steady stream of passive income.

Living off investments allows individuals to have greater financial flexibility, as it provides the opportunity to pursue personal goals and passions without the constraints of a traditional job. It offers the freedom to retire at an earlier age, travel the world, start a business, or spend more time with family and loved ones.

However, living off investments requires careful planning and consideration. It involves evaluating your financial needs, determining your risk tolerance, and creating a well-diversified investment portfolio that aligns with your goals and objectives. It is crucial to strike a balance between generating sufficient income and preserving the value of your investments over the long term.

Living off investments can be achieved through various strategies, including:

- Dividend Income: Investing in dividend-paying stocks or funds that distribute a portion of their earnings to shareholders on a regular basis.

- Rental Income: Owning investment properties and renting them out to generate monthly rental income.

- Interest Income: Investing in fixed-income securities, such as bonds or certificates of deposit, that provide regular interest payments.

- Capital Gains: Selling investments at a profit and reinvesting the proceeds to generate additional income.

It is important to note that living off investments requires a well-thought-out financial plan and a long-term perspective. It is not a get-rich-quick scheme but rather a journey that requires discipline, patience, and a commitment to managing and growing your investment portfolio.

Determining how much you need to live off investments

Calculating how much you need to live off investments is a critical step in the financial planning process. It involves evaluating your current expenses, considering your desired lifestyle, estimating your annual expenses, and understanding the concept of the 4% rule.

1. Evaluating your current expenses: Begin by analyzing your current expenses to get a clear understanding of how much you spend each month. This includes housing costs, utilities, transportation, groceries, healthcare, and other essential expenses. Consider factors like inflation and potential changes in your spending habits during retirement.

2. Considering your desired lifestyle: Determine the lifestyle you want to maintain or achieve during your retirement or financial independence. Consider factors such as travel, hobbies, dining out, entertainment, and any other discretionary expenses. This will help you estimate your future expenses and gauge the level of income you need to support that lifestyle.

3. Estimating your annual expenses: Once you have an understanding of your current expenses and desired lifestyle, estimate your annual expenses by multiplying your monthly expenditure by 12. This will give you a rough idea of how much income you need to generate from your investment portfolio each year to cover your expenses.

4. Understanding the 4% rule: The 4% rule is a guideline often used in retirement planning. It suggests that you can withdraw 4% of your investment portfolio’s value in the first year of retirement and adjust that amount for inflation in subsequent years. This rule is based on historical market performance and is aimed at providing a sustainable income stream for at least 30 years. By applying the 4% rule, you can estimate the size of your investment portfolio needed to support your desired annual expenses.

While the 4% rule serves as a useful starting point, it is important to consider other factors such as your risk tolerance, investment returns, and potential changes in your circumstances. Consulting with a financial advisor can provide valuable insights and help you create a personalized plan tailored to your specific financial situation and goals.

Evaluating your current expenses

When determining how much you need to live off investments, it is crucial to evaluate your current expenses. This step provides a foundation for understanding your financial needs and helps you plan for a sustainable income stream from your investment portfolio.

Gather and assess your financial records: Begin by collecting all of your financial records, including bank statements, credit card bills, utility bills, and any other documents that reflect your monthly expenses. This will give you a comprehensive overview of your current spending habits.

Track your expenses: Take the time to meticulously track all of your expenses for a few months. This will help you identify any patterns or areas where you may be overspending. Make note of both essential expenses, such as housing, utilities, transportation, groceries, and healthcare, as well as discretionary expenses, like dining out, entertainment, and hobbies.

Categorize your expenses: Once you have tracked your expenses, categorize them into different groups. This could include categories like housing, transportation, food, entertainment, healthcare, and debt payments. Categorizing your expenses will give you a clearer picture of where your money is going and enable you to identify areas where you may be able to cut back.

Consider potential changes in retirement: As you evaluate your current expenses, keep in mind that your spending patterns in retirement may differ. For example, you may no longer have work-related expenses, such as commuting costs or wardrobe expenses. On the other hand, you may have additional expenses related to travel, hobbies, or healthcare. Take these potential changes into account when estimating your future expenses.

Factor in inflation: Inflation is an important consideration when evaluating your current expenses. Prices tend to rise over time, reducing the purchasing power of your money. Consider historical inflation rates and project future inflation to estimate how your expenses may increase in the future. This will help ensure that your investment income keeps up with rising costs.

Evaluating your current expenses provides a solid foundation for determining how much you need to live off investments. It allows you to create a realistic budget, identify areas for potential cost savings, and gain a better understanding of your financial needs both now and in the future. Remember to regularly review and update your expenses as circumstances and priorities change, as this will guide your investment and retirement planning decisions.

Considering your desired lifestyle

When determining how much you need to live off investments, it’s essential to consider your desired lifestyle. Your lifestyle choices play a significant role in shaping your financial needs and determining the level of income you require from your investment portfolio.

Visualize your ideal lifestyle: Take some time to envision how you want to live during your retirement or financial independence. Consider factors such as travel, hobbies, dining out, entertainment, and other activities that bring you joy. Think about the experiences and comforts that are important to you.

Estimate your discretionary expenses: Once you have a vision of your ideal lifestyle, estimate the potential expenses associated with it. This includes discretionary expenses that go beyond the basic necessities. Decide how often you plan to travel, dine out at restaurants, attend events, pursue hobbies, or undertake other activities that enhance your quality of life.

Account for any significant life changes: Consider any significant life changes that may impact your desired lifestyle and financial needs. For example, if you plan to downsize your home, this can have an effect on your housing expenses. If you anticipate major healthcare costs, such as long-term care or medical treatments, factor those into your calculations as well.

Balance your desires with financial realities: While it’s important to prioritize your happiness and fulfillment, it’s equally crucial to strike a balance between your desired lifestyle and your financial capabilities. Consider your investment portfolio’s growth potential, expected returns, and any limitations or constraints that may exist. This will ensure that your lifestyle aspirations are realistic and achievable without jeopardizing your long-term financial security.

Adjust financially as needed: Throughout your retirement or financial independence journey, be open to making adjustments as needed. Your desired lifestyle may evolve over time, and your financial circumstances may also change. Regularly review your expenses, income, and investment performance to ensure that they remain aligned with your goals.

Considering your desired lifestyle helps you gauge the level of income required to support it. It allows you to prioritize your wants and needs, ensuring that you can enjoy the activities and experiences that matter most to you. By striking a balance between your aspirations and your financial realities, you can create a plan that provides both financial security and the freedom to live the life you envision.

Estimating your annual expenses

Estimating your annual expenses is a crucial step in determining how much you need to live off investments. This process involves projecting your current expenses into the future, accounting for potential changes and considering both essential and discretionary expenses.

Review your current expenses: Begin by reviewing your current monthly expenses. This includes housing costs, utilities, transportation, groceries, healthcare, and any other essential expenses. Analyze and note down the amounts you spend in each category.

Factor in potential changes: Consider any potential changes in your expenses that may occur during your retirement or financial independence. For example, you may no longer have work-related expenses, such as commuting costs or professional wardrobe expenses. On the other hand, you may have additional expenses related to travel, hobbies, or healthcare. Adjust your current expenses accordingly.

Consider inflation: Take into account the impact of inflation on your annual expenses. Over time, the cost of goods and services tends to rise. Historical inflation rates can provide a rough estimate, but be sure to project future inflation based on your specific circumstances. This will help ensure that your income from investments keeps up with the rising cost of living.

Separate essential and discretionary expenses: Divide your expenses into essential and discretionary categories. Essential expenses include housing, utilities, food, healthcare, and insurance. Discretionary expenses cover non-essential activities, such as vacations, entertainment, dining out, and hobbies. This classification will help you prioritize your spending and determine which expenses are necessary for your desired lifestyle.

Calculate your annual expenses: Multiply your monthly expenses by 12 to estimate your annual expenses. Consider any one-time or irregular expenses that may occur throughout the year, such as annual insurance premiums or vacations. Add these to your annual expenses to ensure accuracy.

Regularly review and adjust your estimates: Keep in mind that your annual expenses may fluctuate over time. Regularly review and update your estimates to reflect any changes in your circumstances or priorities. This will allow you to make informed decisions about your investment strategy and ensure that you maintain a sustainable income from your investments.

Estimating your annual expenses provides a fundamental basis for determining the amount of income you need to generate from your investment portfolio. By taking into account potential changes, inflation, and separating essential and discretionary expenses, you can create a realistic financial plan that supports your desired lifestyle and provides for your long-term financial security.

Understanding the 4% rule

The 4% rule is a widely accepted guideline used in retirement planning to determine how much you can safely withdraw from your investment portfolio each year without depleting your assets prematurely. It provides a framework for calculating the sustainable amount of income you can generate from your investments over the long term.

The rule states that in the first year of retirement, you can withdraw 4% of your investment portfolio’s value, adjusted for inflation in subsequent years. This withdrawal rate is designed to provide a steady income stream for at least 30 years. The 4% rule was initially proposed by financial planner William Bengen in a 1994 study.

The 4% rule is based on historical market data and assumes a diversified investment portfolio consisting of stocks, bonds, and other assets. It takes into account the average long-term returns of these assets and factors in inflation to ensure that your income keeps pace with rising costs.

By adhering to the 4% rule, you have a higher probability of not outliving your assets during retirement. It provides a reasonable withdrawal rate that balances the need for current income with the preservation of your investment portfolio’s value.

It’s important to note that the 4% rule serves as a general guideline and may not be suitable for everyone. Factors such as your risk tolerance, investment returns, and individual circumstances can influence the appropriateness of the rule for your specific situation.

It is advisable to work with a financial advisor to determine the withdrawal rate that best aligns with your goals and risk tolerance. They can help analyze your portfolio, assess your income needs, and provide personalized guidance for managing your investments during retirement or financial independence.

Regularly monitor your investment portfolio and adjust your withdrawal rate as necessary. Market conditions, changes in your financial situation, or unexpected expenses may require modifications to your withdrawal strategy. Through careful planning, ongoing evaluation, and flexibility, you can optimize the benefits of the 4% rule and maintain a sustainable income throughout your retirement years.

Calculating your investment portfolio needed

Calculating the size of the investment portfolio you need to live off can help you determine the financial goal you should strive for. This calculation takes into account your estimated annual expenses, the 4% rule, and the desired income stream you aim to generate.

Start with your annual expenses: Estimate your annual expenses by considering your current expenses, potential changes in retirement, and accounting for inflation. This will give you a baseline number to work with.

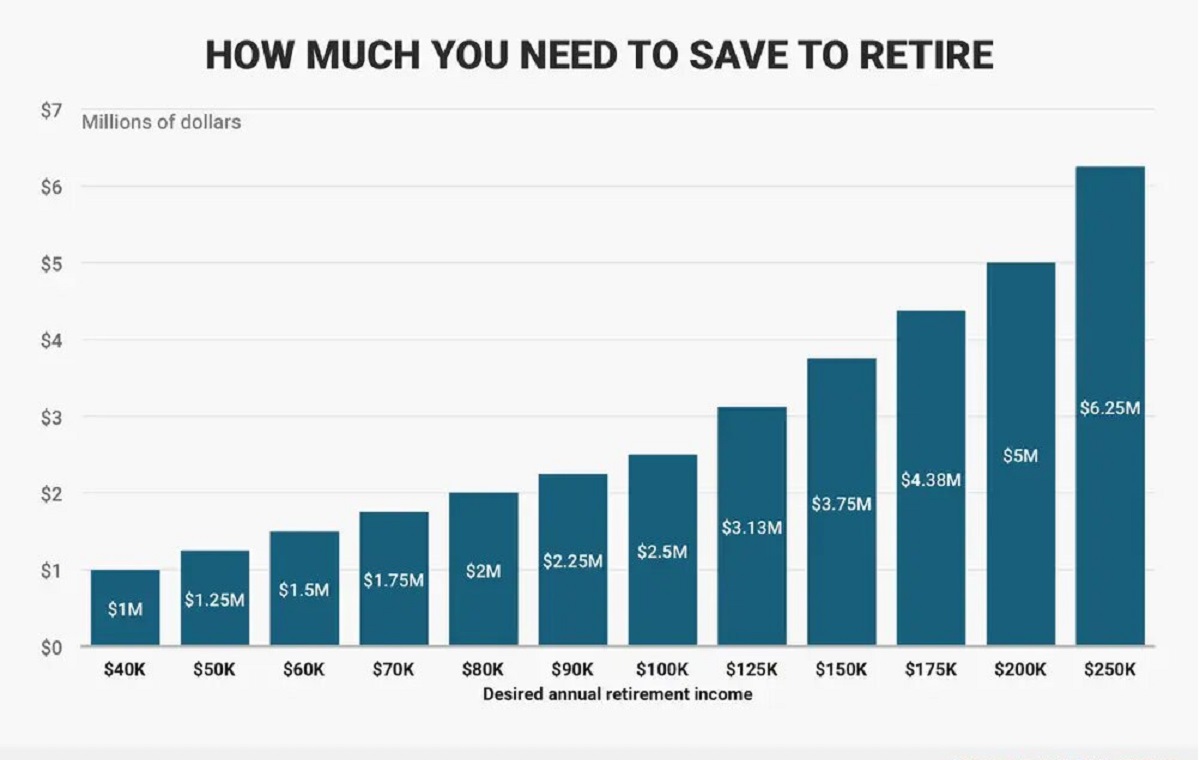

Apply the 4% rule: The 4% rule suggests that you can safely withdraw 4% of your investment portfolio’s value in the first year of retirement, adjusting that amount for inflation in subsequent years. To calculate the size of the investment portfolio needed, divide your annual expenses by 4%. For example, if you require $40,000 per year in retirement, you would need a portfolio of $1 million ($40,000 / 0.04 = $1,000,000).

Factor in additional income sources: Consider any additional income sources you may have, such as Social Security benefits or rental income. Subtract these income sources from your annual expenses to determine the amount you need to generate from your investment portfolio.

Consider your risk tolerance: Your risk tolerance plays a role in determining the size of your investment portfolio. A higher risk tolerance may allow for a higher withdrawal rate, whereas a lower risk tolerance may require a larger portfolio to generate the desired income stream.

Consult a financial advisor: It is recommended to consult with a financial advisor who can provide personalized guidance based on your individual circumstances and investment goals. They can assess various factors, such as your time horizon, risk tolerance, and investment strategies, to help you calculate the investment portfolio size needed to sustain your desired lifestyle.

Regularly evaluate and adjust: Keep in mind that your financial situation and goals may change over time. Periodically reassess your investment portfolio needs, taking into account factors such as market conditions, inflation, and evolving lifestyle preferences. Adjust your calculations and investment strategy as necessary to stay on track towards achieving your financial objectives.

Calculating the investment portfolio size needed to sustain your desired income stream is a vital step in financial planning. By understanding your annual expenses, applying the 4% rule, factoring in additional income sources, and considering your risk tolerance, you can establish a goal that aligns with your financial needs and aspirations.

Factors that can impact your investment needs

Several factors can impact your investment needs when determining how much you require to live off investments. These factors can influence the size of your investment portfolio and the income it needs to generate to sustain your desired lifestyle. It’s essential to consider these factors to ensure your financial plan remains adaptable and aligned with your goals.

1. Inflation: Inflation erodes the purchasing power of your money over time. As the cost of goods and services rises, your expenses will increase. It’s crucial to account for inflation when estimating your future income needs and ensure your investment returns outpace inflation to maintain your standard of living.

2. Market conditions: The performance of financial markets can have a significant impact on your investment needs. Fluctuations in the stock market, bond yields, and other investment vehicles can affect your portfolio’s value and potential returns. It’s important to factor in market conditions when determining how much you need to live off investments and adjust your investment strategy accordingly.

3. Longevity: Your life expectancy plays a crucial role in determining the duration for which your investment portfolio needs to sustain your income. The longer your life expectancy, the more income you will require to cover your expenses over a longer period. Consider your family history, health, and lifestyle factors when estimating your life expectancy.

4. Unforeseen expenses: Unexpected costs, such as medical emergencies or home repairs, can impact your investment needs. It’s important to have a contingency plan and set aside funds for these unforeseen expenses to prevent your investment portfolio from being depleted. Building an emergency fund can provide a safety net during challenging times.

5. Lifestyle changes: Changes in your desired lifestyle can also influence your investment needs. If you decide to pursue new hobbies, travel more frequently, or make significant lifestyle changes, you may need to adjust your income requirements. Be prepared to reassess and adapt your investment plan to accommodate these lifestyle changes.

6. Taxation: Taxation can have a significant impact on your investment needs as it reduces your overall income. Understanding the tax implications of your investment income can help you plan and optimize your tax efficiency. Consult with a tax advisor to explore strategies that can minimize your tax burden and maximize your after-tax income.

7. Changes in personal circumstances: Life events such as marriage, divorce, births, or the death of a loved one can impact your investment needs. These events may necessitate adjustments to your financial goals and income requirements. Stay attuned to changes in your personal circumstances and modify your investment strategy accordingly.

It’s important to regularly review and reassess these factors as part of your financial planning process. Periodically evaluate your investment needs, keeping in mind inflation, market conditions, longevity, unforeseen expenses, lifestyle changes, taxation, and changes in personal circumstances. By staying informed and proactive, you can ensure your investment strategy remains on track to meet your evolving needs and goals.

Managing your investment risks

When living off investments, it’s essential to manage and mitigate investment risks to protect your portfolio and sustain a reliable income stream. By implementing effective risk management strategies, you can minimize the impact of market fluctuations and unforeseen events on your investments.

1. Diversification: Diversifying your investment portfolio is one of the most fundamental risk management strategies. Spread your investments across different asset classes, industries, and geographic regions. This diversification can help reduce the impact of any single investment’s poor performance on your overall portfolio.

2. Asset allocation: Establish an appropriate asset allocation based on your risk tolerance and investment goals. Allocate your assets among stocks, bonds, cash, and other investment vehicles in a way that balances potential returns and risk. Rebalance your portfolio periodically to maintain your desired asset allocation.

3. Regular monitoring: Regularly monitor your investments and stay informed about market conditions. Stay abreast of economic trends, company news, and industry developments that could impact your investment holdings. This information will enable you to make informed decisions and take appropriate action when necessary.

4. Risk assessment: Assess your risk tolerance and understand your capacity for absorbing losses. This evaluation will help you determine the level of risk you can comfortably take on and guide your investment decisions. Consider working with a financial advisor to conduct a comprehensive risk assessment and develop a risk management plan.

5. Stay invested for the long term: Investing for the long term can help mitigate short-term market fluctuations. Avoid making impulsive investment decisions based on short-term market volatility. Instead, focus on the long-term growth potential of your investments and maintain a disciplined approach.

6. Emergency fund: Maintain an emergency fund to cover unexpected expenses or income gaps. This fund should be easily accessible and provide a buffer against financial uncertainties. It can help you avoid the need to withdraw from your investment portfolio at unfavorable times.

7. Regular financial reviews: Conduct regular reviews of your investment portfolio and financial goals. Assess whether your investments are generating the desired income and performing in line with your expectations. Make necessary adjustments to your investment strategy to align with changing market conditions and personal circumstances.

8. Seek professional advice: Consider working with a financial advisor who can provide professional guidance tailored to your specific needs. A financial advisor can help analyze your risk tolerance, develop a customized risk management plan, and provide ongoing support to navigate investment challenges.

By implementing effective risk management strategies, you can mitigate potential risks and secure your investment portfolio’s stability. Diversification, asset allocation, regular monitoring, risk assessment, maintaining an emergency fund, and seeking professional advice are key steps in managing investment risks. Remember that risk management is an ongoing process, and it requires ongoing vigilance and proactive decision-making to protect and grow your investments.

Monitoring and adjusting your investment strategy

Monitoring and adjusting your investment strategy is a crucial aspect of successfully living off investments. Regularly reviewing your portfolio, evaluating performance, and making necessary adjustments can help ensure that your investments continue to align with your financial goals and risk tolerance.

1. Regular portfolio reviews: Schedule periodic reviews of your investment portfolio. Assess the performance, allocation, and risk exposure of each investment. Identify any holdings that may no longer be suitable or are underperforming. Make informed decisions about whether to hold, sell, or adjust your investments based on their alignment with your long-term goals.

2. Evaluate your risk tolerance: Assess whether your risk tolerance has changed over time. Factors such as market conditions, personal circumstances, and time horizon can impact your ability to tolerate risk. Determine whether your current asset allocation is still appropriate, and make adjustments if necessary to ensure that your investment strategy remains aligned with your risk tolerance.

3. Stay informed: Stay updated on market trends, economic indicators, and investment news. This knowledge will enable you to make informed decisions and timely adjustments to your investment strategy when needed. Follow trusted sources, consult with professionals, and consider diversifying your information sources to get a well-rounded perspective.

4. Rebalance your portfolio: Rebalance your portfolio periodically to maintain your desired asset allocation. Over time, some investments may grow at a faster rate than others, leading to an imbalance in your portfolio. Rebalancing involves selling overperforming assets and buying underperforming ones to bring your allocation back in line with your targets.

5. Consider tax implications: Be aware of the tax implications of your investment decisions. Evaluate opportunities to minimize taxes on capital gains and dividends. Consult with a tax professional to explore strategies such as tax-efficient investing, tax loss harvesting, and utilizing tax-advantaged accounts to optimize your tax position.

6. Embrace a long-term perspective: Maintain a long-term perspective when evaluating your investments. Short-term market fluctuations are normal, and reacting impulsively to them can detract from your overall investment performance. Stick to your investment strategy and remain focused on your long-term financial goals.

7. Seek professional advice: Consider working with a financial advisor who can provide personalized guidance and support. A financial advisor can help you monitor your investments, evaluate their performance, and adjust your investment strategy based on your unique circumstances. They can also provide insights, expertise, and regular portfolio reviews to ensure you stay on track towards your financial objectives.

Monitoring and adjusting your investment strategy is an ongoing process. Regularly reviewing your portfolio, evaluating your risk tolerance, staying informed, rebalancing your holdings, considering tax implications, embracing a long-term perspective, and seeking professional advice are essential steps to ensure that your investment strategy remains optimal and in line with your financial goals.

Conclusion

Living off investments is a goal that offers financial independence and the freedom to live life on your own terms. It requires careful planning, evaluation of your financial needs, and the implementation of effective investment strategies. By considering factors such as your current expenses, desired lifestyle, annual expense estimates, the 4% rule, and investment risks, you can determine how much you need to live off investments.

Calculating the size of your investment portfolio needed and managing investment risks are essential steps in achieving your financial goals. Diversification, asset allocation, regular monitoring, and adjusting your investment strategy are key elements in maximizing the potential for long-term growth and sustaining a reliable income stream.

It’s important to regularly review and adjust your investment strategy as market conditions change and your personal circumstances evolve. Stay informed, evaluate performance, and seek professional advice when necessary to ensure that your investment portfolio remains aligned with your goals and risk tolerance.

Living off investments requires discipline, patience, and a long-term perspective. It’s a journey that requires ongoing monitoring and adjustments. By taking a proactive approach, staying informed, and making informed decisions, you can achieve financial independence and enjoy the lifestyle you aspire to.

Remember, living off investments is a personal and unique journey. It’s crucial to tailor your financial plan to your specific circumstances, goals, and risk tolerance. Consulting with a financial advisor can provide valuable insights and guidance to help you navigate the complexities of investment planning and ensure your roadmap to financial freedom is well-defined.