What are Annuities Investments?

Annuities are a type of financial product that can provide a steady stream of income over a predetermined period of time. They are commonly used as a long-term investment strategy to ensure a regular cash flow during retirement. Annuity investments are essentially contracts between an individual and an insurance company, where the individual makes regular payments into the annuity in exchange for specified benefits in the future.

One of the primary advantages of annuities is their ability to provide a reliable and predictable income stream. The money invested in an annuity grows tax-deferred until withdrawals are made, making it an attractive option for individuals looking to supplement their retirement income or secure a guaranteed source of funds.

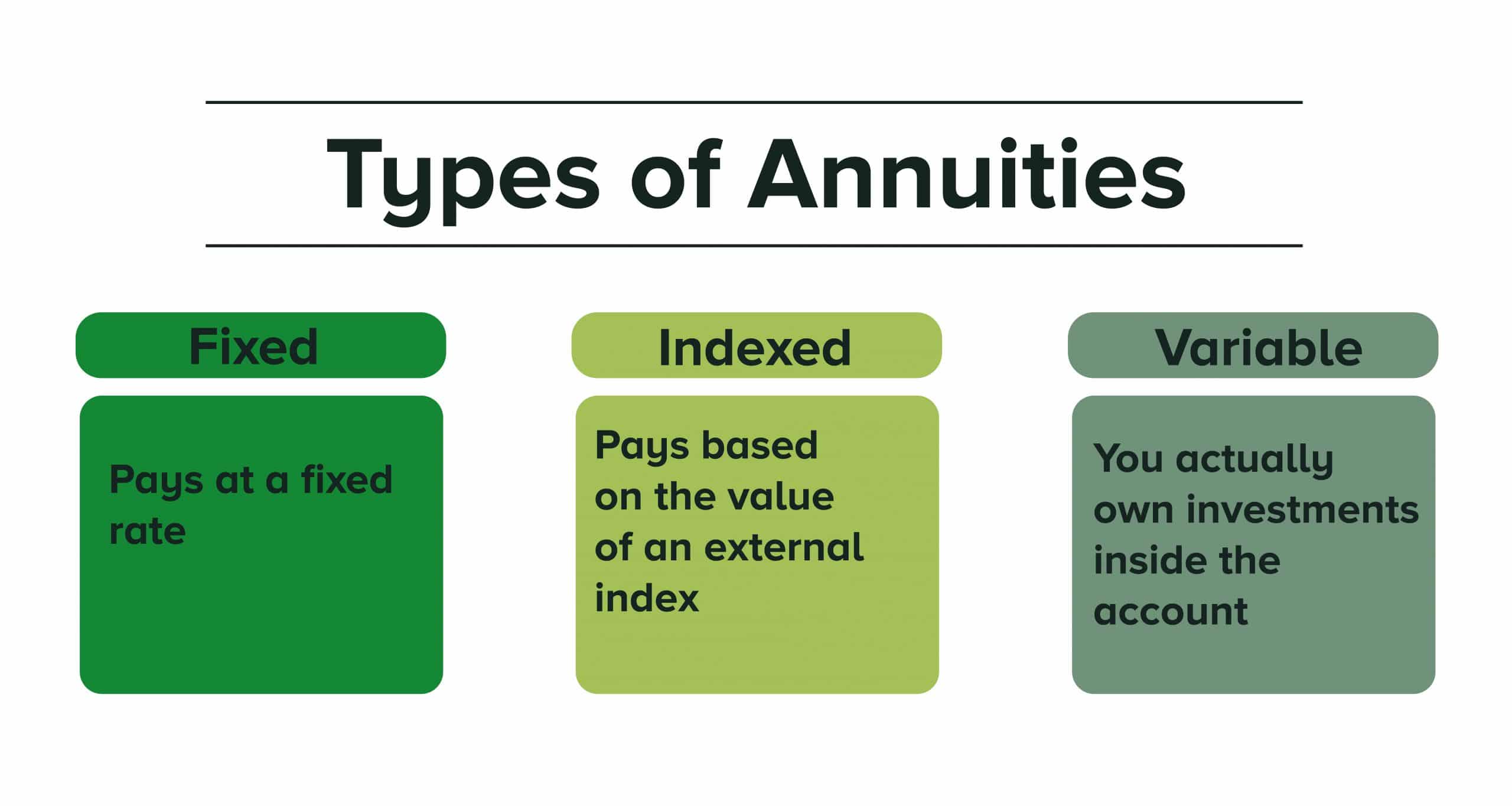

There are different types of annuities, each with its own features and benefits. Fixed annuities offer a guaranteed interest rate for a set period of time, providing stability and security. Variable annuities, on the other hand, allow individuals to invest in a variety of options, such as stocks and bonds, with the potential for higher returns but also greater risk. Indexed annuities combine elements of both fixed and variable annuities, offering a minimum guaranteed return along with potential interest based on the performance of a specific market index.

While annuities can be a valuable investment tool, it is important to carefully consider the costs and fees associated with them. These can include surrender charges, administrative fees, investment management fees, and mortality and expense charges. Understanding these costs is crucial in determining the overall value and potential returns of your annuity investment.

Before investing in an annuity, it is essential to consider your individual financial goals, risk tolerance, and time horizon. Annuities are designed for long-term investors and may not be suitable for everyone. It is recommended to consult with a financial advisor who can assess your specific needs and guide you in making informed investment decisions.

In summary, annuities are a type of investment that can provide a reliable source of income during retirement. They offer various options such as fixed, variable, and indexed annuities, each with its own benefits and considerations. Understanding the costs and fees associated with annuities is crucial, and it is important to carefully evaluate your financial goals before making an investment decision.

How do Annuities Work?

Annuities work by providing a structured payment plan in exchange for an initial investment. When you purchase an annuity, you enter into a contract with an insurance company. The insurance company then agrees to make regular payments to you, either immediately or at a future date, based on the terms of the annuity.

There are two main phases of an annuity: the accumulation phase and the distribution phase. During the accumulation phase, you make contributions to the annuity, either in a lump sum or through periodic payments. These contributions, along with any interest or growth, accumulate over time. The accumulation phase is often used to build up the value of the annuity, allowing for potential growth and compounding.

Once the accumulation phase is complete, the annuity enters the distribution phase. This is when the insurance company begins to make regular payments to you, based on the terms agreed upon in the contract. The payments can be made for a specific period of time, such as 10 or 20 years, or for the remainder of your life.

There are different types of annuities that determine how the payments are calculated. In a fixed annuity, the payments are predetermined and do not change over time. This provides stability and predictability, as you know exactly how much you will receive each payment period. In a variable annuity, the payments are based on the performance of the underlying investments, such as stocks or bonds. This means that the payments may fluctuate based on market conditions and the performance of those investments.

It is important to note that annuities are subject to taxes. The growth of the annuity during the accumulation phase is typically tax-deferred, meaning you do not pay taxes on it until you start receiving distributions. However, once you start receiving payments, those payments are considered taxable income.

Understanding how annuities work is essential in order to make informed decisions about whether they are the right investment strategy for you. Before purchasing an annuity, it is recommended to consult with a financial advisor who can assess your individual financial goals and help determine if an annuity aligns with your needs and risk tolerance.

In summary, annuities work by providing a structured payment plan in exchange for an initial investment. The accumulation phase allows your investment to grow over time, while the distribution phase provides regular payments based on the terms of the annuity contract. Different types of annuities offer varying levels of stability and potential growth. Understanding the tax implications and consulting with a financial advisor are crucial steps in navigating the world of annuities.

Types of Annuities

There are several types of annuities available, each offering different features and benefits to investors. Understanding the different types can help you choose the annuity that aligns with your financial goals and risk tolerance. Here are the most common types of annuities:

- Fixed Annuities: Fixed annuities provide a stable and predictable income stream. With a fixed annuity, the insurance company guarantees a specific interest rate for a predetermined period of time. This means that your payments will remain the same, regardless of any fluctuations in the market. Fixed annuities offer a low-risk investment option, making them suitable for individuals who prioritize safety and security.

- Variable Annuities: Variable annuities allow investors to allocate their annuity funds into various investment options, such as stocks, bonds, and mutual funds. The returns of a variable annuity are dependent on the performance of the underlying investments. This means that while variable annuities offer greater growth potential, they also come with increased market risk. Variable annuities are suitable for investors who are comfortable with market fluctuations and are looking for potential higher returns.

- Indexed Annuities: Indexed annuities combine features of both fixed and variable annuities. They offer a minimum guaranteed interest rate along with the potential to earn additional interest based on the performance of a specific market index, such as the S&P 500. Indexed annuities provide a balance between the safety of a fixed annuity and the growth potential of a variable annuity. They are ideal for investors who seek both stability and the opportunity for higher returns.

- Immediate Annuities: Immediate annuities begin making regular payments to the investor immediately after the initial investment. This type of annuity is often used by individuals who are already in retirement and want a reliable source of income. Immediate annuities provide a steady stream of payments for a specified period of time or for the remainder of the investor’s life.

- Deferred Annuities: Deferred annuities provide investors with the option to accumulate funds during the accumulation phase before starting to receive payments. These annuities allow individuals to save for retirement over a longer period of time. Deferred annuities are suitable for individuals who want to build up their annuity over time and delay receiving payments until a future date.

It is important to carefully consider the features and benefits of each type of annuity and how they align with your financial goals. Consulting with a financial advisor can help you navigate the options and make an informed decision that suits your individual needs.

In summary, there are several types of annuities, each with its own features and considerations. Fixed annuities offer stability, while variable annuities provide potential growth. Indexed annuities combine elements of both fixed and variable annuities. Immediate annuities start making payments immediately, while deferred annuities allow for accumulation before distributions begin. Understanding the different types of annuities can help you make the right choice for your financial future.

Pros and Cons of Annuity Investments

Annuity investments have their advantages and disadvantages, which are important to consider before making any investment decisions. Here are the pros and cons of annuity investments:

Pros of Annuity Investments:

- Guaranteed Income: Annuities can provide a guaranteed income stream, giving individuals peace of mind during retirement.

- Tax-Deferred Growth: The growth of an annuity is tax-deferred, allowing the investment to compound over time without being subject to immediate taxes.

- Protection from Market Volatility: Fixed and indexed annuities offer protection from market downturns, providing a reliable income source regardless of market fluctuations.

- Customizable Options: Annuities offer flexibility in terms of payment options, allowing individuals to choose between immediate or deferred payments, as well as the duration and frequency of payments.

- Death Benefit: Some annuities provide a death benefit, ensuring that the remaining value of the annuity is passed along to beneficiaries after the investor’s death.

Cons of Annuity Investments:

- High Costs and Fees: Annuities often come with high fees and expenses, including administrative fees, investment management fees, and surrender charges.

- Lack of Liquidity: Annuities are typically long-term investments with limited liquidity. Withdrawing funds before the agreed-upon terms can result in penalties and fees.

- Loss of Control: Once the initial investment is made, annuity investors have limited control over how their money is invested. This can be a disadvantage for individuals who prefer to have more control over their investment decisions.

- Complexity: Annuities can be complex financial products, with various types, options, and features. Understanding the terms and conditions of the annuity contract requires careful consideration and possibly the assistance of a financial advisor.

- Inflation Risk: While fixed annuities provide stability, they may not keep pace with inflation, resulting in a decrease in purchasing power over time.

It is important to weigh the pros and cons of annuity investments based on your individual financial goals, risk tolerance, and investment preferences. Consulting with a financial advisor can help you evaluate whether annuities are the right fit for your overall financial plan.

In summary, annuities offer guaranteed income, tax advantages, and protection from market volatility. However, they can come with high costs, lack of liquidity, and loss of control. Understanding the pros and cons of annuity investments is essential in making educated investment decisions that align with your financial objectives.

Understanding the Costs and Fees Associated with Annuities

When considering annuity investments, it is crucial to understand the costs and fees associated with these financial products. Annuities typically come with various fees that can affect the overall value and potential returns of your investment. Here are some key costs and fees to consider:

Surrender Charges:

Surrender charges are fees imposed by insurance companies if you withdraw funds from an annuity before a specified time period, often referred to as the surrender period. These charges are designed to discourage early withdrawals and can be a percentage of the amount withdrawn or a declining charge over time. It is important to be aware of the surrender period and understand the potential impact of these fees on your investment.

Administrative Fees:

Administrative fees cover the costs associated with maintaining and administering your annuity account. These fees can vary depending on the insurance company and the specific annuity product. It is important to review the fee structure and determine whether the benefits of the annuity outweigh the administrative costs.

Investment Management Fees:

For variable annuities, investment management fees are charged to cover the costs of managing the underlying investments, such as mutual funds. These fees are typically a percentage of the assets invested and can vary depending on the investment options chosen. It is essential to understand the investment management fees associated with your annuity and assess whether they are reasonable in relation to the potential returns.

Mortality and Expense Charges:

Mortality and expense (M&E) charges are fees that insurance companies charge for the death benefit protection and insurance risk they assume when providing annuities. These charges cover the costs associated with maintaining the annuity and providing the promised benefits. M&E charges are typically a percentage of the account value or a flat fee deducted annually. It is important to evaluate the M&E charges and consider if the benefits provided outweigh the costs incurred.

Add-On Optional Benefits:

In some cases, annuities offer optional benefits that come at an additional cost. These add-on benefits may include features like guaranteed minimum income benefit, principal protection, or long-term care coverage. While these benefits can provide added security and flexibility, they usually come with extra fees. It is essential to carefully evaluate the costs and benefits of these add-ons to determine if they align with your specific needs and financial goals.

Understanding the costs and fees associated with annuities is crucial in evaluating the overall value and potential returns of your investment. It is recommended to thoroughly review the annuity contract, including the prospectus and disclosure documents, to gain a clear understanding of the fees involved. Consulting with a financial advisor who specializes in annuities can also provide valuable insights and help you make informed investment decisions.

In summary, annuity investments come with various costs and fees, including surrender charges, administrative fees, investment management fees, and mortality and expense charges. Optional benefits may also have additional costs. Having a clear understanding of these costs is essential in assessing the overall value and potential returns of your annuity investment.

Benefits of Annuity Investments

Annuity investments offer several benefits that can make them an attractive option for individuals looking to secure their financial future. Here are some key benefits of investing in annuities:

Guaranteed Income:

One of the primary benefits of annuity investments is the ability to provide a guaranteed income stream. This can be particularly beneficial for retirees who want a reliable source of income during their retirement years. Annuities ensure that you receive regular payments, either for a specific period of time or for the remainder of your life, providing financial stability and peace of mind.

Tax-Deferred Growth:

Annuities offer tax-deferred growth, meaning that the earnings on your investment are not subject to immediate taxes. This provides an advantage by allowing your investment to grow and compound over time without the burden of annual taxes. Taxes are only paid when withdrawals are made, typically during the distribution phase. Tax deferral can be especially beneficial for individuals in higher tax brackets or those looking to maximize the growth of their investment.

Diversification and Investment Options:

Depending on the type of annuity, investors have the opportunity to diversify their investments and choose from a range of options. Variable annuities, for example, allow individuals to invest in a variety of underlying options such as stocks, bonds, and mutual funds. This diversification can help spread risk and potentially enhance returns, allowing for a customized investment strategy tailored to your risk tolerance and financial goals.

Protection from Market Volatility:

Fixed and indexed annuities provide protection from market volatility, allowing investors to safeguard their principal investment. Fixed annuities offer a guaranteed interest rate, ensuring a stable and predictable income stream regardless of market fluctuations. Indexed annuities, on the other hand, provide a minimum guaranteed return along with the potential for additional interest based on the performance of a specific market index. This protection can provide peace of mind and a sense of security, particularly during uncertain economic times.

Potential Death Benefit:

Some annuities offer a death benefit, which can be an attractive feature for individuals concerned about leaving a financial legacy for their loved ones. In the event of the annuity owner’s death, any remaining value in the annuity can be passed on to the designated beneficiaries. This can provide support for beneficiaries and help ensure that your assets are distributed according to your wishes.

It is important to note that the benefits of annuity investments can vary depending on the specific type of annuity and the terms of the contract. It is recommended to carefully evaluate the features and benefits of different annuity options and consult with a financial advisor who can provide personalized guidance based on your unique financial situation and goals.

In summary, annuity investments offer benefits such as guaranteed income, tax-deferred growth, diversification opportunities, protection from market volatility, and the potential for a death benefit for beneficiaries. Understanding these benefits can help individuals make informed investment decisions and secure their financial future.

Risks and Considerations of Annuities

While annuities offer several benefits, it is important to be aware of the risks and considerations associated with these financial products. Understanding the potential drawbacks can help you make informed decisions and assess whether annuities align with your financial goals. Here are some key risks and considerations to keep in mind:

High Costs and Fees:

Annuities often come with high costs and fees, including surrender charges, administrative fees, investment management fees, and mortality and expense charges. These fees can eat into your returns and reduce the overall value of your investment. It is crucial to carefully review the fee structure and assess whether the benefits of the annuity outweigh the costs incurred.

Lack of Liquidity:

Annuities are typically long-term investments with limited liquidity. Withdrawing funds before the agreed-upon terms can result in surrender charges and penalties. This lack of liquidity can be a disadvantage for individuals who may require access to their funds for unexpected expenses or other financial needs. It is important to consider your financial situation and ensure that you have sufficient emergency savings before committing to an annuity.

Loss of Control:

Once you invest in an annuity, you have limited control over how your money is invested. The insurance company makes the investment decisions and manages the underlying investments. This lack of control may not appeal to individuals who prefer to have more autonomy in their investment choices. It is important to evaluate your investment style and determine whether you are comfortable relinquishing control over your investment decisions.

Complexity:

Annuities can be complex financial products with various types, options, and features. Understanding the terms and conditions of the annuity contract may require careful consideration and possibly the assistance of a financial advisor. It is crucial to thoroughly review the annuity contract, including the prospectus and disclosure documents, to gain a clear understanding of the product before making an investment.

Inflation Risk:

While fixed annuities provide stability, they may not keep pace with inflation. This means that over time, the purchasing power of your annuity income may decrease. It is important to consider the potential impact of inflation on your income and explore strategies to mitigate this risk, such as investing in assets that have the potential to outpace inflation.

Before investing in an annuity, it is recommended to evaluate your financial goals, risk tolerance, and investment preferences. An annuity may not be suitable for everyone, and it is important to consider alternatives based on your individual circumstances. Consulting with a financial advisor can provide valuable insights and help you understand the risks and considerations associated with annuities.

In summary, annuities come with risks such as high costs and fees, lack of liquidity, loss of control over investments, complexity, and inflation risk. Understanding these risks and considerations is crucial in making informed decisions and determining whether annuities align with your financial objectives.

Factors to Consider Before Investing in Annuities

Before making the decision to invest in annuities, it is important to carefully consider several factors to ensure they align with your financial goals and circumstances. Annuities can be a valuable investment tool for some individuals, but they may not be suitable for everyone. Here are some key factors to consider before investing in annuities:

Financial Goals and Time Horizon:

Consider your financial goals and the time horizon for your investment. Annuities are typically long-term investments and may not be suitable if you have short-term financial objectives or need immediate access to your funds. Evaluate whether the timeline of an annuity aligns with your goals and if you have other assets or savings to meet your short-term financial needs.

Risk Tolerance:

Assess your risk tolerance and investment preferences. Different types of annuities come with varying levels of risk and return potential. Fixed annuities offer stability and guaranteed income but may not provide as much growth as variable annuities. Consider how comfortable you are with market fluctuations and the potential impact on your investment.

Liquidity Needs:

Evaluate whether you have any near-term liquidity needs. Annuities have limited liquidity, and withdrawing funds before the agreed-upon terms can result in penalties and surrender charges. Ensure that you have sufficient emergency savings and access to funds for unexpected expenses before committing to an annuity.

Inflation Protection:

Consider the potential impact of inflation on your annuity income. Fixed annuities may not keep pace with inflation, which could impact your purchasing power over time. If inflation protection is a concern for you, explore other investment options or strategies to mitigate this risk.

Costs and Fees:

Understand the costs and fees associated with annuities. Different annuities come with different fee structures, including administrative fees, investment management fees, and surrender charges. Review the fee disclosures and assess whether the benefits of the annuity outweigh the costs incurred.

Tax Implications:

Evaluate the tax implications of annuities. While annuities offer tax-deferred growth, meaning you do not pay taxes on the investment gains until withdrawals are made, withdrawals are generally subject to ordinary income tax rates. Consult with a tax advisor to understand how annuities will impact your tax situation and if they align with your overall tax strategy.

Professional Guidance:

Consider seeking professional guidance from a financial advisor who specializes in annuities. An advisor can help assess your individual financial situation, goals, and risk tolerance, and provide personalized recommendations based on your needs. They can also explain the complexities of annuities and help you navigate through the various options available.

By carefully considering these factors, you can make an informed decision about whether investing in annuities is the right choice for you. It is important to evaluate annuities within the broader context of your overall financial plan and explore other investment options that align with your unique circumstances.

In summary, factors to consider before investing in annuities include financial goals and time horizon, risk tolerance, liquidity needs, inflation protection, costs and fees, tax implications, and seeking professional guidance. Evaluating these factors will help you determine whether annuities are a suitable investment option for your financial future.

Frequently Asked Questions about Annuity Investments

Here are answers to some commonly asked questions about annuity investments:

1. What are the main types of annuities?

The main types of annuities include fixed annuities, variable annuities, and indexed annuities. Fixed annuities offer a guaranteed interest rate, variable annuities allow for investment in underlying assets, and indexed annuities provide a minimum guaranteed return along with potential interest based on the performance of a market index.

2. How do annuities differ from other retirement accounts?

Annuities differ from other retirement accounts, such as IRAs and 401(k)s, in their structure and payout method. While both annuities and retirement accounts can provide income during retirement, annuities are insurance products that offer a guaranteed income stream, whereas retirement accounts typically rely on contributions and investment returns to provide income.

3. Are annuities a good investment for everyone?

Annuities may be a suitable investment for certain individuals, especially those looking for a guaranteed income stream and tax-deferred growth. However, annuities may not be suitable for everyone, particularly those with low risk tolerance, short-term financial goals, or a need for liquidity. It is important to carefully evaluate your individual circumstances and consult with a financial advisor before investing in annuities.

4. Can I surrender or withdraw funds from an annuity before the agreed-upon terms?

Yes, you can surrender or withdraw funds from an annuity before the agreed-upon terms, but it may result in surrender charges or penalties. These charges are designed to discourage early withdrawals and can vary depending on the terms of your annuity contract and the length of the surrender period. It is important to carefully review the terms and potential penalties before making any withdrawals.

5. Do annuities provide any death benefits?

Some annuities do provide death benefits. In the event of the annuity owner’s death, any remaining value in the annuity can be passed on to the designated beneficiaries. The beneficiaries can receive the remaining funds either as a lump sum or as periodic payments, depending on the terms of the annuity contract.

6. Are annuity payments taxable?

Yes, annuity payments are generally taxable as ordinary income. However, the growth of the annuity during the accumulation phase is tax-deferred. This means that taxes are only paid when withdrawals or distributions are made from the annuity.

7. Can I make changes to my annuity once it is set up?

The ability to make changes to an annuity after it is set up depends on the specific terms of the annuity contract. Some annuities offer flexibility in terms of additional investments or modifications to the payout options, while others may have limited options for changes. It is important to review the annuity contract or consult with your financial advisor to understand the options available to you.

These are general answers to frequently asked questions about annuity investments. It is important to note that the specific details and terms can vary depending on the annuity product and insurance company. To get personalized and accurate information, it is recommended to consult with a financial advisor or insurance professional who can provide guidance based on your individual needs and circumstances.

Conclusion

Investing in annuities can be a valuable strategy for individuals looking to secure a steady income during retirement and enjoy potential tax advantages. Annuities offer benefits such as guaranteed income, tax-deferred growth, and protection from market volatility.

However, it is important to carefully consider the risks and considerations associated with annuities. These include high costs and fees, limited liquidity, potential loss of control, complexity, and inflation risk. Evaluating these factors and understanding the terms of the annuity contract is crucial in making informed investment decisions.

Before investing in annuities, take the time to assess your financial goals, risk tolerance, and investment preferences. Evaluate whether annuities align with your long-term objectives and consider alternatives that may better suit your needs.

Seeking professional guidance from a financial advisor experienced in annuities can provide valuable insights and help you navigate through the complexities of these financial products. An advisor can assess your unique financial situation, explain the various annuity options, and assist you in making investment decisions that align with your goals.

Remember that annuities are long-term commitments, and it is important to review the terms and conditions of the annuity contract carefully. Be sure to understand the fees, surrender charges, investment options, and potential tax implications before making your investment.

By considering these factors and seeking professional advice, you can make educated decisions regarding annuity investments that contribute to your overall financial well-being and help secure your financial future.