Introduction

Annuities are financial products that offer a source of income in retirement, but they are often regarded as a less favorable investment option. While annuities may have their benefits, there are several reasons why they can be considered bad investments. In this article, we will explore the drawbacks that make annuities a less favorable choice for many investors.

Lack of liquidity is one of the key disadvantages of annuities. When you purchase an annuity, you typically commit your funds for a specific period of time. This means that if you unexpectedly need a large sum of money or want to invest in a different opportunity, accessing your funds from an annuity can be challenging and may come with penalties and fees. This lack of liquidity can limit your financial flexibility and hinder your ability to respond to changing financial needs.

Another issue with annuities is the high fees associated with these investments. Annuities often come with hefty commission charges, management fees, and surrender charges if you choose to withdraw your funds early. These fees can significantly reduce your investment returns and eat into your potential gains over the long term.

In addition to high fees, annuities generally have limited growth potential compared to other investment options. While they provide a guaranteed income stream, the returns on annuities are typically lower than those from other investment vehicles such as stocks or real estate. This can result in a lower growth rate of your capital over time.

The complexity of annuities can also make them unappealing to many investors. With different types of annuities available, each with its own unique features and terms, understanding the intricacies can be a daunting task. The complexity can make it difficult to compare different annuity products and determine which one best suits your financial goals and risk tolerance.

Lack of Liquidity

One major drawback of annuities is the lack of liquidity they offer. When you invest in an annuity, you commit your funds for a specific period, often years or decades. During this time, accessing your money can be challenging and may come with penalties and fees.

Unlike other investments, such as stocks or bonds, which can easily be sold on the open market, annuities have restrictions on when and how you can access your funds. Early withdrawals from annuities are typically subject to surrender charges, which can be as high as 10% of the withdrawal amount. This can significantly diminish the value of your investment and eat into your potential returns.

The lack of liquidity in annuities can limit your financial flexibility and hinder your ability to respond to unexpected expenses or investment opportunities. If you find yourself in a situation where you need a large sum of money, such as for a medical emergency or a down payment on a property, accessing the funds from your annuity can be challenging and time-consuming.

Furthermore, annuities often have limitations on the frequency and amount of withdrawals you can make. Some annuities may only allow you to withdraw a certain percentage of your account value annually, while others may have restrictions on the timing of withdrawals. This can prevent you from accessing your funds when you need them the most.

Additionally, annuities are not easily transferable or sellable. If you decide that an annuity no longer meets your financial needs, you may have limited options to exit the investment. Selling an annuity on the secondary market can be complex and may result in a lower value than the original investment, due to surrender charges and other fees.

Overall, the lack of liquidity in annuities can be a significant drawback for many investors. It restricts their ability to access their funds when needed and can impose penalties and fees for early withdrawals. Before investing in an annuity, it is crucial to consider your future financial needs and ensure that you have enough accessible funds for emergencies or other unforeseen circumstances.

High Fees

Another significant drawback of annuities is the high fees associated with these investments. When you purchase an annuity, you not only invest your money but also pay for various expenses and charges that can significantly impact your overall returns.

One common fee associated with annuities is the commission charged by insurance agents who sell these products. These commissions can be as high as 10% of the initial investment, resulting in a substantial reduction in your overall investment amount right from the start. These front-end sales charges can eat into your potential gains and take a significant portion of your investment before it has the chance to grow.

In addition to the upfront commission, annuities also have ongoing management fees. These fees are typically charged as a percentage of the account value and can range from 0.5% to 2% or more annually. While these percentages may seem small, they can add up over time and reduce your investment’s growth potential.

Early withdrawals from annuities are often subject to surrender charges. These charges are imposed by the insurance company if you withdraw your funds before a specified period, typically known as the surrender period. The surrender charges can be as high as 10% or more and can significantly impact the amount of money you receive if you need to access your funds before the predetermined period.

Furthermore, annuities may also have additional fees, such as administrative fees, rider fees, and mortality and expense charges. These fees can vary depending on the specific annuity contract, but they all contribute to reducing your investment returns.

When considering the high fees associated with annuities, it is essential to evaluate whether the potential benefits outweigh the costs. While annuities may provide guaranteed income in retirement, the fees can eat into your returns and limit the growth potential of your investment. It is crucial to carefully read and understand the fee structure of any annuity contract before making a significant financial commitment.

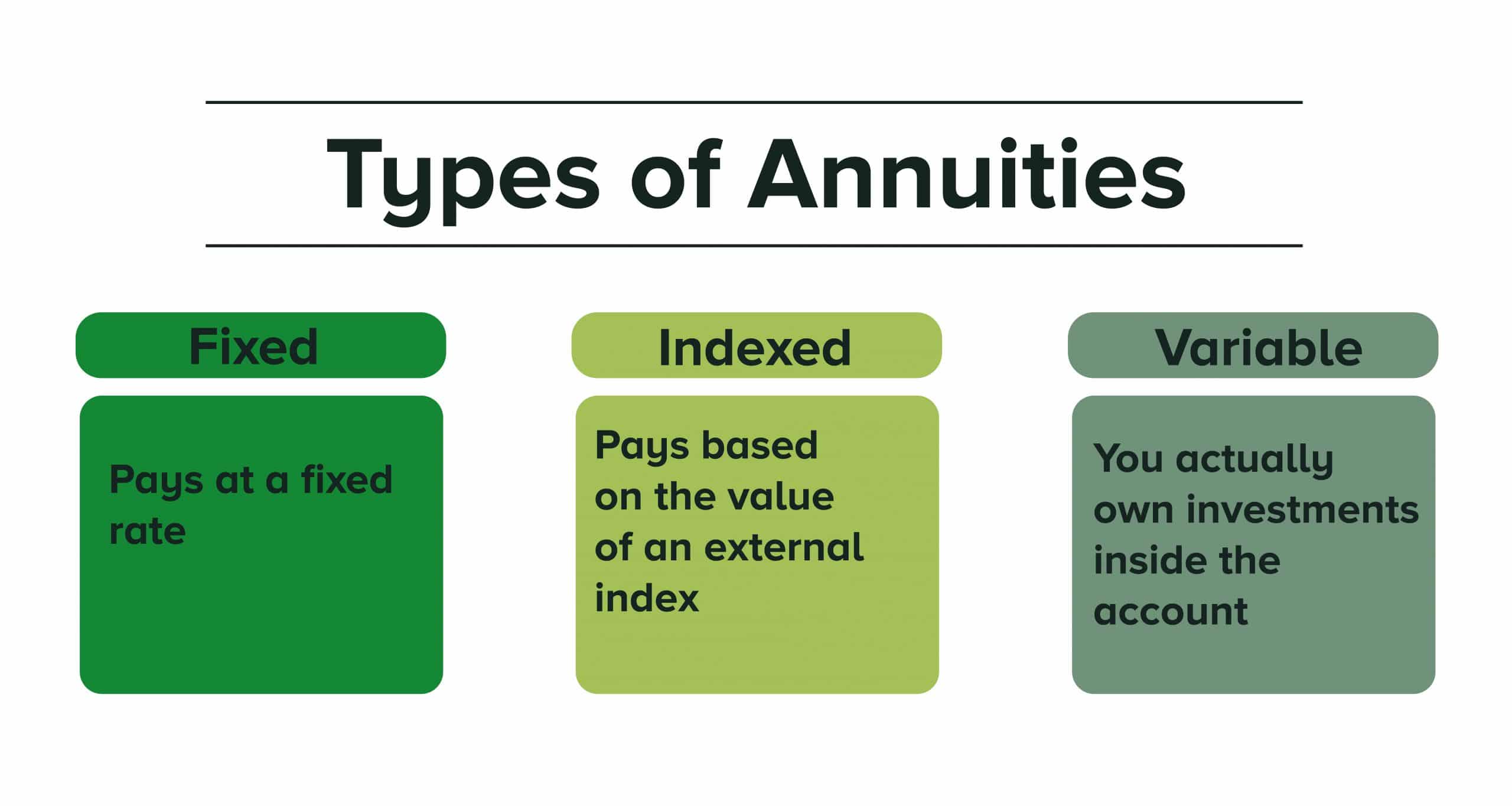

Limited Growth Potential

While annuities provide a guaranteed income stream, they often have limited growth potential compared to other investment options. The growth of an annuity is dependent on the interest rates and the performance of the underlying investments chosen by the insurance company.

One factor that affects the growth potential of annuities is the lower rate of return compared to other investment vehicles such as stocks or real estate. Annuities are generally designed to provide a steady stream of income rather than maximize capital growth. As a result, the returns on annuities tend to be lower compared to investments that have higher market volatility.

Unlike stocks or real estate, where you have the opportunity to benefit from market appreciation and capital gains, annuities typically offer a fixed rate of return. This fixed rate may be influenced by prevailing interest rates but is often lower to account for the guarantee of income. While the stability of a fixed return can be attractive to conservative investors, it may not provide the same level of growth potential as other investment vehicles over the long term.

Additionally, annuities have limitations on the potential growth of your investment due to fees and charges. As discussed earlier, annuities come with various fees, including management fees, commissions, and surrender charges. These fees can significantly reduce the overall growth of your annuity, eating into potential returns and diminishing the value of your investment over time.

It is important to carefully weigh the potential growth of an annuity against your financial goals and risk tolerance. While annuities provide a guaranteed income stream, they may not offer the same level of growth potential as other investments. If capital growth is a primary objective, it may be worth considering alternative investment options that have the potential for higher returns, albeit with higher levels of market risk.

Ultimately, the limited growth potential of annuities is an important factor to consider when weighing the pros and cons of these investment products. It is crucial to align your investment strategy with your financial goals and carefully evaluate the potential returns before committing to an annuity.

Complexity

One criticism often leveled against annuities is their inherent complexity. Annuities come in different types, each with its own unique features, terms, and conditions. Navigating through the complexities of annuities can be a daunting task, particularly for individuals who are not well-versed in financial jargon or experienced in investment management.

Understanding the intricacies of annuities requires careful examination of the contract details, including the payout structure, fees, surrender charges, and potential penalties. Annuities can differ in terms of payout options, such as whether the income is fixed or variable, and if there are any guarantees of minimum income or death benefits.

Furthermore, annuities often have complex provisions regarding withdrawals, annuitization, beneficiaries, and the impact of market fluctuations on income. It can be challenging to fully grasp how these provisions work, making it difficult to make informed decisions about when and how to access your funds or whether to continue with the annuity contract.

Additionally, comparing different annuity products can be a perplexing task. Each annuity provider offers their own set of features, rates, and fees. This makes it crucial to carefully review and analyze the details of each annuity contract, as well as seek professional advice to ensure full understanding before making any commitments.

The complexity of annuities can also be a barrier to evaluating their performance and determining their suitability for individual investors. Unlike stocks or mutual funds, which have easily accessible market data and performance metrics, annuities lack a transparent and standardized method of evaluation. This lack of transparency makes it challenging for investors to assess the relative value, costs, and potential risks associated with annuity investments.

Before investing in annuities, it is important to fully comprehend the complexity involved. Consider consulting with a financial advisor who specializes in annuities to ensure that you have a clear understanding of the terms and conditions. By doing so, you can make informed decisions and align your investment strategy with your financial goals while mitigating potential risks and uncertainties associated with the complex nature of annuities.

Tax Consequences

When considering annuities as an investment option, it is vital to understand the potential tax consequences associated with these financial products. While annuities offer tax-deferred growth, meaning you won’t pay taxes on the earnings until you withdraw funds, there are specific tax considerations to keep in mind.

If you withdraw money from an annuity before the age of 59½, you may be subject to an additional 10% early withdrawal penalty imposed by the IRS. This penalty is applied on top of the regular income taxes you are required to pay on the withdrawn amount. This early withdrawal penalty can significantly reduce your overall investment returns and erode the tax advantages of annuities.

When you start receiving income from an annuity, it is essential to understand how those payments are taxed. The income you receive from an annuity is generally treated as ordinary income, subject to your marginal tax rate. This can potentially lead to higher tax obligations if you are in a higher tax bracket during retirement.

Another important tax consideration is the tax treatment of your beneficiaries after your passing. Inherited annuities may trigger taxable events for your heirs. Depending on the circumstances, your beneficiaries may be required to pay income taxes on the distributions they receive from the annuity. It is crucial to consult with a tax professional to understand the implications for your specific situation.

Furthermore, annuities do not receive the same favorable tax treatment as other investment options, such as stocks or mutual funds, when it comes to capital gains. The appreciation in the value of your annuity is not subject to the lower capital gains tax rates. Instead, the gains are taxed as ordinary income when withdrawn, which could be a disadvantage if you were to compare the tax treatment with other investment strategies.

It is important to consult with a tax advisor or financial professional to fully understand the tax consequences of investing in annuities. By doing so, you can ensure that you are making informed decisions aligned with your overall tax strategy and financial goals.

Inflexibility in Payouts

One significant drawback of annuities is the inflexibility in payout options. Unlike other investments that provide more flexibility in accessing your funds, annuities often have restrictions on how and when you can receive your payments.

When you purchase an annuity, you typically choose a payout option. The most common options include receiving fixed payments for a specific period (known as a period certain), receiving payments for as long as you live (lifetime annuity), or a combination of both. Once you choose a payout option, it is difficult to change or modify it later.

This lack of flexibility can be problematic if your financial situation or needs change over time. For example, if you initially select a fixed period certain payout and later find yourself in need of a lump sum of money, it may be challenging to access the additional funds from your annuity.

In addition to inflexible payout options, annuities typically do not allow for partial withdrawals. Once your annuity is set up, you cannot choose to withdraw a portion of your funds while leaving the rest invested. Instead, you are committed to receiving steady payments based on the selected payout option.

Furthermore, if you choose a lifetime annuity, you may lose control over the principal amount you invested. While the income payments are guaranteed for life, the remaining balance of the annuity typically does not pass on to your beneficiaries upon your death. This lack of control and flexibility in terms of passing on the remaining funds can be a disadvantage for individuals who wish to leave an inheritance to their loved ones.

It is essential to carefully consider your financial needs and goals before committing to an annuity. While the guaranteed income stream may offer a sense of security, the inflexibility in payout options can limit your ability to adapt to changing circumstances.

Before investing in an annuity, explore other investment options that offer greater flexibility, such as taxable investment accounts or Roth IRAs, which allow for more control over your funds and provide more flexibility to adjust withdrawal amounts and timing as needed.

To make an informed decision, consult with a financial advisor to evaluate your specific financial situation and determine the most suitable investment strategy that aligns with your goals and provides the desired flexibility in payout options.

Lack of Transparency

Another drawback of annuities is the lack of transparency surrounding these financial products. Unlike other investments that have easily accessible market data and transparent pricing, annuities often lack standardized measures and clear disclosure of costs and fees.

One challenge is that annuity contracts can be complex and highly detailed, making it difficult for individuals without specialized financial knowledge to fully understand the terms and conditions. The language used in annuity contracts can be technical and confusing, making it challenging for investors to grasp the full scope of the investment they are entering into.

Another aspect of the lack of transparency is the limited availability of comparison tools and resources. Unlike stocks or mutual funds, which have publicly available information and performance metrics, annuities do not have standardized benchmarks or clear measures of performance. This makes it difficult for investors to make informed decisions and evaluate the relative value of one annuity product compared to another.

Furthermore, annuity fees and expenses are not always clearly disclosed. Some costs, such as surrender charges, commissions, or administrative fees, may be buried in the fine print of the contract or not clearly explained upfront. This lack of transparency can result in unexpected costs that eat into potential returns and diminish the value of the investment.

Additionally, the lack of transparency in annuities can hinder investors’ ability to assess the risk associated with these products. While annuities are often considered low-risk investments due to their guaranteed income stream, there can be underlying risks, such as the financial stability of the insurance company issuing the annuity or the potential impact of inflation on the purchasing power of the income payments.

To navigate the lack of transparency, it is crucial for investors to thoroughly review the annuity contract, ask questions, and seek professional advice. Consulting with a financial advisor who specializes in annuities can help ensure a clear understanding of the terms, costs, and potential risks associated with the specific annuity product.

Furthermore, conducting thorough research and comparing multiple annuity options, including their fees, features, and terms, can help shed some light on the investment choices available. Seeking out consumer advocacy groups or independent sources that provide objective analysis and information can also be valuable in gaining a more transparent view of the annuity marketplace.

In summary, the lack of transparency in annuities necessitates extra diligence from investors. Taking the time to understand the terms and fees, seeking professional advice, and exploring alternative investment options can help mitigate the risks associated with the lack of transparency and ensure that financial decisions are made with a clear understanding of the investment at hand.

Unexpected Risk Factors

While annuities are often marketed as low-risk investments, there are several unexpected risk factors that investors should consider. These risks can impact the performance and ultimate value of an annuity investment.

One risk factor is the financial stability of the insurance company that issues the annuity. Annuities are backed by the financial strength and claims-paying ability of the insurance company. If the company becomes financially unstable or goes bankrupt, there is a risk that it may not be able to fulfill its obligations to annuity holders. Researching the financial health and reputation of the insurance company before investing in an annuity is crucial to mitigate this risk.

Another risk is the potential impact of inflation on the purchasing power of annuity income payments. While annuities may provide a guaranteed income stream, the fixed payments may not keep pace with inflation over the long term. This means that the purchasing power of the income may decrease over time, leading to a reduced standard of living in retirement.

Interest rate risk is also a factor to consider with annuities. Annuity returns are influenced by the prevailing interest rates at the time of purchase. If interest rates rise after buying an annuity, it can lead to missed opportunities to earn higher returns on alternative investments. On the other hand, if interest rates decline, the annuity’s returns may be relatively less attractive compared to other investment options in the market.

Another risk is the lack of liquidity, which was discussed earlier. Once funds are committed to an annuity, it can be challenging to access them without incurring penalties and fees. This lack of liquidity can be problematic in situations where investors need immediate access to their funds due to unforeseen circumstances or changing financial needs.

Additionally, annuities are subject to regulatory risks. Changes in tax laws, government regulations, or policy changes can impact the tax advantages, payout options, and overall performance of annuity investments. Keeping abreast of any regulatory changes and seeking professional advice is important to navigate these risks effectively.

Investors should also be aware of the risks associated with surrender charges. Annuities often have longer lock-in periods, and early withdrawals can result in steep surrender charges. If investors need to access their funds before the surrender period ends, they may face significant financial penalties that can erode the value of the investment.

To mitigate these unexpected risks, it is crucial to conduct thorough research, seek professional advice, and carefully read the annuity contract. Understanding the fine print, assessing the financial stability of the insurance company, and evaluating the impact of inflation and interest rate changes are essential steps in managing the risks associated with annuity investments.

Furthermore, diversifying your investment portfolio by including a mix of different asset classes and investment products can help spread the risk and provide a more well-rounded approach to achieving your financial goals in retirement.

Alternatives to Annuities

While annuities have their benefits, they may not be the best investment option for everyone. Fortunately, there are alternatives available that provide different features and may better suit your financial goals and risk tolerance. Here are a few alternative investment options to consider:

1. Stocks and Bonds: Investing in individual stocks or bonds can provide potentially higher returns compared to annuities. These investments offer the opportunity for capital appreciation and dividend income. However, they also come with higher market risk and volatility, requiring careful research and continuous monitoring.

2. Mutual Funds: Mutual funds are investment vehicles that pool money from multiple investors to invest in a diversified portfolio of stocks, bonds, or other assets. They offer a broad range of investment choices and professional management. Mutual funds can be a suitable alternative for those seeking a higher potential for growth while benefiting from diversification and expertise.

3. Exchange-Traded Funds (ETFs): ETFs are similar to mutual funds but trade on stock exchanges, allowing investors to buy and sell shares throughout the trading day. ETFs offer diversification, flexibility, and lower expense ratios compared to mutual funds. They can be a cost-effective alternative for investors with a focus on index tracking or specific sectors or asset classes.

4. Real Estate Investment Trusts (REITs): REITs are companies that own or finance income-generating real estate properties. Investing in REITs provides exposure to the real estate market without the need to directly own and manage properties. REITs can offer potential income through dividends and the potential for capital appreciation.

5. Taxable Investment Accounts: Instead of investing in a tax-advantaged annuity, consider utilizing taxable investment accounts. While these accounts do not offer tax-deferred growth, they provide flexibility in terms of liquidity, investment choices, and potential tax advantages associated with long-term capital gains rates.

6. Retirement Accounts: Maximize contributions to tax-advantaged retirement accounts, such as 401(k)s or IRAs, before considering annuities. These accounts offer tax benefits and a wide range of investment options, including stocks, bonds, and mutual funds. Building a diversified portfolio within these retirement accounts can provide growth potential while taking advantage of tax advantages.

It is important to evaluate your financial goals, risk tolerance, and time horizon when considering alternative investment options. Working with a financial advisor can help you assess and determine the most suitable alternatives to annuities based on your individual circumstances.

Remember, diversification across different asset classes and investment vehicles can help spread risk and optimize your portfolio for long-term growth and financial stability.

Conclusion

While annuities may provide a guaranteed income stream and certain advantages, they also come with drawbacks that make them less favorable investment options for many individuals. The lack of liquidity, high fees, limited growth potential, complexity, tax consequences, inflexibility in payouts, lack of transparency, unexpected risk factors, and alternatives to annuities all contribute to the considerations investors should keep in mind.

When evaluating annuities, it is essential to assess your own financial goals, risk tolerance, and future needs. Thoroughly understanding the terms, fees, and potential risks associated with annuity contracts is crucial before making any investment decisions. Seeking advice from a financial advisor with expertise in annuities can provide valuable insights and help align your investment strategy with your specific goals.

Additionally, exploring alternatives such as stocks, bonds, mutual funds, ETFs, REITs, taxable investment accounts, and retirement accounts can offer more flexibility, growth potential, and transparency—providing a range of options to suit your investment preferences and objectives. Diversifying your investment portfolio across different asset classes can further help mitigate risks and optimize your overall financial strategy.

Ultimately, the decision of whether annuities are suitable for your investment needs depends on your individual circumstances, risk appetite, and long-term financial goals. By conducting thorough research, seeking professional advice, and carefully considering the pros and cons, you can make informed investment decisions that align with your unique financial objectives.