Importance of Risk Tolerance in Investing

When it comes to investing, understanding your risk tolerance is crucial. Risk tolerance refers to an individual’s ability and willingness to endure fluctuations in the value of their investments. It is a measure of how much risk you are comfortable taking with your money. Assessing your risk tolerance is essential because it determines the types of investments that are suitable for you.

Investing in financial markets inherently involves risk, as there is no guaranteed return on investment. Different people have different levels of tolerance for risk, based on factors such as their financial goals, time horizon, and personal comfort level. Some individuals may be more comfortable with a higher degree of risk, while others prefer a more conservative approach.

One of the key reasons why understanding risk tolerance is important is to prevent investors from making impulsive and emotional decisions during periods of market volatility. If an individual invests in assets with a higher level of risk than they are comfortable with, they may panic and sell their investments at the first sign of a market downturn. This knee-jerk reaction can lead to significant losses and hinder long-term financial growth.

On the other hand, investing with a low-risk tolerance allows individuals to have more stability in their portfolios. Though lower-risk investments typically provide lower returns, they offer a higher level of security and peace of mind. This is particularly beneficial for those who have a lower tolerance for losing money and prioritize capital preservation over aggressive growth.

In addition, understanding your risk tolerance helps you align your investment goals with appropriate investment strategies. By considering your risk appetite, you can select investments that have a higher likelihood of meeting your financial objectives while taking into account the level of risk you are willing to accept.

Overall, having a clear understanding of your risk tolerance is crucial for successful investing. It not only helps you make informed decisions but also enables you to create a well-diversified portfolio that aligns with your financial goals and comfort level. So, before embarking on your investment journey, take the time to assess your risk tolerance with the help of a financial advisor or an online questionnaire. By doing so, you can set yourself up for long-term financial success and peace of mind.

Understanding Risk Tolerance

Risk tolerance is a fundamental concept in investing that refers to an individual’s ability to handle uncertainty and withstand potential losses. Each person has a unique risk tolerance level, influenced by factors such as financial circumstances, investment knowledge, time horizon, and emotional disposition.

To assess your risk tolerance, it is important to consider your financial goals and objectives. Are you investing for short-term gains or long-term wealth accumulation? Are you primarily focused on capital preservation or are you comfortable with taking on more risk for potential higher returns?

Another aspect to consider is your emotional response to market volatility. Does the thought of your portfolio declining lead to sleepless nights and feelings of anxiety? Or are you able to view market fluctuations as normal and understand that they are part of the investment journey?

Furthermore, evaluating your financial capacity to bear losses is essential in determining your risk tolerance. This involves analyzing your current financial situation, including your income, assets, liabilities, and expenses. It is crucial to invest only what you can afford to lose without compromising your overall financial wellbeing.

An important point to note is that risk tolerance may vary over time. As circumstances change, such as reaching different life stages or experiencing a shift in your financial situation, your willingness to take on risk may evolve. Regularly reassessing and adjusting your risk tolerance is advisable to ensure that your investments align with your changing needs and goals.

Financial professionals and online questionnaires can help you assess your risk tolerance. These tools typically ask a series of questions to gauge your comfort level with different investment scenarios and determine your risk tolerance profile.

It is crucial to be honest and self-aware when assessing your risk tolerance. Overestimating your risk tolerance may lead to investing in high-risk assets that cause excessive stress and anxiety. Conversely, underestimating your risk tolerance may result in missing out on potential growth opportunities.

Understanding your risk tolerance allows you to make informed investment decisions and construct a diversified portfolio that aligns with your comfort level. Maintaining a balance between risk and reward is key to achieving your financial goals while ensuring you can sleep soundly at night.

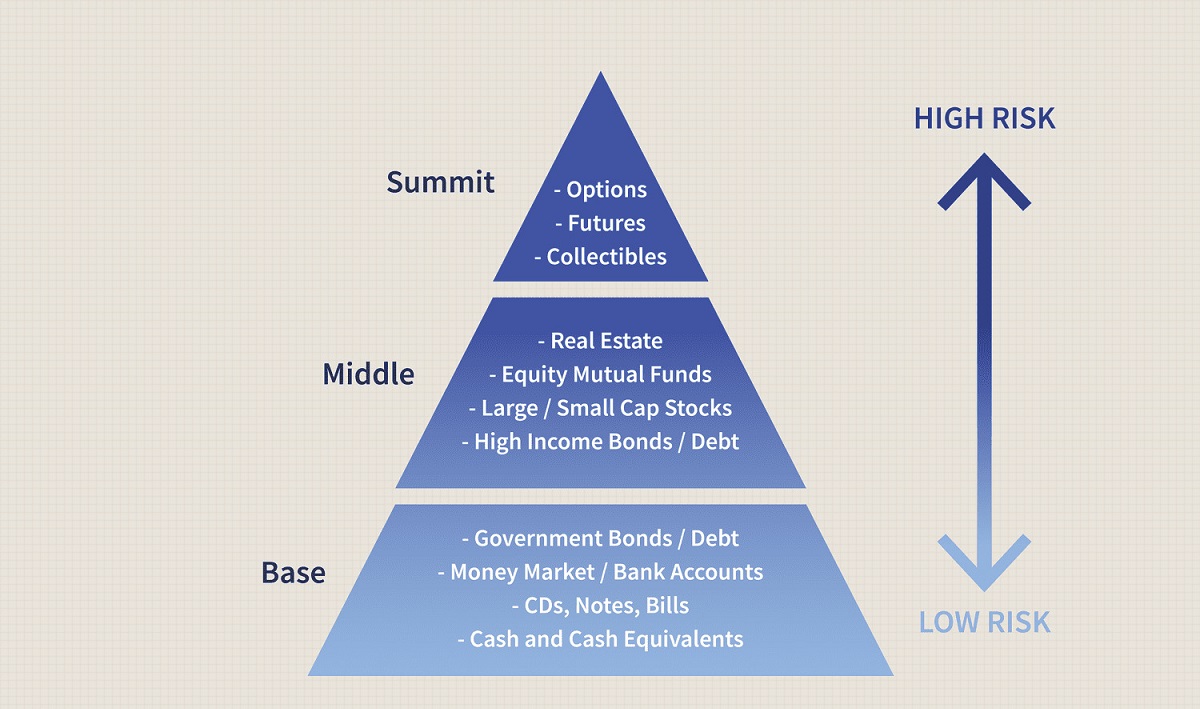

Low-Risk Investments

For individuals with a low-risk tolerance, there are several investment options available that prioritize capital preservation and offer more stable returns. These investments are characterized by lower volatility and are considered safer than higher-risk alternatives.

Here are some common low-risk investments to consider:

- Bonds: Bonds are debt securities issued by governments, municipalities, and corporations. They provide fixed interest payments over a specified period and return the principal amount at maturity. Bonds are generally considered safer than stocks.

- Certificate of Deposit (CD): A CD is a time deposit offered by banks and credit unions. It has a fixed term and fixed interest rate. CDs offer a guaranteed return of principal and usually higher interest rates than traditional savings accounts.

- Money Market Funds: Money market funds invest in highly liquid and low-risk securities such as Treasury bills and short-term commercial paper. They aim to maintain a stable net asset value of $1 per share and provide a low-risk alternative to traditional savings accounts.

- Treasury Securities: Treasury securities are debt obligations issued by the U.S. government. They include Treasury bills, notes, and bonds. These investments are considered very low-risk as they are backed by the full faith and credit of the U.S. government.

- Cash: Holding cash in a savings account or a money market account is a low-risk option. While it may not generate significant returns, it provides immediate liquidity and acts as a buffer against market fluctuations.

- Fixed Annuities: Fixed annuities are insurance contracts that guarantee a fixed rate of return over a specific period. They offer a predictable income stream and are suitable for risk-averse individuals seeking steady income during retirement.

- Dividend-Paying Stocks: Although stocks are generally considered riskier than other low-risk investments, dividend-paying stocks can offer stability and income. These stocks belong to companies with a consistent track record of paying dividends even during economic downturns.

- Blue-Chip Stocks: Blue-chip stocks are shares of large, well-established companies with a history of stable performance. These companies are typically leaders in their industry and are known for reliable dividends and long-term growth potential.

- Index Funds: Index funds are mutual funds or exchange-traded funds (ETFs) that aim to replicate the performance of a specific market index, such as the S&P 500. These funds provide instant diversification and typically have lower expense ratios compared to actively managed funds.

- Conservative Mutual Funds: Conservative mutual funds focus on capital preservation by investing in low-risk assets such as bonds and stable dividend-paying stocks. These funds aim for steady, modest returns with lower volatility.

- Real Estate Investment Trusts (REITs): REITs are investment vehicles that own and operate income-generating properties such as office buildings, apartments, and shopping centers. They offer investors the opportunity to participate in real estate ownership without direct property management responsibilities.

It is important to note that while these investments are generally considered low risk, they are not entirely risk-free. It is advisable to conduct thorough research and consult with a financial advisor to ensure these investments align with your risk tolerance and financial goals.

Bonds

Bonds are fixed-income securities issued by entities such as governments, municipalities, and corporations to raise capital. When you invest in bonds, you essentially lend money to the issuer in exchange for regular interest payments and the return of the principal amount at maturity.

Bonds are considered low-risk investments because they have a predetermined interest rate and maturity date. They offer more stability compared to stocks, as the issuing entity has an obligation to repay the borrowed funds.

There are different types of bonds that you can consider:

- Government Bonds: Government bonds, such as U.S. Treasury bonds, are backed by the full faith and credit of the government. They are often considered the safest type of bond investment, as the risk of default is extremely low.

- Municipal Bonds: Municipal bonds are issued by state and local governments to finance public projects. The interest income from municipal bonds is usually exempt from federal taxes and may be exempt from state and local taxes for residents of the issuing state.

- Corporate Bonds: Corporate bonds are issued by companies to raise capital. They offer higher yields compared to government and municipal bonds but also carry a higher risk. The creditworthiness of the issuing company is an important factor to consider when investing in corporate bonds.

- Zero-Coupon Bonds: Zero-coupon bonds don’t pay regular interest like traditional bonds. Instead, they are sold at a discount to their face value and provide a fixed return at maturity. They are often purchased for future financial goals, as they offer a lump sum payment at the end of the bond term.

- Treasury Inflation-Protected Securities (TIPS): TIPS are U.S. Treasury bonds that are designed to protect investors against inflation. The principal value of TIPS is adjusted based on changes in the Consumer Price Index (CPI), ensuring that the investment keeps pace with inflation.

Bonds can be bought and sold on the bond market before they mature, which means their value can fluctuate. However, if you hold bonds until maturity, you will receive the full face value of the bond, assuming no default occurs.

It’s important to understand that while bonds are generally considered low-risk, they are not entirely risk-free. There is still the risk of default, particularly with corporate bonds, and changes in interest rates can affect bond prices. Additionally, inflation can erode the purchasing power of the fixed interest payments over time.

If you have a low-risk tolerance, investing in bonds can provide stability to your portfolio and generate regular income. However, it’s important to diversify your bond investments and consider the creditworthiness of the issuers to mitigate potential risks.

Certificate of Deposit (CD)

A Certificate of Deposit (CD) is a type of time deposit offered by banks and credit unions. It is a low-risk investment option that provides a fixed interest rate and a guaranteed return of principal at maturity.

When you invest in a CD, you agree to keep your money deposited for a specific period, known as the term. The term can range from a few months to several years, depending on the financial institution and the CD’s terms. During this time, the funds are locked in, and you cannot withdraw them without incurring a penalty.

CDs are considered low-risk because they are insured by the Federal Deposit Insurance Corporation (FDIC) for banks or the National Credit Union Administration (NCUA) for credit unions. This means that even if the issuing institution fails, your investment, up to $250,000 per account holder, is protected.

There are several advantages to investing in CDs:

- Stability: CDs provide stability to your portfolio due to their fixed interest rate and guaranteed return of principal. They are ideal for risk-averse individuals seeking a safe investment option.

- Predictability: With a CD, you know exactly how much interest you will earn during the term and when you will receive your principal back. This predictability makes it easier to plan and manage your finances.

- Higher Interest Rates: CDs typically offer higher interest rates compared to traditional savings accounts. The longer the CD term, the higher the interest rate tends to be. This can be advantageous if you don’t need immediate access to your funds.

- FDIC/NCUA Insurance: The FDIC/NCUA insurance on CDs provides an extra layer of protection for your investment, ensuring that even if the financial institution fails, your money is safe.

- Tax Advantages: The interest earned on CDs is taxable income. However, if you hold the CD in a tax-advantaged account such as an Individual Retirement Account (IRA), you can defer taxes on the interest until you withdraw the funds in retirement.

It’s essential to consider a few factors when investing in CDs. Firstly, the interest rate on a CD is fixed for the duration of the term, which means you may miss out on higher interest rates if rates increase during that time. Additionally, withdrawing funds from a CD before the maturity date typically triggers an early withdrawal penalty, so it’s important to be certain about the timeframe for which you can commit your funds.

CDs are best suited for individuals who have a low-risk tolerance, a specific savings goal in mind, and don’t need immediate access to their funds. They provide a safe and predictable way to earn interest on your money while preserving your capital.

Money Market Funds

Money Market Funds are investment options that provide individuals with a low-risk alternative to traditional savings accounts. These funds invest in short-term, highly liquid, and low-risk securities such as Treasury bills, commercial paper, and certificates of deposit.

Money Market Funds aim to maintain a stable net asset value (NAV) of $1 per share, making them an attractive choice for risk-averse investors seeking liquidity and capital preservation.

Here are some key features and benefits of Money Market Funds:

- Liquidity: Money Market Funds offer a high level of liquidity, allowing investors to easily access their money when needed. They typically allow for check writing or electronic transfers, making it convenient to withdraw funds.

- Stability: These funds are considered low-risk due to their investments in highly rated short-term securities. While they can still be subject to minimal price fluctuations, their primary objective is to preserve capital and maintain a stable NAV.

- Diversification: Money Market Funds provide instant diversification as they invest in a range of short-term securities issued by various entities, such as the government and corporations. This diversification helps to spread risk and minimize exposure to any single issuer.

- Regular Income: Money Market Funds aim to generate income for investors through interest payments from the securities held in the fund’s portfolio. However, it’s important to note that the yield on Money Market Funds is typically lower compared to other types of investments.

- Safety: Money Market Funds are regulated by the Securities and Exchange Commission (SEC) and are subject to strict investment guidelines to ensure investor protection. However, it’s important to select funds from reputable financial institutions with a history of stability and strong management.

- Accessibility: Money Market Funds are available through most brokerage firms, mutual fund companies, and banks. They offer individuals the opportunity to invest with relatively low minimum investment requirements.

While Money Market Funds are generally considered low-risk, it’s important to be aware of a few considerations. First, the yield on these funds can be influenced by interest rate fluctuations and market conditions. Second, although rare, it is important to note that Money Market Funds are not guaranteed by the government, and there is still a potential risk of loss of principal.

Money Market Funds are suitable for individuals with a low-risk tolerance and a need for short-term liquid investments. They can be used as a cash management tool, an alternative to a traditional savings account, or a place to temporarily park funds while waiting for other investment opportunities.

Before investing in Money Market Funds, it’s advisable to carefully review the fund’s prospectus, assess the associated fees, and select funds that align with your investment goals and risk tolerance.

Treasury Securities

Treasury Securities are debt obligations issued by the U.S. Department of the Treasury to fund the government’s operations and pay for federal expenses. These securities are considered one of the safest investment options available, making them a popular choice for risk-averse individuals.

Here are three common types of Treasury Securities:

- Treasury Bills (T-Bills): Treasury Bills are short-term securities with maturities ranging from a few days to one year. They are sold at a discount to their face value and do not pay regular interest. Instead, investors earn interest by purchasing a T-Bill at a discount and receiving the face value at maturity.

- Treasury Notes: Treasury Notes have maturities ranging from two to ten years. They pay semi-annual interest dividends, providing investors with regular income. At maturity, investors receive the full face value of the note.

- Treasury Bonds: Treasury Bonds have the longest maturity periods, ranging from ten to thirty years. They also pay semi-annual interest dividends and provide a predictable income stream. Investors receive the face value of the bond at maturity.

Treasury Securities are considered one of the safest investments because they are backed by the full faith and credit of the U.S. government. This means that the likelihood of default is extremely low, making them virtually risk-free.

Investing in Treasury Securities offers several advantages:

- Safety: Treasury Securities are considered the benchmark for safe investments, as they are backed by the U.S. government. They are an ideal choice for risk-averse individuals seeking capital preservation.

- Stability: These securities offer stable and predictable payments. The interest rate is fixed at the time of issuance, providing investors with a steady income stream.

- Liquidity: Treasury Securities can be easily bought and sold in the secondary market, providing investors with readily available cash if needed. They offer high liquidity compared to other fixed-income investments.

- Tax Advantage: The interest income earned from Treasury Securities is subject to federal income tax but exempt from state and local taxes. This can be advantageous, particularly for investors in high-tax states.

- Diversification: Treasury Securities can be used as a diversification tool within a portfolio, as they tend to have a negative correlation with certain riskier asset classes, such as stocks.

Although Treasury Securities are considered low-risk, there are a few factors to consider. First, changes in interest rates can impact the market value of these securities, especially for longer-term bonds. Second, while Treasury Securities are backed by the government, inflation can erode the purchasing power of their fixed interest payments over time.

Investing in Treasury Securities is suitable for individuals with a low-risk tolerance who prioritize capital preservation and are seeking a safe haven for their investments. They offer stability, safety, and a guaranteed return of principal.

Before investing in Treasury Securities, it’s important to understand your investment goals, review the available options, and consult with a financial advisor if necessary.

Cash

Cash is the most liquid and readily accessible form of asset. While it may not generate substantial returns, holding cash is considered a low-risk investment option, especially for individuals with a low-risk tolerance.

Here are some key aspects to consider when it comes to holding cash as an investment:

- Liquidity: Cash provides immediate access to funds, allowing you to meet unexpected expenses or take advantage of investment opportunities that may arise.

- Stability: Unlike other investments, the value of cash remains relatively stable over time. A dollar today retains its value as a dollar tomorrow.

- Capital Preservation: Holding cash ensures that your capital is preserved, as there is no risk of loss due to changes in market conditions or economic downturns.

- Emergency Fund: Having a portion of your wealth in cash serves as an emergency fund to cover unforeseen circumstances, such as medical expenses or job loss.

- Opportunity Cost: While cash provides stability, it may not keep pace with inflation. Over time, the purchasing power of your cash may decline, resulting in a loss of potential returns.

It is important to strike a balance between holding cash and allocating funds to other investments that offer the potential for growth. Investing solely in cash may not allow you to keep up with inflation or achieve long-term financial goals.

However, having cash on hand provides a sense of security and offers flexibility in managing your financial affairs. It allows you to take advantage of investment opportunities when they arise or navigate through uncertain economic times without relying on external sources of financing.

When considering cash as an investment, it is advisable to regularly review and reassess your financial goals, risk tolerance, and liquidity needs. Maintaining an appropriate amount of cash ensures that you have enough funds readily available for short-term needs while maximizing the potential returns on the remainder of your portfolio through other investment avenues.

Ultimately, the decision to hold cash as an investment should be based on your individual circumstances, financial goals, and risk tolerance. Consulting with a financial advisor can provide you with personalized guidance on how much cash to hold and how to allocate your assets for overall financial well-being.

Fixed Annuities

Fixed annuities are insurance contracts that provide individuals with a guaranteed income stream in retirement. They are a low-risk investment option that offers stability and a predictable source of income.

Here are some key features and benefits of fixed annuities:

- Guaranteed Income: Fixed annuities guarantee a fixed rate of return over a specific period or for life. This provides individuals with a stable income stream during their retirement years, helping to cover basic living expenses and provide financial security.

- Capital Preservation: With fixed annuities, the principal amount is protected against market fluctuations, making them a suitable choice for risk-averse individuals seeking to preserve their capital.

- Tax-Deferred Growth: Annuities allow for tax-deferred growth, meaning you won’t pay taxes on your annuity’s earnings until you start receiving withdrawals or annuitizing the contract. This allows your investment to potentially grow faster over time.

- Flexibility: Fixed annuities offer various payout options to suit individual preferences, such as a lump sum payment, periodic income payments, or a combination of both.

- Death Benefit: Fixed annuities often come with a death benefit, which means that if the contract owner passes away before the annuity payments begin, their beneficiaries will receive a predetermined amount.

- Insurance Protection: Fixed annuities are typically backed by insurance companies, providing an additional layer of protection for investors. It is important to choose annuities from reputable and financially stable insurance providers.

While fixed annuities offer stability and guaranteed income, there are a few factors to consider:

- Illiquidity: Fixed annuities are long-term investments with generally limited or no access to the principal until a specific surrender period is over. Withdrawals made before the end of the surrender period may be subject to surrender charges or penalties.

- Inflation Risk: While fixed annuities provide a stable income, the purchasing power of that income may be eroded by inflation over time. Consider other investment options or strategies to help mitigate the effects of inflation.

- Interest Rate Risk: Fixed annuities’ rates are often locked in at the time of purchase. However, if interest rates rise significantly, the fixed return may not keep pace with other investment opportunities.

- Complexity: Understanding the terms and conditions of fixed annuities can be complex. It is advisable to carefully read the contract and consult with a financial advisor to ensure that you fully comprehend the terms, associated fees, and potential surrender charges.

Fixed annuities are suitable for individuals who prioritize stable retirement income, have a low-risk tolerance, and have a longer-term investment horizon. They provide a guaranteed income stream and can be a valuable component of a well-diversified retirement portfolio.

Before investing in fixed annuities, it’s crucial to assess your financial goals, consult with a financial advisor or insurance professional, and carefully evaluate the terms and conditions of the annuity contract to determine if it aligns with your needs and risk profile.

Dividend-Paying Stocks

Dividend-paying stocks are shares of companies that distribute a portion of their profits to shareholders in the form of dividends. These stocks are a popular investment choice for individuals seeking a combination of potential capital appreciation and regular income.

Here are some key aspects to consider when investing in dividend-paying stocks:

- Regular Income: Dividend-paying stocks provide investors with a steady income stream through regular dividend payments. These payments can be a reliable source of income, especially for individuals seeking consistent cash flow.

- Capital Appreciation: In addition to regular income, dividend-paying stocks offer the potential for capital appreciation. If the stock price increases over time, investors can benefit from both dividend income and an increase in the value of their investment.

- Diversification: Dividend-paying stocks come from various sectors and industries, allowing investors to diversify their portfolio. By investing in multiple dividend-paying stocks, individuals can reduce risk and potentially achieve more stable returns.

- Dividend Growth Potential: Some companies have a history of consistently increasing their dividend payments over time. Investing in dividend-paying stocks with a track record of dividend growth may provide additional income growth and potential for long-term returns.

- Dividend Yield: Dividend yield is a measure of the dividend payment relative to the stock price. It is calculated as the annual dividend per share divided by the stock price. Investors often compare dividend yields to assess the potential income generated by different dividend-paying stocks.

- Company Financial Health: When considering dividend-paying stocks, it is important to assess the financial health of the underlying companies. Look for companies with a strong balance sheet, consistent earnings growth, and a history of maintaining or increasing dividend payments.

- Risk and Volatility: While dividend-paying stocks are generally considered lower risk than growth stocks, they are not entirely risk-free. The stock price can still fluctuate, and companies may cut or suspend dividend payments in challenging economic conditions or if their financial performance deteriorates.

Dividend-paying stocks are suitable for investors who prioritize regular income and are willing to take on some level of market risk. They can be particularly appealing for individuals in or near retirement who are seeking to supplement their cash flow.

It’s important to note that dividend-paying stocks should not be the sole focus of an investment portfolio. Diversification across different asset classes and sectors is key to managing risk and maximizing potential returns.

Before investing in dividend-paying stocks, it’s advisable to conduct thorough research on individual companies, assess their financial health and dividend history, and consider consulting with a financial advisor to ensure that your investment aligns with your financial goals and risk tolerance.

Blue-Chip Stocks

Blue-chip stocks are shares of well-established, financially sound companies that have a history of stable performance and a strong market presence. These stocks are often considered safe, reliable, and suitable for investors with a low-risk tolerance.

Here are some key characteristics and benefits of blue-chip stocks:

- Stability: Blue-chip stocks belong to companies that have withstood the test of time and demonstrated resilience through various market cycles. Their stable performance is attributed to their strong market position and the ability to generate consistent revenue and earnings.

- Blue-Chip Status: The term “blue-chip” originated from the game of poker, where blue chips represent the highest value. Similarly, blue-chip stocks are considered the highest quality stocks in the market.

- Dividend Payments: Many blue-chip stocks are known for their reliable dividend payments. These companies often distribute a portion of their profits to shareholders, providing a steady income stream for investors.

- Large Market Capitalization: Blue-chip stocks typically have a large market capitalization, indicating their significant size and market influence. This can provide added stability and confidence to investors.

- Brand Recognition: Blue-chip companies are often household names with widely recognized brands. Their strong brand presence and customer loyalty contribute to their ability to withstand economic downturns and maintain market leadership.

- Lower Volatility: While no investment is entirely risk-free, blue-chip stocks are known for their lower volatility compared to smaller, growth-oriented companies. These stocks tend to be less susceptible to extreme price fluctuations.

Investing in blue-chip stocks offers the potential for long-term growth and income. However, it is important to consider a few factors:

- Valuation: Blue-chip stocks may be priced at a premium due to their perceived safety and stability. It’s important to carefully assess the valuation and determine whether the stock is trading at a reasonable price relative to its fundamental value.

- Market Conditions: Although blue-chip stocks are generally considered less volatile, they can still be influenced by broad market trends and economic factors. It’s crucial to stay informed about market conditions and monitor the performance of blue-chip companies.

- Diversification: While blue-chip stocks provide stability, it’s important to diversify your portfolio across various sectors and asset classes. This helps spread risk and reduce exposure to any single company or industry.

- Company-specific Risks: Even well-established companies can face industry-specific or company-specific risks. It’s essential to conduct thorough research on individual blue-chip stocks and understand the potential risks associated with their businesses.

Blue-chip stocks can be a valuable addition to a well-diversified investment portfolio, offering stability, income, and the potential for long-term growth. However, it’s important to carefully evaluate individual companies, monitor market conditions, and consider your own risk tolerance and investment goals before investing in blue-chip stocks.

Index Funds

Index funds are investment funds that aim to replicate the performance of a specific market index, such as the S&P 500 or the Dow Jones Industrial Average. These funds offer a low-risk investment option that provides instant diversification and is suitable for investors with a long-term investment horizon.

Here are some key aspects to consider when investing in index funds:

- Diversification: Index funds provide instant diversification across a broad range of securities within the index they track. This diversification helps spread risk and reduces exposure to any individual stock or sector.

- Low Costs: Index funds generally have lower expense ratios compared to actively managed funds. This is because they aim to replicate the performance of an index rather than relying on expensive research or active stock picking. Lower costs can contribute to higher overall returns for investors.

- Passive Management: Index funds follow a passive investment strategy, meaning they seek to match the performance of the index they track rather than trying to outperform it. This approach eliminates the need for frequent buying and selling of securities, reducing transaction costs.

- Market Performance: Index funds provide investors with exposure to the overall performance of the market or a specific segment of the market. This allows investors to participate in market growth and benefit from the long-term upward trend of the index they track.

- Consistency: Index funds offer consistent and predictable investment returns since they aim to replicate the performance of a specific index. Investors can have confidence in the fund’s ability to mirror the index’s performance over time.

- Ease of Investing: Index funds are widely available and can be purchased through brokerage accounts, mutual fund companies, and retirement plans. They are accessible to both individual investors and institutional investors.

While index funds are considered low-risk investments, it’s important to be aware of a few factors:

- Market Volatility: Index funds are still subject to market volatility and can experience fluctuations in value, particularly during periods of broader market uncertainty or economic downturns.

- Specific Index Performance: The performance of an index fund is directly tied to the performance of the specific index it tracks. If the underlying index experiences a downturn or underperforms, the value of the index fund will also be affected.

- No Active Management: While index funds provide broad market exposure, they do not offer the potential for outperformance achieved through active management strategies. The returns of index funds will mirror the performance of the specific index, whether positive or negative.

Investing in index funds can be a prudent and cost-effective approach to long-term investing. They provide diversification, market exposure, and low expense ratios, making them a suitable choice for individuals seeking a low-risk investment option with consistent returns over time.

It’s important to carefully evaluate index funds and select those that align with your investment goals, risk tolerance, and time horizon. Consider consulting with a financial advisor or doing thorough research to understand the fund’s tracking strategy, cost structure, and historical performance before making any investment decisions.

Conservative Mutual Funds

Conservative mutual funds are investment vehicles that prioritize capital preservation and aim to generate steady, modest returns over time. These funds are designed for risk-averse investors who seek stability and income generation without taking on significant market volatility.

Here are some key features and benefits of conservative mutual funds:

- Capital Preservation: Conservative mutual funds focus on preserving the initial investment amount and minimizing downside risk. The fund manager typically invests in a diversified portfolio of low-risk assets, such as high-quality bonds, dividend-paying stocks, and cash equivalents.

- Steady Income: Conservative mutual funds often allocate a portion of their portfolio to income-generating securities, such as bonds and dividend-paying stocks. This allows investors to benefit from regular income distributions, providing a stable cash flow.

- Lower Volatility: These funds tend to have lower volatility compared to more aggressive investments, such as growth or equity funds. The emphasis on stability gives conservative mutual fund investors a sense of security amid market fluctuations.

- Professional Management: Conservative mutual funds are actively managed by professional fund managers who make investment decisions based on the fund’s investment objectives and risk tolerance. Their expertise and research help navigate market conditions and optimize risk-adjusted returns.

- Diversification: Conservative mutual funds strive to achieve diversification by investing across different asset classes, regions, and sectors. This diversification helps spread risk and reduces exposure to any single investment.

- Liquidity: Mutual funds offer high liquidity, allowing investors to buy or sell shares on any business day at the fund’s net asset value (NAV). This makes it easy to access funds when needed compared to other less liquid investment options.

It’s important to consider a few factors when investing in conservative mutual funds:

- Return Potential: Conservative mutual funds typically aim for steady, modest returns rather than aggressive growth. The focus is on capital preservation and income generation, which may result in lower returns compared to higher-risk investments.

- Fund Expenses: Mutual funds charge fees for their management and administration. It’s important to carefully review the fund’s expense ratio and fees, as these can impact overall returns, especially for conservative funds where returns may already be more conservative.

- Market Conditions: While conservative mutual funds aim to minimize risk, they are still influenced by market conditions and factors such as interest rates, economic developments, and geopolitical events. Investors should monitor these factors and consider their potential impact on the fund’s performance.

Investing in conservative mutual funds can be suitable for individuals who prioritize capital preservation, prefer lower volatility, and require a regular income stream. These funds offer a balanced approach to investing, targeting reasonable returns while managing risk.

Before investing in a conservative mutual fund, it’s important to carefully review the fund’s investment objectives, portfolio holdings, and historical performance. Consider consulting with a financial advisor who can assess your investment goals and risk tolerance to ensure that the fund aligns with your individual needs and objectives.

Real Estate Investment Trusts (REITs)

Real Estate Investment Trusts (REITs) are investment vehicles that allow individuals to invest in real estate without directly owning properties. They are a popular choice for investors looking to diversify their portfolios and generate income through real estate investments.

Here are some key aspects to consider when investing in REITs:

- Real Estate Exposure: REITs provide investors with exposure to real estate assets, including commercial properties, residential properties, and infrastructure projects. This allows individuals to potentially benefit from the income and appreciation associated with real estate investment.

- Income Generation: REITs are required by law to distribute a significant portion of their taxable income to shareholders in the form of dividends. This makes them an attractive option for income-seeking investors, as they offer regular income streams.

- Diversification: REITs offer diversification benefits, as they typically own and operate a portfolio of different types of properties across various regions. By investing in REITs, individuals can gain exposure to different sectors of the real estate market without the need for a large capital outlay.

- Professional Management: REITs are managed by professional real estate experts who have the knowledge and experience to select, acquire, and manage properties. Their expertise ensures that the portfolio is managed efficiently and optimized for income generation and long-term growth.

- Liquidity: REITs are traded on major stock exchanges, allowing investors to buy or sell shares easily. This provides liquidity and flexibility compared to directly owning properties, which can be illiquid and require significant capital investments.

- Access to Different Property Types: REITs invest in various types of properties, such as office buildings, shopping malls, residential complexes, and industrial warehouses. This allows investors to diversify their exposure to different sectors of the real estate market and potentially benefit from different market dynamics.

While investing in REITs has its advantages, there are a few factors to consider:

- Market Risks: REITs are subject to market risks, such as changes in interest rates, economic conditions, and property market trends. These factors can impact the overall performance of the REIT and the value of the investment.

- Management Quality: The success of a REIT largely depends on the quality of its management team. It’s important to research the track record, experience, and expertise of the management team to ensure they have a proven ability to navigate the real estate market effectively.

- Risk of Vacancy and Poor Performance: The performance of a REIT can be influenced by factors such as occupancy rates, rental income, and property management practices. Investors should assess the quality and stability of the underlying properties to mitigate the risk of poor performance or high vacancy rates.

- Tax Considerations: REIT dividends are generally taxable income. However, certain tax advantages may be available, such as deductions for depreciation and the potential for favorable tax treatment for qualified dividends. It’s advisable to consult with a tax advisor to understand the tax implications specific to your situation.

Investing in REITs can be suitable for individuals seeking exposure to the real estate market and desiring regular income streams. It offers the potential for diversification and professional management of real estate assets without direct property ownership.

Before investing in REITs, it’s important to thoroughly research the specific REIT you are considering, assess the quality of the underlying properties, review the performance history, and consult with a financial advisor to ensure that the investment aligns with your financial goals and risk tolerance.

Diversification for Low-Risk Investors

Diversification is an essential strategy for low-risk investors seeking to optimize their investment portfolios. By diversifying, investors can spread their risk across different assets, sectors, and geographies, reducing the potential impact of any single investment.

Here are some key reasons why diversification is important for low-risk investors:

- Risk Reduction: Diversification helps mitigate the impact of individual investment losses by spreading risk across multiple assets. When one investment underperforms, others may perform better, minimizing overall portfolio volatility.

- Protection against Market Volatility: Different asset classes and sectors perform differently under varying market conditions. By diversifying across asset classes, such as stocks, bonds, and real estate, low-risk investors can protect their portfolios against market volatility and reduce exposure to any single asset’s performance.

- Preservation of Capital: Diversification is a key strategy for capital preservation. By spreading investments across different assets, low-risk investors can safeguard their capital against the potential loss associated with any single investment.

- Opportunity for Growth: Diversification allows low-risk investors to participate in the growth potential of various asset classes and sectors. While low-risk investments may provide more modest returns, incorporating diversified assets can enhance the overall growth potential of the portfolio.

- Income Generation: Diversification can also aid in generating income. By including income-generating assets, such as bonds or dividend-paying stocks, in the portfolio, low-risk investors can benefit from regular income streams while still maintaining a low-risk profile.

- Adaptation to Changing Market Conditions: Diversification helps protect against unforeseen events or shifts in the market. By diversifying across various assets, low-risk investors can adapt their portfolios to changing economic conditions and reduce vulnerability to any single sector or industry.

When implementing diversification strategies, low-risk investors should consider several factors:

- Asset Allocation: Allocate investment funds across different asset classes, such as stocks, bonds, cash, and real estate, based on your risk tolerance, investment objectives, and time horizon.

- Geographic Diversification: Spread investments across different regions and countries to reduce exposure to any single geographic area’s economic performance.

- Sector Diversification: Invest in companies across different sectors to minimize the impact of sector-specific risks. Diversifying across industries such as technology, healthcare, consumer goods, and utilities can help balance the portfolio.

- Time Diversification: Invest over a period of time rather than making lump-sum investments. This strategy, known as dollar-cost averaging, can help reduce the impact of short-term market volatility.

- Regular Portfolio Rebalancing: Periodically review the portfolio to ensure it aligns with the intended asset allocation and rebalance if necessary. Rebalancing involves adjusting asset weights to maintain the desired risk and return parameters.

While diversification helps mitigate risk, it does not guarantee profits or protect against losses in declining markets. It is crucial for low-risk investors to assess their risk tolerance, conduct thorough research, and seek professional advice when diversifying their portfolios.

By incorporating diversification strategies, low-risk investors can build robust portfolios that offer stability, protection against market downturns, and the potential for steady, long-term growth.

Conclusion

For low-risk investors, making informed investment decisions is crucial to achieve their financial goals while minimizing the potential for loss. By understanding risk tolerance and incorporating suitable investment strategies, low-risk investors can create a well-balanced and secure portfolio.

Investments such as low-risk bonds, certificate of deposits (CDs), money market funds, treasury securities, and cash provide stability and capital preservation. These options are particularly suitable for individuals with a low-risk tolerance who prioritize safeguarding their investments and minimizing volatility.

Furthermore, diversification plays a vital role in mitigating risks for low-risk investors. By spreading investments across different asset classes, sectors, and geographic regions, investors can minimize the impact of any single investment or economic event on their portfolio. Diversification allows for a balanced combination of risk and return, ensuring a more stable and resilient investment approach.

It is essential for low-risk investors to conduct thorough research, assess their risk tolerance, and consult with financial advisors to make informed decisions that align with their financial goals and objectives. Regular monitoring and periodic adjustments to the portfolio will help ensure that the investment strategy remains relevant and in line with changing market conditions and individual circumstances.

In summary, with a clear understanding of risk tolerance, the incorporation of low-risk investments, and the implementation of a well-diversified portfolio, low-risk investors can navigate the investment landscape with confidence, seeking stable returns and peace of mind in their financial journey.