Introduction

Investing is an essential tool for building wealth and achieving financial goals. However, it is crucial to strike a balance between high-risk and low-risk investments to mitigate potential losses while maximizing returns. The investment landscape offers a spectrum of opportunities, each with its own level of risk and potential rewards.

High-risk investments can offer substantial returns, but they come with an increased probability of loss. These may include stocks of emerging companies, speculative assets, or investments in volatile industries. On the other hand, low-risk investments typically offer a lower return, but they provide stability and security. Examples of low-risk investments include government bonds, certificates of deposit, and savings accounts.

Understanding your risk tolerance is a critical first step in maintaining the right balance between high-risk and low-risk investments. This refers to your ability to endure fluctuations in the value of your investments and your comfort level with taking risks. Factors such as your financial goals, time horizon, and personal circumstances should all be considered when determining your risk tolerance.

Diversification is a key strategy for balancing high-risk and low-risk investments. By spreading your investments across different asset classes, industries, and geographical regions, you can reduce the impact of any individual investment’s performance on your overall portfolio. This diversification helps to mitigate risk and increase the potential for consistent returns.

In this article, we will explore how you can maintain a balance between high-risk and low-risk investments. We will discuss the importance of understanding your risk tolerance, the benefits of diversification, and the process of determining the right mix of investments. We will also provide insights on monitoring your portfolio, staying informed about market trends, seeking professional advice, and adjusting your investment strategy as your financial goals evolve.

By implementing these strategies, you can create a well-rounded investment portfolio that aligns with your risk tolerance and financial objectives. Let’s dive deeper into the world of investing and find out how to strike the perfect balance between high-risk and low-risk investments.

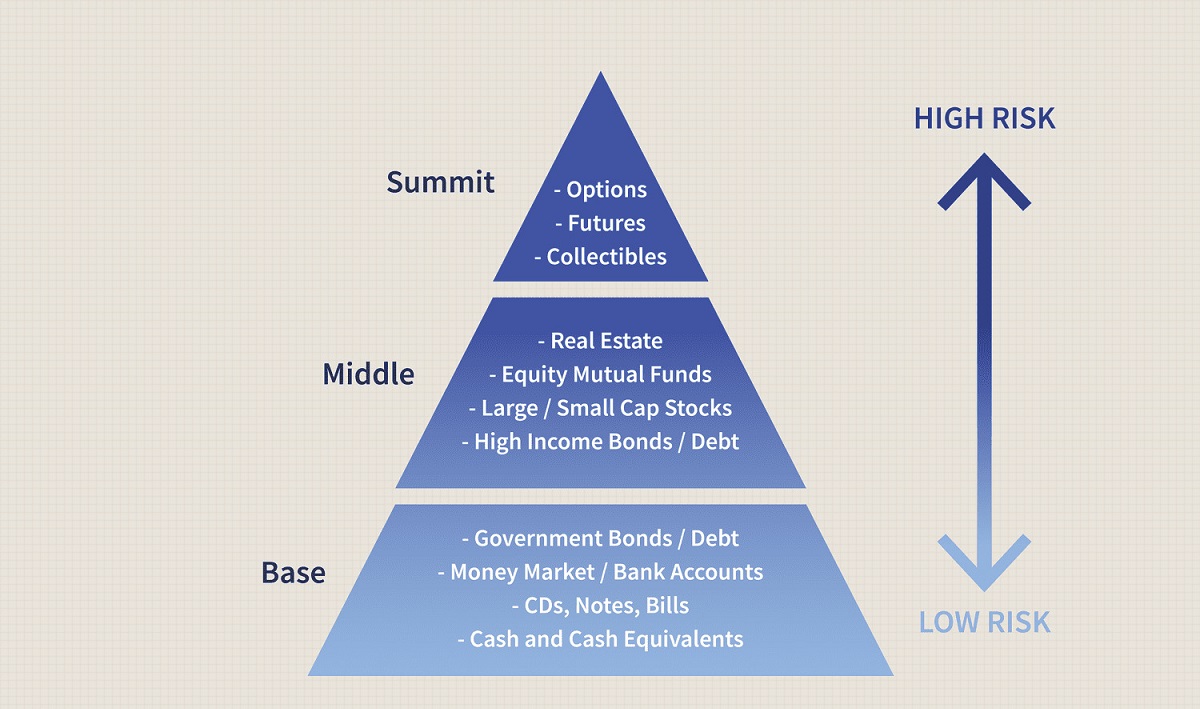

What are High-Risk and Low-Risk Investments?

When it comes to investing, understanding the concept of risk is paramount. High-risk investments are those that have a greater potential for both significant gains and substantial losses. These types of investments often involve higher volatility, uncertainty, and a greater degree of speculation. Examples of high-risk investments include individual stocks of growing companies, initial public offerings (IPOs), and investments in start-up ventures.

On the other hand, low-risk investments are characterized by their relative stability and consistency. They have a lower potential for significant gains but also a lower potential for losses. Low-risk investments are typically considered safe havens for preserving capital and generating modest returns. Common examples of low-risk investments include government bonds, treasury bills, and money market funds.

It’s important to note that not all investments can be neatly classified as high-risk or low-risk. Many investments lie along a spectrum, with varying degrees of risk and potential reward. For example, a blue-chip stock of a well-established company may be regarded as a medium-risk investment, offering a balance of stability and growth.

Investors choose high-risk investments to pursue potentially high returns and capitalize on market opportunities. However, these investments come with a higher likelihood of volatility and potential losses. Therefore, they are more suitable for individuals with a higher risk tolerance and a longer investment horizon.

On the other hand, low-risk investments provide a higher level of security and stability. These investments appeal to conservative investors who prioritize capital preservation and a steady income. Low-risk investments are often favored by those with a lower risk tolerance and a shorter investment timeline.

It’s important to understand that risk and return are inherently linked in investing. Generally, higher returns are associated with higher risks, while lower risks come with lower potential returns. As an investor, it’s crucial to find the right balance between risk and reward that aligns with your financial goals, risk tolerance, and time horizon.

Now that we have a better understanding of high-risk and low-risk investments, let’s explore how to determine your risk tolerance and effectively balance these types of investments.

Understanding Your Risk Tolerance

One of the most critical factors in maintaining a balanced investment portfolio is understanding your risk tolerance. Risk tolerance refers to your ability and willingness to endure fluctuations in the value of your investments. It is influenced by various factors, including your financial goals, time horizon, personal circumstances, and emotional capacity to handle market volatility.

To determine your risk tolerance, it’s essential to evaluate your financial goals. Are you investing for long-term growth or short-term gains? Are you saving for retirement, a down payment on a house, or a child’s education? Understanding your goals will help you gauge the level of risk you can afford to take. For example, if you have a long time horizon, you may have a higher risk tolerance as there is more time to recover from market downturns.

Another critical aspect to consider is your personal circumstances. Factors such as income stability, financial obligations, and dependents can impact your risk tolerance. If you have a secure income and minimal financial obligations, you may be more comfortable taking on higher risk. Conversely, if you have significant financial responsibilities or dependents, you may lean towards a more conservative, low-risk approach.

Emotional capacity plays a vital role in risk tolerance as well. How would you react to fluctuations in the value of your investments? Are you comfortable with the prospect of significant losses? Emotional resilience is crucial in maintaining a disciplined investment approach and avoiding impulsive decisions during market volatility.

An effective way to understand your risk tolerance is by taking a risk assessment questionnaire. Many financial institutions and online platforms offer these assessments, which help you identify your comfort level with different investment scenarios. They ask questions related to your financial situation, investment knowledge, and attitude towards risk. Based on the results, you can gauge your risk tolerance and make informed investment decisions.

Keep in mind that risk tolerance is not a fixed attribute but can change over time. As your financial situation, goals, and personal circumstances evolve, so may your risk tolerance. It’s important to periodically reassess and adjust your risk tolerance to ensure that your investment strategy remains aligned with your current needs and comfort level.

By understanding your risk tolerance, you can determine the appropriate mix of high-risk and low-risk investments that suits your goals and comfort level. In the next section, we will explore how diversification plays a crucial role in maintaining a balanced investment portfolio.

Diversification: The Key to Balancing High-Risk and Low-Risk Investments

When it comes to maintaining a balanced investment portfolio, diversification is a crucial strategy. Diversification involves spreading your investments across different asset classes, industries, and geographic regions. By doing so, you reduce the risk associated with any individual investment and increase the potential for consistent returns.

The primary benefit of diversification is that it helps to mitigate the impact of market volatility and specific company or industry risks. If one investment in your portfolio experiences a decline in value, the overall impact on your portfolio will be reduced if you have a diversified mix of investments. This can help protect your portfolio from significant losses during turbulent market conditions.

One way to achieve diversification is by investing across different asset classes, such as stocks, bonds, real estate, and commodities. Each asset class has unique characteristics and responds differently to economic and market conditions. Therefore, by allocating your investments across different asset classes, you can potentially benefit from the performance of one asset class, even if another asset class is underperforming.

Furthermore, diversification is essential within each asset class as well. For example, within stocks, you should consider investing in companies from various industries and sectors. This helps to balance the impact of any industry-specific risks. By doing so, even if a particular industry is experiencing a downturn or facing challenges, the performance of your entire portfolio won’t be overly affected.

Geographic diversification is another crucial element of a well-diversified portfolio. By investing in different countries and regions, you reduce the risk associated with any specific market. Economic and geopolitical factors can have varying impacts on different regions, so having exposure to multiple regions can help spread risk and potentially capture opportunities in different markets.

While diversification can significantly reduce risk, it’s important to note that it does not guarantee profit or shield against all losses. It is not possible to eliminate all investment risk through diversification, but it is a helpful strategy for managing risk.

Regularly reviewing and rebalancing your portfolio is necessary to maintain diversification. As the value of investments fluctuates, the allocation of your portfolio may change. This can lead to an imbalance and potentially higher risk. Rebalancing involves selling some investments and reinvesting in others to bring the portfolio back to its target allocation. It’s generally recommended to review your portfolio at least annually or when your financial goals, risk tolerance, or market conditions change.

In summary, diversification is the key to balancing high-risk and low-risk investments. By spreading your investments across different asset classes, industries, and regions, you can mitigate risk and increase the potential for consistent returns. However, diversification should be regularly monitored and adjusted to ensure its effectiveness in managing risk and achieving your investment goals.

Determining the Right Mix of High-Risk and Low-Risk Investments

When it comes to investment portfolio construction, finding the right mix of high-risk and low-risk investments is crucial. This mix will depend on factors such as your risk tolerance, financial goals, time horizon, and market conditions. It requires careful consideration and a well-thought-out strategy tailored to your unique circumstances.

One common approach to determining the right mix is the age-based rule of thumb. It suggests that younger investors with a longer time horizon can afford to take on more risk and allocate a higher percentage of their portfolio to high-risk investments, such as stocks. As investors get closer to retirement, they may opt for a more conservative approach and increase their allocation to low-risk investments, such as bonds.

Another approach is the risk-based approach, which involves assessing your risk tolerance and aligning your portfolio accordingly. If you have a higher risk tolerance, you may allocate a larger portion of your portfolio to high-risk investments to pursue higher potential returns. On the other hand, if you have a lower risk tolerance, you may opt for a more conservative allocation with a higher percentage of low-risk investments.

It’s important to note that diversification plays a significant role in determining the right mix of high-risk and low-risk investments. By diversifying your portfolio across various asset classes, industries, and regions, you can mitigate risk and enhance potential returns. The specific allocation will depend on your risk tolerance and the level of diversification you aim to achieve.

Evaluating market conditions is also essential in determining the right mix. During periods of economic expansion and bullish markets, investors may consider allocating a higher percentage to high-risk investments to take advantage of potential growth. Conversely, during economic downturns and bearish markets, investors may lean towards a more conservative allocation with a higher percentage of low-risk investments.

Seeking professional advice from a financial advisor can be immensely helpful in determining the right mix of investments. A financial advisor can assess your risk profile, understand your goals, and provide recommendations tailored to your specific needs. They can also provide valuable insights into market trends, economic factors, and investment opportunities that may impact your portfolio.

It’s crucial to remember that there is no one-size-fits-all approach to determining the right mix of high-risk and low-risk investments. It’s a highly individualized decision that requires continuous monitoring and adjustment as your goals and circumstances evolve. Regularly reviewing your portfolio and assessing its performance against your objectives will allow you to make informed decisions and ensure that your investment strategy remains aligned with your financial goals.

In the next section, we will explore the importance of monitoring and reviewing your investment portfolio to maintain the desired balance between high-risk and low-risk investments.

Monitoring and Reviewing Your Investment Portfolio

Monitoring and regularly reviewing your investment portfolio is a critical step in maintaining the desired balance between high-risk and low-risk investments. By staying informed and proactive, you can make necessary adjustments and ensure that your portfolio continues to align with your financial goals and risk tolerance.

The frequency of monitoring your portfolio will depend on your personal preference and the level of involvement you have in managing your investments. Some investors prefer to review their portfolio on a quarterly basis, while others may choose to do so on a monthly or even more frequent basis.

During the monitoring process, it’s essential to assess the performance of individual investments and the overall performance of your portfolio. Analyze how each investment is contributing to your financial goals and whether they are meeting your expectations. Consider factors such as returns, volatility, and how well they align with your risk tolerance.

It’s also crucial to review the asset allocation of your portfolio. Over time, market conditions and the performance of different asset classes can cause the allocation to deviate from your target. Rebalancing your portfolio involves adjusting the allocation by buying or selling investments to bring it back in line with your desired mix of high-risk and low-risk investments.

As part of the monitoring process, it’s essential to stay informed about market trends, economic factors, and other external variables that can impact your investments. Keep track of news and developments that are relevant to the companies or industries in which you have invested. This information can help you make informed decisions and identify potential risks or opportunities.

Online tools and portfolio tracking platforms can be valuable resources for monitoring and reviewing your portfolio. These tools provide real-time updates on the performance of your investments, asset allocation, and other relevant metrics. Additionally, some platforms offer features such as alerts and customizable reports to help you stay on top of your portfolio’s progress.

During the review process, it’s crucial to reassess your financial goals and risk tolerance. As life circumstances and goals change, your investment strategy may need adjustment. Regularly evaluate your goals to ensure that they are realistic and achievable. If your risk tolerance has changed or your investment timeline has shifted, make the necessary adjustments to your portfolio to reflect these changes.

Lastly, seek professional advice when needed. A financial advisor can provide valuable insights, guidance, and expertise to help you make informed decisions about your investment portfolio. They can offer an objective perspective, help you navigate complex investment strategies, and assist in mitigating potential risks.

By actively monitoring and reviewing your investment portfolio, you can maintain the desired balance between high-risk and low-risk investments. This enables you to make informed decisions, adjust your strategy as needed, and stay on track towards achieving your financial goals.

Staying Informed: Keeping Up with Market Trends and Economic Factors

To effectively manage your investment portfolio and maintain a balance between high-risk and low-risk investments, staying informed about market trends and economic factors is essential. Market dynamics and economic conditions can significantly impact the performance of your investments, and being aware of these factors allows you to make more informed decisions.

One important aspect of staying informed is keeping up with market trends. This involves monitoring the performance of different asset classes, industries, and individual companies. By analyzing trends, you can identify sectors that are experiencing growth or decline, and adjust your portfolio accordingly. For example, if a particular industry is booming, you may consider allocating more of your investments to stocks or funds in that sector.

Regularly reading financial news, following trusted financial websites or publications, and subscribing to newsletters or market updates can help you stay informed about market trends. Additionally, participating in investment forums or joining investment clubs can provide valuable insights and perspectives from other investors.

Monitoring economic factors is also crucial for making informed investment decisions. Economic indicators such as GDP growth, inflation rates, interest rates, and employment data can provide valuable insights into the overall health of the economy and its potential impact on different asset classes. For example, during times of high inflation, investing in assets such as real estate or commodities that tend to perform well in inflationary environments may be more favorable.

Government policies and regulations also play a significant role in shaping the investment landscape. Changes in tax laws, fiscal policies, and monetary policies can impact various sectors and asset classes. Staying informed about these policy changes can help you anticipate their potential impact on your investments and make adjustments accordingly.

In today’s digital age, technology has made it easier than ever to stay informed. There are various financial news apps, websites, and social media platforms that provide real-time updates and analysis. Utilize these resources to stay up to date with the latest market news, investment insights, and economic developments.

While it’s essential to stay informed, it’s equally important to exercise caution and avoid getting caught up in short-term market fluctuations or speculative trends. Remember to base your decisions on a solid understanding of the long-term fundamentals of the investments you hold and your own financial goals.

Lastly, remember that staying informed is an ongoing process. The investment landscape is constantly evolving, and keeping up with the latest developments is crucial to making informed investment decisions. Regularly dedicating time to read, research, and stay updated will help you navigate market volatility, identify emerging trends, and adjust your investment strategy accordingly.

By staying informed about market trends and economic factors, you can make better-informed investment decisions and maintain a balanced portfolio that aligns with your financial goals and risk tolerance.

Seeking Professional Advice: When and Why?

Seeking professional advice from a financial advisor can be invaluable when it comes to managing your investment portfolio and maintaining a balance between high-risk and low-risk investments. Financial advisors possess expertise, experience, and knowledge that can help you make informed decisions and navigate the complexities of the financial markets.

There are several instances when it may be beneficial to seek professional advice:

1. Lack of knowledge or experience: If you are new to investing or lack confidence in your investment knowledge, seeking advice from a financial advisor can provide you with the guidance and education you need. They can help you understand investment options, assess your risk tolerance, and develop a tailored investment plan that aligns with your goals.

2. Complex financial situation: If you have a complex financial situation, such as significant assets, multiple income streams, or unique tax considerations, a financial advisor can help you navigate these complexities. They can help you optimize your investments, minimize taxes, and ensure that your overall financial plan is well-coordinated.

3. Life transitions: Major life events, such as starting a family, changing careers, or nearing retirement, often require adjustments to your investment strategy. Seeking professional advice during these transitions can help you make suitable changes to your portfolio, align it with your new financial goals, and ensure that you are on track towards achieving them.

4. Market uncertainty or volatility: During periods of market uncertainty or volatility, it can be challenging to make rational investment decisions based on emotions alone. A financial advisor can provide a calm, objective perspective and help you navigate through turbulent times. They can help you make rational decisions, stay focused on your long-term goals, and avoid knee-jerk reactions to short-term market fluctuations.

5. Portfolio diversification and rebalancing: Maintaining a well-diversified portfolio is crucial for managing risk. A financial advisor can assist you in assessing your portfolio’s diversification and recommend adjustments to ensure a balanced mix of high-risk and low-risk investments. They can also help with the periodic rebalancing of your portfolio to keep it aligned with your long-term objectives.

6. Planning for retirement: As retirement approaches, seeking professional advice becomes even more important. A financial advisor can help you determine your retirement income needs, assess your current savings, and develop a comprehensive retirement plan. They can guide you on investment options, withdrawal strategies, and help ensure that your retirement income supports your desired lifestyle.

Remember that financial advisors can provide guidance tailored to your specific needs and circumstances. They can offer objective advice, access to professional research, and help you make well-informed decisions about your investments. However, it’s crucial to choose a reputable and qualified financial advisor who has your best interests at heart.

While seeking professional advice comes at a cost, the potential benefits of their expertise and guidance can outweigh the fees associated with their services. Ultimately, the decision to seek professional advice should depend on your comfort level, financial situation, and the complexity of your investment needs.

By seeking professional advice when needed, you can gain peace of mind knowing that you are making informed decisions and have an expert guiding you towards financial well-being.

Adjusting Your Investment Strategy as Your Goals Change

Your financial goals are not static; they can evolve over time due to changes in your personal circumstances, priorities, and aspirations. As your goals change, it is important to adjust your investment strategy accordingly to ensure that your portfolio continues to align with your new objectives.

One common scenario in which adjustments to your investment strategy may be necessary is when your time horizon shifts. For example, if you originally invested with a long-term goal of retirement, but now have a shorter time horizon due to unexpected circumstances, it may be necessary to adjust your portfolio to reduce risk and prioritize capital preservation.

Similarly, as your goals become more focused or specific, your investment strategy may need to be refined. For instance, if you have a goal of purchasing a home in the near future, you may need to shift your investments towards low-risk assets to protect the capital you have saved for the down payment.

Life events such as getting married, having children, or starting a business can also prompt adjustments to your investment strategy. These events often come with new financial responsibilities and may require reallocating funds to secure your family’s future or invest in your business’s growth.

Financial market conditions can also trigger the need for adjustments. During periods of economic uncertainty or market volatility, you may find it necessary to reassess your risk tolerance and make changes to your portfolio allocation. This ensures that your investments remain in line with your comfort level and long-term financial goals.

Regularly reviewing your portfolio performance against your goals is crucial for identifying any necessary adjustments. Assess how your investments are performing, compare them to relevant benchmarks, and determine if they are on track to meet your objectives. If adjustments are needed, consider consulting a financial advisor to help guide you through the process.

Rebalancing your portfolio is an important aspect of adjusting your investment strategy. Over time, certain assets may outperform others, causing your portfolio to deviate from your original asset allocation. Rebalancing involves selling some investments and reinvesting in others to bring your portfolio back to your target allocation. This helps maintain a desired balance between high-risk and low-risk investments.

Lastly, education and staying informed about investment options is crucial in adjusting your investment strategy. As your goals change, you may need to explore different investment vehicles or asset classes that align better with your new objectives. Stay up to date with industry trends, emerging investment opportunities, and changes in regulations or tax laws that may impact your investment choices.

Remember that adjusting your investment strategy requires careful consideration and assessment of your changing circumstances and goals. Consult with a financial advisor to gain professional insights and guidance tailored to your specific situation. By proactively adjusting your investment strategy, you can ensure that your portfolio remains aligned with your evolving goals and increases the likelihood of achieving long-term financial success.

Conclusion

Maintaining a balance between high-risk and low-risk investments is a critical aspect of successful portfolio management. By understanding your risk tolerance, diversifying your investments, and regularly monitoring and reviewing your portfolio, you can effectively achieve this balance. Additionally, seeking professional advice when needed and adjusting your investment strategy as your goals change are key elements to ensure your investments align with your evolving needs.

High-risk investments offer the potential for significant returns but come with a higher possibility of losses. Low-risk investments provide stability and security but offer lower potential returns. Understanding your risk tolerance is crucial in determining the right mix of high-risk and low-risk investments. It is influenced by your financial goals, time horizon, personal circumstances, and emotional capacity to handle market volatility.

Diversification is the key strategy for balancing high-risk and low-risk investments. By spreading your investments across different asset classes, industries, and regions, you can mitigate risk and increase the potential for consistent returns. Regularly monitoring and reviewing your portfolio allow you to assess performance, maintain diversification, and make necessary adjustments based on market trends and economic factors.

Seeking professional advice can provide valuable insights and guidance in managing your investments. Financial advisors can help assess your risk profile, develop tailored investment plans, and provide objective perspectives during market volatility. Additionally, adjusting your investment strategy as your goals change ensures that your portfolio remains aligned with your objectives and enhances the likelihood of achieving financial success.

In conclusion, maintaining a balance between high-risk and low-risk investments requires ongoing attention and evaluation. It is a dynamic process that demands continuous monitoring, regular review, and potential adjustments. By implementing these strategies and remaining proactive in managing your investments, you can navigate the ever-changing investment landscape and work towards achieving your financial goals.