Introduction

Venmo has become an incredibly popular payment app, allowing users to easily send and receive money with just a few taps on their smartphones. Whether it’s splitting the bill at a restaurant, reimbursing a friend for a favor, or paying rent to a roommate, Venmo has simplified the world of electronic transactions. However, with the rise in usage of this app, many users are starting to wonder about the tax implications of using Venmo.

In this article, we will delve into the topic of taxation and Venmo. We will explore how Venmo works, when you might or might not get taxed on Venmo transactions, and the responsibilities that Venmo users have when it comes to reporting their transactions to the appropriate tax authorities.

Understanding the taxation rules surrounding digital payment platforms like Venmo is essential in order to avoid any potential issues with the IRS or other tax authorities. While Venmo itself does not directly deduct taxes from transactions, individuals are still responsible for reporting their income accurately and paying the appropriate taxes.

So, let’s dive into the world of Venmo and taxes to gain a better understanding of how it all works.

Understanding Venmo

Venmo is a popular peer-to-peer payment platform that allows users to easily send and receive money from their mobile devices. It was founded in 2009 and has since gained widespread adoption, particularly among younger generations who are looking for a convenient and cashless way to handle financial transactions.

When someone creates a Venmo account, they can link it to their bank account, credit card, or debit card to fund their transactions. This allows users to easily transfer money between friends, family members, or even businesses, without the need for physical cash or checks.

Venmo also offers a social aspect, allowing users to see and interact with their friends’ transactions. Users can add comments or emojis to their payments, making it a more personalized and engaging experience. It’s this social element that sets Venmo apart from traditional payment methods and makes it a popular choice among millennials and Gen Z.

One important thing to note about Venmo is that it primarily acts as an intermediary between two parties. When a user sends money through Venmo, the funds are first taken from their payment source (bank account, credit card, or debit card) and held in a Venmo account. The recipient can then transfer the funds from their Venmo account to their linked payment source.

However, it’s crucial to remember that Venmo is not a bank. While Venmo does hold the funds temporarily, it is not responsible for any issues that may arise, such as disputes between users or unauthorized transactions. Venmo’s terms and conditions clearly state that users should only send money to people they know and trust.

Overall, Venmo provides a convenient and user-friendly platform for handling digital payments, making it a popular choice for individuals who want a simple and efficient way to exchange money. Understanding how Venmo works is the first step in understanding the tax implications that may arise when using this platform.

How Venmo Works

Venmo operates through a mobile application available for iOS and Android devices. To get started, users must create an account with their email address or through their Facebook profile. Once logged in, users can link their bank account, credit card, or debit card to their Venmo account as funding sources.

When a user wants to send money to someone, they simply need to enter the recipient’s Venmo username, email address, or phone number, along with the amount they wish to send. They can also add a note or an emoji to accompany the payment. The sender then confirms the transaction, and the recipient instantly receives a notification of the incoming payment.

Now, the money sent is initially taken from the sender’s linked funding source and held in the sender’s Venmo account. The recipient can decide to either keep the money in their Venmo account or transfer it to their linked funding source, such as their bank account. This transfer from the Venmo account to the funding source can take one to three business days, depending on the recipient’s bank.

It’s important to note that Venmo offers a social aspect, allowing users to see and interact with their friends’ transactions. The Venmo feed displays a list of transactions made by people in a user’s network, including the names of the sender and recipient, along with any comments or emojis that were included in the payment.

Venmo also provides additional features, such as the ability to split a bill among multiple people, create payment reminders, and make payments through authorized merchants both online and offline. These features make Venmo a versatile platform for a wide range of payment needs.

For security purposes, Venmo offers two-factor authentication, allowing users to set a PIN code, Face ID, or Touch ID to access their accounts. Venmo also has fraud prevention measures in place and provides customer support for any issues or concerns that may arise.

Overall, Venmo offers a simple and user-friendly way to send and receive money instantly. Its social features and additional functionalities distinguish it from other payment platforms and contribute to its growing popularity.

Venmo and Taxes

When it comes to Venmo and taxes, it’s important to understand that Venmo itself is not responsible for deducting taxes from the transactions made on its platform. However, as a Venmo user, you still have certain tax obligations that you need to be aware of.

The Internal Revenue Service (IRS) considers any money earned or received through Venmo as taxable income. This means that if you receive money through Venmo, whether it’s for goods sold or services rendered, it should be reported as income on your tax return.

Similarly, if you use Venmo for business purposes, such as receiving payments from clients or customers, you need to keep accurate records of these transactions and report the income accordingly on your tax return. Even if the amounts received through Venmo are relatively small, they are still subject to taxation.

On the other hand, if you use Venmo solely for personal purposes, such as splitting bills with friends or reimbursing each other for expenses, the money exchanged is generally not considered taxable income. This is because personal transactions, where no goods or services are provided, are typically not taxable.

However, there are some scenarios where you might still be subject to taxes, even for personal Venmo transactions. For example, if you receive a large gift of money from a friend or family member through Venmo, it could be considered a taxable gift, depending on the amount. Gifts above a certain threshold are subject to gift tax rules.

It’s also worth noting that if you receive interest on the money held in your Venmo account, that interest may be subject to taxes. Venmo partners with banks to offer users the option to transfer their Venmo balance to an eligible bank account. If interest is earned on that balance, it should be reported as income on your tax return.

Ultimately, it’s essential to keep thorough records of your Venmo transactions and consult with a tax professional to ensure that you are accurately reporting your income and fulfilling your tax obligations. Being proactive in understanding and complying with the tax rules related to Venmo can help you avoid any potential issues or penalties in the future.

When You Don’t Get Taxed on Venmo

While the IRS considers money received through Venmo as taxable income, there are certain scenarios where you may not be subject to taxes on Venmo transactions.

Firstly, if you use Venmo for personal purposes and only engage in transactions that involve splitting bills with friends or reimbursing each other for expenses, you generally don’t have to worry about being taxed on these transactions. This is because personal transactions, where no goods or services are provided, aren’t typically considered taxable income.

For example, if you and your friends go out for dinner and one person pays the bill using Venmo, and others reimburse that person through Venmo, these transactions are considered personal and non-taxable. Similarly, if you lend money to a friend and they pay you back through Venmo, it is also considered a non-taxable transaction as it is simply reimbursement of a personal loan.

Additionally, if you occasionally receive small amounts of money from friends or family members as a gift through Venmo, it may not be subject to taxes. The IRS allows for a gift tax exclusion, which means that gifts below a certain threshold (currently $15,000 per person per year) are not taxable. However, it’s important to note that if the gift exceeds this threshold, you may need to report it and potentially pay gift taxes.

It’s worth mentioning that if you receive money through Venmo for selling personal belongings or used items at a price lower than their original value, these transactions may still be considered personal and non-taxable. However, if you regularly engage in selling items at a profit or operate a business through Venmo, you may need to report the income as self-employment income or business income.

It’s essential to keep in mind that tax laws can be complex, and the IRS may have specific rules and regulations that apply to your individual situation. Therefore, it’s always recommended to consult a tax professional or seek guidance from the IRS to ensure that you are accurately reporting your income and complying with tax laws.

When You Do Get Taxed on Venmo

While there are certain scenarios where you may not be subject to taxes on Venmo transactions, there are also situations where you do need to consider the tax implications.

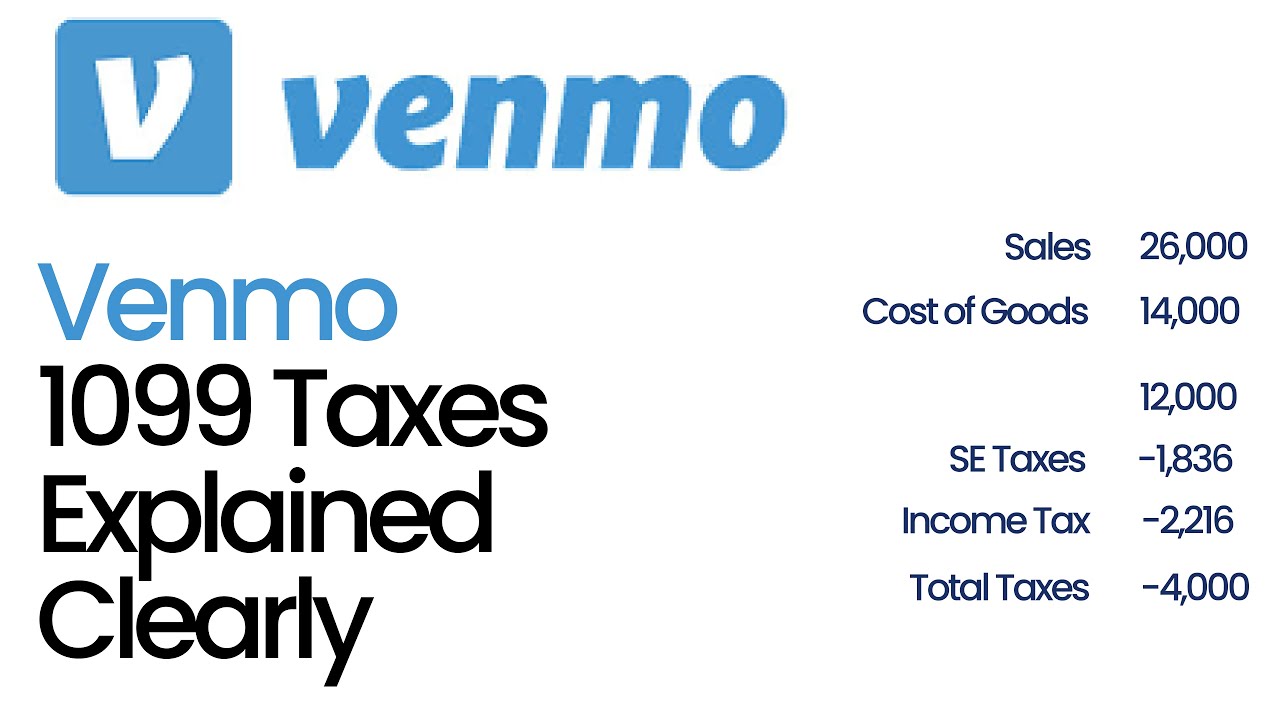

If you use Venmo for business purposes, such as receiving payments from clients or customers, the money you receive through these transactions is considered taxable income. It’s important to keep accurate records of these transactions and report the income on your tax return. Whether you provide services or sell goods, the money earned through Venmo should be treated as business income and reported accordingly.

Even if you use Venmo for personal reasons but frequently engage in activities that generate income, such as selling goods or providing services, you may still be subject to taxes. For instance, if you use Venmo to sell handmade crafts, offer freelance services, or provide any form of consulting, the income generated from these activities should be reported as self-employment income.

It’s worth noting that even personal Venmo transactions may be subject to taxes if they involve larger gifts. While smaller gifts from friends or family members are generally not taxable, the IRS imposes gift tax rules on larger gifts. If you receive a considerable amount of money through Venmo as a gift, it’s essential to consult with a tax professional to determine if you need to report and potentially pay gift taxes.

Another aspect to consider for potential taxation on Venmo is interest earned on the money held in your Venmo account. Venmo offers the option to transfer balances to an eligible bank account, and if interest is earned on that balance, it must be reported as income on your tax return. The interest earned may be minimal, but it’s still important to accurately report it.

It is crucial to remember that tax laws can be complex, and the implications of Venmo transactions may vary based on individual circumstances. To ensure compliance with tax regulations and accurately report your income, it is always advisable to consult with a tax professional or seek guidance from the IRS.

Reporting Venmo Transactions

Reporting Venmo transactions is an important part of fulfilling your tax obligations. While Venmo does not provide tax forms or directly report your transactions to the IRS, you are still responsible for accurately reporting your income from Venmo on your tax return.

When it comes to reporting Venmo transactions, it’s crucial to keep detailed records of your income and expenses. This includes maintaining records of payments received and sent through Venmo, whether they are personal or business-related. You should also keep track of any relevant supporting documents, such as receipts or invoices, to substantiate your transactions.

If you use Venmo for personal purposes and only engage in non-taxable transactions, there is generally no need to report these transactions on your tax return. However, it’s still a good practice to keep a record of these transactions for your own reference.

For those using Venmo for business purposes, it’s important to separate personal and business transactions. Keep a separate record of all business-related income and expenses made through Venmo. You may also consider using accounting software or working with a tax professional to ensure accurate tracking and reporting of your business finances.

When it comes to reporting Venmo income on your tax return, consult the appropriate tax forms based on your filing status and business structure. For example, if you are self-employed and use Venmo for business purposes, you may need to file Schedule C (Form 1040) as part of your individual tax return to report business income and expenses.

It’s important to note that the IRS expects accurate reporting of all income, including income from digital payment platforms like Venmo. Failure to report income properly can result in penalties and potential audits. Therefore, it is crucial to take the time to review tax regulations and consult with a tax professional to ensure compliance with reporting requirements.

Lastly, it’s worth mentioning that tax laws and reporting requirements can vary from country to country. If you reside outside of the United States, be sure to consult the relevant tax authorities to understand the reporting obligations for Venmo transactions in your specific jurisdiction.

Tax Implications for Venmo Users

Venmo, like other digital payment platforms, comes with certain tax implications that users must be aware of. Understanding these tax implications is crucial for accurately reporting income and fulfilling tax obligations. Here are some key tax considerations for Venmo users:

1. Taxable Income: Money received through Venmo, whether for personal or business purposes, is generally considered taxable income by the IRS. It’s important to keep thorough records of all transactions and report the income on your tax return accordingly.

2. Business Use: If you use Venmo for business purposes, such as receiving payments from clients or customers, you need to separate your personal and business transactions. Record and report business-related income and expenses separately to ensure accurate reporting and to take advantage of any applicable deductions.

3. Self-Employment Taxes: For individuals who use Venmo for business purposes, such as freelancers or independent contractors, they may be subject to self-employment taxes. Self-employment taxes include both the employer and employee portions of Social Security and Medicare taxes. Keep track of your business income from Venmo and consult with a tax professional to determine your self-employment tax obligations.

4. Deductions: If you use Venmo for business purposes, you may be eligible to deduct certain business-related expenses. This can include expenses like supplies, transportation, or professional fees. Keep detailed records of these expenses and consult with a tax professional to determine which deductions you may be eligible for.

5. Gift Taxes: While personal transactions on Venmo are generally not taxable, larger gifts received through Venmo may be subject to gift taxes. If you receive a substantial gift from a friend or family member, consult with a tax professional to understand the gift tax rules and potential reporting requirements.

6. Interest Income: If you transfer your Venmo balance to an eligible bank account and earn interest on that balance, the interest income is taxable and should be reported on your tax return. Be sure to keep track of any interest earned and report it accurately.

It’s important to remember that tax laws can be complex, and they may vary depending on your individual circumstances and jurisdiction. To ensure compliance and accurate reporting, consider working with a tax professional who can provide guidance tailored to your specific situation.

Conclusion

As the popularity of Venmo continues to rise, it’s important for users to understand the tax implications that come with using the platform. While Venmo itself does not directly deduct taxes from transactions, individuals are still responsible for accurately reporting their income and fulfilling their tax obligations.

When using Venmo, it’s crucial to distinguish between personal and business transactions and keep thorough records of all transactions, including payments received and sent. Personal transactions, such as splitting bills with friends or reimbursing expenses, are generally not taxable. However, if you use Venmo for business purposes or frequently engage in activities that generate income, you may be subject to taxation and should report the income accordingly on your tax return.

Additionally, larger gifts received through Venmo may be subject to gift taxes, and interest earned on Venmo balances transferred to a bank account should be reported as income. It’s important to understand and comply with the specific tax rules and regulations in your jurisdiction to avoid any potential issues or penalties in the future.

Consulting with a tax professional can provide valuable guidance in navigating the tax implications of using Venmo and ensuring accurate reporting of income. They can help you understand your individual tax obligations, identify any deductions or credits you may be eligible for, and assist in maintaining proper records.

Keeping up-to-date with tax regulations and fulfilling your tax obligations is essential for financial wellness and avoiding any potential legal and financial consequences. By being aware of the tax implications of using Venmo and taking the necessary steps to comply with tax laws, you can enjoy the convenience and simplicity of the platform while staying in good standing with tax authorities.