Truth In Lending Disclosure: What is it?

The Truth In Lending Disclosure is a crucial document that provides vital information to borrowers when they take out a loan or enter into a credit agreement. It is a federally mandated document under the Truth In Lending Act (TILA), designed to protect borrowers by ensuring transparency and fairness in lending practices.

This disclosure provides borrowers with a clear and comprehensive overview of the terms and conditions of their loan, including the interest rate, annual percentage rate (APR), finance charges, and any additional fees or costs associated with the credit agreement. By disclosing this information, lenders enable borrowers to make informed decisions and compare loan offers from different lenders.

The Truth In Lending Disclosure is typically provided during the loan application process, allowing borrowers to review and understand the financial implications of the loan before committing to it. The information contained in the disclosure empowers borrowers to assess whether the loan fits within their budget and financial capabilities.

Moreover, the Truth In Lending Disclosure helps promote transparency and prevent predatory lending practices. By mandating lenders to disclose all pertinent details about the loan, borrowers are protected from hidden fees, excessive interest rates, and other unfair lending practices.

Overall, the Truth In Lending Disclosure serves as a vital tool in fostering a fair and transparent lending environment. It empowers borrowers by providing comprehensive information about the loan terms and ensuring they have the knowledge necessary to make informed financial decisions.

Understanding the Purpose of the Truth In Lending Disclosure

The purpose of the Truth In Lending Disclosure is to promote transparency and protect borrowers when they enter into a lending agreement. This disclosure provides borrowers with essential information about the terms of the loan, enabling them to make informed decisions and avoid financial pitfalls.

One of the primary purposes of the disclosure is to ensure that borrowers have a clear understanding of the cost of the loan. It includes details such as the interest rate, APR, and finance charges, which help borrowers assess the true cost of borrowing. This information allows borrowers to compare different loan offers and choose the most affordable and suitable option for their needs.

Another crucial purpose of the Truth In Lending Disclosure is to prevent deceptive practices in lending. By requiring lenders to disclose all fees, charges, and other costs associated with the loan, borrowers are protected from hidden or unexpected expenses. This promotes fairness in lending and helps borrowers avoid entering into unfavorable loan agreements.

The disclosure also serves as a tool for promoting consumer education. By providing borrowers with clear and concise information about their loan, the disclosure helps increase financial literacy. Borrowers can gain a better understanding of the loan terms, including repayment schedules, late payment penalties, and any potential risks associated with the loan.

Furthermore, the Truth In Lending Disclosure is instrumental in safeguarding borrowers from predatory lending practices. The disclosure requirements ensure that lenders provide honest and accurate information, preventing them from taking advantage of borrowers’ lack of information or financial vulnerability.

Overall, the purpose of the Truth In Lending Disclosure is to level the playing field between lenders and borrowers by ensuring transparency and empowering borrowers with the necessary information to make informed financial decisions. By understanding the terms and costs of the loan, borrowers have the opportunity to secure loans that are fair, affordable, and aligned with their financial goals.

Key Elements of the Truth In Lending Disclosure

The Truth In Lending Disclosure consists of several key elements that provide borrowers with important information about the terms and costs of their loan. These elements include:

- Loan Amount: This indicates the total amount of money that the borrower is borrowing from the lender. It is important for borrowers to review this amount carefully to ensure it aligns with their needs.

- Interest Rate: The interest rate is the percentage of the loan amount that the borrower will be charged as interest over the life of the loan. It is essential for borrowers to understand the interest rate as it directly impacts the total cost of the loan.

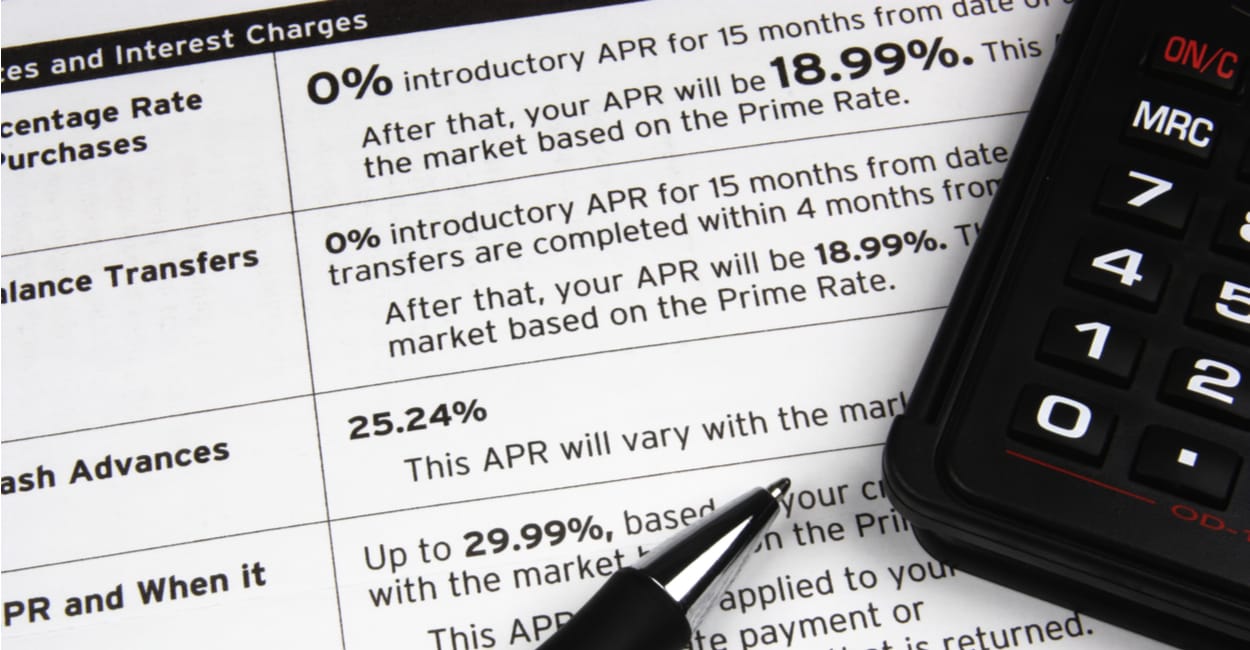

- Annual Percentage Rate (APR): The APR represents the annual cost of the loan, including both the interest rate and any additional fees or charges associated with borrowing. It allows borrowers to compare the cost of different loan offers accurately.

- Finance Charges: This includes any fees or costs that the borrower will incur over the life of the loan. It is crucial for borrowers to review these charges carefully to understand the total cost of the loan.

- Loan Terms: The loan terms specify the duration of the loan, including the repayment schedule, due dates, and the number of payments required to pay off the loan. Borrowers should pay close attention to these terms to ensure they can meet their loan obligations.

- Prepayment Penalties: Some loans may include prepayment penalties, which are fees charged if the borrower pays off the loan before the agreed-upon term. Borrowers should be aware of these penalties and consider them when assessing the loan’s overall cost.

- Late Payment Fees: The disclosure may also include information about any fees charged in the event of late payments. Borrowers should understand these fees to avoid unnecessary costs and penalties.

- Total Amount Repaid: This element outlines the total amount that the borrower will repay over the course of the loan, including the principal amount borrowed, interest, and any additional charges.

These key elements are essential for borrowers to understand fully. Reviewing and comprehending these elements will enable borrowers to make informed decisions and choose a loan that aligns with their financial goals and capabilities.

How to Read and Interpret the Truth In Lending Disclosure

Reading and interpreting the Truth In Lending Disclosure is essential for borrowers to understand the terms and costs of their loan fully. Here are some steps to follow when reviewing this important document:

- Read the document carefully: Start by thoroughly reading the entire Truth In Lending Disclosure. Pay close attention to each section and make sure you understand the information provided.

- Identify the key elements: Look for the key elements discussed earlier, including the loan amount, interest rate, APR, finance charges, loan terms, and any additional fees or penalties.

- Understand the total cost: Calculate the total amount you will repay over the life of the loan by adding the principal amount, interest, and any applicable fees. This will give you a clear idea of the overall cost of the loan.

- Review the repayment schedule: Examine the loan terms and repayment schedule to understand the duration of the loan, the number of payments required, and the due dates. Make sure you can comfortably meet these obligations.

- Consider the APR: The APR represents the true cost of borrowing, including both the interest rate and fees. Compare the APRs of different loan offers to determine which one is the most affordable and suitable for your needs.

- Check for prepayment penalties or late payment fees: Look for any potential penalties or fees that you may incur if you pay off the loan early or make late payments. Consider these charges in your decision-making process.

- Ask questions: If you come across any unclear or confusing information, don’t hesitate to ask the lender for clarification. It’s crucial to fully understand the terms and conditions of the loan before proceeding.

- Seek professional advice if necessary: If you’re unsure about certain aspects of the loan or feel overwhelmed by the information in the disclosure, consider consulting a financial advisor or loan expert who can provide additional guidance.

By following these steps, borrowers can read and interpret the Truth In Lending Disclosure effectively. Understanding the terms, costs, and obligations of the loan will empower borrowers to make informed decisions and choose a loan that aligns with their financial goals.

Importance of the Truth In Lending Disclosure for Borrowers

The Truth In Lending Disclosure holds great significance for borrowers as it provides crucial information that empowers them to make informed financial decisions. Here are key reasons why this disclosure is essential:

- Transparency: The disclosure promotes transparency by requiring lenders to provide comprehensive and accurate information about the loan terms and costs. It enables borrowers to have a clear understanding of what they are agreeing to and what they can expect throughout the loan’s duration.

- Informed Decision-Making: By disclosing important details such as the interest rate, APR, finance charges, and any additional fees, the disclosure enables borrowers to compare loan offers and choose the most suitable one for their needs. It empowers borrowers to make informed decisions based on their budget and financial capabilities.

- Protection Against Deceptive Practices: The Truth In Lending Disclosure serves as a safeguard against deceptive lending practices. It ensures that borrowers are aware of all costs associated with the loan, preventing hidden fees or unfair terms that could harm borrowers financially.

- Preventing Overburdening Debt: The disclosure allows borrowers to assess the affordability of the loan, taking into account their income and expenses. It helps borrowers avoid taking on excessive debt that could lead to financial strain or inability to make timely repayments.

- Promoting Financial Literacy: Understanding the information provided in the Truth In Lending Disclosure helps improve borrowers’ financial literacy. It empowers them to comprehend complex financial concepts, such as APR and finance charges, and apply that knowledge to make better financial choices in the future.

- Fostering Consumer Protection: The disclosure requirements established by the Truth In Lending Act ensure that borrowers are protected from predatory lending practices. By mandating lenders to provide transparent information, borrowers are shielded from unscrupulous lenders who may take advantage of their lack of knowledge or financial vulnerability.

- Encouraging Accountability: By providing borrowers with a written record of the agreed-upon loan terms and costs, the Truth In Lending Disclosure holds lenders accountable for delivering what was promised during the loan application process. It provides a reference point in case of any disputes or discrepancies.

The importance of the Truth In Lending Disclosure cannot be overstated. It plays a vital role in ensuring fairness, transparency, and consumer protection in the lending industry. By arming borrowers with the necessary information, it enables them to make responsible financial decisions and safeguards them from potential harm.

Legal Requirements for Truth In Lending Disclosure

The Truth In Lending Act (TILA) imposes legal requirements on lenders regarding the Truth In Lending Disclosure. These requirements are in place to protect borrowers and ensure that they have access to transparent and accurate information about the terms and costs of their loan. Here are the key legal requirements for the Truth In Lending Disclosure:

- Mandatory Disclosure: The TILA mandates that lenders provide borrowers with a written disclosure of the key terms and costs of the loan. This disclosure must be provided before the borrower is legally bound to the loan or pays any fees, allowing borrowers to review and understand the terms before entering into the agreement.

- Specific Information: The Truth In Lending Disclosure must include specific information, such as the loan amount, finance charge, annual percentage rate (APR), payment schedule, and total repayment amount. This ensures that borrowers have a clear understanding of the loan terms and costs.

- Uniform Format: The TILA requires that the Truth In Lending Disclosure be presented in a uniform format, making it easier for borrowers to compare loan offers from different lenders. This standardized format allows borrowers to quickly identify and comprehend the pertinent information.

- Clear and Conspicuous: The disclosure must be presented in a clear and conspicuous manner, making it easily readable and understandable for borrowers. The font size, formatting, and placement of the disclosure must be designed to ensure that borrowers can easily identify and comprehend the information presented.

- Timing of Disclosure: Lenders are required to provide the Truth In Lending Disclosure in a timely manner, allowing borrowers sufficient time to review and understand the terms before committing to the loan. Generally, the disclosure must be provided before the borrower becomes legally obligated to the loan.

- Accuracy of Information: Lenders are obligated to provide accurate and truthful information in the disclosure. Any errors or discrepancies must be promptly addressed and corrected to ensure that borrowers have access to reliable and precise information about their loan.

- Translations: In cases where borrowers do not understand English or are more comfortable reading in a different language, the TILA requires lenders to provide the Truth In Lending Disclosure in a language that the borrower understands. This ensures that all borrowers have access to the necessary information in a language they can comprehend.

Compliance with these legal requirements is essential for lenders to ensure they meet their obligations under the Truth In Lending Act. By adhering to these requirements, lenders help promote transparency, fairness, and consumer protection in the lending process.

Common Mistakes to Avoid when Reviewing Truth In Lending Disclosure

Reviewing the Truth In Lending Disclosure is a crucial step in understanding the terms and costs of a loan. However, there are several common mistakes that borrowers should avoid when reviewing this important document:

- Skipping or Rushing Through the Review: One of the most common mistakes is not taking the time to thoroughly review the disclosure. It is essential to read the document carefully and ensure that you understand all the terms and costs associated with the loan.

- Disregarding Additional Fees: Some borrowers make the mistake of focusing solely on the interest rate and APR, while ignoring additional fees and charges mentioned in the disclosure. It is vital to pay attention to these costs to have a comprehensive understanding of the total expense of the loan.

- Overlooking the Repayment Schedule: Ignoring the repayment schedule can lead to future problems. Ensure that you understand the number of payments, due dates, and any penalties for late payments. This will help you plan your finances and make timely repayments.

- Not Asking Questions: If something is unclear in the disclosure, don’t hesitate to ask the lender for clarification. It is better to resolve any doubts upfront rather than facing surprises or misunderstandings later on.

- Ignoring Prepayment Penalties: Some loans may have prepayment penalties if you choose to pay off the loan early. Be aware of these penalties and consider them if you anticipate the possibility of paying off the loan before the agreed term.

- Not Comparing Loan Offers: Another mistake is not comparing loan offers from different lenders. It is vital to review multiple loan options to find the most favorable terms and costs that meet your financial needs.

- Forgetting to Review Disclosures for All Borrowers: If you are entering into a joint loan with another person, ensure that all borrowers have reviewed the disclosure. Each borrower has the responsibility to understand the terms and costs of the loan.

- Not Seeking Professional Advice: If you find the disclosure overwhelming or have difficulty understanding certain aspects, consider seeking advice from a financial advisor or loan expert. Their expertise can help you navigate the disclosure and make an informed decision.

Avoiding these common mistakes when reviewing the Truth In Lending Disclosure is crucial for a borrower. By staying vigilant and taking the time to understand the terms and costs of the loan, you can make informed decisions and avoid potential financial pitfalls.

FAQs about Truth In Lending Disclosure

Here are some frequently asked questions about the Truth In Lending Disclosure:

- What is the purpose of the Truth In Lending Disclosure?

- When do I receive the Truth In Lending Disclosure?

- What information is included in the Truth In Lending Disclosure?

- Can I negotiate the terms and costs mentioned in the Truth In Lending Disclosure?

- What should I do if I find errors or discrepancies in the Truth In Lending Disclosure?

- Is the Truth In Lending Disclosure the same for all types of loans?

- Do I have to sign the Truth In Lending Disclosure?

- Can I request a copy of the Truth In Lending Disclosure?

The purpose of the Truth In Lending Disclosure is to ensure transparency in lending practices and provide borrowers with essential information about the terms and costs of their loan. It empowers borrowers to make informed decisions and protects them from deceptive lending practices.

Lenders are required to provide the Truth In Lending Disclosure before borrowers become legally obligated to the loan or pay any fees. This allows borrowers to review and understand the terms and costs before committing to the loan.

The Truth In Lending Disclosure includes information such as the loan amount, interest rate, annual percentage rate (APR), finance charges, repayment schedule, and any additional fees or penalties. It provides a comprehensive overview of the terms and costs of the loan.

While the terms of the loan, including the interest rate, may be negotiable with the lender, some costs and fees mentioned in the disclosure may be non-negotiable. However, it is always worth discussing your concerns or preferences with the lender to see if any adjustments can be made.

If you discover errors or discrepancies in the disclosure, promptly notify the lender and request that they address and correct the inaccuracies. It is crucial to have an accurate disclosure that reflects the terms and costs of the loan correctly.

The basic requirements for the Truth In Lending Disclosure are the same for most consumer credit transactions. However, certain types of loans, such as mortgages or adjustable-rate mortgages, have additional disclosure requirements specific to their nature. Lenders must provide the appropriate disclosures based on the loan type.

Borrowers typically do not have to sign the Truth In Lending Disclosure, as it serves as a document for informational purposes. However, lenders may require borrowers to sign other loan documents to indicate their agreement to the terms and conditions.

Absolutely. As a borrower, you have the right to request a copy of the Truth In Lending Disclosure for your records. It is advisable to keep a copy of all loan documents and disclosures throughout the loan term.

These frequently asked questions address some of the common queries borrowers may have about the Truth In Lending Disclosure. If you have any specific questions or concerns, it is best to consult with your lender or seek professional advice.

Conclusion

The Truth In Lending Disclosure serves as a vital tool in the lending process, providing borrowers with essential information about the terms and costs of their loan. By promoting transparency, it empowers borrowers to make informed financial decisions and protects them from deceptive lending practices.

Understanding the purpose of the Truth In Lending Disclosure is crucial. It promotes transparency, allows for informed decision-making, prevents overburdening debt, and fosters financial literacy. Compliance with the legal requirements ensures that borrowers have access to accurate and reliable information.

When reviewing the Truth In Lending Disclosure, it is important to avoid common mistakes such as rushing through the document, disregarding additional fees, and not comparing loan offers. Taking the time to read and interpret the disclosure, asking questions, and seeking professional advice when needed will help borrowers navigate the loan process effectively.

Lastly, familiarizing yourself with frequently asked questions about the Truth In Lending Disclosure will provide you with valuable insights and address common concerns about this important document.

Overall, the Truth In Lending Disclosure promotes fairness, transparency, and consumer protection in the lending industry. By understanding and utilizing this crucial document, borrowers can make informed decisions, avoid financial pitfalls, and ensure a positive lending experience.