Overview of the Truth in Lending Act

The Truth in Lending Act (TILA) is a federal law enacted in 1968 that aims to protect consumers in credit transactions by promoting transparency and fairness. TILA requires lenders to disclose important information about the terms and costs of credit, allowing borrowers to make informed decisions. The act applies to a wide range of credit transactions, including mortgages, credit cards, and personal loans.

One of the primary goals of TILA is to ensure that consumers have access to clear and accurate information about the credit they are applying for. Lenders must provide borrowers with a standardized disclosure statement, called the Truth in Lending Disclosure, which outlines the key terms of the credit agreement. This allows borrowers to compare offers from different lenders and understand the true cost of borrowing.

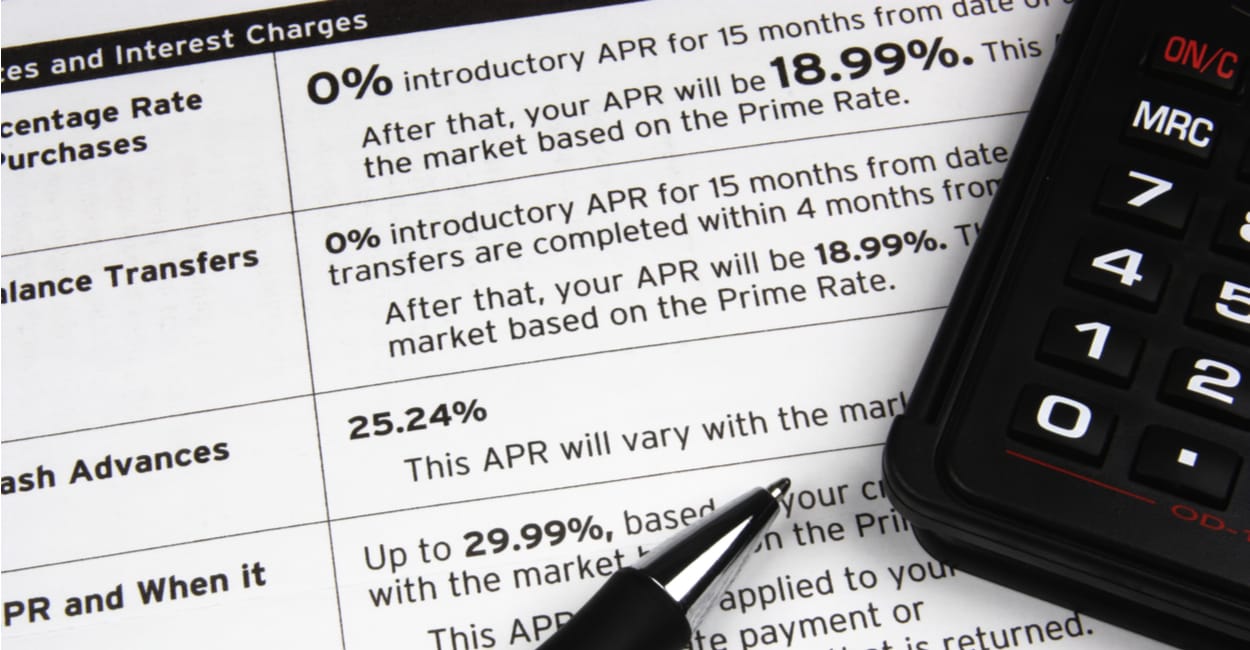

Under TILA, lenders are required to disclose the annual percentage rate (APR), which includes both the interest rate and any additional fees or charges associated with the loan. This helps borrowers understand the total cost of borrowing over the life of the loan. Lenders must also disclose the total amount of finance charges, the payment schedule, and any late payment or prepayment penalties.

In addition to disclosure requirements, TILA also provides certain rights and protections for borrowers. For example, the act gives borrowers the right to rescind certain types of loans, such as home equity loans and refinances, within a specified timeframe. This allows borrowers to reconsider their decision and cancel the loan if they believe it is not in their best interest.

TILA also imposes restrictions on unfair and deceptive practices by lenders. For instance, the act prohibits lenders from engaging in bait-and-switch tactics, where they advertise one set of terms and then offer different terms when the borrower applies for the credit. It also prohibits lenders from charging excessive fees or making false or misleading statements about the credit terms.

Overall, the Truth in Lending Act plays a crucial role in safeguarding the rights of consumers in credit transactions. By requiring lenders to provide clear and accurate information and prohibiting unfair practices, TILA helps consumers make informed decisions and avoid abusive lending practices. It empowers borrowers by promoting transparency and fairness in the credit market and serves as a vital tool for consumer protection.

History and Purpose of the Truth in Lending Act

The Truth in Lending Act (TILA) has a rich history dating back to the 1960s when concerns about deceptive lending practices and lack of transparency in the credit industry were on the rise. At the time, many consumers found themselves entering into loans without a clear understanding of the terms and costs involved.

In response to these concerns, Congress enacted the Truth in Lending Act in 1968 with the primary goal of promoting transparency and fairness in credit transactions. The legislation aimed to address the power imbalance between lenders and consumers by requiring lenders to provide accurate and complete information about the terms and costs of credit.

Prior to the enactment of TILA, consumers were often subject to predatory lending practices, hidden fees, and misleading advertisements. This made it difficult for borrowers to make informed decisions and resulted in financial vulnerability. The act sought to change this by ensuring that borrowers had access to the necessary information to make intelligent choices when taking on credit.

By introducing standardized disclosure requirements, TILA revolutionized the lending industry and enabled borrowers to compare credit options and make informed decisions. The law mandated that lenders provide borrowers with clear and concise disclosures, including the APR, finance charges, payment schedule, and any additional fees or penalties.

Over the years, TILA has undergone several amendments and updates to keep pace with changing market practices and address emerging consumer protection concerns. These changes have strengthened the act and extended its protections to encompass various types of credit, including mortgages, credit cards, and personal loans.

The purpose of TILA goes beyond merely providing information; it also aims to prevent unfair and deceptive lending practices. The act prohibits lenders from making false or misleading statements about the terms of credit. It also places limits on certain predatory practices, such as excessive fees and deceptive advertising.

Through its history, the Truth in Lending Act has been instrumental in shaping the credit industry and protecting consumers from abusive lending practices. It has empowered borrowers by giving them the tools to make informed decisions, increasing transparency, and promoting fair competition among lenders.

Today, TILA continues to play a critical role in safeguarding consumer rights in credit transactions, ensuring that borrowers have access to accurate and understandable information. While the lending landscape may continue to evolve, the fundamental purpose of TILA remains unchanged – to ensure fairness, transparency, and informed decision-making in the credit market.

Key Provisions of the Truth in Lending Act

The Truth in Lending Act (TILA) contains several key provisions designed to protect consumers in credit transactions. These provisions ensure that borrowers have access to clear, accurate, and standardized information so they can make informed decisions when seeking credit.

One of the primary provisions of TILA is the requirement for lenders to provide borrowers with a Truth in Lending Disclosure statement. This disclosure, also known as the TILA disclosure, outlines essential details about the loan, including the annual percentage rate (APR), finance charges, and payment terms. By providing this information in a standardized format, borrowers can easily compare different loan offers from various lenders.

TILA also requires lenders to disclose any applicable fees or penalties associated with the loan. This helps borrowers fully understand the costs they may incur throughout the life of the loan. Some common fees that must be disclosed include origination fees, prepayment penalties, and late payment fees.

In addition to the disclosure requirements, TILA provides borrowers with certain rights and protections. One of these rights is the right to rescind certain types of loans within a limited timeframe. For example, borrowers have the right to rescind a home equity loan or refinancing within three days of the transaction, giving them the opportunity to reconsider their decision without incurring any penalties.

TILA also addresses advertising practices in the credit industry. The act prohibits lenders from making false or misleading statements in their advertisements. Lenders must accurately disclose the terms of the credit being offered, ensuring that consumers are not misled into believing they will receive more favorable terms than what is actually available.

Another important provision of TILA is the requirement for lenders to provide borrowers with a loan estimate and closing disclosure for mortgage transactions. These documents provide borrowers with a breakdown of the loan terms, including the interest rate, closing costs, and estimated monthly payments. The loan estimate must be provided within three business days of applying for a loan, while the closing disclosure must be provided at least three business days before the loan closing.

Overall, the key provisions of the Truth in Lending Act focus on ensuring that consumers have access to accurate and transparent information about the credit they are seeking. By standardizing disclosures and prohibiting deceptive practices, TILA empowers borrowers to make informed decisions and protects them from unfair lending practices. These provisions play a vital role in creating a more equitable and transparent credit market for consumers.

Regulated Transactions under the Truth in Lending Act

The Truth in Lending Act (TILA) applies to a wide range of credit transactions, ensuring that consumers are protected and provided with essential information in various lending scenarios. Understanding which transactions fall under TILA’s regulatory scope is crucial for both lenders and borrowers.

TILA covers many types of credit transactions, including mortgages, credit cards, personal loans, auto loans, and certain installment loans. Whether the credit is extended by a bank, credit union, finance company, or retailer, TILA ensures that borrowers receive accurate and standardized disclosures regarding the terms and costs of the credit.

Mortgage loans constitute a significant category of regulated transactions under TILA. Whether it’s a mortgage to purchase a home or refinance an existing loan, TILA ensures that borrowers have access to important information through the loan estimate and closing disclosure. These documents detail key terms such as the loan amount, interest rate, closing costs, and estimated monthly payments, helping borrowers make informed decisions.

Credit cards are also subject to TILA’s regulations. Credit card issuers must provide clear and concise disclosures regarding the card’s interest rate, annual fees, and any applicable penalties or fees. Additionally, credit card issuers must disclose the grace period, which is the time frame during which no interest accrues if the balance is paid in full.

Personal loans, including unsecured loans, are also regulated under TILA. Lenders must provide borrowers with comprehensive disclosures outlining the APR, finance charges, and repayment terms. By ensuring transparency in personal loan transactions, TILA empowers borrowers to evaluate and compare loan offers to make the best choice for their financial needs.

Auto loans, another category of regulated transactions, fall under TILA’s oversight. Whether obtained from a dealership or a financial institution, borrowers are entitled to receive disclosures that detail the terms and costs of the auto loan, including the interest rate, repayment schedule, and any add-ons or fees.

TILA also covers certain types of installment loans, which are loans where the borrower repays the debt in regular installments. Examples of regulated installment loans include furniture financing, retail installment contracts, and student loans.

It’s important for both lenders and borrowers to be aware of TILA’s scope and requirements for regulated transactions. Lenders must ensure compliance by providing accurate and timely disclosures, while borrowers should take advantage of the information provided to make informed decisions about the credit they are seeking.

In summary, TILA applies to a broad range of credit transactions, including mortgages, credit cards, personal loans, auto loans, and installment loans. By regulating these transactions, TILA ensures that consumers receive standardized, transparent disclosures to make informed decisions and protect their interests.

Rights and Protections for Borrowers

The Truth in Lending Act (TILA) provides borrowers with various rights and protections to ensure fairness and transparency in credit transactions. These rights empower borrowers and give them the ability to make informed decisions while protecting them from abusive lending practices.

One of the key rights under TILA is the right to receive accurate and standardized disclosures. Lenders are required to provide borrowers with a Truth in Lending Disclosure statement, which outlines the terms and costs of the credit. This allows borrowers to compare different loan offers and understand the true cost of borrowing.

TILA also gives borrowers the right to rescind certain types of loans within a specified timeframe. For example, borrowers have the right to rescind a home equity loan or refinancing transaction within three days of the transaction. This provision allows borrowers to reconsider their decision and cancel the loan if they believe it is not in their best interest.

Borrowers also have the right to dispute errors on their credit statements. Under the Fair Credit Billing Act (FCBA), which is closely connected to TILA, borrowers have the right to dispute billing errors on credit card statements. If a borrower identifies an error, they can file a dispute with the credit card issuer, who is then obligated to investigate and correct any verified errors.

TILA protects borrowers from unfair and deceptive lending practices. Lenders are prohibited from engaging in practices such as bait-and-switch tactics, where they advertise one set of terms and then offer different terms when the borrower applies for the credit. Lenders are also prohibited from charging excessive fees or making false or misleading statements about the credit terms.

Borrowers also have the right to review the terms and conditions of the credit agreement before accepting the loan. This allows borrowers to carefully examine the terms, including interest rates, fees, payment schedules, and any potential penalties or charges. By providing borrowers with this opportunity, TILA ensures that they have the necessary information to make an informed decision.

Additionally, TILA requires lenders to provide borrowers with a notice of the consequences of default. This notice informs borrowers of the potential consequences they may face if they fail to make timely payments or default on the loan. It helps borrowers understand the seriousness of the financial commitment and encourages responsible borrowing behavior.

Overall, the rights and protections provided by TILA empower borrowers to make informed decisions, protect them from unfair practices, and promote transparency in the lending process. By knowing their rights, borrowers can enter into credit transactions with confidence, knowing they are protected by law and have the necessary information to make responsible financial choices.

Disclosures and Requirements for Lenders

The Truth in Lending Act (TILA) imposes specific disclosure requirements on lenders to ensure that borrowers receive clear and accurate information about the terms and costs of credit. These requirements enable borrowers to make informed decisions and compare different loan offers effectively.

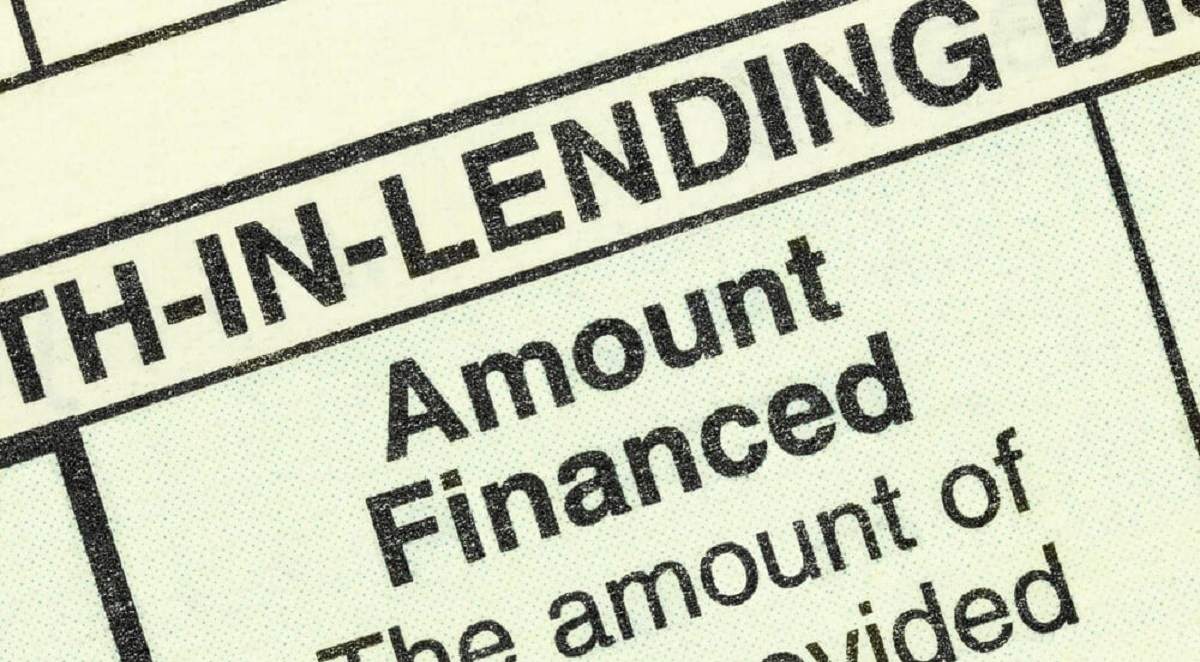

One of the primary disclosures mandated by TILA is the Truth in Lending Disclosure. Lenders must provide borrowers with this standardized disclosure statement, which includes essential details such as the annual percentage rate (APR), finance charges, payment schedule, and any applicable fees or penalties. The purpose of this disclosure is to help borrowers understand the total cost of the credit and compare offers from various lenders.

TILA also requires lenders to disclose the total amount financed, which represents the total amount of credit provided to the borrower. This disclosure ensures that borrowers have a clear understanding of the actual funds they will receive and are required to repay.

In mortgage transactions, lenders must also provide borrowers with a loan estimate and a closing disclosure. The loan estimate is provided within three business days of applying for a mortgage loan and includes detailed information about the loan terms, estimated closing costs, and projected monthly payments. The closing disclosure is provided at least three business days before the loan closing and outlines the final terms of the loan, including the interest rate, closing costs, and amount due at closing.

Furthermore, TILA requires lenders to disclose information related to the borrower’s right to rescind certain loan transactions. For example, for certain home equity loans and refinances, lenders must provide borrowers with a notice of their right to rescind within three business days of the transaction. This disclosure ensures that borrowers are aware of their ability to cancel the loan if they choose to do so.

Aside from disclosures, TILA also imposes specific requirements on lenders. For instance, lenders must provide a written acknowledgement of receipt of any written request for payoff balances within a reasonable time. This requirement ensures that borrowers have access to the necessary information when paying off their loan or refinancing.

Lenders are also required to keep records of credit transactions for a specified period. This requirement allows for the verification and examination of the lender’s compliance with TILA and provides a means to investigate any potential violations or disputes that may arise.

By imposing these disclosure requirements and obligations on lenders, TILA promotes transparency and ensures that borrowers receive accurate and complete information about the terms and costs of credit. These disclosures enable borrowers to understand their financial obligations, compare loan offers, and make informed decisions, all while protecting them from predatory lending practices.

Penalties for Violations of the Truth in Lending Act

The Truth in Lending Act (TILA) establishes penalties for lenders who violate its provisions, ensuring that there are consequences for non-compliance and promoting accountability in the credit industry. These penalties serve as deterrents and reinforce the importance of adhering to TILA’s requirements to protect consumers from unfair lending practices.

One of the primary penalties that can be imposed for TILA violations is a civil liability. TILA allows borrowers who have been harmed by a lender’s non-compliance to file lawsuits seeking damages. If the court finds that a lender has willfully violated TILA’s requirements, borrowers may be entitled to actual damages plus statutory damages, which can range from $500 to $5,000 per violation.

TILA also empowers the Federal Trade Commission (FTC) and other federal agencies to enforce its provisions. If the FTC or another agency determines that a lender has engaged in unfair or deceptive practices in violation of TILA, they may initiate enforcement actions against the lender. These actions can result in civil penalties, injunctive relief, and other remedies.

In addition to civil liability and enforcement actions, TILA violations can also result in criminal penalties in certain circumstances. For example, willful violations of TILA’s requirements with intent to defraud can be prosecuted as criminal offenses. If convicted, individuals can face fines and imprisonment.

Furthermore, TILA provides for rescission rights for borrowers in certain cases of non-compliance by lenders. If a lender fails to provide the required disclosures or violates other TILA provisions, borrowers may have the right to rescind the loan within a specific timeframe. If the lender refuses to honor the borrower’s rescission request, they may be liable for actual and statutory damages as well as the borrower’s attorney’s fees.

It is important to note that TILA also allows for administrative enforcement by regulatory agencies such as the Consumer Financial Protection Bureau (CFPB). These agencies have the authority to investigate potential TILA violations, issue civil administrative actions, impose fines, and require corrective measures to be taken by the non-compliant lenders.

The penalties established by TILA underscore the seriousness of non-compliance and the significance of protecting consumers in credit transactions. By imposing civil liability, empowering regulatory agencies, and potentially resulting in criminal consequences, TILA ensures that lenders have strong incentives to comply with the law and adhere to the standards set forth in the act.

In summary, the penalties for violations of the Truth in Lending Act include civil liability, enforcement actions by regulatory agencies, rescission rights for borrowers, and potential criminal penalties. These penalties aim to deter non-compliance, promote accountability, and protect consumers from unfair lending practices.

How to File a Complaint under the Truth in Lending Act

If you believe that a lender has violated the provisions of the Truth in Lending Act (TILA) and you have been harmed as a result, you have the right to file a complaint to seek resolution and potential remedies. Filing a complaint is an important step in holding lenders accountable and protecting your rights as a consumer.

The first step in filing a complaint is to gather all relevant documentation related to the loan or credit transaction. This may include loan agreements, statements, and any correspondence or communication with the lender. These documents will support your complaint and provide evidence of the alleged TILA violations.

Next, you should contact the appropriate regulatory agency that handles TILA complaints. The Consumer Financial Protection Bureau (CFPB) is the primary federal agency responsible for enforcing TILA. You can file a complaint with the CFPB online through their website or via mail by submitting a completed complaint form.

When filing a complaint, it is essential to provide as much detail as possible about the TILA violations you believe have occurred. Clearly explain the circumstances, including dates, the specific provisions of TILA that have been violated, and how you have been harmed as a result. Be sure to include all supporting documentation to strengthen your case.

The CFPB or the relevant regulatory agency will review your complaint and may conduct an investigation into the lender’s practices. They have the authority to take various actions, including issuing warnings, initiating enforcement actions, imposing fines, or demanding corrective measures. Keep in mind that the process may take time, and the agency may contact you for additional information or clarification during the investigation.

In addition to filing a complaint with the CFPB or the relevant agency, you may also consider seeking legal advice from an attorney who specializes in consumer protection laws. The attorney can guide you through the process, help assess the strength of your case, and assist in negotiations or legal proceedings, if necessary.

Overall, filing a complaint under the Truth in Lending Act is an important step in protecting your rights as a borrower and seeking resolution for any TILA violations that have occurred. By reporting violations and working with regulatory agencies, you contribute to the enforcement of TILA and help maintain a fair and transparent credit market for all consumers.

Recent Developments and Updates to the Truth in Lending Act

The Truth in Lending Act (TILA) has seen significant developments and updates over the years to adapt to changing market practices and address emerging consumer protection concerns. These developments aim to enhance transparency, provide additional safeguards for borrowers, and promote fair lending practices.

One notable recent development is the implementation of the TILA-RESPA Integrated Disclosure (TRID) Rule, also known as the “Know Before You Owe” rule. This rule, introduced by the Consumer Financial Protection Bureau (CFPB), combines the loan estimate and closing disclosure into a single document, ensuring borrowers receive comprehensive and standardized information about their mortgage loan. The TRID rule aims to simplify the disclosure process and make it easier for borrowers to understand the terms and costs of their mortgage loan.

In response to the financial crisis of 2008, which was largely fueled by irresponsible lending practices, Congress passed the Dodd-Frank Wall Street Reform and Consumer Protection Act. This legislation included amendments to TILA that enhanced consumer protections, such as prohibiting certain predatory lending practices, addressing unfair credit card practices, and improving mortgage lending standards. These changes strengthened TILA’s framework and expanded its scope of protection.

Another significant update to TILA is the expansion of the definition of a “mortgage loan originator.” This amendment requires individuals who act as mortgage loan originators to meet certain licensing and registration requirements. The goal is to ensure that individuals providing mortgage loan services are qualified and adhere to ethical and professional standards.

Additionally, the CFPB has issued various rulemakings and guidance to provide clarity and guidance on TILA’s requirements. The CFPB’s focus has been on enforcing TILA, enhancing consumer disclosures, and ensuring that lenders comply with the mandated disclosures, particularly in the mortgage industry.

Furthermore, technological advancements and the rise of digital lending platforms have prompted discussions and considerations about how TILA can adapt to the changing landscape. The CFPB has been exploring ways to streamline and modernize the disclosure requirements under TILA to accommodate digital transactions while maintaining the necessary consumer protections.

It’s important to stay informed about these recent developments and updates to TILA to ensure you have the most up-to-date information and can benefit from the additional protections and transparency measures. By being aware of these changes, you can better navigate the credit market and make informed decisions when seeking credit.

In summary, TILA has undergone notable developments and updates in recent years to adapt to evolving market practices and address consumer protection concerns. The TRID rule, amendments through the Dodd-Frank Act, expanded definitions, CFPB rulemakings, and considerations for digital lending platforms are all examples of efforts to enhance transparency, consumer disclosures, and fair lending practices under TILA.

Conclusion

The Truth in Lending Act (TILA) is a crucial piece of legislation that plays a vital role in protecting consumers in credit transactions. Through its disclosure requirements, rights and protections for borrowers, penalties for violations, and recent updates, TILA aims to promote transparency, fairness, and informed decision-making in the lending industry.

TILA ensures that borrowers have access to clear and accurate information about the terms and costs of credit. By disclosing the annual percentage rate (APR), finance charges, payment schedules, and other key details, borrowers can effectively compare loan offers and make informed decisions. TILA also grants borrowers certain rights, such as the right to rescind certain loans and dispute billing errors, providing them with avenues for protection and recourse.

Non-compliance with TILA can result in penalties for lenders, including civil liability, enforcement actions, and potential criminal penalties. These repercussions serve as deterrents to ensure lenders adhere to TILA’s requirements and promote fair lending practices across the credit industry.

Recent developments and updates to TILA, such as the TRID rule and amendments through the Dodd-Frank Act, demonstrate the ongoing effort to enhance consumer protections and adapt to changing market practices. These developments aim to simplify disclosures, address predatory lending practices, and streamline the lending process, all while promoting transparency and accountability.

It is essential for both lenders and borrowers to be aware of the rights, requirements, and protections outlined by TILA. Lenders must comply with the disclosure obligations and adhere to ethical lending practices, while borrowers should utilize the information provided to make informed decisions and protect their interests.

In conclusion, the Truth in Lending Act serves as a linchpin of consumer protection in credit transactions. By providing borrowers with essential disclosures, enforcing their rights, and imposing penalties for violations, TILA ensures transparency, fairness, and informed decision-making in the credit market. Through continued awareness of TILA’s provisions and ongoing vigilance, both lenders and borrowers can contribute to a more equitable and responsible lending environment.