Introduction

Welcome to our guide on the Truth in Lending Act (TILA) and its accompanying regulation, known as Regulation Z. If you have ever taken out a loan or used a credit card, you may be familiar with these terms. But what exactly do they entail? In this article, we will provide you with a comprehensive overview of the Truth in Lending Act and shed light on the specific requirements set forth by Regulation Z.

The Truth in Lending Act was enacted by the United States Congress in 1968 with the goal of promoting transparency and fairness in consumer credit transactions. It aimed to ensure that lenders provide clear and accurate information about the terms and costs of credit to borrowers. Regulation Z, on the other hand, was implemented by the Federal Reserve Board to provide detailed guidelines on how lenders must comply with the requirements of the Truth in Lending Act.

Understanding TILA and Regulation Z is crucial for both consumers and lenders. For borrowers, it means having access to accurate and comprehensive information about the terms and costs associated with their credit. This empowers them to make informed decisions and compare different loan offers effectively. For lenders, complying with these regulations ensures fair and responsible lending practices, while also protecting them from potential legal consequences.

In the following sections, we will delve deeper into the specific requirements of Regulation Z, including the disclosure of terms and conditions, the calculation of the Annual Percentage Rate (APR), the inclusion of finance charges and fees, the right of rescission, and the guidelines for advertising and promotional materials. We will also touch upon the enforcement mechanisms and penalties associated with non-compliance.

By the end of this article, you will have a comprehensive understanding of the Truth in Lending Act and Regulation Z and their significant impact on consumer credit transactions. So, let’s dive in and explore what these regulations require!

Overview of the Truth in Lending Act

The Truth in Lending Act (TILA) is a federal law designed to protect consumers in credit transactions by requiring lenders to disclose key information about the terms and costs of credit. The law applies to various types of credit, including mortgages, credit cards, auto loans, and personal loans.

One of the primary objectives of the Truth in Lending Act is to ensure that consumers have access to clear and accurate information about the terms of their credit. Lenders must provide borrowers with the following information before they enter into a credit agreement:

- The annual percentage rate (APR): This is the cost of borrowing expressed as a yearly interest rate, including both the interest charges and certain fees.

- The finance charge: This is the total cost of credit, including interest and other charges, expressed in dollars.

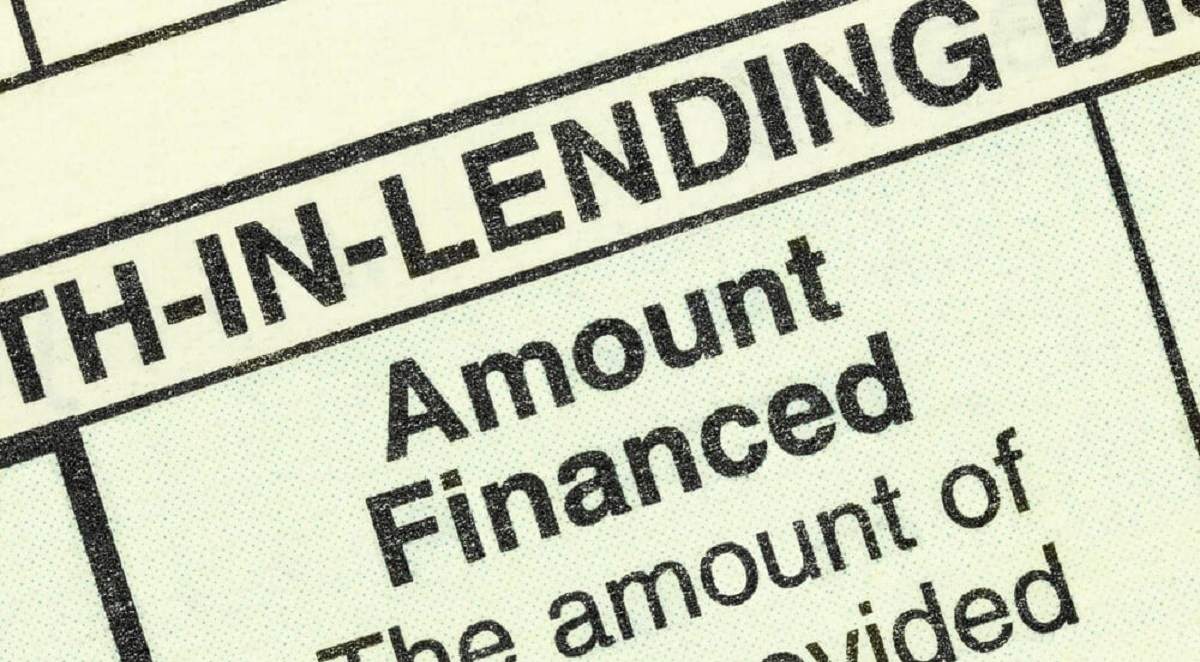

- The total amount financed: This is the total amount borrowed or the credit limit available.

- The total of payments: This is the total amount the borrower will have paid by the end of the loan term if they make all payments as scheduled.

- The number of payments: This refers to the total number of payments required to repay the loan.

- The payment schedule: This outlines the amount and due date of each payment.

In addition to these disclosures, TILA also provides consumers with certain rights and protections. For example, the law requires lenders to provide consumers with a notice of their right to cancel certain types of transactions within a specified period, known as the right of rescission. This gives borrowers the opportunity to reconsider their decision and potentially cancel the loan without penalty.

It is important to note that TILA does not regulate the interest rate or fees that lenders can charge. Instead, the law focuses on ensuring that consumers are provided with clear and accurate information to make informed decisions about credit. By providing this information, TILA promotes transparency and helps consumers compare loan offers effectively, thereby encouraging fair and responsible lending practices.

Enforcement of the Truth in Lending Act is primarily the responsibility of the Consumer Financial Protection Bureau (CFPB). The CFPB is empowered to take legal action against lenders who violate TILA’s provisions and to impose penalties for non-compliance.

Now that we have covered the basics of the Truth in Lending Act, let’s delve into the specific requirements set forth by the accompanying regulation, known as Regulation Z.

What is Regulation Z?

Regulation Z is a set of guidelines established by the Federal Reserve Board to implement and enforce the provisions of the Truth in Lending Act (TILA). It provides specific requirements and instructions for lenders to ensure compliance with TILA’s disclosure and consumer protection provisions.

The primary goal of Regulation Z is to provide consumers with clear and transparent information about the costs and terms of credit. It aims to prevent deceptive and unfair practices in lending and promote fairness and responsibility in the consumer credit market.

Under Regulation Z, lenders are required to provide written disclosures to consumers before they enter into a credit agreement. These disclosures must include information about the annual percentage rate (APR), finance charges, and other fees associated with the credit. Lenders must also provide details about the payment schedule, the total amount financed, and the total of payments.

Regulation Z also sets guidelines for advertising and promotional materials used by lenders. It requires lenders to provide accurate and non-misleading information about credit terms and costs in their advertising materials. This ensures that consumers are not deceived or misled by attractive offers that fail to disclose important information or include hidden costs.

Furthermore, Regulation Z provides specific rules regarding the right of rescission. It outlines the circumstances in which borrowers have the right to cancel certain credit transactions within a specific timeframe. For example, the regulation grants borrowers a three-day right of rescission for certain home equity loans and refinance transactions.

In addition to these requirements, Regulation Z prohibits certain unfair practices by lenders. It prohibits lenders from charging excessive fees, engaging in loan flipping (repeated refinancing of a loan), and including mandatory arbitration clauses in certain credit agreements.

It is important to note that Regulation Z does not set limits on interest rates or fees that lenders can charge. Instead, it focuses on ensuring that consumers have access to clear and accurate information to make informed decisions about credit.

If lenders fail to comply with the disclosures and requirements outlined in Regulation Z, they may be subject to legal action, penalties, and potential liability for damages. The Consumer Financial Protection Bureau (CFPB) is responsible for enforcing Regulation Z and taking action against non-compliant lenders.

In the next section, we will explore in detail the specific requirements that Regulation Z imposes on lenders in order to ensure transparency and consumer protection in credit transactions.

The Purpose of Regulation Z

The main purpose of Regulation Z, which is implemented under the authority of the Truth in Lending Act (TILA), is to promote transparency, fairness, and consumer protection in credit transactions. It aims to ensure that consumers have access to clear and accurate information about the terms and costs of credit, enabling them to make informed decisions and compare credit offers effectively.

One of the core objectives of Regulation Z is to prevent deceptive and unfair practices by lenders. By setting specific guidelines and requirements for creditor disclosures, advertising, and other aspects of consumer credit, Regulation Z aims to eliminate misleading information and misleading marketing tactics. This provides consumers with the necessary information to understand the true costs and terms of the credit they are seeking.

Another purpose of Regulation Z is to ensure fairness in lending practices. It prohibits lenders from engaging in certain practices, such as charging excessive fees or imposing unfair penalties. This helps to create a level playing field for borrowers and prevents lenders from taking advantage of the borrower’s lack of knowledge or bargaining power.

Regulation Z also incorporates provisions that protect consumer privacy. It requires lenders to maintain appropriate safeguards and procedures to protect the confidentiality of consumer information and prevent unauthorized access or use.

Moreover, Regulation Z plays a vital role in promoting responsible borrowing and lending by setting standards that lenders must adhere to. By mandating clear and accurate disclosure of loan terms and costs, it encourages responsible lending practices. Additionally, by outlining the right of rescission, it provides borrowers with an opportunity to reconsider their decision without any penalty and ensures they are not locked into unfavorable credit agreements.

The implementation of Regulation Z also aims to foster competition in the credit market. By requiring consistent disclosure of key loan terms and costs, it facilitates easier comparison of credit offers from different lenders. This enables borrowers to make more informed decisions and encourages lenders to provide competitive terms to attract borrowers.

Enforcement of Regulation Z primarily falls under the jurisdiction of the Consumer Financial Protection Bureau (CFPB), which has the authority to take action against non-compliant lenders. The CFPB ensures that lenders follow the guidelines set forth by Regulation Z and holds them accountable for any violations of consumer rights.

In summary, the purpose of Regulation Z is to create a fair and transparent consumer credit market. It aims to provide consumers with accurate information, protect their rights, and promote responsible lending practices. By complying with the requirements of Regulation Z, lenders can contribute to a healthier and more equitable credit environment.

What Does Regulation Z Require?

Regulation Z, which implements the provisions of the Truth in Lending Act (TILA), outlines specific requirements that lenders must follow to ensure transparency and consumer protection in credit transactions.

One of the key requirements of Regulation Z is the disclosure of terms and conditions. Lenders are obligated to provide borrowers with clear and accurate information about the terms, costs, and risks associated with the credit being offered. This includes disclosing the annual percentage rate (APR), finance charges, payment schedule, total amount financed, and total of payments.

Regulation Z also requires lenders to disclose important information related to credit card agreements. This includes the rules for calculating finance charges, the methods used to repay the outstanding balance, and any potential penalties or fees that may be imposed for late payments or other violations of the agreement.

Furthermore, Regulation Z imposes specific requirements for the calculation and disclosure of the annual percentage rate (APR) for credit transactions. The APR reflects the true cost of borrowing, including both the interest rate and certain fees. Lenders must accurately calculate and disclose the APR to ensure that borrowers have a clear understanding of the total cost of credit.

Finance charges and fees are also subject to regulation under Regulation Z. Lenders are required to disclose all applicable fees and charges associated with the credit transaction. They must clearly identify the finance charges, which encompass the interest and certain other fees, and present them in a way that is easy for the borrower to understand.

Another significant requirement of Regulation Z is the right of rescission. This gives borrowers the ability to cancel certain credit transactions within a specified timeframe without incurring any penalties. Regulation Z mandates that lenders provide clear and conspicuous notice to borrowers about their right to rescind and the procedures for exercising that right.

Regulation Z also addresses the use of advertising and promotional materials by lenders. It requires that lenders present accurate and non-misleading information about the terms and costs of credit in their advertisements. This ensures that consumers are not misled by attractive offers that fail to disclose important information or include hidden costs.

Non-compliance with Regulation Z can result in severe penalties for lenders. The Consumer Financial Protection Bureau (CFPB) has the authority to take legal action against lenders who violate the provisions of Regulation Z and to impose monetary penalties for non-compliance.

Overall, Regulation Z plays a vital role in ensuring that consumers have access to clear and accurate information about the terms and costs of credit. By complying with the requirements of Regulation Z, lenders can contribute to a transparent and fair consumer credit market while protecting borrowers’ rights.

Disclosure of Terms and Conditions

One of the core requirements of Regulation Z is the disclosure of terms and conditions associated with credit transactions. Lenders are obligated to provide borrowers with clear and comprehensive information about the key terms, costs, and risks of the credit being offered. This ensures that consumers have the necessary information to make informed decisions and compare different loan offers effectively.

The disclosures required by Regulation Z include the annual percentage rate (APR), finance charges, payment schedule, total amount financed, and total of payments. The APR represents the true cost of borrowing, including both the interest rate and certain fees. Lenders must accurately calculate and disclose the APR to provide borrowers with a clear understanding of the total cost of credit.

Finance charges, which encompass the interest charges and certain other fees, must be clearly identified and disclosed by the lender. This allows borrowers to assess the cost of the credit they are obtaining. Lenders must also provide a payment schedule that outlines the amount and due dates of each payment, enabling borrowers to plan their budgets accordingly.

In addition to the APR and finance charges, Regulation Z requires lenders to disclose the total amount financed and the total of payments. The total amount financed represents the total amount borrowed or the credit limit available, while the total of payments indicates the overall amount that the borrower will have paid by the end of the loan term if all payments are made as scheduled.

Furthermore, Regulation Z mandates that lenders disclose any balloon payments, prepayment penalties, or other significant terms and conditions that may impact the borrower’s repayment obligations. This ensures that borrowers are fully aware of any potential risks or costs associated with the credit agreement.

To ensure that borrowers have ample time to review and understand the terms and conditions, lenders must provide the required disclosures before the consummation of the credit transaction. This allows borrowers to assess the terms, costs, and risks associated with the credit and make an informed decision.

Additionally, Regulation Z requires lenders to provide certain disclosures in writing. This helps to ensure that borrowers have a tangible record of the terms and conditions of the credit agreement. This written documentation can serve as a valuable reference and can protect borrowers in case of any disputes or misunderstandings.

By complying with the disclosure requirements of Regulation Z, lenders play a crucial role in promoting transparency and consumer protection in the credit market. These disclosures empower borrowers to understand the terms and costs of their credit, make informed decisions, and avoid potential pitfalls or hidden charges that may arise from inadequate disclosure practices.

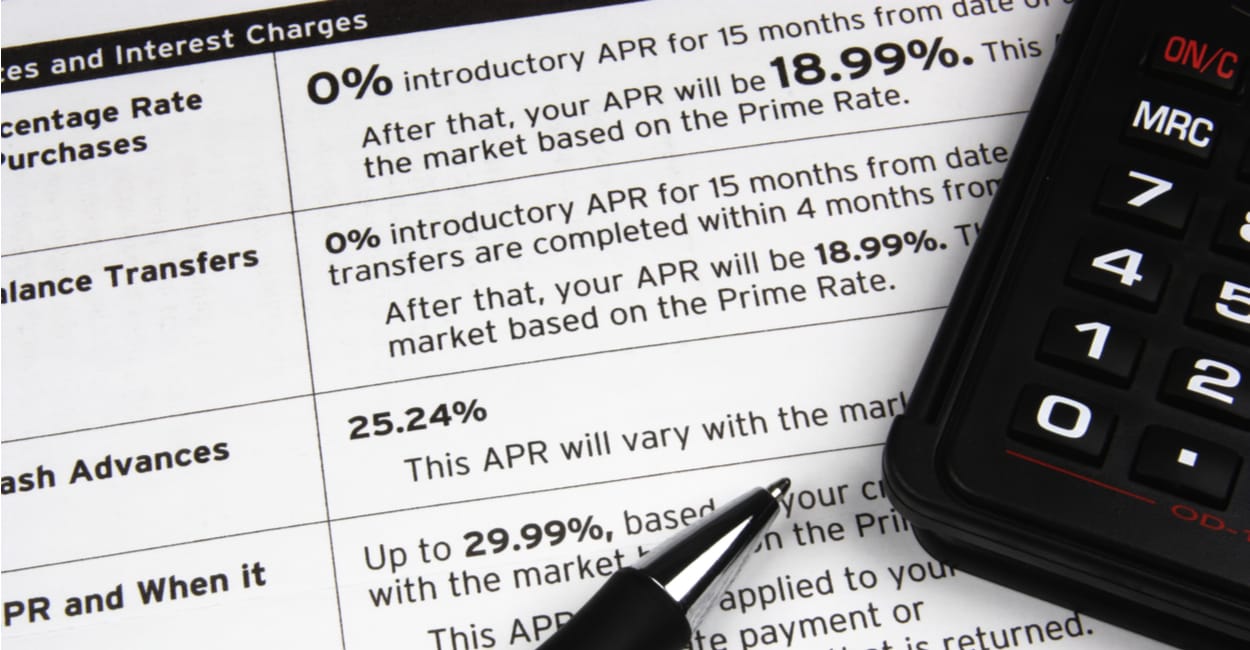

Annual Percentage Rate (APR)

The Annual Percentage Rate (APR) is a critical component of credit transactions that is regulated by Regulation Z. The APR represents the true cost of borrowing, including both the interest rate and certain fees associated with the credit. It is a standardized measure that allows borrowers to compare different loan offers and make informed decisions about credit.

Regulation Z mandates that lenders accurately calculate and disclose the APR to borrowers. By doing so, lenders must include not only the interest rate but also certain fees, such as origination fees, prepaid finance charges, and mortgage insurance premiums. These additional charges are combined with the interest rate to reflect the total cost of credit over the loan term.

The inclusion of various fees and charges in the APR ensures that borrowers have a comprehensive understanding of the costs associated with credit. It prevents lenders from hiding additional charges outside of the interest rate, enhancing transparency and allowing borrowers to make more informed decisions.

Proper disclosure of the APR enables borrowers to compare credit offers more effectively. By evaluating the APR of different loans, borrowers can determine the total cost they will incur with each option. This facilitates better decision-making, as borrowers can select the loan with the most favorable terms and lowest overall cost.

It is important for borrowers to note that the APR may not always be the same as the stated interest rate. This is because the APR takes into account additional costs and fees associated with the credit. As a result, the APR is typically slightly higher than the stated interest rate.

Understanding the APR is crucial for borrowers, as it allows them to accurately assess the affordability of credit and its impact on their finances over the loan term. A higher APR signifies higher borrowing costs, while a lower APR indicates a more cost-effective loan. By considering the APR, borrowers can make informed decisions and avoid potentially burdensome financial situations.

Regulation Z ensures that lenders provide the APR in a clear and prominent manner, allowing borrowers to easily locate and compare this vital information across different loan products. By standardizing the calculation and disclosure of the APR, Regulation Z aims to promote transparency and protect consumers from deceptive or misleading practices in the credit market.

In summary, the APR is a crucial element of credit transactions governed by Regulation Z. It provides borrowers with a comprehensive view of the true cost of credit, considering both the interest rate and applicable fees. By calculating and disclosing the APR accurately, lenders facilitate transparency and empower borrowers to make well-informed decisions when obtaining credit.

Finance Charges and Fees

Finance charges and fees are an important aspect of credit transactions, and Regulation Z mandates that lenders disclose these costs to borrowers. By understanding finance charges and fees, borrowers can accurately assess the total cost of credit and make informed decisions.

Finance charges refer to the cost of credit, including both interest charges and certain other fees imposed by the lender. It is essential for lenders to clearly identify finance charges and present them in a way that is easy for borrowers to understand. This allows borrowers to know the actual cost of borrowing and compare it across different loan options.

Regulation Z requires lenders to disclose finance charges in a prominent and accurate manner. This helps borrowers assess the affordability of credit and make informed choices. By including finance charges in the disclosure, lenders contribute to a transparent credit market and ensure that borrowers have access to the necessary information to properly evaluate the costs of credit.

In addition to finance charges, Regulation Z also governs the disclosure of various fees associated with credit transactions. These fees may include application fees, origination fees, late payment fees, prepayment penalties, and other charges assessed by the lender.

Regulation Z mandates that lenders disclose all applicable fees, enabling borrowers to have a comprehensive understanding of the financial obligations associated with the credit agreement. By providing transparent and accurate fee disclosures, lenders ensure that borrowers are not surprised by unexpected charges or hidden costs.

Lenders must disclose fees in a clear and conspicuous manner, allowing borrowers to make informed decisions about the credit being offered. This promotes fairness in lending by preventing lenders from concealing or downplaying fees that may significantly impact the total cost of credit.

It is crucial for borrowers to carefully review the disclosure of finance charges and fees before entering into a credit agreement. By doing so, borrowers can accurately assess the total cost of the credit and evaluate whether the terms are reasonable and affordable.

Regulation Z also requires lenders to provide an itemized breakdown of the finance charges and fees in the loan agreement. This allows borrowers to understand the specific components of the costs they are being charged and identify any potential discrepancies or errors in the disclosures.

By disclosing finance charges and fees in a transparent and accurate manner, lenders contribute to a fair and responsible lending environment. This empowers borrowers to make informed decisions, compare loan offers effectively, and avoid potential financial pitfalls that may arise from inadequate disclosure practices.

In summary, finance charges and fees are an essential part of credit transactions that lenders are required to disclose under Regulation Z. These disclosures enable borrowers to understand the overall cost of credit, make informed choices, and protect themselves from misleading or deceptive lending practices.

Right of Rescission

The right of rescission is an important protection for borrowers under Regulation Z. It provides borrowers with the ability to cancel certain credit transactions within a specified timeframe without incurring any penalties or fees.

Regulation Z grants borrowers the right of rescission for specific types of transactions, such as home equity loans and mortgage refinance transactions. This right allows borrowers to reconsider their decision and potentially cancel the loan if they believe it is not in their best interest.

Upon exercising the right of rescission, borrowers must notify the lender in writing of their intent to cancel the transaction. The lender is then required to refund any payments made by the borrower and terminate the security interest in the borrower’s property.

The right of rescission is designed to protect borrowers from entering into credit agreements that they may later regret or find unfavorable. This can be particularly important when borrowers are rushed or pressured to make a quick decision, such as in situations involving door-to-door sales or timeshare presentations.

By providing borrowers with the right of rescission, Regulation Z promotes responsible lending practices and ensures that borrowers have the opportunity to fully evaluate the terms of the credit before committing to it. It allows borrowers a reasonable timeframe to review the loan documents, seek independent advice if necessary, and assess whether the loan aligns with their financial goals and circumstances.

It is important for borrowers to be aware of the specific timeframe in which they can exercise the right of rescission. The rescission period typically lasts for three business days following the consummation of the transaction or the receipt of the required disclosures, whichever occurs later.

However, certain transactions may have different rescission periods. For example, home equity loans secured by the borrower’s primary residence generally have a three-day rescission period, while loans for the purchase of a home are not subject to the right of rescission under Regulation Z.

It is crucial for borrowers to carefully consider their options and make an informed decision within the rescission period if they wish to exercise their right of rescission. Failing to do so may result in the loan becoming legally binding, and the borrower may no longer have the opportunity to cancel the transaction without penalty.

Regulation Z requires lenders to provide borrowers with clear and conspicuous notice of their right of rescission. This ensures that borrowers are aware of this important protection and understand the procedures for exercising their rights.

By including the right of rescission in Regulation Z, borrowers are provided with an additional layer of consumer protection. It allows borrowers to reconsider their loan decisions and address any potential concerns or issues that may have been overlooked during the loan application process.

In summary, the right of rescission under Regulation Z provides an important safeguard for borrowers, allowing them to reconsider and cancel certain credit transactions within a specified timeframe. By exercising this right, borrowers have the opportunity to fully evaluate the terms and make informed decisions before committing to the loan.

Advertising and Promotional Materials

Regulation Z includes specific guidelines for lenders regarding the use of advertising and promotional materials. The purpose of these guidelines is to ensure that consumers are provided with accurate and non-misleading information about the terms and costs of credit in advertisements.

Lenders are required to provide clear and conspicuous disclosures in their advertising materials to indicate the true nature of the credit being offered. This includes disclosing important information such as the annual percentage rate (APR), any applicable fees, and other key terms that may affect the borrower’s decision.

Regulation Z also prohibits lenders from making false or misleading statements in their advertising. Lenders must present information in a way that avoids confusion or deception. This helps to protect consumers from being lured into credit agreements that do not align with the advertised terms.

Additionally, lenders must disclose any significant limitations or restrictions on the advertised credit terms. For example, if an advertisement promotes a low introductory interest rate that increases after a certain period, such as with an adjustable-rate mortgage, this information must be clearly disclosed.

Regulation Z also requires lenders to include certain additional disclosures in their advertising materials, such as the payment amounts, payment periods, and any other significant terms that will govern the credit transaction.

The purpose of these advertising guidelines is to provide consumers with the necessary information to make informed decisions about credit. By ensuring that advertisements are clear, accurate, and non-misleading, Regulation Z helps to protect consumers from deceptive practices and promotes fairness in the credit market.

Furthermore, Regulation Z prohibits lenders from making statements or using visuals that minimize the importance of disclosures or present credit as free or substantially less costly than it actually is. This helps to prevent borrowers from being misled by attractive offers that fail to disclose important information or include hidden costs.

It is important for lenders to comply with these advertising guidelines to avoid potential legal consequences. Failure to adhere to the requirements of Regulation Z can result in penalties and legal action by regulatory agencies such as the Consumer Financial Protection Bureau (CFPB).

Borrowers should review advertisements and promotional materials critically and be mindful of any claims that appear too good to be true. They should seek additional information and clarification if necessary before making any credit-related decisions.

By ensuring that lenders follow strict guidelines for advertising and promotional materials, Regulation Z aims to protect consumers from deceptive practices, promote transparency, and help borrowers make well-informed choices when seeking credit.

In summary, Regulation Z establishes clear guidelines for lenders regarding the use of advertising and promotional materials. It requires lenders to provide accurate and non-misleading information, make appropriate disclosures, and avoid deceptive practices. These guidelines help borrowers make informed decisions and protect them from misleading or false advertising in the credit market.

Enforcement and Penalties

Regulation Z, which implements the provisions of the Truth in Lending Act (TILA), includes enforcement mechanisms and penalties to ensure compliance with its requirements. The purpose of these enforcement measures is to protect consumers and encourage lenders to adhere to the regulations set forth by Regulation Z.

The primary entity responsible for enforcing Regulation Z is the Consumer Financial Protection Bureau (CFPB), a federal agency tasked with protecting consumers in the financial marketplace. The CFPB has the authority to take legal action against lenders who violate the provisions of Regulation Z and to impose penalties and other remedies.

In cases where a lender is found to have violated Regulation Z, the CFPB can seek monetary penalties and restitution on behalf of harmed consumers. The exact amount of the penalty is determined based on various factors, including the severity and extent of the violation, the financial resources of the lender, and the impact on consumers.

The CFPB may also require lenders to take corrective action, such as revising their policies and procedures to ensure future compliance with Regulation Z. In some cases, lenders may be required to provide redress to affected consumers, such as refunding fees or compensating for financial harm caused by non-compliance.

Additionally, lenders found to be in violation of Regulation Z may be subject to reputational damage and loss of consumer trust. Negative publicity surrounding non-compliance can have long-lasting consequences for lenders, potentially resulting in a loss of business and reduced customer confidence.

It is important for lenders to proactively ensure compliance with Regulation Z to avoid potential penalties and consequences. This can involve implementing robust compliance management systems, conducting regular internal audits, and staying updated on changes and interpretations of the regulation.

Regulation Z also allows consumers to take legal action against lenders for non-compliance. If a borrower believes their rights under Regulation Z have been violated, they may have the option to file a lawsuit seeking remedies. This can include damages, attorney fees, and other relief as deemed appropriate by the court.

However, it is worth noting that individual lawsuits can be complex and costly. As such, borrowers may also choose to report suspected violations to the CFPB or other relevant regulatory agencies. Reporting non-compliance helps authorities identify patterns of misconduct and take appropriate enforcement action.

By enforcing Regulation Z and imposing penalties for non-compliance, the CFPB aims to protect consumers from deceptive practices, promote transparency, and foster fair and responsible lending practices in the financial marketplace.

In summary, Regulation Z is enforced by the Consumer Financial Protection Bureau, which has the authority to take legal action against lenders who violate its provisions. Penalties can include monetary fines, restitution to affected consumers, and reputational damage. Lenders should ensure compliance with Regulation Z to avoid penalties and maintain consumer trust, while consumers have the option to take legal action or report non-compliance to regulatory authorities for enforcement.

Conclusion

The Truth in Lending Act (TILA) and its accompanying regulation, Regulation Z, play a crucial role in promoting transparency, fairness, and consumer protection in credit transactions. These regulations ensure that borrowers are provided with clear and accurate information about the terms and costs of credit, empowering them to make informed decisions and protect themselves from deceptive practices.

Through TILA and Regulation Z, borrowers have the right to receive disclosures that outline important details of the credit, including the annual percentage rate (APR), finance charges, payment schedule, total amount financed, and total of payments. These disclosures enable borrowers to compare loan offers effectively and understand the true cost of borrowing.

Regulation Z also addresses other key aspects of credit transactions, such as the right of rescission, which allows borrowers to cancel certain credit transactions within a specified timeframe without penalty. Additionally, the regulation mandates guidelines for advertising and promotional materials to ensure that borrowers are provided with accurate and non-misleading information about credit terms and costs.

Enforcement of TILA and Regulation Z is the responsibility of the Consumer Financial Protection Bureau (CFPB), which has the authority to impose penalties and bring legal action against lenders who violate the regulations. This enforcement ensures that lenders adhere to the requirements of TILA and Regulation Z, maintaining fairness and trust in the consumer credit market.

Compliance with TILA and Regulation Z is essential for lenders to protect consumers and promote transparency in credit transactions. By providing accurate disclosures and adhering to the guidelines, lenders contribute to a fair and responsible lending environment.

For borrowers, understanding the rights and protections afforded by TILA and Regulation Z is critical when entering into credit agreements. It allows them to be informed consumers, compare loan options effectively, and protect themselves against unfair practices.

In conclusion, TILA and Regulation Z provide essential safeguards for consumers in credit transactions. These regulations ensure transparency, fairness, and responsible lending practices. By understanding and complying with the requirements of these regulations, lenders and borrowers can work together to create a credit market that promotes transparency, protects consumers, and fosters financial well-being.