Introduction

The Truth in Lending Act (TILA) is a federal law in the United States aimed at protecting consumers when they engage in credit transactions. Enacted in 1968, TILA requires lenders to provide clear and accurate information about the terms and costs associated with borrowing money. By doing so, it promotes transparency and empowers consumers to make informed financial decisions.

Obtaining credit is common practice for individuals and businesses alike. Whether you’re applying for a mortgage, car loan, or using a credit card, it’s important to understand the terms and conditions of the credit agreement. TILA ensures that lenders and creditors adhere to certain disclosure requirements, enabling borrowers to compare offers and choose the best option for their needs.

Under TILA, lenders are obligated to disclose specific information to borrowers in a standardized format. This includes details about the annual percentage rate (APR), finance charge, total loan amount, payment schedule, and more. By providing this information, lenders can help borrowers assess the affordability, terms, and overall cost of the loan.

In this article, we will explore the various disclosure requirements mandated by the Truth in Lending Act. Understanding these requirements will empower consumers to make informed decisions when it comes to credit transactions. Let’s delve into the key aspects of TILA and how it affects borrowers and lenders alike.

What is the Truth in Lending Act?

The Truth in Lending Act (TILA), also known as Regulation Z, is a federal law designed to ensure that consumers receive clear and accurate information about the terms and costs associated with credit transactions. It was enacted in 1968 to promote transparency, fairness, and the informed use of credit.

TILA applies to a wide range of credit transactions, including loans, credit cards, and other forms of consumer credit. The law is administered and enforced by the Consumer Financial Protection Bureau (CFPB), which works to protect consumers from unfair, deceptive, or abusive lending practices.

The main objective of TILA is to provide consumers with information that allows them to compare credit offers and make informed decisions. By mandating certain disclosure requirements, the law ensures that lenders convey key information in a standardized format, making it easier for consumers to understand and compare loan terms.

One of the fundamental principles of TILA is the concept of “full disclosure.” This means that lenders must clearly and accurately disclose the terms and costs of a loan before the consumer is contractually obligated. The goal is to prevent consumers from being misled or surprised by hidden fees or unfavorable loan terms.

While TILA primarily focuses on the disclosure of financial terms, it also includes provisions to protect consumers from certain abusive practices. For example, the law prohibits lenders from making false statements in advertising or engaging in unfair practices such as unfair late fees or charging excessive interest rates.

Overall, the Truth in Lending Act plays a crucial role in promoting transparency and fairness in the credit market. By equipping consumers with the necessary information to understand borrowing costs and terms, TILA helps individuals make informed decisions and protects them from deceptive practices. Understanding the basics of TILA is essential for anyone engaging in credit transactions to ensure they are being treated fairly and have the information they need to make the best financial choices.

Disclosure Requirements

Under the Truth in Lending Act (TILA), lenders are required to disclose certain information to borrowers in a clear and understandable manner. These disclosure requirements ensure that consumers have the necessary information to make informed decisions when entering into credit transactions. Let’s explore the key disclosure requirements mandated by TILA:

- Annual Percentage Rate (APR): Lenders must disclose the annual percentage rate, or APR, which represents the cost of credit on an annual basis. The APR includes not only the interest rate, but also any additional fees or charges associated with the loan. This allows borrowers to compare the overall cost of credit across different lenders and loan options.

- Finance Charge: Lenders are required to disclose the finance charge, which is the total cost of credit expressed in dollars. It includes both the interest charged on the loan and any other fees or finance charges required by the lender. The finance charge provides borrowers with a clear understanding of the amount they will ultimately pay for borrowing money.

- Total Loan Amount: Lenders must disclose the total loan amount, which is the amount of money being borrowed. This includes both the principal, or the initial loan amount, and any finance charges or fees rolled into the loan. The total loan amount helps borrowers understand the full cost of the loan and the amount they will need to repay.

- Payment Schedule: Lenders must provide borrowers with a payment schedule, which outlines the number of payments, the amount of each payment, and the due dates. This allows borrowers to see how the loan will be repaid over time and helps them budget and plan their finances accordingly.

- Other Terms and Conditions: In addition to the above, TILA also requires lenders to disclose other important terms and conditions of the loan, such as any prepayment penalties, late payment fees, or changes to the interest rate over time. These disclosures ensure that borrowers are aware of all the key terms that may impact the cost and repayment of the loan.

It’s important to note that TILA requires lenders to provide these disclosures in a clear and understandable format. The information must be presented in a way that is easy to comprehend, allowing borrowers to make meaningful comparisons between loan offers. By providing these disclosures, TILA safeguards consumers against hidden fees, misleading terms, and other deceptive practices.

Understanding the disclosure requirements under TILA is crucial for borrowers. By carefully reviewing the provided information, individuals can confidently assess the affordability, terms, and overall cost of credit, enabling them to make informed decisions that align with their financial goals and needs.

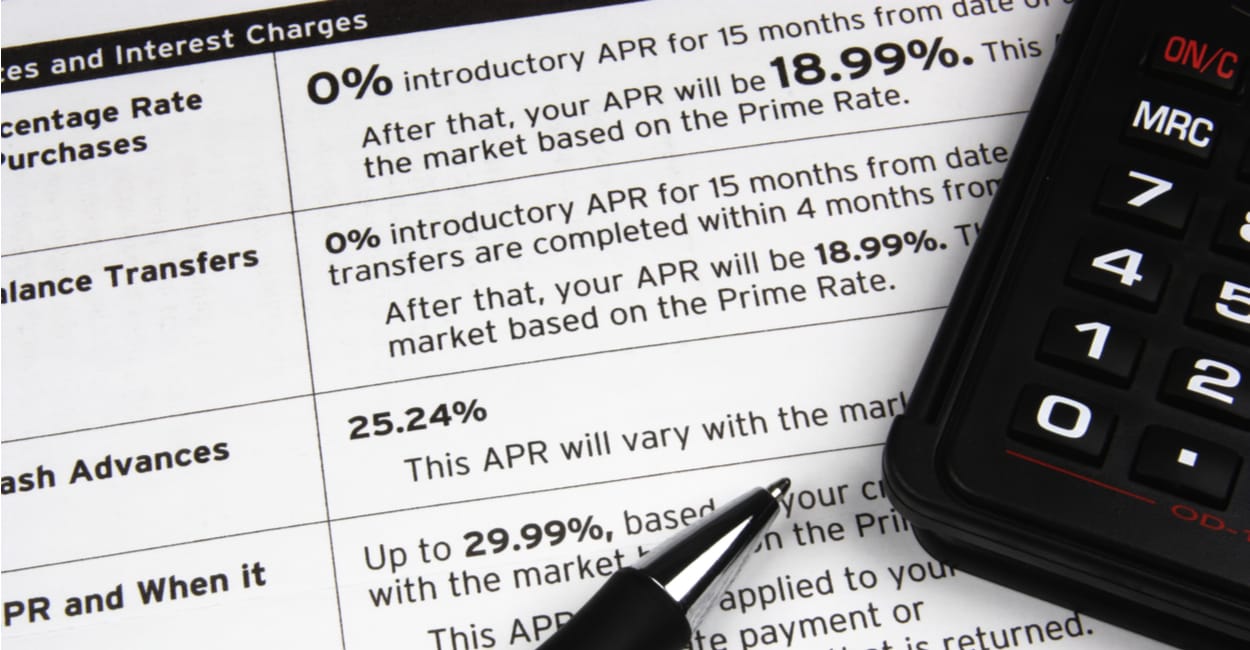

Annual Percentage Rate (APR)

When borrowing money, it’s important to have a clear understanding of the cost of credit. The Truth in Lending Act (TILA) requires lenders to disclose the Annual Percentage Rate (APR) to borrowers. The APR represents the annual cost of credit expressed as a percentage, taking into account not only the interest rate, but also any additional fees or charges associated with the loan.

The APR serves as a standardized measure that allows borrowers to compare the overall cost of credit across different lenders and loan products. By disclosing the APR, lenders provide borrowers with a transparent view of the total cost of borrowing.

Calculating the APR involves considering various factors, including the interest rate, loan term, and any additional fees or finance charges. This comprehensive approach enables borrowers to gain a complete understanding of the true cost of the loan, beyond just the interest rate.

For example, let’s assume a borrower is comparing two loan offers. Loan A has an interest rate of 5% with no additional fees, while Loan B has an interest rate of 4.5% but includes an origination fee and other charges. Without considering the fees, Loan B may seem like the better option based on the lower interest rate. However, when the APR is calculated, it takes into account the additional fees, providing a more accurate representation of the total cost of credit for each loan.

By comparing the APRs of Loan A and Loan B, the borrower can make a more informed decision about which loan truly carries a lower cost. The APR takes into consideration all relevant factors, allowing borrowers to see the complete picture and avoiding potential surprises down the line.

It’s important to note that while the APR is a valuable tool for comparing loan offers, it may not always capture the full cost of credit in certain situations. For example, loans with variable interest rates or complex payment structures may make calculating the exact APR more challenging. However, in most cases, the APR provides a reliable benchmark to assess the cost of borrowing.

By disclosing the APR, lenders comply with TILA’s requirements and provide borrowers with an essential piece of information for making informed financial decisions. It enables borrowers to compare loan offers on an apples-to-apples basis, assess affordability, and choose the option that best suits their needs and financial circumstances.

Finance Charge

When taking out a loan or using a credit card, it’s important to consider the total cost of credit, which goes beyond the interest rate. The Truth in Lending Act (TILA) requires lenders to disclose the finance charge to borrowers, providing a clear and comprehensive understanding of the total cost of borrowing.

The finance charge represents the total amount of money a borrower will pay in interest and any additional fees or finance charges associated with the loan. It is expressed in dollars rather than as a percentage like the Annual Percentage Rate (APR).

The finance charge includes various components, such as interest payments and fees charged by the lender. Additional fees can include origination fees, application fees, and any other charges imposed by the lender for processing and issuing the loan. It’s important for borrowers to be aware of all finance charges to accurately assess the cost of their credit.

By disclosing the finance charge, lenders enable borrowers to evaluate the overall cost of the loan, helping them make informed decisions about their credit options. This information allows borrowers to compare different loan offers and choose the most favorable terms for their financial situation.

Understanding the finance charge is crucial for borrowers, as it directly affects the total amount they will repay over the life of the loan. For example, a loan with a higher interest rate may result in a higher finance charge, increasing the overall cost of credit.

When comparing loan offers, it’s important for borrowers to consider both the Annual Percentage Rate (APR) and the finance charge. While the APR takes into account the interest rate and other fees, the finance charge provides a specific dollar amount that borrowers will pay in addition to the principal loan amount.

By knowing the finance charge, borrowers can accurately budget and plan their repayments. It allows them to understand the precise amount they will owe and make informed decisions regarding their finances.

Transparency in disclosing the finance charge is a crucial requirement under TILA. Lenders must provide this information to borrowers in a clear and understandable manner, ensuring that borrowers have the necessary knowledge to make informed choices when it comes to credit products.

By understanding the finance charge, borrowers can better evaluate the total cost of credit and select the most suitable borrowing options for their individual needs and financial circumstances.

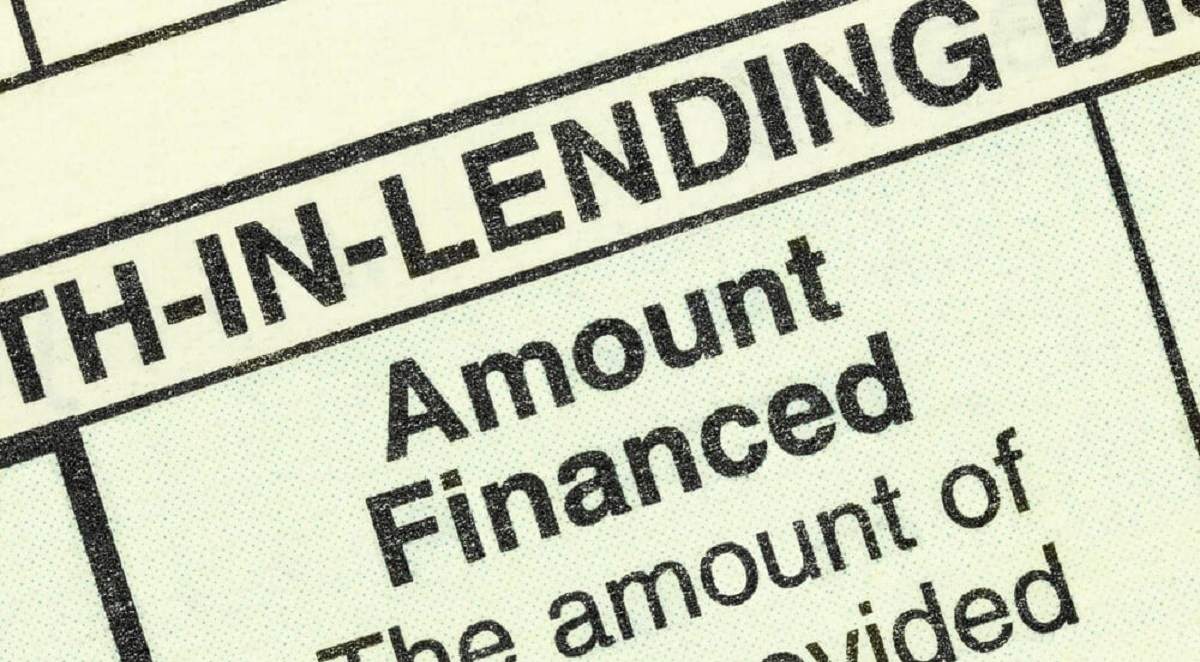

Total Loan Amount

When borrowing money, it’s essential to have a clear understanding of the total amount that will be borrowed, including both the principal loan amount and any additional fees or charges. The Truth in Lending Act (TILA) requires lenders to disclose the total loan amount to borrowers, ensuring transparency and allowing borrowers to evaluate the full cost of the loan.

The total loan amount represents the actual amount of money that will be disbursed to the borrower. It includes not only the principal loan amount but also any fees or charges rolled into the loan, such as origination fees, processing fees, or other financing costs.

By disclosing the total loan amount, lenders provide borrowers with a complete picture of the funds that will be available to them and enable them to make informed decisions.

Understanding the total loan amount is crucial because it directly impacts the amount that the borrower will need to repay over the life of the loan. By knowing the exact amount, borrowers can plan their budgets and manage their finances effectively.

Additionally, by disclosing the total loan amount, lenders ensure that borrowers can accurately compare loan offers from different providers. This information allows borrowers to assess the affordability of the loan and make informed decisions about taking on the debt.

It’s important for borrowers to review the total loan amount carefully and consider it in conjunction with other loan terms, such as interest rates, repayment periods, and monthly payment amounts. This holistic view will provide a clearer understanding of the overall cost of the loan and its impact on their financial situation.

Borrowers may also find it beneficial to compare the total loan amount with their own financial obligations and income to ensure that the loan is within their means to repay comfortably. Doing so can help prevent financial strain and ensure responsible borrowing.

By mandating the disclosure of the total loan amount, TILA aims to safeguard consumers from hidden costs and surprise fees. This requirement ensures that borrowers have the necessary information to assess the true cost of credit accurately and make informed borrowing decisions.

By understanding the total loan amount, borrowers can effectively budget and plan for the repayment of their loan, ensuring that they stay in control of their finances and make responsible borrowing choices.

Payment Schedule

When borrowing money, it’s important to understand the repayment terms, including the payment schedule. The Truth in Lending Act (TILA) requires lenders to disclose the payment schedule to borrowers, providing clarity and allowing borrowers to plan and budget their repayments.

The payment schedule outlines the timing and amount of each payment that the borrower is required to make throughout the loan term. It includes the number of payments, the frequency, and the due dates of those payments.

By disclosing the payment schedule, lenders ensure that borrowers have a clear understanding of their repayment obligations. This information allows borrowers to assess their ability to meet the payment requirements and plan their finances accordingly.

The payment schedule can vary depending on the type of loan and the lender’s terms. For example, a mortgage loan may have monthly payments over a 30-year term, while a car loan may have bi-weekly or monthly payments over a shorter period.

Understanding the payment schedule is crucial because it helps borrowers plan their budgets and ensure that they have sufficient funds to make the required payments on time. It allows individuals to align their income and expenses with the loan repayment obligations to avoid missing payments or facing financial difficulties.

Reviewing the payment schedule also provides borrowers with an opportunity to assess whether the proposed repayment plan aligns with their financial situation. It allows them to evaluate whether they can comfortably manage the payments and make adjustments if needed.

Additionally, the payment schedule provides clarity on the total number of payments required to repay the loan fully. This allows borrowers to determine the duration of their financial commitment and plan for any changes or life events that may occur during the loan term.

By disclosing the payment schedule, lenders comply with TILA’s requirement for transparency and consumer protection. This requirement ensures that borrowers have access to accurate information regarding their repayment obligations, enabling them to make informed decisions about their borrowing and budgeting priorities.

Understanding the payment schedule empowers borrowers to stay on track with their loan repayments and avoid default or late payment penalties. By adhering to the outlined schedule, borrowers can fulfill their financial obligations responsibly and maintain a positive credit history.

In summary, the payment schedule is a crucial element of loan disclosure, providing borrowers with the necessary information to plan and manage their repayment obligations effectively.

Right of Rescission

The Truth in Lending Act (TILA) grants borrowers a “Right of Rescission” for certain types of loans, providing an opportunity to cancel the loan agreement within a specified period. This right allows borrowers to carefully reconsider their decision and potentially withdraw from the loan without any penalties or fees.

The Right of Rescission applies specifically to certain types of transactions, including home equity loans, refinancing of a mortgage, or a home equity line of credit. The intention behind this provision is to protect homeowners by giving them time to review the loan terms, seek advice if needed, and make a well-informed decision about their financial commitment.

Under TILA, borrowers have a three-business-day window to exercise their Right of Rescission. This means they have three business days to provide written notice to the lender expressing their desire to cancel the loan agreement. If the borrower chooses to exercise this right, the loan is considered null and void, and any fees or charges imposed during that period must be refunded.

It’s important to note that the Right of Rescission does not apply to all types of loans. For example, it does not typically apply to traditional mortgages used to purchase a home. However, certain refinancing or home equity transactions may qualify.

By providing the Right of Rescission, TILA aims to give borrowers an opportunity to carefully consider their loan commitments and make informed decisions. It is designed to protect homeowners from potential high-pressure sales tactics or misleading loan terms that could have long-lasting financial implications.

Borrowers who are considering exercising their Right of Rescission should carefully review the loan documents, seek legal advice if necessary, and evaluate the potential consequences of canceling the loan. It’s important to understand that rescission may have implications on the borrower’s future borrowing ability or access to credit.

Lenders are required to provide borrowers with detailed information about the Right of Rescission, including the timeline and specific procedures for exercising this right. By providing this information, lenders comply with TILA’s requirements for customer protection and ensure that borrowers are aware of their rights and options.

Understanding the Right of Rescission empowers borrowers to make well-informed decisions and exercise control over their financial commitments. It gives homeowners the peace of mind and opportunity to carefully consider their loan agreements, ensuring that they are entering into a transaction that aligns with their financial goals and needs.

Advertising Disclosures

Under the Truth in Lending Act (TILA), lenders are required to provide clear and accurate information to consumers in their advertisements for credit products. This ensures that consumers can make informed decisions based on truthful representations and avoid deceptive practices.

TILA requires lenders to include specific disclosures in their advertisements to provide clarity and transparency about the terms and conditions of the credit being offered. These disclosures are intended to prevent misleading or deceptive advertising practices that could mislead consumers or conceal important information.

Some of the key advertising disclosure requirements under TILA include:

- Annual Percentage Rate (APR): Lenders must disclose the APR in their advertisements. This allows consumers to understand the cost of credit and make meaningful comparisons between different loan offers.

- Additional Charges: Lenders must disclose any additional fees or charges that may apply, including origination fees, application fees, or other costs associated with the loan.

- Terms and Conditions: Lenders must provide clear and accurate information about the key terms and conditions of the credit being advertised, such as the loan amount, repayment period, and any special features or limitations of the loan.

- Qualifications: In cases where specific qualifications or eligibility requirements apply, lenders must disclose these requirements in their advertisements to avoid misleading consumers.

- Trigger Terms: If an advertisement contains specific terms, such as the amount of down payment required or the number of payments, it may trigger additional disclosure requirements to provide further context and avoid confusion.

TILA’s advertising disclosure requirements promote fair competition and protect consumers from misleading or deceptive advertising practices. By providing clear and accurate information, lenders enable consumers to evaluate credit offers accurately and make informed decisions about their financial choices.

It’s important for consumers to pay attention to the disclosures provided in credit advertisements and carefully consider the terms and conditions before entering into any credit agreement. By understanding the information presented and asking questions if necessary, consumers can ensure that they are fully informed and protected when engaging in credit transactions.

Lenders must comply with TILA’s advertising disclosure requirements, and failure to do so can have legal consequences. The Consumer Financial Protection Bureau (CFPB) oversees compliance with TILA and takes action against lenders who engage in deceptive or unfair advertising practices.

By enforcing advertising disclosure requirements, TILA aims to create a fair and transparent marketplace where consumers can make informed decisions about credit products based on accurate and truthful information.

Penalties for Violations

The Truth in Lending Act (TILA) establishes penalties and remedies for lenders who violate its provisions. These penalties are in place to enforce compliance with the law and protect consumers from deceptive practices in the credit market.

For violations of TILA, both civil and criminal penalties can be imposed on lenders or creditors. The specific penalties depend on the nature and severity of the violation. Let’s explore some of the potential penalties for TILA violations:

- Civil Penalties: Lenders found in violation of TILA can face civil penalties, which are monetary fines imposed by regulatory authorities. These fines can vary depending on the number of violations, the harm caused to consumers, and other factors. The Consumer Financial Protection Bureau (CFPB) has the authority to enforce TILA and impose civil penalties on violators.

- Private Lawsuits: TILA allows consumers to file private lawsuits against lenders who violate the law. If a consumer prevails in such a lawsuit, they may be entitled to recover actual damages, statutory damages, and even attorney fees. This gives consumers an additional avenue for seeking redress and holding lenders accountable for violations.

- Recission Rights: In cases where lenders fail to provide the required disclosures or engage in other TILA violations, borrowers may have the right to rescind the loan. This means they can cancel the loan agreement and have any fees or charges refunded. Rescission rights act as a strong deterrence for lenders, as it nullifies the loan and can result in substantial financial consequences for them.

- Injunctions and Cease-and-Desist Orders: Regulatory authorities, such as the CFPB, can seek court orders to stop lenders from engaging in unlawful practices or to compel them to comply with TILA requirements. Injunctions and cease-and-desist orders are powerful tools to prevent further harm to consumers and ensure compliance with the law.

- Criminal Penalties: In egregious cases, criminal penalties may be pursued against lenders or individuals involved in TILA violations. These penalties can include fines and imprisonment. Criminal penalties are typically reserved for deliberate or fraudulent acts that significantly harm consumers.

The penalties and remedies under TILA are designed to deter lenders from engaging in unfair, deceptive, or abusive practices, and to provide avenues for consumers to seek relief. They play a crucial role in ensuring compliance with the law and protecting the rights of borrowers.

It’s important for lenders and creditors to understand their obligations under TILA to avoid penalties and comply with the law. By providing accurate and transparent disclosures, treating consumers fairly, and adhering to the requirements of TILA, lenders can maintain compliance and build trust with their customers.

Regulators, such as the CFPB, actively monitor the credit market and investigate potential violations of TILA. They play a critical role in upholding the law, enforcing penalties when necessary, and ensuring a level playing field for lenders and protection for consumers.

By establishing penalties for violations, TILA maintains the integrity of the credit market and supports fair and transparent practices that benefit both lenders and borrowers.

Conclusion

The Truth in Lending Act (TILA) serves as a vital protection for consumers in credit transactions. By requiring lenders to provide clear and accurate information about the terms and costs of borrowing, TILA promotes transparency, fairness, and informed decision-making. Understanding the key aspects of TILA is crucial for borrowers to ensure they are well-informed and empowered when entering into credit agreements.

We explored various aspects of TILA, starting with its purpose and significance. TILA’s disclosure requirements, such as the Annual Percentage Rate (APR), finance charge, total loan amount, payment schedule, and right of rescission, ensure that consumers have access to the necessary information to make informed decisions about credit transactions.

Through advertising disclosures, TILA aims to prevent misleading or deceptive practices, requiring lenders to provide accurate information about the terms and conditions of credit products in their advertisements. Furthermore, TILA establishes penalties and remedies for violations, ensuring accountability and protecting consumers from unfair practices.

By complying with TILA requirements, lenders create a fair and transparent credit market, fostering consumer trust and support. For borrowers, understanding TILA helps them assess loan offers, budget for repayments, and avoid hidden fees or unfavorable terms that can lead to financial difficulties.

It’s important for both lenders and borrowers to be aware of their rights and obligations under TILA. Lenders must comply with disclosure requirements, avoiding deceptive practices, and providing accurate information to borrowers. Borrowers, on the other hand, should carefully review the disclosures, ask questions if needed, and seek legal advice if they believe their rights under TILA have been violated.

Ultimately, TILA plays a crucial role in fostering transparency, fairness, and the informed use of credit. It empowers borrowers to make well-informed decisions, protects them from deceptive practices, and maintains the integrity of the credit market. By understanding and adhering to the provisions of TILA, lenders and borrowers alike contribute to a healthier and more equitable financial ecosystem.