Introduction:

The Truth in Lending Act (TILA), enacted by the U.S. Congress in 1968, is a federal law designed to protect consumers in their transactions with lenders and creditors. Under TILA, lenders are required to disclose important information about the terms and costs of credit before consumers enter into any agreements or contracts. One of the key components of TILA is the Schumer Box, named after former U.S. Senator Chuck Schumer, who advocated for clearer and more transparent credit card disclosures.

The Schumer Box is a standardized table that provides consumers with essential information about credit card offers, including interest rates, fees, and other terms and conditions. Its purpose is to make it easier for consumers to compare credit card offers and make informed decisions. In this article, we will delve into the details of the Schumer Box, its importance, and how to decipher the information it contains.

Understanding the Schumer Box is crucial for consumers who are considering applying for a credit card. By knowing how to interpret and analyze the information provided, they can better assess the cost and benefits of each credit card offer. In the following sections, we will break down the key components of the Schumer Box and explain the significance of each element.

It is important to note that while the Schumer Box is a useful tool for comparing credit card offers, it does have some limitations. We will also explore these limitations and discuss how consumers can go beyond the Schumer Box to make well-informed decisions when choosing a credit card.

What is the Truth in Lending Act?

The Truth in Lending Act (TILA) is a federal law that aims to protect consumers by requiring creditors to disclose key information about the terms and costs of credit. It was enacted by Congress in 1968 and is enforced by the Consumer Financial Protection Bureau (CFPB).

The purpose of TILA is to ensure that consumers have the necessary information to make informed decisions when dealing with lenders and creditors. Under this law, lenders are required to provide clear and understandable disclosures about credit terms and costs before consumers enter into any credit agreements or contracts.

TILA covers a wide range of credit transactions, including loans, credit cards, and lines of credit. It applies to both personal and household transactions, providing protections for individual consumers as well as small businesses.

One of the main goals of TILA is to promote transparency and prevent abusive practices in the lending industry. By mandating creditors to disclose important information upfront, TILA helps consumers understand the true cost of credit and avoid deceptive or unfair lending practices.

TILA requires lenders to disclose the following information in a clear and conspicuous manner:

- The annual percentage rate (APR): This is the cost of credit expressed as a yearly interest rate, which includes not only the interest charges but also certain fees and charges associated with the credit transaction.

- The finance charge: This is the total dollar amount that the credit will cost the consumer, expressed as a dollar amount.

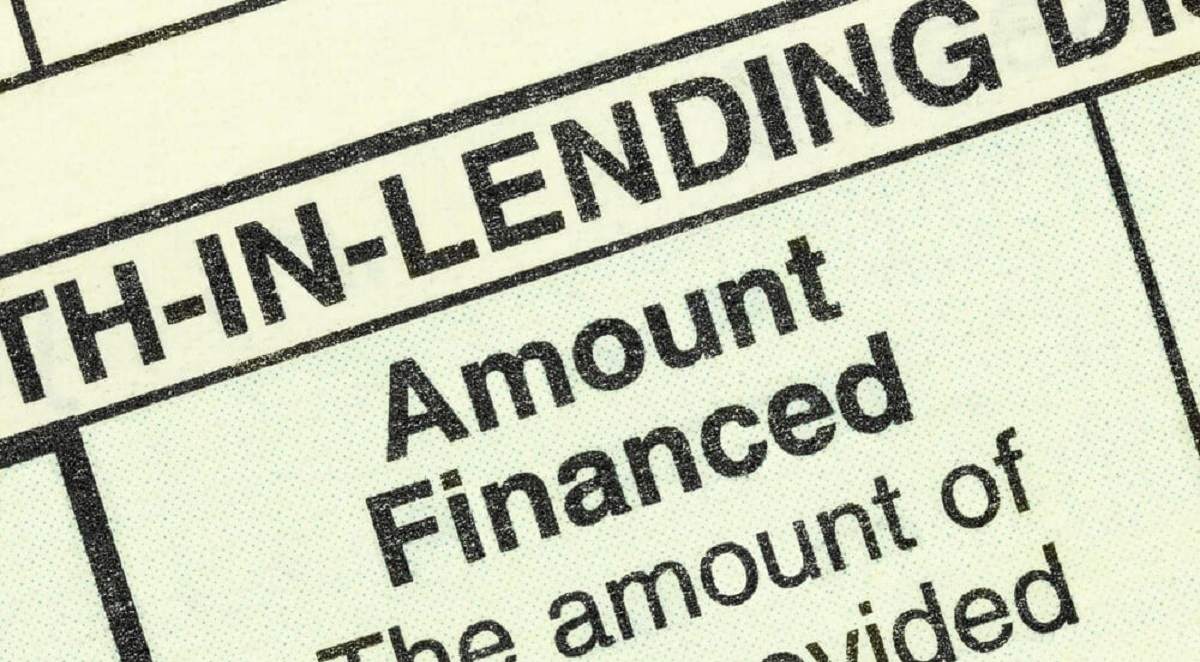

- The amount financed: This is the total amount of credit that is provided to the consumer.

- Total payments: This is the total amount that the consumer will have paid by the end of the credit term, including both principal and interest.

- The payment schedule: This includes the number of payments, the amount of each payment, and the due date of each payment.

In addition to these mandatory disclosures, TILA also regulates certain practices such as advertising, credit card billing, and credit card account management. It provides consumers with rights and remedies in case of violations and promotes fair treatment in credit transactions.

Overall, the Truth in Lending Act plays a crucial role in safeguarding consumer interests and ensuring transparency in the lending marketplace. By providing consumers with clear and concise information regarding credit terms and costs, TILA empowers individuals to make informed decisions about borrowing and using credit.

What is a Schumer Box?

A Schumer Box, named after former U.S. Senator Chuck Schumer, is a standardized table that provides consumers with essential information about credit card offers. It is a key component of the Truth in Lending Act (TILA), designed to make credit card terms and conditions more transparent and easily understandable.

The Schumer Box is typically found in credit card solicitations, applications, and account disclosures. Its purpose is to summarize, in a standardized format, the key terms and costs associated with the credit card offer. It allows consumers to compare different credit card offers side by side and make informed decisions on which card best suits their needs.

The Schumer Box is typically located in a prominent position within the credit card document, making it easily accessible for consumers. It contains information that is required by law to be disclosed in a clear and conspicuous manner.

The layout of the Schumer Box is structured and consistent, regardless of the credit card issuer. Its standardized format ensures that consumers can quickly locate and understand the important terms and costs associated with the credit card offer.

The key components of the Schumer Box include:

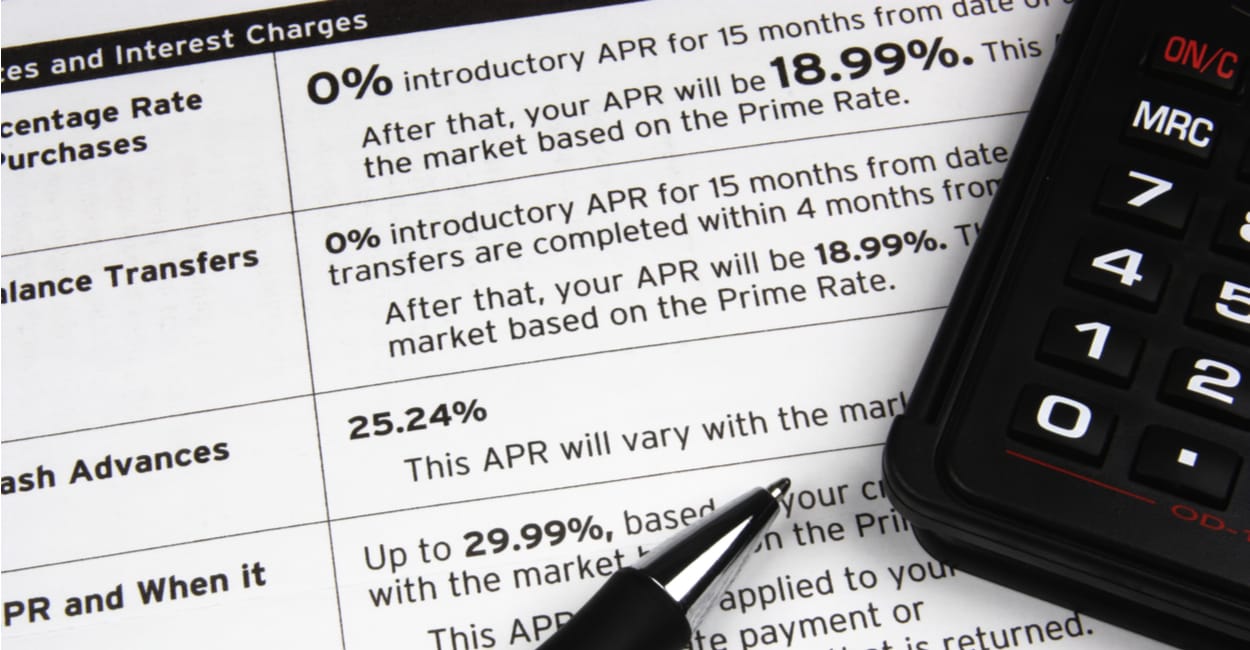

- Annual Percentage Rate (APR): This is the interest rate that will be applied to the outstanding balance on the credit card. It may include different APRs for purchases, balance transfers, and cash advances.

- Minimum Finance Charge: This is the minimum charge that will be applied if the consumer carries a balance from month to month. It is typically a small fee that is added to the account if the calculated finance charge is lower than the minimum.

- Annual Fee: Some credit cards may charge an annual fee for the privilege of having the card. This fee is disclosed in the Schumer Box.

- Transaction Fees: Certain credit card transactions, such as balance transfers or cash advances, may incur additional fees. These fees are clearly stated in the Schumer Box.

- Grace Period: The Schumer Box specifies whether the credit card offers a grace period, which is a period of time during which no interest is charged on new purchases.

- Penalty APR and Fees: If a consumer fails to make payments on time, the credit card issuer may impose a penalty APR and associated fees. These are disclosed in the Schumer Box.

Having this information presented in a standardized format allows consumers to easily compare credit card offers and understand the costs and terms associated with each offer. It helps them make informed decisions based on their financial needs and preferences.

The Schumer Box is an important tool that promotes transparency in the credit card industry and empowers consumers to choose the credit card that best aligns with their financial goals and responsibilities.

Understanding the Schumer Box

The Schumer Box is a standardized table that provides consumers with crucial information about credit card offers. By understanding the components and purpose of the Schumer Box, consumers can make more informed decisions when choosing a credit card that best suits their financial needs.

At first glance, the Schumer Box may appear overwhelming or confusing due to the various terms and numbers presented. However, breaking down the elements within the Schumer Box can help consumers understand the significance of each piece of information.

One of the key components to understand in the Schumer Box is the Annual Percentage Rate (APR). The APR reflects the annual cost of borrowing, including both the interest rate and any additional fees associated with the credit card. It is important for consumers to pay attention to the different APRs listed in the Schumer Box, as they may vary depending on the type of transaction, such as purchases, balance transfers, or cash advances.

Another important aspect of the Schumer Box is the minimum finance charge. This fee is triggered when a consumer carries a balance from month to month. By understanding this charge, consumers can better manage their credit card usage and make informed decisions about paying their balances in full or carrying a balance.

Credit card fees are also outlined in the Schumer Box. These fees may include an annual fee, which is an amount charged yearly for possessing the credit card, as well as transaction fees for specific actions like balance transfers or cash advances. Knowing the fees associated with a credit card offer helps consumers assess the overall cost and determine if the benefits outweigh the additional charges.

The Schumer Box also provides information on the grace period, which is the timeframe during which no interest is charged on new purchases. Understanding the grace period helps consumers plan their payments and avoid unnecessary interest charges.

In addition, the Schumer Box highlights penalty APRs and associated fees. These are applied by credit card issuers when a consumer fails to make payments on time. Being aware of these penalties empowers consumers to prioritize timely payments and avoid expensive repercussions.

By comprehending the contents of the Schumer Box, consumers can make apples-to-apples comparisons between credit card offers. It enables them to evaluate the costs, fees, and terms of each card and choose the one that best aligns with their financial goals and spending habits.

While the Schumer Box provides essential information, consumers should also read the complete terms and conditions of the credit card offer. This ensures they have a comprehensive understanding of all the provisions and requirements before making a decision.

Ultimately, understanding the Schumer Box enables consumers to navigate the credit card market with confidence and make informed choices when selecting a credit card that suits their needs.

Key components of the Schumer Box

The Schumer Box, a standardized table found in credit card offers, contains several key components that provide essential information for consumers. By understanding these components, consumers can effectively compare credit card offers and make informed decisions regarding their financial choices.

1. Annual Percentage Rate (APR): The APR is the interest rate charged on outstanding credit card balances. It is crucial to pay attention to the APR as it directly impacts the cost of borrowing. The Schumer Box typically presents different APRs for various types of transactions, such as purchases, balance transfers, and cash advances.

2. Minimum Finance Charge: The minimum finance charge is the smallest fee a credit card issuer can charge if a consumer carries a balance from month to month. It is important to note this charge, as it may affect the overall cost of credit for those who do not pay their balances in full every month.

3. Annual Fee: Some credit cards may entail an annual fee simply for the privilege of having the card. This fee varies among different credit card offers and should be considered when evaluating the overall value of the card.

4. Transaction Fees: The Schumer Box also includes information about transaction fees, such as balance transfer fees or cash advance fees. These fees are additional charges incurred for specific credit card transactions and should be carefully assessed to ensure they align with the consumer’s financial needs and habits.

5. Grace Period: The grace period indicates the time during which interest is not charged on new purchases. Understanding the presence or absence of a grace period is important as it can impact interest calculations and payment strategies.

6. Penalty APR and Fees: The Schumer Box highlights the penalty APR and any associated fees that may be imposed by the credit card issuer for late payments or other violations of the credit card agreement. Being aware of potential penalty charges can motivate consumers to adhere to payment deadlines and avoid unnecessary expenses.

These key components of the Schumer Box provide consumers with critical information necessary to evaluate credit card offers effectively. By comparing APRs, fees, grace period availability, and potential penalties, consumers can make informed choices that align with their financial goals and circumstances.

It is important to note that while the Schumer Box simplifies the presentation of these components, consumers should also review the full terms and conditions of the credit card offer. This ensures a comprehensive understanding of the obligations, benefits, and limitations associated with the credit card before making a decision.

By carefully considering the key components of the Schumer Box, consumers can gain clarity and confidence in selecting a credit card that suits their needs and helps them achieve their financial objectives.

Importance of the Schumer Box

The Schumer Box plays a crucial role in promoting transparency and empowering consumers when it comes to choosing a credit card. Its standardized format and inclusion of key information allow consumers to make informed decisions and avoid potential pitfalls. Understanding the importance of the Schumer Box helps individuals navigate the complex landscape of credit card offers.

One of the primary benefits of the Schumer Box is its ability to provide consumers with a quick and clear overview of the most important terms and costs associated with a credit card offer. By presenting this information in a standardized format, the Schumer Box enables consumers to compare multiple credit card offers side by side, making it easier to assess the benefits, costs, and potential risks of each card.

Another important aspect of the Schumer Box is its role in promoting transparency in the credit card industry. By mandating that credit card issuers disclose key information in a clear and conspicuous manner, the Schumer Box ensures that consumers have access to essential details about interest rates, fees, and other terms and conditions. This transparency helps individuals avoid surprises and make informed decisions that align with their financial goals.

The Schumer Box also empowers consumers to evaluate and understand the true cost of credit. By clearly displaying the Annual Percentage Rate (APR), minimum finance charge, annual fees, and any transaction fees, consumers can assess the overall cost of borrowing with a particular credit card. This information enables consumers to evaluate the value and affordability of a credit card offer.

In addition to cost considerations, the Schumer Box highlights important details such as the presence of a grace period and potential penalties. This information empowers consumers to manage their credit responsibly and make timely payments. Understanding the consequences and rewards associated with the credit card offer helps individuals avoid unnecessary interest charges and potential fees.

The Schumer Box also reinforces consumer protection by providing individuals with the necessary information to combat deceptive or unfair practices. By ensuring that credit card issuers disclose comprehensive terms, costs, and risks, the Schumer Box helps consumers identify any misleading claims or hidden charges. This transparency helps individuals make sound financial decisions and guards against potential exploitation.

Overall, the Schumer Box is of significant importance as it enhances transparency, enables informed decision-making, and safeguards consumer interests in the credit card market. By understanding and utilizing the information contained in the Schumer Box, consumers can navigate the complexities of credit card offers with confidence and select the cards that best align with their financial needs and goals.

How to read a Schumer Box

Understanding how to read and interpret the information presented in a Schumer Box is crucial for consumers who want to make informed decisions when choosing a credit card. By following these steps, individuals can navigate a Schumer Box with ease and gain a comprehensive understanding of the terms and costs associated with a credit card offer.

1. Familiarize Yourself with the Layout: The Schumer Box is typically presented in a standardized format, making it easy to locate and review key information. Take a moment to familiarize yourself with the layout, which often includes headings and columns to display different details.

2. Identify the Annual Percentage Rate (APR): The APR is one of the most important components of the Schumer Box. It represents the interest rate charged on outstanding balances and indicates the cost of borrowing. Pay attention to the different APRs listed for various transactions, such as purchases, balance transfers, and cash advances.

3. Check for a Minimum Finance Charge: Look for the minimum finance charge, which is the smallest fee that can be charged if you carry a balance from month to month. This charge is relevant if you do not pay your credit card balance in full each billing cycle.

4. Note Any Annual Fees: Some credit cards may come with an annual fee, which is an amount charged yearly for holding the card. Take note of whether a credit card offer includes an annual fee and consider this cost when evaluating the overall value of the credit card.

5. Pay Attention to Transaction Fees: The Schumer Box will outline any additional fees associated with specific transactions, such as balance transfers or cash advances. Be aware of these transaction fees, as they can contribute to the overall cost of using the credit card.

6. Determine the Grace Period: Look for information on the grace period, which is the timeframe during which no interest is charged on new purchases. Knowing the presence or absence of a grace period allows you to plan your payments and avoid unnecessary interest charges.

7. Be Mindful of Penalty APRs and Fees: The Schumer Box will specify if there are penalty APRs and any associated fees that may be incurred for late payments or other violations of the credit card agreement. Understanding these penalties is essential for ensuring responsible credit card usage.

Remember to also read the full terms and conditions of the credit card offer, as the Schumer Box provides a summary of key details. The terms and conditions will provide additional information about the credit card, including payment allocation, dispute resolution, and any applicable rewards or benefits.

By following these steps and carefully reviewing the information presented in the Schumer Box, consumers can make informed decisions about credit card offers. Understanding the terms, costs, and potential risks enables individuals to choose the credit card that aligns with their financial goals and responsibilities.

Limitations of the Schumer Box

While the Schumer Box serves as a valuable tool for consumers to compare credit card offers, it is important to recognize its limitations. Although it provides essential information, there are certain factors that the Schumer Box may not fully convey, which consumers should be aware of when evaluating credit card options.

1. Personalized Interest Rates: The Schumer Box typically provides a range of APRs for different types of transactions. However, the actual interest rate offered to an individual may vary based on their creditworthiness. The specific APR assigned to a consumer may be higher or lower than the range displayed in the Schumer Box, depending on their credit history, income, and other factors determined by the credit card issuer.

2. Credit Limit: The Schumer Box does not include information about the credit limit that will be assigned to a consumer. The credit limit determines the maximum amount that can be charged on the credit card. It is an important consideration for individuals who have specific spending needs or want to avoid exceeding their credit limit.

3. Rewards and Benefits: The Schumer Box may not provide detailed information about the rewards programs or additional benefits associated with a credit card offer. These can include cash back rewards, travel rewards, purchase protections, or extended warranty coverage. Consumers should refer to the credit card’s terms and conditions or supplementary materials to understand the full scope of the rewards and benefits offered.

4. Special Promotional Offers: If a credit card offer includes special promotional rates or limited-time offers, the Schumer Box may not fully capture these terms. Consumers should carefully review the terms and conditions accompanying the offer to understand the specific requirements and duration of any promotional deals.

5. Comprehensive Fees: While the Schumer Box does outline some transaction fees, it may not disclose all potential charges that could be incurred. Additional fees such as foreign transaction fees, over-limit fees, or penalty fees for specific activities may be specified in the terms and conditions but might not be captured in the summarized format of the Schumer Box.

6. Consumer Circumstances: The Schumer Box does not consider individual financial circumstances, goals, or preferences. While it provides standardized information for comparison, consumers should evaluate credit card offers based on their specific needs, spending habits, and financial situation.

Despite these limitations, the Schumer Box remains a valuable tool for consumers to assess and compare credit card offers. It provides a transparent and standardized format for displaying key information, which allows individuals to make more informed decisions. However, it is important for consumers to not solely rely on the Schumer Box and to read the full terms and conditions of an offer to truly understand all aspects of the credit card.

Conclusion

The Schumer Box, a standardized table included in credit card offers, plays a vital role in promoting transparency and empowering consumers when it comes to choosing a credit card. By providing essential information in a clear and concise format, the Schumer Box enables individuals to compare credit card offers and make informed decisions based on their financial needs and preferences.

The significance of the Schumer Box lies in its ability to simplify complex credit card terms and costs, making it easier for consumers to understand and evaluate different options. By presenting information such as the APR, minimum finance charge, annual fees, and transaction fees, the Schumer Box helps consumers assess the overall cost of using a credit card, enabling a more accurate comparison between offers.

Furthermore, by highlighting the presence or absence of a grace period, penalty APRs, and associated fees, the Schumer Box empowers individuals to manage their credit responsibly and avoid unnecessary interest charges or penalties.

However, it is important to recognize the limitations of the Schumer Box. Individual interest rates, credit limits, rewards programs, and specific fees may not be fully captured in the standardized format. To gain a comprehensive understanding of a credit card offer, consumers should review the full terms and conditions accompanying the Schumer Box.

In conclusion, the Schumer Box serves as a valuable tool for consumers to navigate the credit card market. By understanding how to read and interpret the information presented in the Schumer Box, individuals can make well-informed decisions, select the credit card that aligns with their financial goals, and effectively manage their credit. Ultimately, the Schumer Box promotes transparency, empowers consumers, and helps individuals make financially sound choices when it comes to credit cards.