Introduction

Welcome to the world of banking, where trust and security are paramount. In order to safeguard the integrity of the financial system and protect against fraudulent activities, banks have implemented various procedures and protocols. One of the most crucial aspects of banking operations is conducting customer due diligence.

Customer due diligence, often referred to as CDD, is a process that banks and financial institutions undertake to verify and understand the identity of their customers. By conducting thorough due diligence, banks can ensure that they are dealing with legitimate individuals or entities and mitigate the risk of financial crime.

Over the years, customer due diligence has become increasingly important in the banking industry. With the rise in sophisticated money laundering schemes, terrorist financing, and other criminal activities, banks face substantial regulatory pressure to implement robust due diligence practices.

The objective of customer due diligence is multifaceted. First and foremost, it allows banks to comply with stringent regulations and follow anti-money laundering (AML) and Know Your Customer (KYC) guidelines. These regulations aim to prevent money laundering and terrorist financing by identifying and verifying customers’ identities, understanding the nature of their financial dealings, and monitoring for suspicious activities.

Moreover, customer due diligence helps banks maintain a trustworthy relationship with their clients. By ensuring the validity of customer information, banks can reduce the risk of identity theft and fraudulent transactions. Additionally, it allows banks to better understand their customers’ financial needs and provide tailored services.

In the following sections, we will delve deeper into the concept of customer due diligence in banking. We will explore the three stages of the due diligence process, discuss the role of technology in enhancing these procedures, and highlight key regulations and compliance requirements. Furthermore, we will examine best practices for implementing customer due diligence to ensure its effectiveness within the banking industry.

Let’s embark on this insightful journey to understand the significance of customer due diligence and the vital role it plays in the world of banking.

What is Customer Due Diligence?

Customer due diligence (CDD) is a process performed by banks and financial institutions to assess and verify the identity and background of their customers. It is a crucial step in the anti-money laundering and counter-terrorism financing efforts of the financial industry.

The primary objective of customer due diligence is to mitigate the risk of financial crimes, such as money laundering, fraud, and terrorist financing. By conducting due diligence, banks can gather relevant information about their customers and assess the potential risks associated with them.

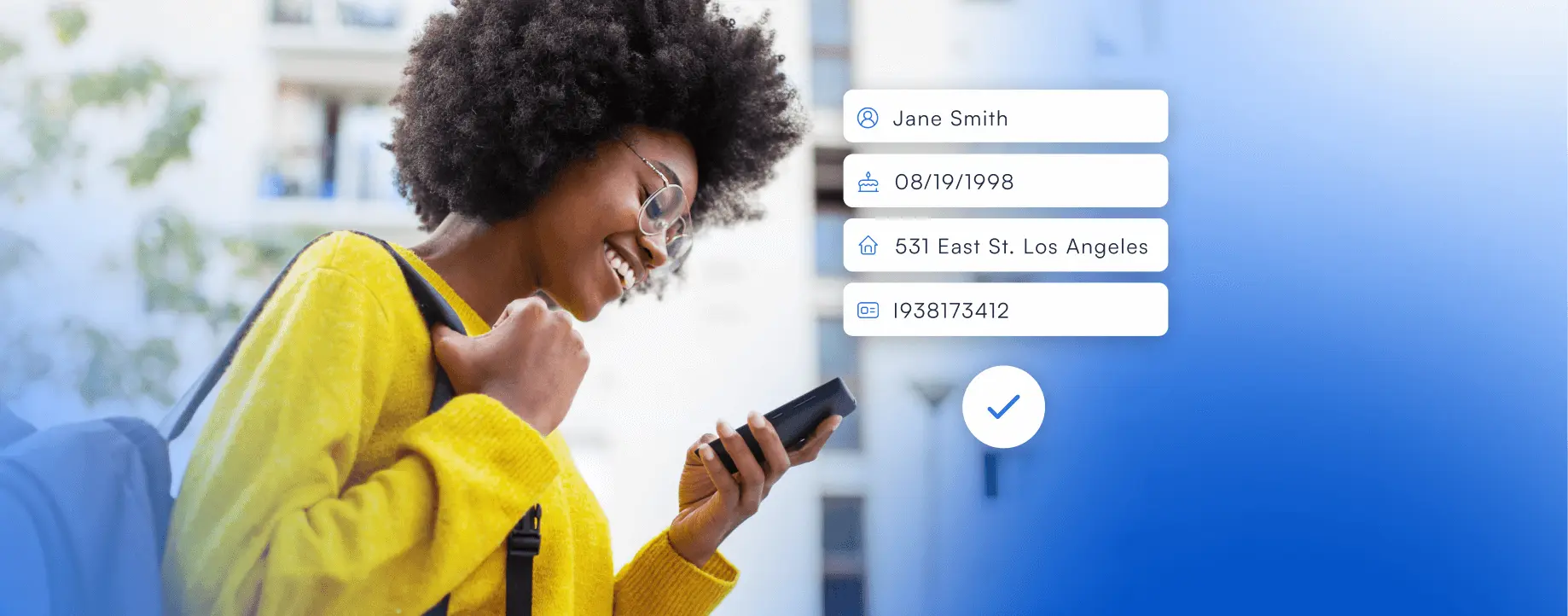

In the context of customer due diligence, gathering customer information involves collecting personal and financial details, such as name, address, date of birth, occupation, source of funds, and beneficial ownership. Banks also use various identification documents, such as passports or government-issued identification cards, to verify the identity of their customers.

Customer due diligence is a multi-step process that involves three main stages: customer identification, customer verification, and monitoring and ongoing due diligence.

The first stage, customer identification, involves collecting basic information about the customer, such as their name, address, and date of birth. This step is crucial for establishing the customer’s identity and ensuring they are not involved in any illegal activities.

The second stage, customer verification, is the process of verifying the information provided by the customer. Banks use various methods for verification, including document checks, online verification services, and interaction with the customer through face-to-face meetings or video conferencing.

The third stage, monitoring and ongoing due diligence, is an ongoing process where banks monitor customer transactions and activities for any suspicious or unusual behavior. This includes keeping track of changes in customer profiles, monitoring large transactions, and conducting periodic reviews to ensure the integrity of the customer relationship.

Effective customer due diligence relies on the use of technology to streamline the process and enhance its accuracy. Banks utilize automation tools, artificial intelligence, and data analytics to efficiently gather and analyze customer data, identify potential risks, and detect suspicious activities.

Customer due diligence is not only a regulatory requirement but also a means for banks to establish trust, maintain the integrity of their operations, and protect themselves and their customers from financial crimes. It is an essential part of establishing and nurturing a strong and sustainable relationship between banks and their customers.

By implementing robust customer due diligence processes, banks can ensure compliance with regulations, protect their reputation, and contribute to the overall stability and security of the financial system.

Why is Customer Due Diligence Important in Banking?

Customer due diligence (CDD) plays a critical role in the banking industry for several compelling reasons. From mitigating the risk of financial crimes to maintaining regulatory compliance and building trust with customers, the importance of customer due diligence cannot be overstated.

One of the primary reasons why customer due diligence is crucial in banking is its role in preventing money laundering and terrorist financing. By verifying the identity of customers and understanding their financial activities, banks can identify and report any suspicious transactions or behaviors to the relevant authorities. This helps in the global fight against illicit activities and contributes to maintaining the integrity of the financial system.

Besides preventing financial crimes, customer due diligence helps banks comply with strict regulatory requirements, particularly in relation to anti-money laundering (AML) and Know Your Customer (KYC) regulations. Regulatory bodies across the world have imposed stringent guidelines to ensure that banks conduct thorough due diligence on their customers. Failure to comply with these regulations can result in hefty fines, reputational damage, and even legal consequences for financial institutions.

Moreover, implementing effective customer due diligence practices allows banks to establish a reliable system for assessing the risk associated with their customers. By gathering comprehensive information about the customer’s background, their sources of funds, and their financial activities, banks can evaluate the level of risk involved in maintaining a relationship with that customer. This risk assessment is vital for determining the appropriate level of monitoring and control measures required to mitigate potential risks.

Customer due diligence is also essential in building trust and maintaining a strong relationship with customers. In an era where identity theft, fraud, and cybercrimes are prevalent, customers expect their banks to prioritize their safety and protect their personal and financial information. By conducting thorough due diligence, banks demonstrate their commitment to safeguarding their customers’ interests, supporting transparency, and fostering trust.

Furthermore, an effective customer due diligence process enables banks to better understand their customers’ financial needs and tailor their services accordingly. By gathering information on customers’ financial goals, risk tolerance, and investment preferences, banks can personalize their offerings and provide tailored solutions that meet their customers’ unique requirements. This enhances the overall customer experience and strengthens the bank-customer relationship.

In summary, customer due diligence is vital in banking because it helps prevent financial crimes, ensures regulatory compliance, assesses risk, builds trust with customers, and enables personalized service delivery. It is a critical component of safeguarding the integrity of the financial system and creating a secure environment for both banks and their customers.

The Three Stages of Customer Due Diligence

Customer due diligence (CDD) is a comprehensive process that involves three distinct stages to verify the identity and assess the risks associated with banking customers. These stages are customer identification, customer verification, and monitoring and ongoing due diligence.

The first stage of customer due diligence is customer identification. During this stage, banks collect basic information from customers, such as their name, address, date of birth, and contact details. This information helps establish the identity of the customer and ensures that they are not involved in any illicit activities. Banks may also request additional documentation, such as passports or government-issued identification cards, to validate the customer’s identity.

The second stage is customer verification, which is the process of confirming the information provided by the customer. Banks utilize various verification methods to ensure the accuracy and authenticity of customer details. This may include document checks, where the bank verifies the validity of identification documents and other supporting materials provided by the customer. Additionally, banks may use online identity verification services, which leverage technology and databases to confirm the customer’s identity.

In some cases, banks may engage in face-to-face meetings or video conferencing with the customer to further verify their identity. These interactions allow bank representatives to compare the customer’s physical appearance with the information provided and ask additional questions to establish the legitimacy of the customer and their financial activities.

The third stage of customer due diligence is monitoring and ongoing due diligence. This stage aims to ensure that the customer’s activities remain consistent with their declared profile and that no suspicious or unusual behavior is detected. Banks employ various monitoring mechanisms to achieve this, such as automated systems that track customer transactions for any signs of money laundering, fraudulent activity, or other financial crimes.

Monitoring and ongoing due diligence involve periodic reviews of customer accounts and activities. Banks assess any changes in customer behavior, such as large transactions, sudden changes in transaction patterns, or discrepancies in financial information provided. By conducting regular reviews, banks can identify and investigate any potential red flags, enabling them to take appropriate action to mitigate risks.

It is crucial for banks to maintain up-to-date customer records and conduct ongoing due diligence, as the risk profile of customers can change over time. Changes in a customer’s personal circumstances, business operations, or financial activities may affect their risk level. Therefore, continuous monitoring and regular reviews are vital to ensure that banks are aware of any changes and can promptly respond to mitigate potential risks.

The three stages of customer due diligence work together to create a comprehensive process that enables banks to verify customer identities, assess the risks associated with serving those customers, and monitor their activities for any suspicious behavior. By implementing these stages effectively, banks can enhance their compliance with regulatory requirements, reduce the risk of financial crimes, and build trusted relationships with their customers.

Stage 1: Customer Identification

The first stage of customer due diligence (CDD) is customer identification, which is a crucial step in the verification process for banks. This stage involves collecting basic information from customers to establish their identity and ensure compliance with regulatory requirements.

During customer identification, banks gather essential details such as the customer’s full name, address, date of birth, and contact information. This information serves as the foundation for verifying the customer’s identity and conducting further due diligence. Banks may also request additional information, such as occupation, source of funds, and other relevant details if required by law or bank policy.

Banks use various channels and methods to collect customer identification information. This can include online application forms, in-person meetings, or electronic record systems. Regardless of the channel, banks must ensure that the collected information is accurate and reliable.

To validate the customer’s identity, banks often rely on identification documents, such as passports, driver’s licenses, or government-issued identification cards. These documents provide official proof of identity and allow banks to link the provided information to a specific individual.

Additionally, banks may request supporting documents that further substantiate the customer’s identity. These documents can include utility bills, bank statements, or other official documents that show the customer’s name and residential address. Verification of these supporting documents adds an extra layer of assurance to the identification process.

Customer identification is not only important for verifying the accuracy of customer-provided information, but it also helps banks comply with Know Your Customer (KYC) regulations. These regulations require banks to have a clear understanding of their customers and their financial activities to prevent money laundering, terrorist financing, and other fraudulent activities.

By establishing the identity of their customers, banks can better assess the risk associated with each customer and tailor their services accordingly. Additionally, customer identification enables banks to create comprehensive customer profiles, facilitating future interactions and providing a foundation for ongoing due diligence.

Customer identification is an essential step in the customer due diligence process, ensuring the legitimacy and integrity of banking relationships. By collecting accurate and verified identification information, banks can reduce the risk of fraudulent activities and contribute to a more secure financial environment.

Stage 2: Customer Verification

Following customer identification, the next crucial stage of customer due diligence (CDD) in banking is customer verification. This stage involves validating the information collected during the identification process in order to ensure the accuracy and authenticity of customer details.

Customer verification is a critical step as it helps banks confirm the identity of their customers and detect any potential fraudulent activities. It serves as a safeguard against identity theft, false identities, and other illicit practices, contributing to a more secure banking environment.

Banks employ various methods and techniques to verify customer information. One commonly utilized method is document checks, where banks examine the authenticity and validity of identification documents provided by the customer. This involves verifying the document’s security features, cross-checking it against databases or official records, and ensuring that it has not been tampered with.

Online verification services are also commonly used by banks to validate customer information. These services leverage advanced technology and data sources to verify identity information provided by the customer. Through comparison algorithms and data matching, banks can determine the accuracy and reliability of customer-provided details.

In some cases, banks may conduct face-to-face meetings or video conferences as part of the verification process. These interactions allow bank representatives to personally verify the customer’s identity by matching their physical appearance to the identification documents provided. It also provides an opportunity to ask additional questions to further validate the customer’s information.

Customer verification is not limited to confirming identity alone. In certain situations, banks may also verify the legitimacy of the customer’s source of funds. This involves assessing the origin and legitimacy of the money being used for banking transactions. By verifying the source of funds, banks can ensure that the customer’s financial activities are not associated with illegal activities.

Verification is a continuous process throughout the customer relationship. Banks periodically review and re-verify customer information to ensure that it remains accurate and up to date. This helps banks maintain compliance with regulatory requirements and stay proactive in identifying any changes or discrepancies that may indicate potential risks.

The customer verification stage is vital for banks to establish the trustworthiness and credibility of their customers. It helps protect the financial institution and its clients from potential fraud, money laundering, and other illicit activities. By conducting thorough verification, banks can build a secure and reliable banking environment for both themselves and their customers.

Stage 3: Monitoring and Ongoing Due Diligence

Once the initial stages of customer due diligence (CDD) are complete, the third and equally important stage begins: monitoring and ongoing due diligence. This stage involves the continuous monitoring of customer activities and maintaining a vigilant approach to identify any suspicious or unusual behavior.

Monitoring and ongoing due diligence play a critical role in keeping banks aware of changes in customer profiles, identifying red flags, and ensuring long-term compliance with regulations. These proactive measures help banks mitigate risks, prevent financial crimes, and maintain the integrity of their operations.

The monitoring process involves tracking and analyzing customer transactions and activities on an ongoing basis. Banks employ advanced technology and automated systems to monitor large volumes of data and detect any unusual patterns or anomalies. These systems are designed to identify potential money laundering activities, terrorist financing, fraud, and other illicit practices.

Additionally, banks conduct periodic reviews of customer accounts to assess the ongoing validity and accuracy of customer information. This involves requesting updated documentation or conducting follow-up checks to confirm the customer’s identity and legitimacy. By conducting these reviews, banks ensure that customer profiles remain up to date and aligned with their risk assessment practices.

Monitoring and ongoing due diligence extend beyond the verification of customer details. Banks also monitor and assess customer transactions based on their risk profile. Unusual or high-value transactions may trigger alerts and require additional scrutiny. Banks investigate and analyze these transactions to determine if they are legitimate or potentially indicative of illicit activities.

Furthermore, banks maintain close communication with customers to promptly address any concerns or questions that may arise. They have a responsibility to educate customers about their due diligence procedures and the importance of complying with regulatory requirements. This ongoing communication fosters a strong relationship with customers and strengthens their awareness about the bank’s commitment to maintaining a secure financial environment.

Regular training and education for bank employees are also essential for effective monitoring and ongoing due diligence. Employees need to stay informed about the latest trends and techniques used in financial crimes to recognize suspicious activities and respond proactively. By equipping employees with the necessary knowledge and tools, banks can enhance their ability to mitigate risks and ensure compliance.

The monitoring and ongoing due diligence stage is continuous throughout the entire banking relationship with customers. It allows banks to remain vigilant, adapt to changing circumstances, and adjust their risk assessment accordingly. This proactive approach helps banks identify and address potential risks before they escalate into more significant issues.

By implementing robust monitoring and ongoing due diligence processes, banks demonstrate their commitment to combating financial crime, protecting their customers, and maintaining a secure financial system. It is an essential step in mitigating risks, enhancing regulatory compliance, and preserving the integrity of the banking industry.

The Role of Technology in Customer Due Diligence

Technology plays a crucial role in enhancing the efficiency, accuracy, and effectiveness of customer due diligence (CDD) in the banking industry. With the ever-increasing volume of customer data and the need for real-time monitoring, technology-driven solutions have become essential in streamlining the CDD process and mitigating risks.

One of the key contributions of technology in CDD is automation. Manual processes can be time-consuming, prone to errors, and inefficient when handling large amounts of customer data. By employing automation tools, banks can significantly reduce manual effort and improve the efficiency of data collection, analysis, and verification.

Artificial intelligence (AI) and machine learning are also valuable technologies in CDD. These systems can analyze vast amounts of customer data and identify patterns and anomalies that may indicate potential risks. AI-powered systems can detect suspicious transactions, monitor changes in customer behavior, and even perform sentiment analysis to identify signals of illegal activities.

Another aspect where technology is invaluable is in online identity verification. Digital solutions leverage various methods, such as biometric authentication, facial recognition, and document scanning, to verify the identity of customers remotely. These technologies allow banks to conduct customer due diligence securely and conveniently in the digital space.

Data analytics plays a significant role in CDD as well. By leveraging big data analytics, banks can gain valuable insights into customer behavior, transaction patterns, and risk profiles. This helps in identifying potential risks, enhancing risk assessment models, and improving decision-making processes.

Incorporating technology into the monitoring phase of CDD enables banks to monitor customer activities in real-time. Advanced software systems can detect suspicious activities, such as sudden increases in transaction volume or unusual transaction patterns, and trigger alerts for further investigation. Real-time monitoring improves risk mitigation efforts, allowing banks to respond promptly to potential threats.

Technology also facilitates the automation of compliance checks against regulatory requirements. Banks can integrate regulatory databases and guidelines into their automated systems, ensuring that customer due diligence practices align with evolving compliance requirements. This helps banks stay up to date with changing regulations and reduces the risk of non-compliance.

Moreover, technology enables the secure storage and management of customer data. Banks can employ robust data security measures, such as encryption and access controls, to safeguard sensitive customer information. By ensuring data privacy and security, banks build trust with their customers and maintain compliance with privacy regulations.

While technology enhances the efficiency and effectiveness of CDD, it is crucial to strike a balance with human judgment and expertise. Human intervention is still essential in interpreting the results generated by technology-driven systems and making informed decisions based on the data analysis.

In summary, technology empowers banks to streamline and enhance the customer due diligence process. Automation, artificial intelligence, machine learning, data analytics, and secure data management contribute to the accuracy of customer verification, real-time monitoring, compliance with regulations, and risk mitigation efforts. By leveraging technology, banks can drive efficiency, reduce costs, and strengthen their ability to detect and prevent financial crimes.

Key Regulations and Compliance Requirements in Customer Due Diligence

Customer due diligence (CDD) in the banking industry is governed by various regulations and compliance requirements. These regulations aim to prevent money laundering, terrorist financing, fraud, and other financial crimes. Compliance with these requirements is crucial for banks to maintain the integrity of their operations and fulfill their obligations in safeguarding the financial system.

One of the key regulations in CDD is the anti-money laundering (AML) framework. AML regulations are designed to detect and prevent the laundering of illicit funds through financial institutions. These regulations require banks to establish robust processes for customer identification, verification, and ongoing monitoring. AML laws are enforced by regulatory bodies such as the Financial Action Task Force (FATF) and are implemented at both national and international levels.

Know Your Customer (KYC) regulations are another essential aspect of CDD. KYC requirements mandate that banks have a clear understanding of their customers, their transactions, and the risks associated with those relationships. Banks must collect and verify customer information, identify beneficial ownership, and assess the purpose and expected nature of the business relationship. KYC regulations help banks ensure that they are not facilitating criminal activities or unwittingly participating in money laundering or terrorist financing schemes.

The Financial Crimes Enforcement Network (FinCEN) in the United States requires banks to comply with the Bank Secrecy Act (BSA), which includes CDD obligations. The BSA requires banks to establish a risk-based approach to customer due diligence, monitor customer transactions, and report suspicious activities to the relevant authorities.

In the European Union, the Fourth Money Laundering Directive (4MLD) and the Fifth Money Laundering Directive (5MLD) establish the legal framework for AML and CDD. The directives require banks to implement risk-based approaches to customer due diligence and enhance the detection and reporting of suspicious transactions. 5MLD adds more stringent requirements, including measures to mitigate risks associated with transactions involving high-risk countries and the identification of politically exposed persons (PEPs).

Other regulatory bodies and organizations, such as the Office of Foreign Assets Control (OFAC) in the United States and the Financial Conduct Authority (FCA) in the United Kingdom, also issue guidance and regulations related to CDD. These bodies provide additional guidance on screening and verifying customers against national and international sanction lists and implementing appropriate risk-based due diligence procedures.

Compliance with these regulations and requirements is not just a legal obligation for banks; it is a vital aspect of maintaining a trustworthy banking system. Failure to comply with CDD regulations can result in severe consequences, including significant financial penalties, reputational damage, and potential criminal liability for the financial institution and its officers.

Continuous monitoring of changing regulatory landscapes and ensuring that CDD processes align with evolving requirements is essential for banks. Staying up to date with emerging regulations and industry best practices allows banks to implement effective compliance programs, mitigate risks, and contribute to the global efforts against financial crimes.

Best Practices for Implementing Customer Due Diligence in Banking

Implementing robust customer due diligence (CDD) practices is crucial for banks to mitigate risks, ensure compliance with regulations, and protect the integrity of their operations. By adhering to best practices, banks can establish effective CDD processes that are efficient, accurate, and aligned with industry standards. Here are some key best practices for implementing CDD in banking:

1. Establish a Risk-Based Approach: Implement a risk-based approach to CDD, where the level of due diligence is commensurate with the assessed risk of the customer. This allows banks to allocate resources effectively and focus more attention on higher-risk customers.

2. Develop Comprehensive Policies and Procedures: Establish clear policies and procedures that outline the steps and requirements for conducting CDD. Document these processes to ensure consistency and provide guidance to employees.

3. Enhance Employee Training: Provide regular training and education to employees on customer due diligence practices, regulatory requirements, and emerging trends in financial crimes. This ensures that employees understand their roles and responsibilities in implementing effective CDD processes.

4. Implement Robust Customer Data Management: Establish secure and efficient customer data management systems. Ensure that customer information is accurate, up to date, and stored securely, while complying with data privacy and security regulations.

5. Leverage Technology: Embrace technology solutions that automate CDD processes, enhance data analysis, and provide real-time monitoring capabilities. Artificial intelligence, machine learning, and data analytics tools can improve the efficiency and accuracy of CDD practices.

6. Regularly Update Customer Information: Implement procedures to regularly review and update customer information. Conduct periodic customer reviews to identify any changes in customer risk profiles, including changes in ownership, structure, or business activities.

7. Establish Robust Audit and Review Processes: Conduct regular internal audits and reviews of CDD processes to identify any weaknesses or gaps in compliance. This helps ensure that CDD practices remain effective and aligned with regulatory requirements.

8. Foster Collaboration: Foster collaboration between different departments within the bank, such as compliance, risk management, and technology teams. This collaboration ensures cohesive implementation of CDD practices and enables a holistic view of customer risk.

9. Stay Informed about Regulatory Changes: Keep abreast of evolving regulations, guidelines, and industry best practices related to CDD. Regularly review and update CDD processes to align with changing regulatory landscapes.

10. Foster a Culture of Compliance: Promote a culture of compliance throughout the organization. Create a tone from the top that emphasizes the importance of CDD and highlights the ethical and legal obligations of the bank in preventing financial crimes.

By adopting these best practices, banks can establish effective customer due diligence processes that not only comply with regulations but also help mitigate risks, protect customers, and maintain the trust and integrity of the financial industry.

Conclusion

Customer due diligence (CDD) is of utmost importance in the banking industry. It serves as a vital safeguard against financial crimes, such as money laundering, fraud, and terrorist financing. By implementing robust CDD processes, banks can verify the identity of their customers, assess the risks associated with them, and ensure compliance with regulatory requirements.

The three stages of CDD – customer identification, customer verification, and monitoring and ongoing due diligence – provide a comprehensive framework for banks to establish trust, mitigate risks, and contribute to the overall integrity of the financial system.

Technology plays a significant role in enhancing the effectiveness and efficiency of CDD processes. Automation, artificial intelligence, machine learning, data analytics, and secure data management systems enable banks to streamline their CDD practices, monitor customer activities in real-time, and detect potential risks.

Compliance with key regulations, such as anti-money laundering (AML) and know your customer (KYC) requirements, is fundamental in CDD. The continual monitoring of regulatory changes allows banks to adapt to evolving compliance standards and implement effective CDD practices.

Implementing best practices in CDD helps banks establish comprehensive risk assessment procedures, enhance employee training, optimize customer data management, foster collaboration, and maintain a strong culture of compliance.

Ultimately, customer due diligence is essential for banks to protect themselves, their customers, and the integrity of the financial system. It ensures the legitimacy of banking relationships, prevents financial crimes, and contributes to a secure and trustworthy banking environment.

By adhering to the best practices outlined in this article, banks can establish robust customer due diligence processes that not only comply with regulations but also mitigate risks, enhance customer trust, and promote a stronger and more sustainable banking industry.