Introduction

Forex trading, also known as foreign exchange trading, is the buying and selling of currencies on the foreign exchange market. It is one of the largest and most liquid financial markets in the world, with daily trading volumes exceeding trillions of dollars. If you’re looking to make money through forex trading, you’ve come to the right place.

Forex trading offers numerous opportunities for individuals to profit from currency fluctuations. Whether you’re an experienced trader or a novice just starting out, this article will guide you through the steps to succeed in the forex market.

Before diving in, it’s important to note that forex trading comes with risks, and it’s crucial to approach it with a strategic mindset. This article will provide you with a comprehensive overview of the essential factors to consider when venturing into forex trading, including understanding the market, formulating a trading strategy, selecting a reliable broker, and managing risk.

Additionally, we will discuss the importance of analyzing market trends and indicators, as well as the process of setting up a trading account, placing trades, and monitoring your positions. With the right knowledge and approach, you can maximize your profits and minimize your risks in forex trading.

Moreover, we will explore the key aspects of exiting trades and cashing out your profits, as well as the importance of continuous education and adapting your strategies to stay ahead in the ever-evolving forex market. By following these guidelines, you’ll be well-equipped to embark on your forex trading journey and work towards financial success.

Understanding Forex Trading

Before diving into forex trading, it is essential to have a solid understanding of how the market works and what factors influence currency fluctuations. Forex trading involves the simultaneous buying of one currency and selling of another, with the goal of profiting from changes in exchange rates.

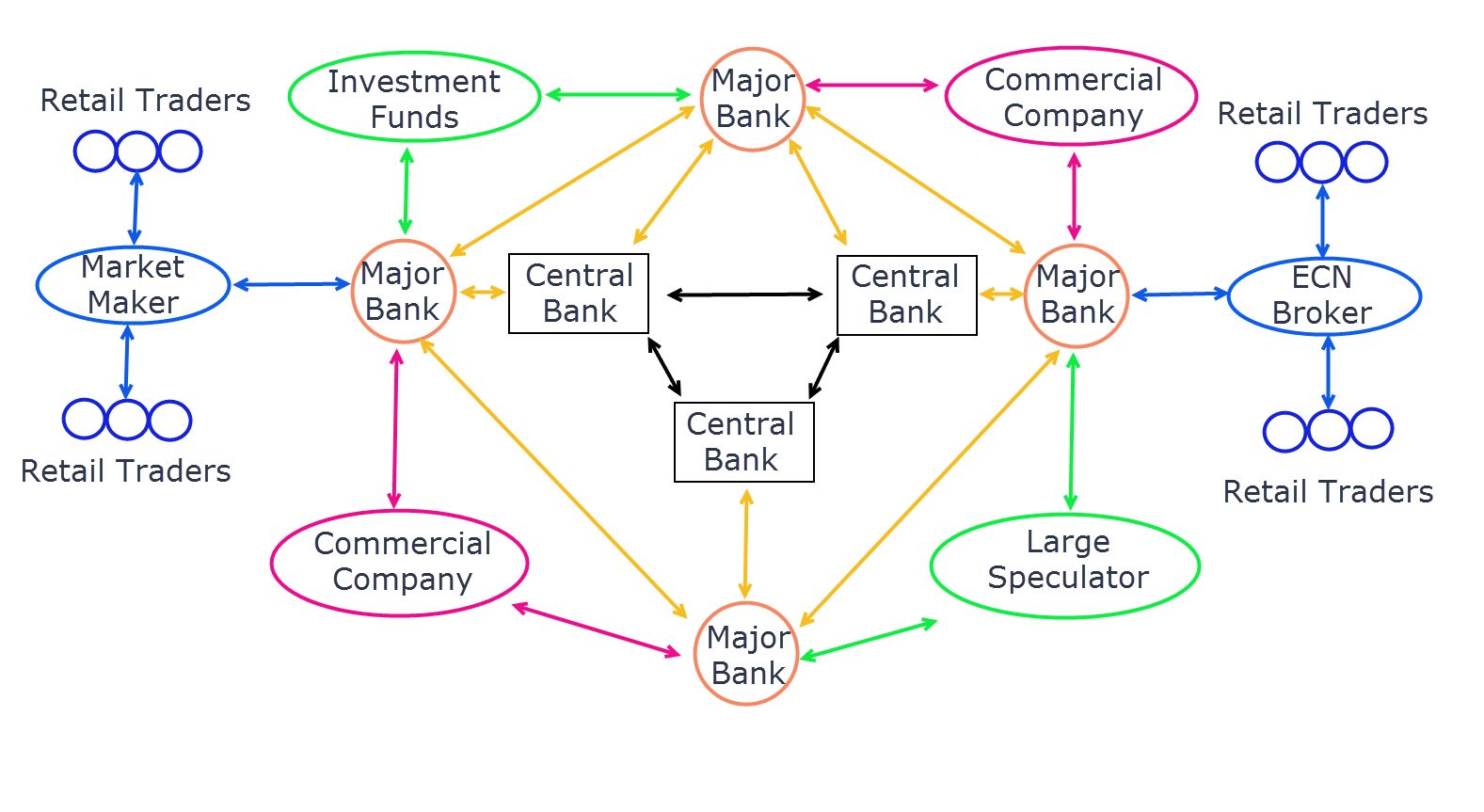

The forex market operates 24 hours a day, five days a week, allowing traders to participate in global currency trading and take advantage of different time zones. The primary participants in the forex market include banks, financial institutions, corporations, governments, and individual traders.

One of the key principles in forex trading is the concept of currency pairs. Each forex trade involves the simultaneous buying of one currency and selling of another. Currency pairs are denoted by three-letter codes, such as EUR/USD, representing the euro against the U.S. dollar. Understanding how currency pairs work is crucial, as changes in exchange rates between the two currencies determine the profitability of trades.

Forex trading is heavily influenced by various economic and geopolitical factors, which can cause currencies to fluctuate. Factors such as interest rates, economic data, political stability, and market sentiment all play a role in determining the value of currencies. Traders need to stay informed about these factors and analyze their impact on currency movements to make informed trading decisions.

In addition to fundamental analysis, technical analysis is a widely used method in forex trading. It involves the use of charts, patterns, and indicators to identify trends and potential trading opportunities. Technical analysis helps traders understand market dynamics and make predictions about future price movements.

Furthermore, leverage is an important aspect of forex trading. Leverage allows traders to control larger positions with a smaller amount of capital. While leverage can amplify profits, it also increases the risk of potential losses. It is essential for traders to use leverage responsibly and understand the associated risks.

Overall, understanding the fundamentals of forex trading, including currency pairs, market influences, and analysis techniques, is crucial for success in the forex market. Armed with this knowledge, traders can make informed decisions and navigate the complexities of the forex market.

Creating a Forex Trading Strategy

A well-defined trading strategy is essential for success in forex trading. It provides a systematic approach to decision-making and helps traders stay focused and disciplined in the face of market fluctuations. Creating a solid trading strategy involves a combination of analysis, risk management, and personal preferences.

The first step in creating a trading strategy is to determine your trading goals and objectives. Are you aiming for short-term gains or long-term profitability? Are you more comfortable with day trading or swing trading? Defining your goals will help shape your strategy and guide your trading decisions.

Once you have identified your goals, the next step is to perform thorough market analysis. This includes analyzing economic indicators, monitoring news events, and studying technical charts. By understanding the market trends and identifying potential entry and exit points, you can make more informed trading decisions.

Another important aspect of a trading strategy is risk management. It is vital to set clear risk parameters and determine your risk tolerance level. This involves deciding on the maximum percentage of your trading capital you are willing to risk on each trade and implementing stop-loss orders to limit potential losses.

Diversification is also crucial in designing a trading strategy. Instead of relying on a single currency pair, consider diversifying your portfolio by trading multiple currency pairs. This helps spread the risk and increases the potential for profitability.

Furthermore, it is important to establish clear entry and exit criteria. Determine the conditions that signal a favorable entry point, such as a specific price level or a certain technical indicator pattern. Likewise, identify the criteria that indicate it is time to exit a trade, whether it’s reaching a profit target or a predetermined stop-loss level.

Lastly, document your trading strategy in a trading plan. This plan serves as a blueprint for your trades and helps you stay disciplined and focused. It should outline your trading goals, risk management rules, entry and exit criteria, and any other relevant guidelines that govern your trading activities.

Remember, a trading strategy is not set in stone. It should be continuously evaluated and refined based on market conditions and personal experiences. Regularly review and analyze the performance of your strategy and make adjustments when necessary.

By creating a well-defined trading strategy and adhering to its principles, you can increase your chances of success in forex trading. A solid strategy helps you avoid impulsive decisions driven by emotions and provides a framework for consistent and profitable trading.

Choosing the Right Forex Broker

Choosing the right forex broker is a critical decision that can greatly impact your trading success. With numerous brokers available in the market, it’s important to consider several factors to ensure you find a reliable and reputable broker that meets your trading needs.

First and foremost, check for regulation and licensing. A reputable forex broker should be regulated by a recognized financial authority. Regulation provides a level of protection for traders and ensures that the broker operates with transparency and follows industry standards.

Next, consider the broker’s trading platform. A user-friendly and intuitive platform is essential for executing trades efficiently. Look for a platform that offers a range of technical analysis tools, real-time charts, and the ability to customize settings to suit your trading preferences.

Additionally, examine the range of currency pairs offered by the broker. Ensure that they offer the pairs you are interested in trading. Furthermore, consider the broker’s transaction costs, including spreads, commissions, and overnight swap rates. Low transaction costs can significantly impact your profitability in the long run.

Another crucial factor to consider is the broker’s customer service. A reliable broker should provide excellent customer support, with responsive and knowledgeable representatives readily available to assist you with any issues or inquiries. Test their customer service by reaching out to them with any questions you may have.

Furthermore, consider the broker’s educational resources. A good broker will offer educational materials, such as tutorials, webinars, and market analysis, to help you enhance your trading skills and knowledge. Access to quality educational resources can be invaluable, especially for novice traders.

It is also essential to evaluate the broker’s trading account options. Look for a broker that offers account types suitable for your trading style and preferences. Consider factors such as minimum deposit requirements, leverage options, and the availability of demo accounts for practice.

Lastly, read reviews and seek recommendations from other traders. Feedback from experienced traders can provide valuable insights into the broker’s reputation and reliability. Consider factors such as withdrawal processes, trade execution speed, and overall trading experience.

Choosing the right forex broker requires careful consideration of various factors. Take your time to thoroughly research and compare different brokers before making a decision. Remember, a reliable broker is essential for a smooth and successful trading experience.

Setting Up a Forex Trading Account

Setting up a forex trading account is the first step towards entering the exciting world of currency trading. Here are the key steps to follow in order to set up your forex trading account:

1. Research and choose a broker: Select a reputable forex broker that suits your trading needs. Consider factors such as regulation, trading platforms, currency pairs offered, transaction costs, customer service, and educational resources.

2. Complete the registration process: Visit the broker’s website and click on the ‘Open an Account’ or ‘Register’ button. Fill out the necessary personal and financial information as required by the broker. These details may include your name, address, country of residence, date of birth, email, and phone number.

3. Verify your identity: Most brokers require verification of identity and address documents. This is to ensure compliance with Know Your Customer (KYC) regulations and to prevent fraudulent activities. You may need to provide a copy of your passport or driver’s license, as well as a utility bill or bank statement as proof of address.

4. Choose your trading account type: Select the type of trading account that aligns with your trading goals and preferences. The account options typically include standard accounts, mini accounts, and demo accounts for practice.

5. Fund your account: Deposit funds into your trading account. Most brokers offer a variety of payment options, including bank transfers, credit cards, and online payment methods. Ensure that you are aware of any deposit fees or minimum deposit requirements.

6. Set up your trading platform: Download and install the trading platform provided by your broker. Familiarize yourself with the platform’s features, navigation, and tools. If the broker offers a web-based platform, simply log in to your account through their website.

7. Practice with a demo account: Many brokers offer demo accounts where you can practice trading with virtual money. This is an invaluable opportunity to get hands-on experience with the trading platform and test your strategies without risking real funds.

8. Start trading: Once your account is funded and you have familiarized yourself with the trading platform, you are ready to start trading. Analyze the market, identify potential trading opportunities, and execute your trades based on your trading strategy. Remember to always practice risk management techniques and never risk more than you can afford to lose.

Setting up a forex trading account is an important process that ensures you have access to the forex market and can begin your trading journey. Follow these steps diligently and make sure to choose a reputable and reliable broker for a smooth and successful trading experience.

Analyzing Forex Market Trends and Indicators

Analyzing forex market trends and indicators is a crucial aspect of successful trading. It helps traders identify potential opportunities and make informed decisions. Here are some key factors to consider when analyzing forex market trends:

1. Fundamental analysis: This involves analyzing economic indicators, such as interest rates, GDP growth, employment data, and geopolitical events. Economic factors can influence currency values and understanding their impact on the forex market is vital.

2. Technical analysis: This approach involves studying price charts, patterns, and indicators to identify trends and potential trading opportunities. Traders use tools such as moving averages, support and resistance levels, and oscillators to make predictions about future price movements.

3. Candlestick patterns: Candlestick patterns provide visual representations of price movements. Patterns such as doji, hammer, engulfing, and shooting star can signal potential trend reversals or continuations. Learning to recognize and interpret these patterns can be a valuable skill for traders.

4. Support and resistance levels: Support levels are price levels at which demand exceeds supply, potentially causing prices to bounce back up. Resistance levels, on the other hand, are price levels at which supply exceeds demand, potentially causing prices to decline. Identifying these levels can help traders determine potential entry and exit points.

5. Moving averages: Moving averages smooth out price fluctuations and help identify trends. The most commonly used moving averages are the simple moving average (SMA) and the exponential moving average (EMA). Traders often use the crossover of different moving averages as a signal to enter or exit trades.

6. Oscillators: Oscillators, such as the Relative Strength Index (RSI) and the Stochastic Oscillator, help measure the speed and change of price movements. These tools can indicate overbought or oversold conditions in the market, suggesting potential reversal points.

7. Sentiment analysis: Monitoring market sentiment can provide insights into the overall mood of traders towards a particular currency pair. Sentiment can be measured through various indicators and tools, such as the Commitment of Traders (COT) report or sentiment surveys.

It’s important to remember that no single method guarantees accurate predictions in forex trading. A combination of fundamental and technical analysis, along with understanding market sentiment, provides a holistic view that can guide your trading decisions.

By staying informed, regularly analyzing market trends and indicators, and adapting your strategies accordingly, you can increase your chances of success in the forex market.

Practicing Risk Management Techniques

Risk management is a crucial aspect of forex trading that helps protect your capital and minimize potential losses. Implementing effective risk management techniques is essential for long-term success. Here are some key techniques to consider:

1. Determine risk-reward ratio: Before entering a trade, calculate the potential risk and reward. Assess whether the potential profit justifies the risk you are taking. Aim for a risk-reward ratio of at least 1:2, meaning the potential reward should be double the potential risk.

2. Set stop-loss orders: A stop-loss order is a predetermined level at which a trade will be automatically closed to limit losses. Place stop-loss orders based on your risk tolerance and ensure they are positioned at logical levels, such as below support or above resistance.

3. Use take-profit orders: Similar to stop-loss orders, take-profit orders help secure profits by automatically closing a trade when the price reaches a target level. Set take-profit orders based on your profit target and align them with technical analysis levels or key support and resistance zones.

4. Avoid overleveraging: While leverage can amplify profits, it also increases the risk of significant losses. Utilize leverage responsibly by only risking a small percentage of your trading capital on each trade. Avoid excessive leverage that can lead to margin calls and wipe out your account.

5. Diversify your portfolio: Spread your risk by trading different currency pairs and not concentrating all your trading capital on a single trade. Diversification can help mitigate the impact of potential losses from one trade on your overall trading account.

6. Regularly review and adjust your risk management plan: As market conditions change, regularly review and adapt your risk management plan. Evaluate the effectiveness of your strategies and adjust your risk parameters if necessary. Stay disciplined and avoid letting emotions drive your trading decisions.

7. Use position-sizing techniques: Determine the appropriate position size for each trade based on your account size, risk tolerance, and the distance to your stop-loss level. Proper position sizing ensures that a single trade does not overly impact your overall trading account.

Remember that risk management is an ongoing process and should be an integral part of your trading routine. By implementing effective risk management techniques and sticking to your plan, you can protect your trading capital and increase your chances of long-term success in forex trading.

Placing Forex Trades

Placing forex trades involves executing buy or sell orders in the currency market. Here are some key steps to consider when placing forex trades:

1. Analyze the market: Use your chosen analysis techniques, such as fundamental or technical analysis, to identify potential trading opportunities. Look for patterns, trends, or signals that align with your trading strategy.

2. Determine entry and exit points: Once you have identified a trading opportunity, determine the price at which you want to enter the trade. This could be based on specific support or resistance levels, chart patterns, or technical indicators. Similarly, identify your target profit level and set a stop-loss order to limit potential losses.

3. Calculate position size: Determine the appropriate position size based on your risk tolerance and the distance to your stop-loss level. Consider using position sizing techniques to determine the appropriate lot size or quantity of currency to trade.

4. Place the trade: Log in to your trading platform and enter the relevant parameters for your trade, such as the currency pair, position size, entry price, stop-loss level, and take-profit level. Double-check the details before confirming the trade.

5. Monitor your trade: Once your trade is live, monitor its progress. Keep an eye on price movements, news events, and any factors that may impact your trade. Avoid making impulsive decisions based on short-term fluctuations and stick to your trading plan.

6. Adjust your trade if necessary: As the market evolves, you may need to make adjustments to your trade. If the price approaches your take-profit level, consider adjusting the level to secure profits. Similarly, if the trade is moving against you, evaluate if any changes need to be made to your stop-loss level.

7. Keep track of your trades: Maintain a trading journal to record the details of your trades, including entry and exit points, reasons for taking the trade, and the outcome. This record can help you analyze your trading performance and identify areas for improvement.

8. Stay disciplined: Stick to your trading plan and avoid emotional decision-making. Avoid the temptation to constantly monitor your trades, as this can lead to overtrading or making impulsive decisions.

Remember that forex trading involves inherent risks, and not all trades will be profitable. It’s important to manage your risk, practice patience, and maintain a long-term perspective. With time and experience, you can refine your trading skills and increase your chances of success in the forex market.

Monitoring and Reviewing Trades

Monitoring and reviewing your trades is a vital aspect of forex trading. By regularly assessing your trades, you can make informed decisions, identify strengths and weaknesses in your trading strategy, and improve your overall trading performance. Here are some key considerations when monitoring and reviewing your trades:

1. Track trade performance: Keep a record of each trade, including entry and exit points, profit or loss, and the reasoning behind the trade. This will allow you to evaluate the success of your trades over time and identify any patterns or trends in your trading performance.

2. Review trade outcomes: Assess the outcome of each trade objectively. Analyze whether the trade followed your trading plan and if the outcome was in line with your expectations. Identify any factors that may have influenced the trade, such as news events or market conditions.

3. Analyze trade execution: Evaluate how well you executed your trades. Consider factors such as entry and exit timing, slippage, and any mistakes or missed opportunities. Reviewing the execution of your trades will help you identify areas for improvement in your trading process.

4. Identify patterns and trends: Look for patterns or trends in your trading performance. Pay attention to the types of trades that have been consistently profitable and those that have resulted in losses. This analysis can help you identify your strengths and weaknesses as a trader.

5. Assess risk management: Review your risk management techniques for each trade. Evaluate whether you adhered to your predetermined risk and reward ratios and if you effectively managed your positions with stop-loss and take-profit orders. Adjust your risk management approach if needed to ensure proper capital preservation.

6. Learn from mistakes: Mistakes are a natural part of trading, but it’s important to learn from them. Identify any recurring mistakes in your trading decisions and take steps to avoid them in the future. Learn from your losses and use them as valuable learning experiences.

7. Adapt your trading strategy: Based on your trade reviews, make necessary adjustments to your trading strategy. Incorporate lessons learned and refine your approach to align with your strengths and goals. Continuously evolve your strategy to adapt to changing market conditions.

8. Seek outside perspective: Consider seeking feedback from peers or mentors in the trading community. They can provide objective insights and offer guidance based on their own experiences. Engaging in discussions and participating in trading forums can also help broaden your understanding.

Monitoring and reviewing your trades is an ongoing process that should be a regular part of your trading routine. By actively assessing your trades, making necessary adjustments, and continuously learning and improving, you can enhance your trading skills and increase your chances of success in the forex market.

Exiting and Cashing Out

Knowing when and how to exit a trade is just as important as entering it. Properly managing your exits and cashing out your profits is a vital aspect of successful forex trading. Here are some key considerations when it comes to exiting trades:

1. Stick to your trading plan: Exiting a trade should be guided by your predetermined trading plan. Your plan should outline the conditions under which you would exit a trade, such as reaching a certain profit target or hitting a predetermined stop-loss level. Avoid making emotional decisions that deviate from your plan.

2. Take partial profits: If a trade is moving in your favor, consider taking partial profits along the way. This allows you to lock in some gains while still giving the trade room to potentially reach your target profit level. Scaling out of positions can help manage risk and secure profits.

3. Adjust stop-loss levels: As a trade progresses, consider adjusting your stop-loss level to protect your profits. This technique is known as trailing stop-loss. By adjusting the stop-loss level to a point where it protects a portion of your profits, you can ensure that you exit the trade with a profit even if the market reverses.

4. Use trailing take-profit orders: Similar to trailing stop-loss orders, trailing take-profit orders allow you to automatically adjust your profit target as the market moves in your favor. This technique enables you to capture more profits if the market continues to trend in your desired direction.

5. Monitor market conditions: Stay vigilant and continuously assess the market conditions. If there are signs that contradict your initial trade analysis or if the market dynamics change, consider exiting the trade early to manage risk. Flexibility and adaptability are key in forex trading.

6. Take emotions into account: Emotions can influence trading decisions, leading to irrational behavior. Avoid being overly greedy or fearful. Stick to your trading plan and make rational decisions based on objective analysis of the market and your trade performance.

7. Review your trades after exiting: Once you have exited a trade, take the time to review its outcome and analyze your decision-making. Evaluate whether the exit timing was optimal and whether you followed your trading plan. This review process can provide valuable insights for future trades.

When it comes to cashing out your profits, consult the specific procedures and withdrawal options provided by your broker. Most brokers offer various withdrawal methods, such as bank transfers or e-wallets. Ensure that you understand any associated fees or minimum withdrawal amounts.

Remember, successful trading involves not just the entry but also the exit. By properly managing your exits, taking profits along the way, and sticking to your trading plan, you can optimize your trading results and effectively cash out your profits.

Continually Educating Yourself and Adapting Strategies

In the ever-evolving world of forex trading, it is crucial to continually educate yourself and adapt your strategies to stay ahead of the game. Forex markets are dynamic, influenced by various economic, political, and social factors, making it essential for traders to embrace ongoing learning and adapt their approaches. Here are some key aspects to consider:

1. Stay updated on market news: Keep abreast of the latest economic news, central bank announcements, geopolitical events, and market trends. Subscribing to reliable news sources and following reputable forex websites can provide you with valuable insights and help you make informed trading decisions.

2. Expand your knowledge: Forex trading is a vast field, and there is always more to learn. Explore different analysis techniques, study diverse trading strategies, and deepen your understanding of technical indicators. Continuous learning will broaden your perspective and help you develop new trading approaches.

3. Attend webinars and seminars: Many forex brokers and industry professionals offer webinars and seminars on various trading topics. Take advantage of these educational resources to gain insights from expert traders, learn new strategies, and stay updated with the latest trends and market developments.

4. Analyze your trading performance: Regularly evaluate your trading performance to identify patterns and areas for improvement. Look for recurring mistakes, learn from your losses, and identify successful strategies. Tracking your trades and reviewing your performance will help refine your trading techniques and adapt to changing market conditions.

5. Seek feedback and mentorship: Engage with other traders, join trading communities, and seek feedback on your trading strategies. The insights and experiences of more seasoned traders can provide valuable guidance and help you identify blind spots in your trading approach.

6. Embrace innovative technologies: The forex market is continuously evolving, with new technological advancements providing traders with powerful tools and resources. Stay informed about the latest trading software, algorithmic trading systems, and automated strategies. Embracing innovations can enhance your trading efficiency and effectiveness.

7. Adapt to market changes: Markets are dynamic, and what works in one market condition may not work in another. Be flexible and adapt your trading strategies to changing market environments. Constantly assess the effectiveness of your strategies and be ready to adjust your approach when necessary.

Remember, forex trading is a journey of continuous learning and improvement. As you educate yourself, develop new skills, and adapt your strategies, you can strengthen your trading approach and increase your chances of consistent profitability in the forex market.

Conclusion

Forex trading is a challenging yet potentially rewarding endeavor that offers individuals the opportunity to profit from currency fluctuations. By understanding the fundamentals of forex trading, creating a solid trading strategy, choosing a reliable forex broker, and practicing effective risk management, you can increase your chances of success in the forex market.

Analyzing forex market trends, monitoring and reviewing trades, and continually educating yourself are essential components of a successful trading journey. By staying informed about market news, expanding your knowledge, and adapting your strategies to changing market conditions, you can enhance your trading skills and increase your profitability.

It is important to approach forex trading with discipline, patience, and a long-term perspective. Avoid succumbing to emotions and impulsive decisions. Stick to your trading plan and risk management techniques, and never risk more than you can afford to lose.

Remember that forex trading involves risks, and not all trades will be profitable. It requires continuous learning, adaptability, and a commitment to self-improvement. Embrace the journey of forex trading, analyze your trades, learn from your experiences, and refine your strategies accordingly.

By following the guidelines outlined in this article, you are well-equipped to embark on your forex trading journey. Arm yourself with knowledge, practice discipline, and remain determined in your pursuit of financial success in the forex market.

Happy trading!