Introduction

Digital currency, such as Bitcoin and Ethereum, has become increasingly popular in recent years. With this rise in popularity comes the need for clearer guidelines on how to handle taxation of profits from digital currency sales. The Internal Revenue Service (IRS) has provided guidelines on how to treat these transactions, along with reporting and tax obligations.

Understanding how the IRS treats profits from digital currency sales is crucial for anyone involved in this industry. Failure to comply with tax regulations can result in penalties and other legal consequences. In this article, we will delve into the taxation of digital currency sales and discuss the reporting requirements, determination of profit or loss, applicable tax rates, and other important considerations.

It is important to note that digital currency is treated as property by the IRS, which means that the tax principles that apply to property transactions also apply to digital currency transactions. This includes the buying, selling, exchanging, or mining of digital currency.

As the market for digital currency grows and evolves, it is essential for individuals and businesses to stay informed about their tax obligations. By understanding the IRS guidelines and reporting requirements, individuals can ensure that they remain compliant and avoid unnecessary penalties.

In the following sections, we will explore the various aspects of taxation related to digital currency sales and provide practical tips for accurately reporting and documenting these transactions.

What is Digital Currency?

Digital currency, also known as cryptocurrency, is a form of digital or virtual money that operates on a decentralized network called blockchain. Unlike traditional currencies issued by governments, digital currencies are not controlled by any central authority. Instead, they rely on cryptographic technology to secure transactions and control the creation of new units.

The most well-known and widely used digital currency is Bitcoin, which was created in 2009. Since then, numerous other digital currencies have emerged, such as Ethereum, Litecoin, and Ripple.

One of the key features of digital currency is its ability to facilitate peer-to-peer transactions without the need for intermediaries, such as banks. This decentralization factor, coupled with the secure and transparent nature of blockchain technology, has attracted a growing number of users.

Another aspect that sets digital currency apart from traditional fiat currencies is its limited supply. Most digital currencies have a predetermined maximum supply, ensuring that they cannot be devalued through excessive printing or inflationary measures.

Digital currency can be acquired through various means. Individuals can purchase digital currency using traditional fiat currencies, mine them through complex computational processes, or receive them as payment for goods and services.

While digital currency offers many advantages, such as fast and low-cost transactions, it also presents some challenges. Its volatility is a notable concern, as the value of digital currencies can experience significant fluctuations in short periods. Additionally, the decentralized nature of digital currency raises questions about regulatory oversight, consumer protection, and security.

Despite these challenges, digital currency continues to gain mainstream recognition and acceptance. Businesses, including e-commerce platforms and online retailers, are increasingly embracing digital currency as a valid form of payment. Governments and financial institutions are also exploring ways to regulate and incorporate digital currencies into their existing frameworks.

In summary, digital currency is a form of decentralized and digital money that operates on a blockchain network. It offers unique advantages and challenges compared to traditional currencies, and its growing popularity has prompted governments and businesses to adapt their approaches to accommodate this emerging financial landscape.

Taxation of Digital Currency Sales

When it comes to taxation, the IRS treats digital currency sales as property transactions. This means that any gains or losses from the sale or exchange of digital currency are subject to taxation. The tax implications will depend on whether the digital currency is held as an investment or used for regular transactions.

For individuals who hold digital currency as an investment, any gains realized from the sale or exchange of the digital currency are considered capital gains. The holding period determines whether the gains are classified as short-term or long-term capital gains, which have different tax rates. Short-term gains occur when the digital currency is held for a year or less, while long-term gains occur when the holding period exceeds one year.

In the case of digital currency used for regular transactions, such as buying goods or services, any gains or losses resulting from the exchange or sale are treated as ordinary income or loss. This means that the gains would be subject to the individual’s applicable income tax rate.

It is important to note that the basis of the digital currency, which is used to calculate the gain or loss, is determined by the fair market value of the digital currency at the time of acquisition. The fair market value can be established through reliable exchange rates or other credible sources.

Additionally, when digital currency is used in a transaction, it may trigger a taxable event. This means that even if no gain or loss is realized, the individual may still be required to report the transaction and its value for tax purposes.

It’s important for individuals who engage in digital currency transactions to maintain accurate records of their transactions. This includes keeping track of the date, amount, and fair market value of each transaction. Proper recordkeeping can help support accurate reporting and minimize the risk of errors or discrepancies.

In the next section, we will explore the specific tax reporting requirements for digital currency sales and discuss how individuals can accurately determine their profit or loss from these transactions.

Tax Reporting Requirements for Digital Currency Sales

As with any taxable transaction, it is crucial to adhere to the IRS’s reporting requirements when it comes to digital currency sales. Individuals must accurately report their gains or losses from these transactions on their federal tax returns.

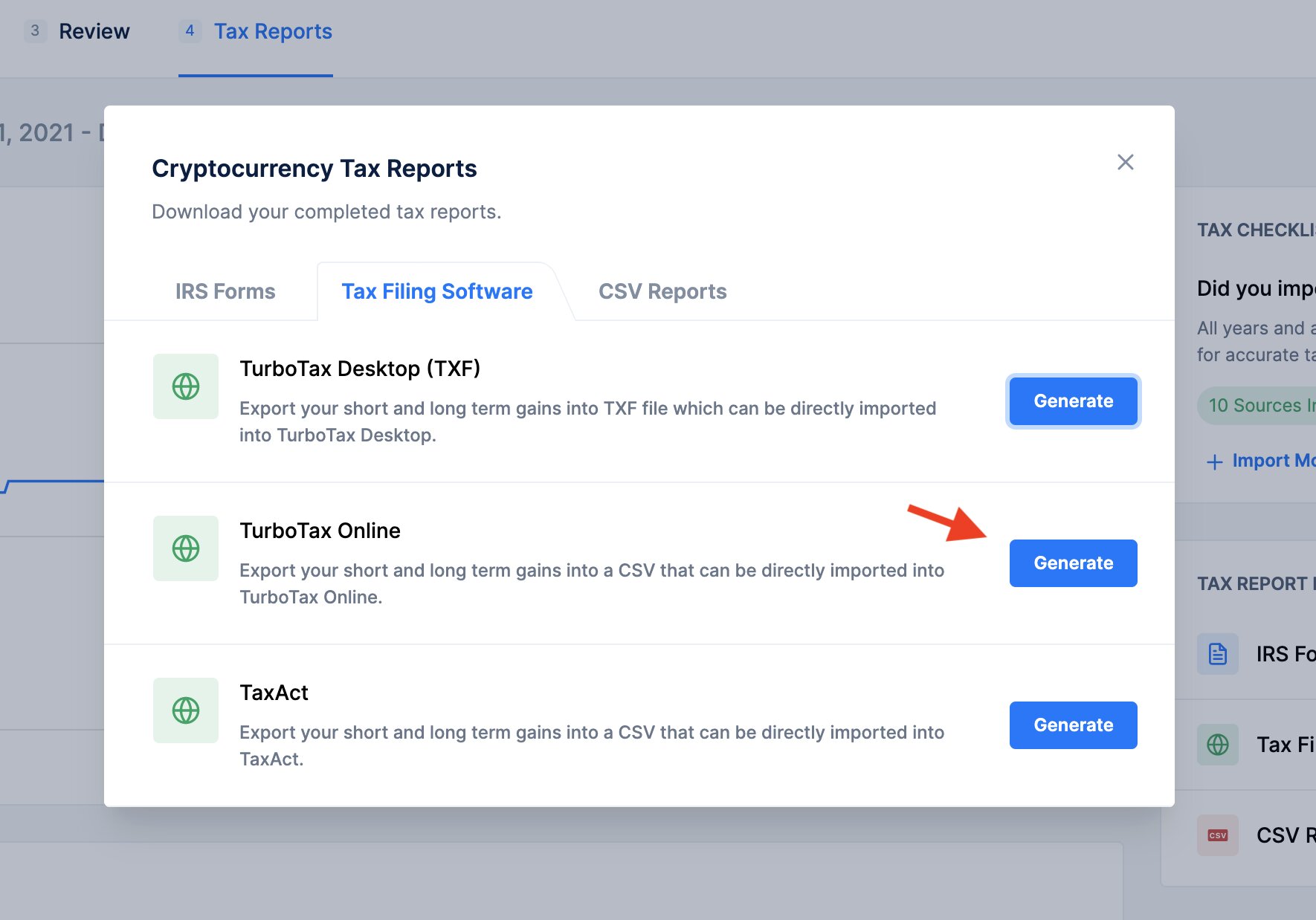

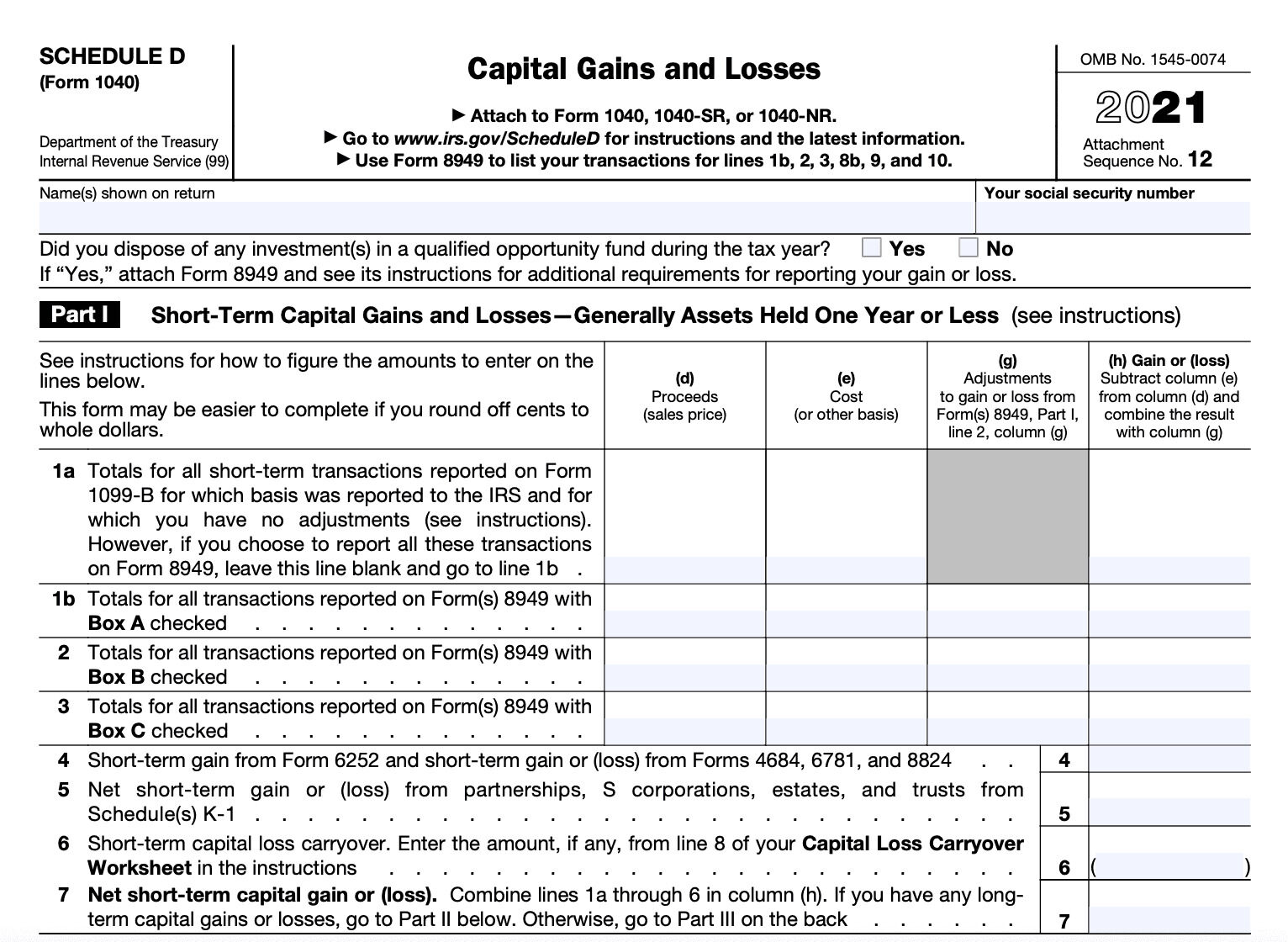

The primary form used for reporting digital currency sales is Form 8949, which is used to report capital gains and losses. Individuals must provide detailed information about each transaction, including the date of acquisition, date of sale or exchange, proceeds from the sale, cost basis, and any adjustments. This information is essential for calculating the gain or loss and ensuring accurate reporting.

To report the capital gains or losses from digital currency sales, the totals from Form 8949 must be transferred to Schedule D, where the net gain or loss is calculated. This net gain or loss will then be included on the individual’s Form 1040 when filing their federal tax return.

It is important to note that all digital currency transactions must be reported, including those conducted on foreign exchanges. The IRS has made efforts to ensure compliance by requiring domestic and foreign digital currency exchanges to provide transaction records to taxpayers.

Individuals who receive digital currency as payment for goods or services must also report the fair market value of the digital currency at the time of receipt as part of their gross income. This is important to ensure accurate reporting of ordinary income for tax purposes.

In addition to federal tax reporting requirements, it is essential to be aware of any state-specific tax obligations regarding digital currency sales. Some states may have their own guidelines or additional reporting requirements, so it is essential to research and understand the rules in your specific state.

Proper recordkeeping is crucial for fulfilling tax reporting requirements. It is recommended to keep detailed records of all digital currency transactions, including receipts, statements, and any other relevant documentation. These records will be instrumental in accurately reporting gains or losses and providing documentation in the event of an audit.

Next, we will explore how to determine the profit or loss from digital currency sales and discuss the factors that come into play.

Determining Profit or Loss from Digital Currency Sales

When it comes to determining the profit or loss from digital currency sales, there are several factors to consider. The basic formula for calculating gains or losses is the proceeds from the sale minus the cost basis of the digital currency.

The cost basis refers to the original value of the digital currency at the time of acquisition. This can include the purchase price, any fees associated with the transaction, and other acquisition costs. It’s important to keep accurate records of these costs to ensure an accurate calculation of the cost basis.

The proceeds from the sale or exchange of digital currency are the amount received in a transaction, which can include money, property, or other forms of consideration. This value is determined based on the fair market value of the digital currency at the time of the transaction.

If the proceeds from the sale are higher than the cost basis, then a gain is realized. On the other hand, if the proceeds are lower than the cost basis, a loss is incurred. These gains or losses are then classified as either short-term or long-term, based on the holding period of the digital currency.

It’s crucial to accurately track the cost basis and the proceeds from each digital currency sale and exchange. This can be a complex task, especially if there are multiple transactions involved. Utilizing digital currency tracking tools or professional accounting software can help streamline this process and minimize the risk of errors or omissions.

Furthermore, it’s important to note that any expenses incurred in the process of selling or exchanging digital currency may be deductible. For example, transaction fees, exchange fees, and other related expenses can be deducted from the proceeds when calculating gains or losses. Keeping detailed records of these expenses can help ensure that eligible deductions are claimed.

In summary, determining the profit or loss from digital currency sales involves calculating the proceeds from the sale and subtracting the cost basis. Accurate recordkeeping and consideration of applicable expenses are key to properly determining gains or losses. In the next section, we will discuss how to report capital gains or losses from digital currency sales on your tax return and explore the tax rates that apply.

Reporting Capital Gains or Losses from Digital Currency Sales

Reporting capital gains or losses from digital currency sales is an important step in fulfilling your tax obligations. The IRS requires individuals to report these gains or losses on their federal tax return using Form 8949 and Schedule D.

Form 8949 is used to report the details of each digital currency sale or exchange transaction, including the date of acquisition, date of sale or exchange, proceeds, cost basis, and any adjustments. It is important to accurately report this information to ensure proper calculation of the capital gains or losses.

After completing Form 8949, the totals from all transactions are transferred to Schedule D, where the net gain or loss is calculated. The net gain or loss from digital currency sales is then included on your Form 1040 when filing your federal tax return.

It’s important to note that if you have multiple digital currency transactions, you may need to fill out multiple Forms 8949 and attach them to your tax return. The transactions should be reported in chronological order, with separate sections for short-term and long-term transactions.

When determining whether a gain or loss is short-term or long-term, the holding period of the digital currency is considered. If the digital currency was held for one year or less before the sale or exchange, the gain or loss is classified as short-term. If the holding period exceeds one year, it is classified as long-term. Different tax rates apply to short-term and long-term capital gains.

It is important to remain consistent with the reporting of gains or losses. For example, if you consistently report gains or losses as short-term on previous tax returns, you should continue to do so in subsequent tax years, unless there is a change in the holding period.

It’s also worth mentioning that the tax rates for capital gains can vary depending on your income level and the type of gain (short-term or long-term). It is recommended to consult with a tax professional or refer to the IRS tax brackets and rates to determine the applicable tax rates for your situation.

Lastly, if you have any capital loss carryovers from previous years, you may be able to offset the gains from digital currency sales. This can help reduce your overall tax liability. However, specific rules and limitations apply, so it is important to understand the guidelines and consult with a tax professional if necessary.

Next, we will explore the reporting of digital currency sales on state taxes and discuss any additional considerations or requirements.

Tax Rates for Digital Currency Sales

The tax rates for digital currency sales depend on whether the gains or losses are classified as short-term or long-term. Short-term capital gains are taxed at higher rates compared to long-term capital gains.

Short-term capital gains arise from digital currency sales where the holding period is one year or less. These gains are taxed at ordinary income tax rates, which are based on the individual’s tax bracket. The tax rates for short-term capital gains can range from 10% to 37%, depending on income level.

On the other hand, long-term capital gains occur when the digital currency is held for more than one year before it is sold or exchanged. The tax rates for long-term capital gains are generally more favorable. For individuals in the lower tax brackets, the long-term capital gains tax rate can be as low as 0%, while for higher-income individuals, the maximum long-term capital gains tax rate is 20%.

It’s important to note that the tax rates for capital gains can be subject to change due to updates in tax laws and regulations. Staying informed about any changes can help ensure accurate reporting and calculating tax liabilities.

In addition to federal tax rates, it’s also important to consider any applicable state tax rates on digital currency sales. Each state may have its own tax regulations, including specific tax rates for capital gains. Some states may even have different tax rules for digital currency compared to traditional investments.

It’s crucial to research and understand the tax laws of your state to fulfill your tax obligations correctly. Working with a tax professional who is knowledgeable about digital currency taxation can provide valuable guidance in navigating the state tax requirements.

Properly evaluating and understanding the tax rates for digital currency sales is essential for accurate reporting and compliance. By understanding the applicable tax rates and any potential deductions or credits, individuals can effectively manage their tax liabilities related to digital currency transactions.

In the next section, we will explore the reporting of digital currency sales on state taxes and discuss any additional considerations or requirements.

Reporting Digital Currency Sales on State Taxes

In addition to federal taxes, individuals who engage in digital currency sales may also have state tax obligations to fulfill. The reporting requirements and treatment of digital currency sales on state taxes can vary from state to state.

Some states have specific guidelines or regulations regarding the tax treatment of digital currency transactions. These guidelines may include definitions of digital currency, rules for determining gains or losses, and reporting requirements.

When reporting digital currency sales on state taxes, it is important to determine how your state classifies digital currency for tax purposes. Some states may treat digital currency as property, similar to the federal tax treatment, while others may have different classifications or unique rules specifically for digital currency.

State tax reporting for digital currency sales typically follows a similar process as federal tax reporting. You may need to complete state-specific forms or schedules to report your capital gains or losses from digital currency transactions.

It’s important to keep in mind that not all states have adopted specific regulations or guidance for digital currency. In these cases, it may be necessary to consult with a tax professional or review state-specific tax publications to determine how to report your digital currency sales accurately.

Furthermore, if you reside in a state that does not have an income tax, such as Texas or Florida, you may not have state tax obligations related to digital currency sales. However, it is still essential to stay updated on any changes in state tax laws to ensure compliance.

Penalties for non-compliance with state tax requirements can vary by state and can include fines, interest, and other potential consequences. Therefore, it is crucial to take the necessary steps to fulfill your state tax obligations.

It is recommended to consult with a tax professional who is knowledgeable in state tax laws and regulations. They can provide guidance on how to correctly report your digital currency sales on your state tax returns and ensure compliance with state-specific requirements.

Next, we will discuss deducting expenses related to digital currency sales and the importance of recordkeeping and documentation.

Deducting Expenses Related to Digital Currency Sales

When it comes to digital currency sales, there are certain expenses that individuals may incur that can be deducted when determining their taxable gains or losses. Deductible expenses can help offset the overall tax liability and should be considered to ensure accurate reporting.

Some of the common expenses that may be deductible include transaction fees, exchange fees, and other costs associated with the purchase or sale of digital currency. These expenses can typically be subtracted from the proceeds when calculating gains or losses.

It’s important to keep detailed records of these expenses, including receipts and documentation, to support the deductions claimed. Accurate recordkeeping is crucial in the event of an audit or if the IRS requests additional information regarding the expenses claimed.

In addition to transaction-related expenses, individuals who mine digital currency may also be able to deduct certain mining-related expenses. For example, the cost of purchasing mining hardware, electricity costs, and other expenses directly related to the mining operation may be deductible.

However, it’s important to note that there are additional rules and limitations when deducting mining expenses. These rules may involve the classification of mining activities as a trade or business, the calculation of cost basis for mined digital currency, and other factors. Consulting with a tax professional who specializes in digital currency taxation can provide valuable guidance to ensure compliance with deduction rules.

It’s worth mentioning that deductions can only be claimed for expenses that are directly related to digital currency sales or mining activities. General expenses, such as personal computer costs or internet connection fees, are typically not deductible unless they are used exclusively for digital currency-related activities.

While deductions can help reduce the overall tax liability, it is important to follow IRS guidelines and requirements when claiming deductions. It is recommended to seek professional advice and review the specific rules and guidelines related to your situation.

Next, we will discuss the importance of recordkeeping and documentation for digital currency sales and other tax-related purposes.

Recordkeeping and Documentation for Digital Currency Sales

Proper recordkeeping and documentation are crucial when it comes to digital currency sales and related tax obligations. Keeping accurate and organized records ensures that you can accurately report your transactions, calculate gains or losses, and support any deductions or credits claimed.

Here are some key practices for effective recordkeeping:

1. Transaction Details: Record important details for each digital currency transaction, such as the date, time, and amount of the transaction, the fair market value of the digital currency at the time of the transaction, and any fees or costs associated with the transaction.

2. Acquisition and Disposal Information: Keep track of the acquisition date, cost basis, and fair market value at the time of acquisition for each digital currency you hold. This information is crucial for accurately calculating gains or losses when you sell or exchange the digital currency.

3. Receipts and Invoices: Retain all receipts, invoices, and statements related to your digital currency transactions. These documents provide evidence of your transactions and can be used to support your reporting if required.

4. Mining Activities: If you mine digital currency, keep records of your mining activities, including expenses incurred, mining equipment costs, electricity bills, and any other relevant information. These records can help support potential deductions related to mining operations.

5. Exchange and Wallet Statements: Maintain statements from digital currency exchanges and digital wallets that detail your account activity, including balances, transactions, and any relevant fees. These statements can help reconcile your records and provide an additional layer of documentation.

6. Communication and Correspondence: Keep copies of any communication or correspondence with digital currency exchanges, mining pools, or other parties involved in your digital currency activities. These documents may be helpful in demonstrating the nature of your transactions and supporting your tax reporting.

By adopting these recordkeeping practices, you can ensure that you have accurate and organized records for your digital currency sales and related tax obligations. These records will not only help you meet your tax reporting requirements but also provide a clear trail of your transactions in case of an audit or any inquiries from tax authorities.

It’s worth mentioning that technology can be a useful tool in maintaining proper records. Digital currency tracking software or apps can automate the recording of transaction details and help generate accurate reports for tax purposes. Utilizing such tools can streamline the recordkeeping process and reduce the chances of errors or omissions.

In the next section, we will highlight some common mistakes to avoid when reporting digital currency sales, to ensure compliance with tax regulations and minimize the risk of penalties.

Common Mistakes to Avoid in Reporting Digital Currency Sales

When it comes to reporting digital currency sales, there are several common mistakes that individuals should be aware of to ensure accurate reporting and compliance with tax regulations. Avoiding these mistakes can help minimize the risk of penalties and unnecessary audits. Here are some common mistakes to avoid:

1. Failure to Report All Transactions: One of the most crucial mistakes is failing to report all digital currency transactions. Every sale, exchange, or use of digital currency for goods or services should be reported, even if no gain or loss was realized. Keep track of all your transactions and ensure they are accurately reported on your tax return.

2. Inaccurate Cost Basis Calculation: Properly calculating the cost basis of digital currency is essential for accurately determining gains or losses. Failing to include acquisition costs, transaction fees, or other necessary expenses can result in an inaccurate cost basis calculation and potentially lead to improper reporting.

3. Omitting Foreign Digital Currency Transactions: If you engage in digital currency transactions on foreign exchanges, it is important to report those transactions as well. The IRS requires taxpayers to report all digital currency transactions, regardless of whether they occurred domestically or internationally.

4. Mixing Personal and Business Transactions: It is important to separate personal and business-related digital currency transactions. Mixing these transactions can lead to confusion and potentially result in improper reporting. Maintain separate records for personal and business transactions to ensure accurate reporting.

5. Neglecting State Tax Obligations: Each state may have its own tax regulations and requirements related to digital currency sales. Neglecting state tax obligations can lead to penalties or other consequences. Research and understand your state’s tax laws and fulfill your state tax obligations accordingly.

6. Failing to Keep Accurate Records: Proper recordkeeping is essential. Failing to keep accurate and organized records of your digital currency transactions, acquisition costs, and other relevant information can make it challenging to accurately report your sales and meet your tax obligations. Maintain detailed and organized records to avoid potential errors or omissions.

7. Ignoring Tax Professional Advice: Digital currency taxation can be complex, and laws and regulations can change. Ignoring the advice of a tax professional who specializes in digital currency taxation could lead to improper reporting. Consult with a qualified tax professional to ensure compliance with tax regulations and optimize your tax position.

By avoiding these common mistakes and taking the necessary steps to accurately report your digital currency sales, you can ensure compliance with tax regulations and minimize the risk of penalties or audits. It is always recommended to stay up-to-date on the latest tax guidelines and consult with a tax professional for personalized advice based on your specific situation.

In the concluding section, we will summarize the key points discussed in this article.

Conclusion

Understanding how the IRS treats profits from digital currency sales is essential for individuals and businesses involved in this emerging financial landscape. By adhering to tax regulations and accurately reporting digital currency sales, individuals can ensure compliance and minimize the risk of penalties or audits.

Throughout this article, we explored various aspects of taxation related to digital currency sales. We discussed the classification of digital currency as property, the tax reporting requirements, and the determination of profit or loss. We also delved into the tax rates for digital currency sales and the importance of reporting on state taxes.

We emphasized the significance of proper recordkeeping and documentation in accurately reporting digital currency transactions. Keeping detailed records helps in calculating gains or losses, supporting deductions, and providing evidence in case of any inquiries or audits from tax authorities.

Additionally, we highlighted common mistakes that individuals should avoid when reporting digital currency sales. These include failing to report all transactions, inaccurately calculating cost basis, neglecting state tax obligations, and mixing personal and business transactions, among others. By being aware of these mistakes, individuals can take steps to ensure accurate reporting and compliance.

In areas where individuals may require specific expertise, such as calculating cost basis or navigating state tax regulations, consulting with a tax professional who specializes in digital currency taxation can provide valuable guidance and mitigate potential issues.

As digital currency continues to evolve, it is crucial to stay informed about tax regulations and any updates or changes that may impact reporting requirements. Staying up-to-date and maintaining a proactive approach to tax compliance will contribute to a smooth and accurate tax reporting process.

In summary, understanding and fulfilling tax obligations related to digital currency sales is vital for individuals and businesses. By considering the IRS guidelines, accurately reporting transactions, properly determining gains or losses, and meeting state tax obligations, individuals can navigate the tax landscape surrounding digital currency sales and ensure compliance with tax regulations.