What Is The Tax on Cryptocurrency?

As the popularity of cryptocurrency continues to soar, so too does the need for a clear understanding of the tax implications surrounding this digital form of currency. Unlike traditional forms of currency, such as cash or bank transfers, cryptocurrencies like Bitcoin, Ethereum, and Litecoin operate on a decentralized platform called blockchain. This unique characteristic raises questions about how cryptocurrency transactions are taxed and what obligations investors have to report their earnings to tax authorities.

Although cryptocurrency operates outside the realm of traditional financial institutions, it is still subject to taxation in many jurisdictions. The tax treatment of cryptocurrency transactions varies from country to country, and even within different states or regions. Therefore, it is crucial for cryptocurrency investors to familiarize themselves with the tax laws and reporting requirements specific to their jurisdiction.

The taxation of cryptocurrency primarily revolves around the concept of capital gains. When an individual buys or sells cryptocurrency, it is considered a taxable event. This means that any profits made from selling cryptocurrency are subject to capital gains tax, while losses can potentially be used to offset other capital gains.

Reporting cryptocurrency transactions can be complex, especially for those dealing with multiple exchanges and wallets. It is vital to keep detailed records of every transaction, including the date, time, amount, and value of the cryptocurrency involved. These records will be crucial when calculating capital gains or losses for tax reporting purposes.

For those who invest in foreign-based cryptocurrency exchanges or hold investments in foreign cryptocurrencies, additional reporting requirements may apply. In some cases, taxpayers may be required to file informational forms, such as the Foreign Bank Account Report (FBAR) or the Foreign Account Tax Compliance Act (FATCA) form.

As with any investment, taxes on cryptocurrency can be complex and require careful planning and strategy. Cryptocurrency investors should consider consulting a tax professional with expertise in this area to ensure compliance with the tax laws and to maximize potential tax benefits.

In summary, the tax on cryptocurrency is a complex and evolving topic. Investors must navigate the specific tax laws and reporting requirements of their jurisdiction. It is essential to keep accurate records of transactions and consider seeking professional tax advice to ensure compliance and optimize tax planning.

Introduction

Cryptocurrency has emerged as a revolutionary form of digital currency that operates independently of traditional financial institutions. With the increasing adoption of cryptocurrencies like Bitcoin, Ethereum, and Litecoin, it is crucial to understand the tax implications associated with them. This article aims to provide a comprehensive overview of the tax on cryptocurrency, helping investors navigate the often complex and evolving landscape of crypto taxation.

Unlike traditional fiat currencies, cryptocurrencies are decentralized and operate on a technology called blockchain. This decentralized nature, along with the potential for anonymity, has led to questions about how cryptocurrency transactions should be taxed. Governments around the world have started grappling with this issue, developing tax frameworks to ensure that cryptocurrency holders are accountable for their earnings.

The tax treatment of cryptocurrency varies from country to country and is subject to ongoing regulatory developments. While some countries have implemented detailed guidelines, others are still in the process of formulating comprehensive regulations. It is important for cryptocurrency investors to understand the tax laws and reporting requirements specific to the jurisdiction in which they reside.

One of the key aspects of crypto taxation is the concept of capital gains. When a person buys or sells cryptocurrency, it is considered a taxable event. The difference in value between the purchase price and the sale price determines whether a capital gain or loss has occurred. These gains and losses are subject to taxation, with the applicable tax rates varying depending on factors such as the holding period and the taxpayer’s income bracket.

Additionally, reporting cryptocurrency transactions can present its own set of challenges. Investors must keep meticulous records of all transactions, including dates, amounts, and values of the cryptocurrency involved. Failure to accurately report transactions can result in audits, penalties, and potential legal consequences. Therefore, it is crucial to maintain accurate and up-to-date records to ensure compliance with tax authorities.

This article will delve into the specifics of capital gains tax on cryptocurrency, reporting requirements for cryptocurrency transactions, taxation of foreign cryptocurrency investments, tax withholding and estimated payments, and offer insights into tax strategies for cryptocurrency investors. By understanding the tax implications surrounding cryptocurrency, investors can make informed decisions and ensure compliance with their tax obligations.

Understanding Cryptocurrency

Cryptocurrency is a digital or virtual form of currency that uses cryptography for secure financial transactions, control the creation of new units, and verify the transfer of assets. It operates on a technology called blockchain, which is a decentralized and distributed ledger that records all transactions across a network of computers.

One of the key features of cryptocurrency is its decentralization, meaning it is not controlled or regulated by any central authority or government. This feature provides users with a sense of financial autonomy and allows for peer-to-peer transactions without the need for intermediaries such as banks or payment processors.

Bitcoin, the first and most well-known cryptocurrency, was created in 2009 by an anonymous person or group of individuals using the pseudonym Satoshi Nakamoto. Since then, thousands of different cryptocurrencies, commonly referred to as altcoins, have been developed, each with its own unique features and purposes.

Transactions in cryptocurrency are facilitated through cryptographic techniques, which ensure the security and integrity of the transaction data. Public and private keys are used to authenticate and authorize transactions, with the public key acting as the user’s address and the private key serving as the signature to verify ownership.

The value of cryptocurrency is determined by supply and demand dynamics, similar to traditional currencies. Factors such as market sentiment, adoption rates, technological advancements, and regulatory developments can all influence the price fluctuations of cryptocurrencies. Due to their volatile nature, cryptocurrencies have gained a reputation for high-risk investments.

While some cryptocurrencies are primarily used as a medium of exchange, others serve specific purposes within decentralized networks. For example, Ethereum, the second-largest cryptocurrency by market capitalization, enables the creation and execution of smart contracts, which are self-executing agreements with the terms of the contract directly written into code.

Another notable aspect of cryptocurrency is its potential for providing financial inclusion to individuals without access to traditional banking services. Cryptocurrencies enable users to send and receive funds across borders quickly and at a relatively low cost, empowering the unbanked population to participate in the global economy.

It is important to note that the regulatory landscape surrounding cryptocurrencies varies across jurisdictions. Some countries have embraced cryptocurrencies, providing clear legal frameworks and regulatory oversight, while others have taken a more cautious approach or have outright banned the use of cryptocurrencies. Investors and users should familiarize themselves with the legal and regulatory environment of their respective jurisdictions to ensure compliance.

In summary, cryptocurrency is a digital form of currency that operates on blockchain technology. It offers decentralization, security, and potential financial inclusion. However, the extensive use and adoption of cryptocurrencies have raised questions about their tax implications, which will be explored further in the subsequent sections.

The Tax Implications

The rapid growth and widespread adoption of cryptocurrency have prompted tax authorities around the world to address the tax implications associated with these digital currencies. While the tax treatment of cryptocurrencies varies from country to country, it is essential for investors to understand the general tax principles that apply to their cryptocurrency holdings.

In most jurisdictions, cryptocurrency is treated as property or an asset, rather than traditional currency. This means that the tax implications are similar to those of stocks, bonds, or real estate. When you buy, sell, or exchange cryptocurrencies, it may trigger taxable events, resulting in potential tax liabilities.

One of the primary tax implications of cryptocurrency is capital gains tax. When you sell or exchange cryptocurrency for a profit, it is considered a capital gain, and you are generally required to report and pay taxes on the gain. Conversely, if you sell cryptocurrency for less than what you initially paid, it may result in a capital loss, which may be used to offset other capital gains or carried forward to future tax years.

It is essential to note that the holding period of the cryptocurrency may affect the tax rate. In many jurisdictions, if you hold the cryptocurrency for less than a year before selling it, it is considered a short-term capital gain and subject to ordinary income tax rates. If you hold the cryptocurrency for more than a year, it is considered a long-term capital gain and may qualify for lower tax rates.

Additionally, mining cryptocurrency, which involves using computer power to solve complex mathematical problems to validate transactions on the blockchain, can also have tax implications. In most cases, the rewards obtained from mining activities are considered income and need to be reported as such, subject to the appropriate tax rates.

Furthermore, if you receive cryptocurrency as payment for goods or services, it is considered taxable income. The fair market value of the cryptocurrency at the time of receipt should be reported as income on your tax return. This applies whether you receive cryptocurrency as payment for freelance work, salary, or as a business owner accepting cryptocurrency as a form of payment.

Another crucial aspect to consider regarding tax implications is the reporting of cryptocurrency transactions. Many tax authorities require individuals to maintain detailed records of their cryptocurrency transactions, including the date, type of transaction, value in cryptocurrency, and corresponding value in fiat currency. Failure to adequately report these transactions can result in penalties, fines, or audits.

While tax laws and regulations surrounding cryptocurrency are still evolving, it is important to consult with a tax professional or accountant knowledgeable in cryptocurrency taxation to ensure compliance with the specific tax requirements of your jurisdiction.

To summarize, the tax implications of cryptocurrency include capital gains tax, reporting requirements for transactions, taxing mining activities, and the taxation of cryptocurrency received as income. Understanding and complying with the tax laws and regulations regarding cryptocurrency are essential for investors to effectively manage their tax responsibilities.

Taxable Events in Cryptocurrency

When it comes to cryptocurrency, various transactions can trigger tax liabilities. It is crucial for investors to be aware of these taxable events to ensure compliance with tax laws and reporting requirements. Here are some of the key taxable events in cryptocurrency:

1. Buying or Selling Cryptocurrency: Whenever you buy or sell cryptocurrency, it is considered a taxable event. Whether you exchange cryptocurrency for fiat currency (e.g., USD, EUR) or another cryptocurrency, any gains realized from the transaction may be subject to capital gains tax. The specific tax treatment will depend on the holding period and the tax laws of your jurisdiction.

2. Exchanging Cryptocurrency: Exchanging one type of cryptocurrency for another can also trigger a taxable event. If you trade Bitcoin for Ethereum, for example, the exchange is treated as a sale of Bitcoin and a purchase of Ethereum. The difference in value between the two cryptocurrencies at the time of the exchange may result in a capital gain or loss.

3. Using Cryptocurrency for Goods and Services: Using cryptocurrency to purchase goods or services is considered a taxable event. The value of the cryptocurrency at the time of the transaction needs to be reported as income, and any gain or loss may be subject to capital gains tax.

4. Receiving Cryptocurrency as Income: If you receive cryptocurrency as payment for work performed or as a form of income, it is considered taxable income. The fair market value of the cryptocurrency at the time of receipt needs to be reported as income, and you may be subject to income tax on that value.

5. Mining Cryptocurrency: Mining cryptocurrency involves solving complex mathematical problems to validate transactions on the blockchain network. When you successfully mine cryptocurrency, the rewards obtained are generally considered taxable income. The value of the cryptocurrency at the time of receipt needs to be reported as income, and income tax may apply.

6. Airdrops and Forks: Airdrops occur when new tokens or cryptocurrencies are distributed for free to existing cryptocurrency holders. Forks, on the other hand, happen when a blockchain splits into two, resulting in a new cryptocurrency. Both airdrops and forks can have tax implications, as the newly acquired tokens or cryptocurrencies may be subject to income tax at their fair market value, or categorized as capital assets.

It is important to note that the taxation of these events may vary depending on the laws and regulations of your jurisdiction. Understanding the specific tax treatment and reporting requirements is crucial to ensure compliance and avoid potential penalties or audits.

Overall, being aware of the taxable events in cryptocurrency is essential for accurately reporting income and capital gains to tax authorities. If you have any doubts or questions about the tax implications of your cryptocurrency transactions, it is advisable to consult with a tax professional who specializes in cryptocurrency taxation.

Capital Gains Tax on Cryptocurrency

Capital gains tax is a significant component of the tax treatment of cryptocurrency transactions. When you sell or exchange cryptocurrency for a profit, it is considered a capital gain, and the tax implications vary depending on the holding period and the tax laws of your jurisdiction.

Short-term Capital Gains: If you hold cryptocurrency for one year or less before selling or exchanging it, any profits are typically categorized as short-term capital gains. Short-term capital gains are subject to ordinary income tax rates, which means they are taxed at the same rate as your regular income. It is important to note that short-term capital gains taxes can be higher than long-term capital gains taxes.

Long-term Capital Gains: If you hold cryptocurrency for more than one year before selling or exchanging it, any profits are generally considered long-term capital gains. Long-term capital gains are typically subject to lower tax rates than short-term gains. Depending on your income level, the long-term capital gains tax rates may vary. Some jurisdictions may offer preferential tax rates for long-term capital gains to incentivize long-term investment and economic growth.

Calculating Capital Gains: To calculate your capital gains or losses from cryptocurrency transactions, you need to determine the cost basis and the fair market value at the time of the transaction. The cost basis is the original purchase price of the cryptocurrency, including any fees or commissions paid. The fair market value is the current value of the cryptocurrency in fiat currency at the moment of the sale or exchange.

If the fair market value of your cryptocurrency at the time of sale or exchange is higher than the cost basis, you have a capital gain. Conversely, if the fair market value is lower, you have a capital loss. These gains or losses are reported on your tax return, and any capital gains tax owed is calculated based on your taxable income and applicable capital gains tax rates.

Offsetting Capital Gains and Losses: Capital losses from cryptocurrency transactions can be used to offset capital gains from other investments. If you have capital losses, you can apply them against your capital gains to reduce your overall tax liability. However, there may be specific rules and limitations on how losses can be used to offset gains, such as wash-sale rules that prevent claiming losses if a substantially identical asset is repurchased within a certain period.

Reporting Capital Gains: The reporting of capital gains from cryptocurrency transactions varies depending on the tax laws of your jurisdiction. In many cases, you need to report your capital gains and losses on Schedule D of your tax return, along with the required supporting documentation. Failure to accurately report these transactions can lead to penalties, fines, or audits from tax authorities.

It is important to stay informed about the tax laws and regulations surrounding cryptocurrency and consult with a tax professional or accountant who is knowledgeable in cryptocurrency taxation. Seeking professional advice can help ensure that you accurately calculate and report your capital gains from cryptocurrency transactions, optimizing your tax position while staying compliant with the tax laws in your jurisdiction.

Reporting Cryptocurrency Transactions

Accurate and timely reporting of cryptocurrency transactions is crucial to ensure compliance with tax laws and regulations. Due to the decentralized and complex nature of cryptocurrencies, specific reporting requirements may vary depending on your jurisdiction. Here are some key considerations for reporting cryptocurrency transactions:

1. Transaction Records: It is essential to maintain detailed records of all cryptocurrency transactions. These records should include information such as the date and time of each transaction, the type of transaction (buying, selling, exchanging, or using cryptocurrency for goods/services), the amount of cryptocurrency involved, the value in both cryptocurrency and fiat currency at the time of the transaction, and any associated fees or commissions.

2. Conversion Rates: When reporting cryptocurrency transactions, you may need to convert the transaction amounts from cryptocurrency to fiat currency value at the time of the transaction. The conversion rate can be obtained from reputable cryptocurrency exchanges or financial data sources. Using accurate and consistent conversion rates is important for proper reporting.

3. Capital Gains and Losses: Capital gains and losses from cryptocurrency transactions should be calculated and reported accurately. Determine the cost basis (original purchase price plus any fees), as well as the fair market value of the cryptocurrency at the time of the transaction. Calculate the capital gains or losses based on the difference between the sale/exchange value and the cost basis.

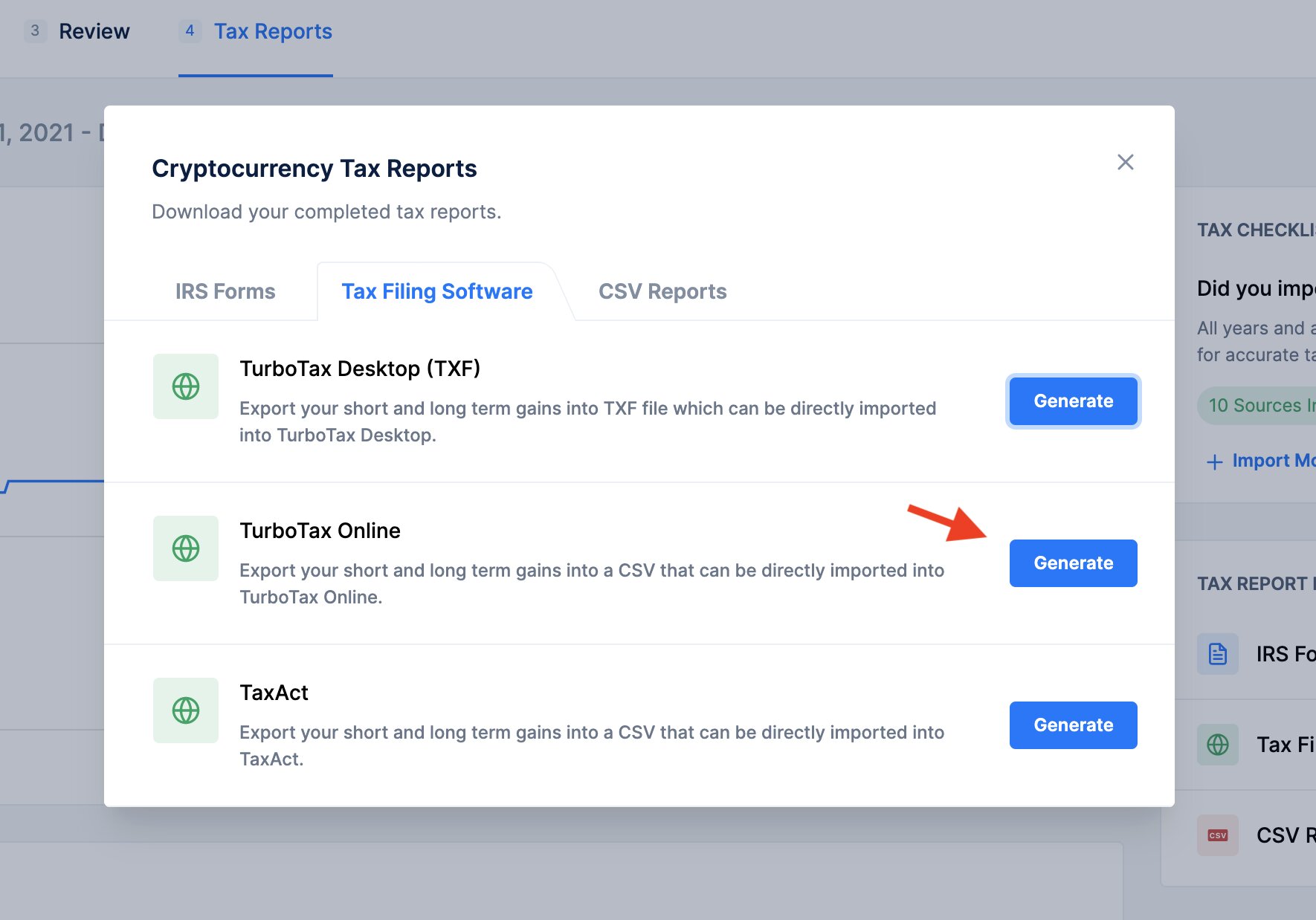

4. Tax Forms: Depending on your jurisdiction, you may need to report cryptocurrency transactions on specific tax forms. In the United States, for example, you may report capital gains and losses from cryptocurrency on IRS Form 8949, which is then used to complete Schedule D of your tax return. Familiarize yourself with the tax forms and schedules required by your tax authority to ensure proper reporting.

5. Third-Party Exchanges and Wallets: If you use cryptocurrency exchanges or digital wallets to facilitate transactions, it is important to gather the necessary records and statements from these platforms. Many exchanges provide transaction histories, which can help verify and support your reported cryptocurrency transactions. Some tax authorities may require you to report these transactions on specific forms or schedules.

6. Reporting Thresholds: Be aware of reporting thresholds set by tax authorities. In some jurisdictions, you may not be required to report cryptocurrency transactions below a certain value or frequency. However, it is still important to keep accurate records and consult with a tax professional to determine whether you meet the reporting thresholds or if reporting is recommended for other reasons, such as ensuring proper compliance.

7. Seek Professional Assistance: Given the complexities and evolving nature of cryptocurrency taxation, it is advisable to seek the guidance of a tax professional or accountant specializing in cryptocurrency transactions. They can help you navigate the reporting requirements, ensure compliance with tax laws, and maximize potential tax benefits.

By maintaining thorough records, calculating capital gains and losses accurately, and reporting cryptocurrency transactions in accordance with the tax laws of your jurisdiction, you can ensure compliance and minimize the risk of penalties or audits. Stay informed about the evolving tax guidelines and seek professional assistance to navigate the reporting process effectively.

Foreign Cryptocurrency Investments

With the global nature of cryptocurrencies, investors often engage in foreign cryptocurrency investments by trading on international exchanges or holding investments in foreign-based cryptocurrencies. Foreign cryptocurrency investments introduce additional considerations and reporting requirements that investors need to be aware of to comply with tax laws and regulations.

1. Reporting Foreign Accounts: If you hold cryptocurrency investments in foreign accounts, you may be subject to additional reporting requirements. Many countries have adopted regulations such as the Foreign Account Tax Compliance Act (FATCA) or foreign bank account reporting (FBAR) requirements. These regulations may require taxpayers to disclose their foreign cryptocurrency accounts and report their holdings or transactions.

2. Currency Exchange Rates: When dealing with foreign cryptocurrency investments, you need to consider currency exchange rates when calculating gains or losses for tax purposes. For example, if you purchase a foreign-based cryptocurrency using your local fiat currency, the exchange rate between the two currencies at the time of purchase will affect the cost basis and potential gain/loss when you eventually sell or exchange that cryptocurrency.

3. Tax Treaties: Depending on the tax treaties between your country and the foreign jurisdiction where your cryptocurrency investments are located, there may be provisions that impact how your investments are taxed. Tax treaties can affect withholding tax rates, tax credits, and other aspects of cross-border taxation. Familiarize yourself with the relevant tax treaties to understand how they may influence the taxation of your foreign cryptocurrency investments.

4. Reporting Obligations: Understand the reporting obligations specific to your jurisdiction regarding foreign cryptocurrency investments. This may involve disclosing the existence of foreign accounts, reporting income or gains generated from those investments, and complying with any anti-money laundering (AML) or know-your-customer (KYC) requirements imposed by the foreign jurisdiction.

5. Exchange Regulations: Be aware of any regulatory restrictions or requirements imposed by foreign jurisdictions when it comes to trading or holding foreign-based cryptocurrencies. Some countries may have specific rules or licensing requirements for cryptocurrency exchanges or may restrict access to certain cryptocurrencies. Ensure your activities comply with applicable regulations to avoid legal complications.

6. Seek Professional Guidance: Given the complexity of foreign cryptocurrency investments and their tax implications, it is advisable to seek guidance from a tax professional or accountant experienced in international taxation. They can assist you in navigating the reporting requirements, understanding tax treaties, and ensuring compliance with the tax laws of both your home country and the foreign jurisdiction where your investments are held.

Foreign cryptocurrency investments add an additional layer of complexity to an already intricate tax landscape. It is essential to understand and fulfill the reporting obligations related to these investments to maintain compliance with tax laws and regulations in both your home country and the foreign jurisdiction. Seeking professional advice can help you navigate the intricacies of foreign cryptocurrency investments and optimize your tax position.

Tax Withholding and Estimated Payments

When it comes to cryptocurrency taxation, tax withholding and estimated payments play a crucial role in ensuring compliance with tax obligations. Understanding these concepts can help cryptocurrency investors stay on top of their tax responsibilities and avoid potential penalties or underpayment of taxes.

1. Tax Withholding: Tax withholding refers to the practice of deducting taxes from income or gains at the source, before the funds are received by the taxpayer. In some jurisdictions, cryptocurrency exchanges or platforms may be required to withhold a certain percentage of taxes on cryptocurrency transactions. This means that when you sell or exchange cryptocurrency on such platforms, the platform withholds the applicable tax amount and remits it to the tax authorities on your behalf.

2. Estimated Payments: Estimated tax payments are periodic payments made throughout the tax year to prepay the expected tax liability. Cryptocurrency investors who have significant income or gains from their cryptocurrency activities may be required to make estimated tax payments to ensure they meet their tax obligations. The specific rules and requirements for estimating and making these payments vary by jurisdiction. It is crucial to understand your jurisdiction’s tax laws and consult with a tax professional to ensure you make accurate and timely estimated tax payments.

3. Self-Employment Tax: If you receive cryptocurrency as payment for freelance work or operate a cryptocurrency mining business, you may be subject to self-employment taxes. Self-employment taxes typically cover Social Security and Medicare taxes. It is important to calculate and pay these taxes in addition to any income taxes that may be applicable on your self-employment income.

4. Failure to Withhold or Make Estimated Payments: Failing to properly withhold taxes or make estimated tax payments can result in underpayment penalties or interest charges. It is essential to stay up to date with the tax laws applicable to your jurisdiction and make accurate calculations to avoid any potential penalties. Consulting with a tax professional can help ensure that you are meeting your tax withholding and estimated payment requirements.

5. Record-Keeping: Keeping accurate and organized records of your cryptocurrency activities, including transactions, income, and expenses, is crucial for calculating your tax liability and meeting reporting requirements. Good record-keeping practices enable you to track your income and gains, properly determine cost basis, and support any deductions or credits you may be eligible for. Utilize software or tools specifically designed for cryptocurrency record-keeping to simplify this process.

6. Seek Professional Advice: Given the complexities surrounding tax withholding and estimated payments in the cryptocurrency space, it is recommended to seek the guidance of a tax professional or accountant with expertise in cryptocurrency taxation. They can help you navigate the specific requirements of your jurisdiction and provide invaluable advice to ensure compliance and optimize your tax position.

Understanding tax withholding and estimated payments is vital for cryptocurrency investors to fulfill their tax responsibilities. Familiarize yourself with the rules and requirements specific to your jurisdiction, maintain accurate records, and consult with a tax professional to ensure that you are meeting your obligations and optimizing your tax position.

Tax Strategies for Cryptocurrency Investors

As a cryptocurrency investor, you can employ specific tax strategies to minimize your tax liability, maximize tax benefits, and optimize your overall financial position. Here are some tax strategies to consider:

1. Holding Period: The holding period of your cryptocurrency can have a significant impact on the tax treatment and the applicable tax rates. If you hold your cryptocurrency for more than a year before selling or exchanging it, you may qualify for lower long-term capital gains tax rates. Consider the potential tax advantages of holding your cryptocurrency for an extended period to benefit from lower tax rates.

2. Tax-Loss Harvesting: Tax-loss harvesting involves strategically selling cryptocurrency assets that have experienced a loss to offset other capital gains. By realizing capital losses, you can reduce your overall tax liability. However, be mindful of the wash-sale rules in your jurisdiction, which prevent you from repurchasing the same or substantially identical cryptocurrency assets within a designated time frame.

3. Gifting and Donating Cryptocurrency: Gifting or donating cryptocurrency can be a tax-efficient strategy. By gifting cryptocurrency to family or friends, you can potentially transfer the tax burden to the recipient, especially if they are in a lower tax bracket. Additionally, donating cryptocurrency to eligible charitable organizations can provide you with a tax deduction based on the fair market value at the time of the donation.

4. Tax-Advantaged Accounts: Consider investing in tax-advantaged retirement accounts, such as Individual Retirement Accounts (IRAs) or Self-Directed Solo 401(k)s, that allow for cryptocurrency investments. Contributions to these accounts may have tax advantages, such as tax-deferred growth or tax-free withdrawals in retirement. Consult with a financial advisor or tax professional to understand the specific rules and requirements related to cryptocurrency investments within these accounts.

5. Proper Documentation and Reporting: Maintaining detailed and accurate records of your cryptocurrency transactions is crucial. Keep track of the dates, transaction amounts, values, and any associated costs or fees. Use digital tools or software specifically designed for cryptocurrency record-keeping to simplify the process. Proper documentation ensures correct reporting, reduces the risk of errors or audits, and allows you to take advantage of any available deductions or credits.

6. Seek Professional Guidance: Given the intricacies of cryptocurrency taxation, consulting with a tax professional or accountant specializing in cryptocurrency is highly recommended. They can provide personalized advice tailored to your specific situation, help you navigate complex tax regulations, and maximize your tax benefits while ensuring compliance with reporting requirements.

It is essential to stay updated with the tax laws in your jurisdiction and explore the various tax strategies available to cryptocurrency investors. By employing sound tax strategies, you can minimize the impact of taxes on your cryptocurrency investments and optimize your overall financial position.

Conclusion

The tax implications of cryptocurrency transactions can be complex and vary depending on the jurisdiction in which you reside. As a cryptocurrency investor, it is crucial to understand and comply with the tax laws and reporting requirements specific to your jurisdiction to ensure proper tax compliance.

Throughout this article, we have covered various aspects of cryptocurrency taxation, including capital gains tax, reporting requirements, foreign cryptocurrency investments, tax withholding, estimated payments, and tax strategies. By familiarizing yourself with these concepts and seeking professional advice when needed, you can effectively manage your tax obligations while optimizing your tax position.

Accurate record-keeping is essential in the world of cryptocurrency taxation. Keeping detailed records of your cryptocurrency transactions, including dates, types, amounts, and values, is crucial for calculating accurate capital gains or losses and fulfilling reporting requirements. Utilize specialized software or tools designed for cryptocurrency record-keeping to simplify the process and ensure accuracy.

Remember to stay informed about any updates or changes in the tax laws and regulations regarding cryptocurrency in your jurisdiction. The evolving nature of cryptocurrencies requires ongoing vigilance and an understanding of any new tax guidelines or reporting obligations that may arise.

Lastly, seeking professional guidance from a tax professional or accountant well-versed in cryptocurrency taxation can provide invaluable support. They can provide personalized advice, help you navigate complex tax regulations, and ensure compliance with reporting requirements, optimizing your tax position while minimizing the risk of penalties or audits.

By understanding the tax implications associated with cryptocurrency transactions and implementing the appropriate tax strategies, you can effectively manage your tax liabilities, maximize tax benefits, and ensure compliance with tax laws. Stay proactive, keep accurate records, and consult with experts to navigate the complex world of cryptocurrency taxation successfully.