What is cryptocurrency?

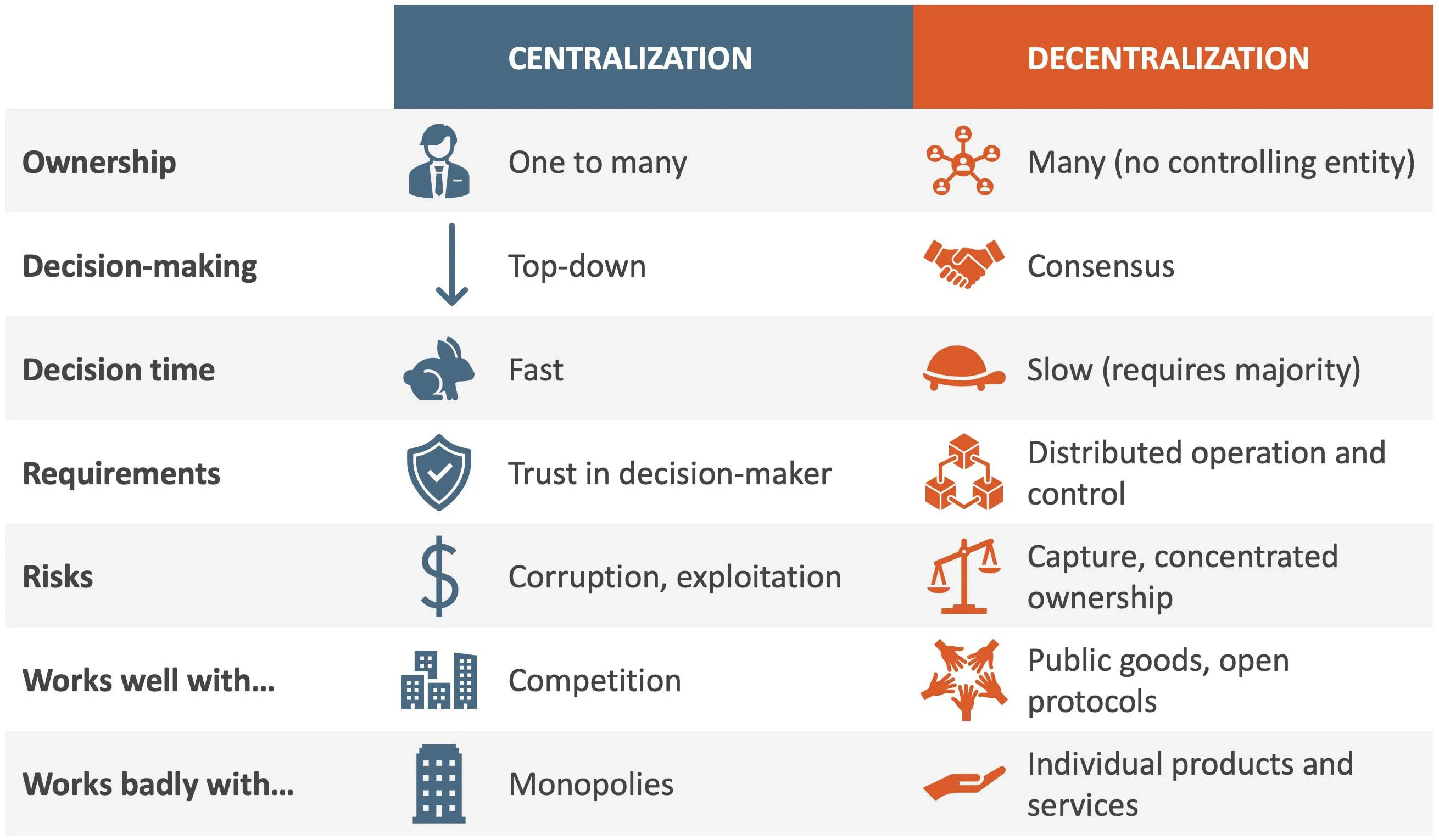

Cryptocurrency is a digital or virtual form of currency that uses cryptography for secure financial transactions, control the creation of new units, and verify the transfer of assets. It is decentralized and operates on a technology called blockchain, which is a distributed ledger system.

Unlike traditional currencies issued by governments, such as the US dollar or the Euro, cryptocurrencies are not physically tangible and exist only in electronic form. They are based on cryptographic principles that secure transactions and control the creation of new units. This decentralized nature and encryption make cryptocurrencies highly secure and resistant to fraud.

The most well-known and widely used cryptocurrency is Bitcoin, which was introduced in 2009 by an anonymous person or group of people using the pseudonym Satoshi Nakamoto. Since then, thousands of other cryptocurrencies, known as altcoins, have been developed, each with its own unique features and purposes.

Cryptocurrencies offer several advantages over traditional forms of payment. They provide faster and cheaper transactions, as they eliminate the need for intermediaries such as banks or payment processors. Additionally, cryptocurrencies enable cross-border transactions without the need for currency conversion, making them highly convenient for international transfers.

Furthermore, cryptocurrencies offer privacy and anonymity in transactions. While the details of each transaction are recorded on the blockchain, the identities of the transacting parties are often pseudonymous, providing a level of privacy not typically found in traditional banking systems.

Overall, cryptocurrencies have gained significant popularity and are increasingly being adopted by businesses and individuals around the world. They offer a new form of digital currency that is secure, efficient, and can revolutionize various aspects of financial transactions and services.

How does cryptocurrency work?

Cryptocurrency operates on a decentralized technology called blockchain. A blockchain is a distributed ledger that records and verifies transactions across multiple computers or nodes. Here’s a simplified explanation of how cryptocurrency works:

1. Transactions: When someone initiates a cryptocurrency transaction, it is broadcasted to the network of computers running the blockchain software. These transactions are secured through cryptography, ensuring their integrity and privacy.

2. Validation: The network of computers validates the transaction by verifying the details and ensuring that the user has sufficient funds to make the transaction. This process is performed by specialized nodes called miners, who compete to solve complex mathematical problems to validate the transactions and add them to the blockchain.

3. Adding to the Blockchain: Once the transaction is validated, it is grouped with other transactions into a block. Miners compete to add the new block to the blockchain by solving the mathematical problem associated with it. This process is known as mining and requires significant computational power.

4. Consensus Mechanism: Cryptocurrencies use different consensus mechanisms to agree on the valid state of the blockchain. The most common consensus mechanism is called Proof of Work (PoW), where miners compete to solve complex mathematical puzzles and the first to solve it adds the block to the blockchain. Other cryptocurrencies use variants like Proof of Stake (PoS), Delegated Proof of Stake (DPoS), or Byzantine Fault Tolerance (BFT).

5. Security and Integrity: Once a transaction is added to the blockchain, it is incredibly difficult to alter or tamper with. The decentralized nature of the blockchain and the use of cryptographic techniques ensure the security and immutability of the transactions.

6. Wallets: Cryptocurrency holders use digital wallets to store and manage their cryptocurrencies. These wallets securely store the user’s private keys, which are needed to access and sign transactions.

7. Peer-to-Peer Transactions: Cryptocurrencies enable direct peer-to-peer transactions without the need for intermediaries such as banks. Users can send and receive funds securely and quickly across the globe, with minimal transaction fees.

Overall, cryptocurrencies leverage blockchain technology to create a decentralized, secure, and transparent system for financial transactions. They eliminate the need for intermediaries, offer privacy and security, and have the potential to transform various industries beyond the realm of finance.

How to choose a cryptocurrency wallet

A cryptocurrency wallet is a software program or a physical device that allows users to securely store, manage, and interact with their cryptocurrencies. Choosing the right wallet is crucial to ensure the safety of your digital assets. Here are some factors to consider when selecting a cryptocurrency wallet:

1. Security: The first and most important aspect to consider is security. Look for wallets that offer strong encryption, two-factor authentication (2FA), and backup and recovery options. Ensure that the wallet uses industry-standard security protocols to protect your private keys and funds.

2. Type of Wallet: There are different types of wallets available, including desktop, mobile, web, and hardware wallets. Desktop wallets are installed on your computer, mobile wallets are apps for smartphones, web wallets are accessed through a browser, and hardware wallets are physical devices. Each type has its own advantages and considerations. Hardware wallets are generally considered the most secure since they store your private keys offline.

3. Supported Cryptocurrencies: Check if the wallet supports the cryptocurrencies you are interested in storing. Not all wallets support all cryptocurrencies. Make sure the wallet you choose is compatible with the specific digital assets you own.

4. User-Friendly Interface: Consider the ease of use and user interface of the wallet. A good wallet should have a simple and intuitive interface that makes it easy to send and receive funds, view transaction history, and manage your portfolio.

5. Development Team and Reputation: Research the wallet’s development team and reputation within the cryptocurrency community. Look for wallets that have a strong track record and positive reviews from users. It is also important to choose a wallet that is regularly updated and supported by an active development team.

6. Community Support: Consider the level of community support and resources available for the wallet. A strong and active community can provide valuable assistance and guidance if you encounter any issues or have questions about using the wallet.

7. Additional Features: Some wallets offer additional features like built-in exchange services, multi-signature support, and integration with popular decentralized applications (dApps). Assess if these additional features align with your needs and preferences.

8. Customer Support: Finally, consider the availability and responsiveness of customer support provided by the wallet. In case you encounter any issues or need assistance, it is comforting to know that there is reliable customer support to help you navigate through any problems.

By considering these factors, you can make an informed decision when choosing a cryptocurrency wallet that meets your security requirements and fits your needs for ease of use and functionality.

How to buy cryptocurrency

Buying cryptocurrency can seem intimidating for those new to the world of digital currencies, but the process is actually quite straightforward. Here’s a step-by-step guide on how to buy cryptocurrency:

1. Choose a cryptocurrency exchange: Start by selecting a reputable cryptocurrency exchange platform. There are many exchanges to choose from, so consider factors such as security, user interface, supported cryptocurrencies, fees, and availability in your region.

2. Sign up and complete the verification process: Create an account on your chosen exchange platform and go through the necessary verification process. This typically involves providing identification documents and personal information to comply with Know Your Customer (KYC) and Anti-Money Laundering (AML) regulations.

3. Deposit funds: Once your account is set up and verified, you’ll need to deposit funds into your exchange account. Most exchanges accept deposits in traditional currencies like USD, EUR, or GBP. You can usually deposit funds via bank transfer, credit/debit card, or cryptocurrency transfer from an external wallet.

4. Choose the cryptocurrency to buy: Select the cryptocurrency you wish to buy. Popular options include Bitcoin (BTC), Ethereum (ETH), Litecoin (LTC), and many others. You can usually find a wide range of cryptocurrencies available for purchase on most exchanges.

5. Place an order: Decide on the amount of cryptocurrency you want to buy and place an order on the exchange. You can choose between market orders, which execute at the current market price, or limit orders, which let you set a specific price at which you want to buy.

6. Monitor your purchase: Once your order is placed, keep an eye on the exchange platform as your purchase is processed. It may take a few minutes for the transaction to be completed, especially during times of high market activity.

7. Secure your cryptocurrency: After the transaction is confirmed, consider transferring your purchased cryptocurrency to a secure wallet that you control. While many exchanges have their own wallets, using a personal wallet provides an extra layer of security.

Remember to exercise caution while buying cryptocurrency and be aware of potential scams. Only use reputable exchanges, safeguard your login credentials and use two-factor authentication (2FA) to protect your account.

It’s important to note that the market value of cryptocurrencies can be volatile, so be prepared for price fluctuations after your purchase. It’s advisable to do thorough research and possibly consult with a financial advisor before investing significant amounts.

By following these steps, you can confidently buy your desired cryptocurrency and start participating in the exciting world of digital currencies.

How to store and secure your cryptocurrency

As a cryptocurrency holder, it is crucial to prioritize the security of your digital assets. The following are important steps to store and secure your cryptocurrency:

1. Use a secure wallet

Select a secure cryptocurrency wallet to store your digital assets. Hardware wallets, such as Ledger and Trezor, are often recommended for their high level of security. These devices store your private keys offline, reducing the risk of them being exposed to online threats. Alternatively, you can use software wallets like Trust Wallet or Exodus, which offer a combination of convenience and security.

2. Keep your private keys offline

Keep your private keys offline and never share them with anyone. Private keys grant access to your funds and should be kept secure. Consider writing down your private keys on a piece of paper and storing it in a safe place, like a bank vault or a secure home safe. Avoid saving them digitally, as online storage increases the risk of hacks and unauthorized access.

3. Enable two-factor authentication (2FA)

Enable two-factor authentication (2FA) on your cryptocurrency exchanges and wallets. 2FA adds an extra layer of security by requiring a second verification step, usually through a mobile app or SMS code, to access your accounts. This added step ensures that even if your password is compromised, unauthorized access to your funds is significantly harder.

4. Be cautious of phishing attempts

Beware of phishing attempts, where scammers try to trick you into revealing sensitive information. Be cautious of emails, messages, or websites that appear to be from legitimate sources but are actually fraudulent. Always double-check URLs, verify the authenticity of communications, and never provide your private keys or login credentials to untrusted sources.

5. Keep your software up to date

Regularly update your wallet software, operating system, and security software to protect against any known vulnerabilities or bugs. Software updates often contain crucial security patches that help safeguard your funds and enhance the overall security of your digital assets.

6. Diversify your storage solutions

Consider diversifying your storage solutions by using multiple wallets or even multiple types of wallets. This way, if one wallet is compromised or malfunctions, your funds stored in other wallets remain secure. However, ensure you keep track of your wallets and private keys to avoid confusion or potential loss of access to your assets.

7. Backup your wallet

Regularly backup your wallet and keep multiple copies in secure locations. This backup will help you recover your funds in case of wallet loss, damage, or theft. Be mindful of where you store your backups and make sure they are protected from physical or digital threats.

By following these steps, you can significantly enhance the security of your cryptocurrency holdings. Remember that maintaining caution and staying informed about the latest security practices are essential to safeguarding your digital assets.

How to send and receive cryptocurrency

Sending and receiving cryptocurrency involves transferring digital assets between cryptocurrency wallets. Here’s a step-by-step guide on how to send and receive cryptocurrency:

Sending cryptocurrency:

1. Open your wallet: Launch your cryptocurrency wallet and ensure that you have sufficient funds in the wallet to send.

2. Enter recipient’s address: Obtain the recipient’s cryptocurrency wallet address. It is a long alphanumeric string that uniquely identifies their wallet. Enter this address in the “recipient” field of your wallet.

3. Specify the amount: Indicate the amount of cryptocurrency you want to send. Double-check that the amount is accurate and within your available balance. Note that some wallets allow you to specify the transaction fee, which affects the speed of the transaction.

4. Review transaction details: Carefully review the transaction details, including the recipient’s address and the amount to be sent. Once you are certain that all information is correct, confirm the transaction.

5. Authenticate the transaction: Depending on the security measures enabled on your wallet, you may need to provide additional verification, such as two-factor authentication (2FA) or a password. Follow the prompts to authenticate and confirm the transaction.

6. Wait for confirmation: After confirming the transaction, it is added to the network’s mempool, where it awaits validation by miners. Confirmation times may vary depending on the cryptocurrency and network congestion. You can track the progress and confirmation status on the blockchain explorer.

Receiving cryptocurrency:

1. Share your wallet address: To receive cryptocurrency, you need to share your wallet address with the sender. Your wallet address is a unique identifier consisting of a long alphanumeric string.

2. Double-check the address: It is important to double-check the accuracy of the wallet address before sharing it. Even a small mistake can result in the funds being sent to the wrong address and irretrievable loss.

3. Receive the funds: Once the sender initiates the transfer and it is confirmed by the network, the cryptocurrency will be deposited into your wallet. The transaction will reflect in your wallet’s transaction history, showing the sender’s address, amount, and timestamp.

4. Confirm the receipt: After receiving the funds, it is advisable to verify the balance in your wallet to ensure that the correct amount has been deposited. Remember to refresh your wallet or check the associated blockchain explorer for the latest balance.

5. Use the funds: You can now utilize the received cryptocurrency for various purposes, such as making purchases, trading, investing, or holding for future use.

It is important to note that transaction times and fees can vary depending on the cryptocurrency and network congestion. Additionally, always ensure that you are using the correct wallet address and exercise caution when sharing it to prevent any potential errors or fraud.

By following these steps, you can easily send and receive cryptocurrency, enabling seamless transactions and interactions within the digital asset ecosystem.

How to trade cryptocurrency

Trading cryptocurrency involves buying and selling digital assets on cryptocurrency exchanges. Whether you’re looking to capitalize on short-term price movements or invest for the long term, here’s a step-by-step guide on how to trade cryptocurrency:

1. Choose a reputable cryptocurrency exchange:

Select a cryptocurrency exchange that offers a wide range of tradable cryptocurrencies, robust security measures, competitive fees, and a user-friendly interface. Popular exchanges include Binance, Coinbase, Kraken, and Bitstamp.

2. Create an account and verify your identity:

Sign up for an account on your chosen exchange and complete the necessary verification process. This typically involves providing identification documents and personal information to comply with Know Your Customer (KYC) regulations.

3. Deposit funds:

Deposit funds into your exchange account. Most exchanges support deposits in fiat currencies like USD, EUR, or GBP. You can also deposit supported cryptocurrencies from external wallets to use for trading.

4. Understand the market:

Educate yourself about the cryptocurrency market and the specific cryptocurrencies you wish to trade. Stay informed about the latest news, trends, and developments that may impact cryptocurrency prices.

5. Set up a trading strategy:

Develop a trading strategy based on your goals, risk tolerance, and market analysis. Determine factors such as the type of trade (long-term or short-term), target profit levels, stop-loss levels, and risk management techniques.

6. Execute trades:

On the exchange platform, navigate to the trading section and select the cryptocurrency pair you want to trade. Place buy or sell orders based on your trading strategy. You can choose between market orders (executed at the current market price) or limit orders (set a specific price at which you want to buy or sell).

7. Monitor and manage your trades:

Monitor the progress of your trades and make necessary adjustments. You may want to set up alerts or use trading tools provided by the exchange to stay updated on price movements and market conditions.

8. Practice risk management:

Mitigate potential risks by setting stop-loss orders to limit losses and take-profit orders to secure profits. Diversify your trades and avoid investing more than you can afford to lose. Continuously assess your trades and adapt your strategy as needed.

9. Withdraw your funds:

Once you’ve achieved your trading goals, consider withdrawing your profits or moving funds to a secure wallet. Leaving funds on an exchange carries a higher risk due to potential security breaches or hacks.

Remember that trading cryptocurrency entails risks, including price volatility and market manipulation. It’s essential to conduct thorough research, keep emotions in check, and never invest more than you can afford to lose.

By following these steps and continuously learning and adapting, you can engage in cryptocurrency trading and potentially capitalize on market opportunities.

How to use cryptocurrency for online purchases

Using cryptocurrency for online purchases provides a secure, convenient, and globally accessible alternative to traditional payment methods. Here are the steps to follow when using cryptocurrency for online purchases:

1. Find merchants that accept cryptocurrency:

Look for online merchants and businesses that accept cryptocurrency as a form of payment. Many e-commerce platforms and online retailers now offer this option. Additionally, there are directories and websites specifically dedicated to listing businesses that accept cryptocurrency.

2. Create a digital wallet:

If you don’t already have a cryptocurrency wallet, create one. Choose a reliable wallet that supports the specific cryptocurrency you plan to use for your online purchases. Ensure that your wallet is compatible with your preferred device (such as desktop, mobile, or hardware) and offers a user-friendly interface.

3. Acquire cryptocurrency:

If you don’t already own the cryptocurrency you want to use for your online purchases, you’ll need to buy it. Use a reputable cryptocurrency exchange to purchase the desired cryptocurrency using fiat currency or another cryptocurrency. Once acquired, transfer the purchased cryptocurrency to your wallet.

4. Check compatibility and payment instructions:

Before making a purchase, check if the chosen merchant accepts the specific cryptocurrency you own. Additionally, review the payment instructions provided by the merchant. They may provide a unique payment address or QR code that you will need to initiate the payment from your wallet.

5. Initiate the payment:

Using your wallet, initiate the payment by pasting the merchant’s payment address or scanning the provided QR code. Enter the amount of cryptocurrency you wish to send and review the transaction details carefully. Once you are sure everything is accurate, confirm the transaction.

6. Wait for confirmation:

After confirming the transaction, it is added to the blockchain network for validation. Wait for the network to confirm the transaction. Confirmation times may vary depending on the cryptocurrency and network congestion. It is advisable to wait for a few confirmations to ensure the transaction has been successfully processed.

7. Verify the payment:

Once the transaction is confirmed, the merchant should receive the payment. In some cases, you may receive an email or notification confirming the successful payment. Keep a record of the transaction details for future reference.

8. Ensure security and privacy:

While cryptocurrency transactions are generally secure, it’s important to take additional measures to protect your information. Ensure that you are using a trusted merchant website, use secure internet connections, and consider utilizing privacy-focused features available in certain cryptocurrencies.

By following these steps, you can successfully use cryptocurrency for online purchases, enjoying the benefits of secure, borderless transactions while contributing to the growing adoption of digital currencies in the e-commerce space.

How to use cryptocurrency for investments

Using cryptocurrency for investments can be an exciting opportunity to diversify your portfolio and potentially achieve financial growth. Here’s a guide on how to use cryptocurrency for investments:

1. Conduct thorough research:

Before investing in any cryptocurrency, conduct thorough research to understand its underlying technology, use cases, market trends, and potential risks. Stay updated with the latest news and developments in the cryptocurrency space to make informed investment decisions.

2. Choose the right cryptocurrency:

Consider investing in cryptocurrencies that align with your investment goals, risk tolerance, and personal interests. Bitcoin (BTC) and Ethereum (ETH) are the most established and widely recognized cryptocurrencies, but there are thousands of other options, known as altcoins, to explore.

3. Select a reputable cryptocurrency exchange:

Choose a reputable cryptocurrency exchange that offers a wide range of cryptocurrencies, robust security measures, competitive fees, and user-friendly features. Some popular exchanges include Coinbase, Binance, Kraken, and Gemini. Ensure that the chosen exchange is available in your region and complies with regulatory standards.

4. Create an account and verify your identity:

Sign up for an account on your chosen cryptocurrency exchange and complete the necessary verification process. This typically involves providing identification documents and personal information to comply with Know Your Customer (KYC) regulations.

5. Deposit funds into your exchange account:

Deposit funds into your exchange account using fiat currency or other cryptocurrencies. The deposit methods may vary depending on the exchange, but common options include bank transfers, credit/debit cards, and cryptocurrency transfers from external wallets.

6. Set a budget and establish a risk management strategy:

Set a budget for your investments and establish a risk management strategy that aligns with your financial goals. Determine the percentage of your overall portfolio that you are comfortable allocating to cryptocurrency investments and stick to your predetermined budget.

7. Start with a diverse portfolio:

Consider diversifying your cryptocurrency investments by allocating funds to multiple cryptocurrencies. This helps spread the risk and reduces the impact of any individual cryptocurrency’s price volatility. Research and select a mix of well-established cryptocurrencies and promising projects in various sectors.

8. Monitor your investments:

Regularly monitor the performance of your cryptocurrency investments. Utilize the tools and resources available on the cryptocurrency exchange platform, as well as external sources, to track market trends, price movements, and news updates related to your investments.

9. Consider long-term holding:

While short-term trading can be lucrative, consider the potential benefits of long-term holding, also known as “HODLing.” Cryptocurrency markets can be highly volatile, and holding onto a well-researched cryptocurrency for an extended period can allow for potential growth and capitalizing on long-term trends.

10. Stay updated and adapt:

Continuously educate yourself about the cryptocurrency market and adapt your investment strategy as needed. Markets can change rapidly, and it’s important to stay aware of new opportunities, potential risks, and evolving regulatory landscapes.

Investing in cryptocurrency comes with risks, and it’s essential to only invest what you can afford to lose. Consult with a financial advisor if needed, and regularly reassess your investment decisions based on your financial situation and risk tolerance.

By following these steps and exercising due diligence, you can use cryptocurrencies as an investment tool, potentially diversifying your portfolio and capitalizing on the growth of this innovative asset class.

How to use cryptocurrency for fundraising

Cryptocurrencies have opened up new avenues for fundraising, providing innovative solutions for individuals and organizations to raise funds for various causes. Here’s a guide on how to use cryptocurrency for fundraising:

1. Define your fundraising goals:

Start by defining your fundraising goals and the purpose of your campaign. Determine how much funds you need to raise, the timeline for the campaign, and the specific cause or project that the funds will support.

2. Choose a suitable cryptocurrency:

Select a cryptocurrency that aligns with your fundraising goals. Bitcoin (BTC) and Ethereum (ETH) are popular choices, but consider other cryptocurrencies that may fit your cause or have a strong community aligned with your mission.

3. Set up a cryptocurrency wallet:

Create a cryptocurrency wallet that supports the chosen cryptocurrency. This will be used to receive and securely store the donated funds. Choose a reputable wallet provider that offers strong security measures.

4. Educate potential donors:

Educate potential donors about cryptocurrencies and the benefits of donating using digital currencies. Explain the potential impact of their contributions and how cryptocurrency donations can provide transparency, traceability, and ease of cross-border transactions.

5. Promote your campaign:

Spread the word about your fundraising campaign through various channels. Leverage social media, email newsletters, and community forums to raise awareness about your cause and the option to donate using cryptocurrencies. Consider reaching out to cryptocurrency influencers or partnering with crypto-related platforms to amplify your message.

6. Provide clear donation instructions:

Clearly provide donation instructions to potential donors. Include your cryptocurrency wallet address, any specific requirements for donations, and guidelines for different donation amounts. Consider providing step-by-step instructions for first-time cryptocurrency donors.

7. Track and acknowledge donations:

Monitor and track the incoming cryptocurrency donations. Ensure that you have processes in place to accurately track each donation and acknowledge them appropriately. Send personalized thank-you messages or provide updates on the progress of your fundraising campaign to show gratitude to your donors.

8. Adhere to regulations:

Consider any legal and regulatory requirements related to fundraising in your jurisdiction. Ensure compliance with tax laws and any necessary reporting obligations when accepting and using cryptocurrency donations for fundraising purposes.

9. Consider utilizing smart contracts:

Explore the use of smart contracts, especially if you are conducting a fundraising campaign with specific milestones or conditions. Smart contracts can automate the distribution of funds based on predefined rules, enhancing transparency and trust in the fundraising process.

10. Stay engaged and provide updates:

Keep your donors engaged by providing regular updates on the progress of your fundraising campaign and its impact. Share success stories, milestones reached, or future plans to maintain the trust and support of your donors.

By following these steps and leveraging the features of cryptocurrencies, you can create innovative and efficient fundraising campaigns, providing a secure and transparent way for individuals and organizations to support your cause.

How to use cryptocurrency for remittances

Cryptocurrencies have the potential to revolutionize the remittance industry, offering a faster, more cost-effective, and efficient alternative to traditional money transfer methods. Here’s a guide on how to use cryptocurrency for remittances:

1. Choose a suitable cryptocurrency:

Select a cryptocurrency that is widely accepted and has good liquidity in both the sender’s and recipient’s countries. Bitcoin (BTC) and stablecoins like Tether (USDT) or Dai (DAI) are commonly used for remittances due to their global availability and relatively stable value.

2. Set up cryptocurrency wallets:

Both the sender and recipient need to have cryptocurrency wallets. The sender’s wallet is used to convert fiat currency into cryptocurrency, while the recipient’s wallet is used to receive and convert the cryptocurrency back into local currency. Choose user-friendly wallets that support the chosen cryptocurrency.

3. Convert fiat currency to cryptocurrency:

The sender needs to convert their local fiat currency into cryptocurrency. This can be done by depositing funds into a cryptocurrency exchange that supports fiat-to-crypto conversions. After the conversion, the sender’s wallet will hold the equivalent amount of cryptocurrency.

4. Initiate the remittance:

Using their wallet, the sender initiates the remittance by specifying the recipient’s cryptocurrency wallet address and the amount of cryptocurrency to be sent. Ensure that both the sender and recipient have agreed on the cryptocurrency to be used and the corresponding exchange rate to avoid any confusion.

5. Confirm the transaction:

The sender reviews the transaction details, including the recipient’s wallet address and the amount of cryptocurrency to be sent. Once confirmed, the transaction is broadcasted to the cryptocurrency network for validation and inclusion in the blockchain.

6. Convert cryptocurrency to local currency:

Upon receiving the cryptocurrency, the recipient can convert it to their local fiat currency. This can be done by using a local cryptocurrency exchange or a peer-to-peer platform that facilitates cryptocurrency-to-fiat conversions. The converted funds are then deposited into the recipient’s bank account or provided in cash, depending on the available options.

7. Monitor and track the transaction:

Both the sender and recipient can track the progress of the transaction using the transaction ID or wallet address provided by the sender. Cryptocurrency transactions are typically posted on the blockchain, allowing for easy visibility and transparency.

8. Consider exchange rate risks:

Fluctuations in the exchange rate between the cryptocurrency and the local fiat currency can impact the final remittance amount received by the recipient. It’s important to consider this exchange rate risk and potential fees associated with the conversion to ensure that the remittance amount meets the recipient’s needs.

9. Understand local regulations and compliance:

Be aware of any local regulations and compliance requirements related to cryptocurrency remittances in the sender’s and recipient’s countries. Ensure compliance with applicable money transmission laws, tax obligations, and any reporting requirements to avoid legal issues.

By utilizing cryptocurrencies for remittances, individuals can benefit from faster, cost-effective cross-border transfers, especially in regions with limited access to traditional banking services. However, it’s crucial to understand the risks involved and adhere to local regulations to ensure a smooth and secure remittance process.

How to use cryptocurrency for privacy and anonymity

Cryptocurrencies can offer enhanced privacy and anonymity compared to traditional financial systems. If you value privacy and want to maintain your anonymity while using cryptocurrencies, here are some steps to follow:

1. Use privacy-focused cryptocurrencies:

Choose cryptocurrencies that prioritize privacy and anonymity. Examples of privacy-focused cryptocurrencies include Monero (XMR), Zcash (ZEC), and Dash (DASH). These cryptocurrencies utilize advanced cryptographic techniques to obfuscate transaction details and protect user identities.

2. Utilize private wallets:

Use wallets that offer built-in privacy features. Certain wallets, such as Monero’s official wallet or the Zcash Sapling-enabled wallets, are specifically designed to enhance transaction privacy. These wallets employ advanced encryption techniques and privacy protocols to safeguard your transaction data.

3. Mix your transactions:

Consider utilizing cryptocurrency mixing services, also known as tumblers, which help break the link between your original transaction and the destination address. Mixing services combine transactions from multiple users and redistribute the funds, making it difficult to trace the origin or destination of the coins.

4. Use anonymous communication channels:

If privacy is a top concern, use anonymous communication channels, such as Tor or Virtual Private Networks (VPNs), when accessing cryptocurrency-related websites, exchanges, or wallet services. These tools can help mask your IP address and make it harder for third parties to track your online activities.

5. Avoid using personal identifiable information (PII):

When creating accounts or participating in cryptocurrency-related activities, avoid providing unnecessary personally identifiable information (PII). Instead, use pseudonyms or anonymous usernames to help maintain your online privacy and separate your cryptocurrency activities from your real-world identity.

6. Be cautious with public addresses:

Publicly shared cryptocurrency addresses can be linked to your identity, potentially compromising privacy. Consider using different addresses for each transaction and avoid reusing addresses whenever possible. Additionally, utilize the privacy features offered by certain cryptocurrencies, such as stealth addresses or shielded transactions.

7. Conduct peer-to-peer (P2P) transactions:

Utilize peer-to-peer cryptocurrency exchanges and decentralized platforms to trade or transact directly with other individuals. P2P transactions can offer greater privacy by eliminating the need for intermediaries and reducing the possibility of your transactions being traced or monitored.

8. Stay informed about privacy enhancements:

Keep abreast of the latest advancements in privacy-oriented technologies and features within the cryptocurrency ecosystem. Participate in community discussions, follow project updates and news sources that focus on privacy-related developments, and adopt new tools and techniques that can help strengthen your privacy.

It’s important to note that while cryptocurrencies can enhance privacy and anonymity, they are not completely anonymous by default. Persistent effort is required to maintain privacy and stay ahead of potential privacy risks and emerging technologies that may impact anonymity.

By following these steps and adopting privacy-centric practices, you can take greater control of your privacy and anonymity while using cryptocurrencies.

How to use cryptocurrency for charity

Cryptocurrencies have opened up new possibilities for charitable giving, enabling individuals and organizations to make donations in a secure, transparent, and efficient manner. If you are interested in using cryptocurrency for charitable purposes, here’s a guide on how to do so:

1. Research and select a reputable charity:

Start by researching and selecting a reputable charity or nonprofit organization that aligns with your philanthropic goals. Look for organizations that have a track record of transparency and accountability in their operations.

2. Verify the charity’s acceptance of cryptocurrency:

Ensure that the chosen charity accepts donations in cryptocurrencies. Check their website or contact them directly to confirm their cryptocurrency donation options. Some charities may have preferred cryptocurrencies or specific wallets for receiving donations.

3. Choose a suitable cryptocurrency:

Select a cryptocurrency that you wish to donate. Consider factors such as the charity’s preference, liquidity of the chosen cryptocurrency, and any potential tax implications. Popular choices for charitable donations include Bitcoin (BTC), Ethereum (ETH), and Ripple (XRP).

4. Set up a digital wallet:

Create a digital wallet for the chosen cryptocurrency. Ensure that the wallet is secure and compatible with the cryptocurrency you plan to donate. Use a reputable wallet provider that offers strong security features.

5. Make the donation:

Transfer the desired amount of cryptocurrency from your wallet to the charity’s designated cryptocurrency wallet address. Follow the specific instructions provided by the charity, such as including a unique reference or donation ID, to ensure proper attribution of your donation.

6. Track your donation:

Keep a record of your cryptocurrency donation transaction. Use the transaction ID provided by the cryptocurrency network to track the progress and confirmation of the donation. Many cryptocurrencies have blockchain explorers that allow you to view the details of your transaction.

7. Consider tax implications:

Consult with a tax advisor or accountant to understand and comply with any tax obligations related to your cryptocurrency donation. Regulations regarding cryptocurrency donations can vary by jurisdiction, and it’s important to ensure compliance with local tax laws.

8. Encourage others to donate with cryptocurrency:

Spread the word about the benefits of donating with cryptocurrencies. Educate others about the ease, transparency, and potential impact of using cryptocurrencies for charitable giving. Encourage friends, family, and colleagues to consider making cryptocurrency donations to charitable organizations as well.

9. Request a donation receipt:

Reach out to the charity and request a donation receipt or acknowledgment for your contribution. This receipt can be useful for tax purposes and will serve as evidence of your donation.

By using cryptocurrencies for charitable giving, you can support causes you care about while taking advantage of the benefits offered by blockchain technology. Remember to conduct due diligence when selecting charities and stay informed about any updates or changes to cryptocurrency donation practices.

How to use cryptocurrency for microtransactions

Cryptocurrencies offer a convenient and efficient solution for microtransactions, allowing for the transfer of small amounts of value quickly and at a low cost. Here’s a guide on how to use cryptocurrency for microtransactions:

1. Choose a suitable cryptocurrency:

Consider selecting a cryptocurrency that is well-suited for microtransactions. Look for cryptocurrencies with low transaction fees and fast confirmation times. Bitcoin’s Lightning Network, for example, enables faster and cheaper microtransactions by leveraging off-chain payment channels.

2. Set up a digital wallet:

Create a digital wallet that supports the chosen cryptocurrency. Ensure that the wallet provides a user-friendly interface, secure storage, and compatibility with microtransactions. Some wallets have specific features designed for microtransactions, such as customizable transaction fees or support for payment channels.

3. Fund your wallet:

Ensure that your wallet has sufficient funds for making microtransactions. Depending on the cryptocurrency, you may need to purchase or acquire the cryptocurrency through an exchange or other means before transferring it into your wallet.

4. Identify platforms accepting microtransactions:

Look for platforms, websites, or services that accept microtransactions in cryptocurrencies. This could include content creators, online gaming platforms, digital content marketplaces, or even specialized microtransaction platforms built on blockchain technology.

5. Initiate the microtransaction:

Once you have identified a platform accepting microtransactions, proceed to the specific microtransaction process outlined by the platform. This typically involves specifying the amount to be transferred and confirming the transaction using your cryptocurrency wallet.

6. Confirm and track the transaction:

After confirming the microtransaction, wait for the transaction to be confirmed by the cryptocurrency network or the designated payment channel. Track the progress and view the details of the transaction using a blockchain explorer or the platform’s provided transaction history.

7. Assess transaction fees and scalability:

When engaging in microtransactions, pay attention to the transaction fees. For cryptocurrencies with high transaction fees, it may be beneficial to aggregate or batch multiple microtransactions together to reduce overall costs. Additionally, consider the scalability of the chosen cryptocurrency, as congestion on the network can impact transaction speed and cost.

8. Explore new technologies and solutions:

Stay informed about emerging technologies and solutions that aim to optimize microtransactions on blockchains. Pay attention to advancements in layer 2 scalability solutions, such as the Lightning Network, which can improve the efficiency and speed of microtransactions on certain blockchains.

By utilizing cryptocurrencies for microtransactions, you can engage in inexpensive and rapid transactions that open up new opportunities for monetizing digital content, participating in online services, and enabling innovative business models.

How to use cryptocurrency for gaming

Cryptocurrencies have gained popularity in the gaming industry for their potential to revolutionize in-game transactions, enhance player ownership, and enable new gaming experiences. Here’s a guide on how to use cryptocurrency for gaming:

1. Participate in blockchain-based games:

Explore blockchain-based games that utilize cryptocurrencies as an integral part of their gameplay and economy. These games leverage blockchain technology to provide players with true ownership and control over in-game assets.

2. Use cryptocurrency for in-game purchases:

Many games now accept cryptocurrencies as a form of payment for in-game purchases. Instead of using traditional payment methods, opt to use cryptocurrencies to buy in-game items, skins, upgrades, or additional game content.

3. Trade in-game assets with cryptocurrencies:

Cryptocurrencies can facilitate peer-to-peer trading of in-game assets. Platforms or exchanges specifically designed for gaming can enable players to buy, sell, and trade their in-game assets directly using cryptocurrencies.

4. Earn cryptocurrencies through gaming:

Engage in play-to-earn games, where players can earn cryptocurrencies by participating in the game’s activities and achieving specific accomplishments. These games often have mechanisms in place to reward players with cryptocurrency tokens for their achievements.

5. Engage in eSports betting:

Participate in eSports betting platforms that accept cryptocurrencies. These platforms allow users to place bets on their favorite eSports teams and events, using cryptocurrencies as the betting currency.

6. Explore decentralized gaming platforms:

Decentralized gaming platforms built on blockchain technology offer new opportunities for interaction and collaboration among players. These platforms use smart contracts to enable transparent and fair gameplay, as well as reward participants with cryptocurrencies for their contributions.

7. Secure your gaming assets:

Utilize cryptocurrency wallets to securely store your gaming assets. A wallet that supports the specific cryptocurrencies used in gaming can ensure the safe storage and ownership of your in-game items and currencies.

8. Stay informed and join gaming communities:

Stay up to date with the latest developments and news in the cryptocurrency gaming space. Participate in gaming communities, forums, and social media groups focused on cryptocurrency and gaming to exchange insights, discover new opportunities, and stay connected.

As cryptocurrencies gain traction in the gaming industry, they offer exciting possibilities for players to enhance their gaming experiences, participate in innovative gaming economies, and truly own their in-game assets. By leveraging cryptocurrencies, gamers can immerse themselves in a thriving ecosystem that combines the best of blockchain technology and gaming.

How to use cryptocurrency for decentralized finance (DeFi)

Decentralized Finance (DeFi) has emerged as a groundbreaking application of cryptocurrency and blockchain technology. It offers financial services and products that operate without centralized intermediaries, providing users with more control and transparency over their financial activities. Here’s a guide on how to use cryptocurrency for DeFi:

1. Choose a decentralized finance platform:

Select a reputable DeFi platform that aligns with your financial goals. The platform should offer a variety of decentralized financial services such as lending, borrowing, yield farming, decentralized exchanges (DEXs), or liquidity provision.

2. Set up a digital wallet:

Create a digital wallet that supports the specific cryptocurrency or blockchain network used by the DeFi platform. This wallet will serve as your secure gateway for interacting with DeFi protocols.

3. Fund your wallet:

Ensure that your wallet has sufficient funds in the cryptocurrency required by the DeFi platform. This may involve acquiring the necessary cryptocurrency through a cryptocurrency exchange or by converting from other supported cryptocurrencies.

4. Explore lending and borrowing:

Utilize DeFi lending protocols that allow you to lend your cryptocurrency and earn interest or borrow funds by using your cryptocurrency as collateral. These lending platforms often use smart contracts to automate and secure the lending and borrowing processes.

5. Participate in yield farming and liquidity provision:

Engage in yield farming and liquidity provision on DeFi platforms by supplying your cryptocurrency to liquidity pools. In return, you earn rewards in the form of additional cryptocurrency or fees generated by the platform’s users.

6. Use decentralized exchanges (DEXs):

Trade cryptocurrencies directly on decentralized exchanges (DEXs) without the need for intermediaries or centralized order books. DEXs operate using smart contracts and allow users to trade cryptocurrencies directly from their wallets.

7. Take advantage of DeFi protocols and assets:

Explore different DeFi protocols and assets that offer unique features and opportunities. This can include stablecoins, decentralized derivatives, decentralized insurance, or tokenization platforms that represent real-world assets on the blockchain.

8. Stay informed and assess risks:

Stay updated with the latest developments and constantly assess the risks associated with using DeFi platforms. DeFi is a rapidly evolving space, and understanding the potential risks and vulnerabilities is crucial to safeguarding your assets and participating in a responsible manner.

9. Research and review smart contracts:

When using DeFi platforms, thoroughly review the code and functionalities of the smart contracts involved. Understand the risks associated with smart contract bugs, vulnerabilities, or exploits, and consider utilizing auditing services or relying on audits conducted by reputable third parties.

10. Contribute to DeFi governance:

Many DeFi protocols have built-in governance mechanisms that allow token holders to participate in decision-making processes. Consider acquiring governance tokens and actively participate in voting and governance proposals to shape the future development of DeFi platforms.

By utilizing cryptocurrencies for decentralized finance, individuals can access a wide range of financial services in a decentralized and permissionless manner, providing greater financial freedom and control over their assets.

How to use cryptocurrency for smart contracts

Cryptocurrencies have become closely intertwined with smart contracts, offering a secure and efficient way to execute and interact with these self-executing contracts. Here’s a guide on how to use cryptocurrency for smart contracts:

1. Choose a cryptocurrency platform:

Select a cryptocurrency platform that supports smart contracts. Ethereum is the most popular platform for smart contracts, but other platforms like Binance Smart Chain, Cardano, and EOS also offer smart contract functionality.

2. Acquire the required cryptocurrency:

Obtain the cryptocurrency native to the chosen platform. This usually involves purchasing the cryptocurrency on a cryptocurrency exchange using fiat currency or swapping it with another supported cryptocurrency.

3. Set up a digital wallet:

Create a digital wallet that supports the cryptocurrency used for the smart contract platform. Ensure that the wallet is secure and compatible with the chosen cryptocurrency.

4. Familiarize yourself with smart contract concepts:

Understand the fundamentals of smart contracts, including their purpose, structure, and programming languages used for development, such as Solidity for Ethereum. This knowledge will help you interact with and understand the capabilities of smart contracts.

5. Explore existing smart contracts:

Take time to explore and study existing smart contracts already deployed on the chosen platform. Platforms like Ethereum have platforms where you can browse and review available smart contracts. This will give you insights into the functionalities and possible applications of smart contracts.

6. Interact with smart contracts:

Use your wallet to interact with existing smart contracts or deploy your own. Interactions can include participating in token sales (if applicable), sending and receiving tokens, executing predefined functions within the smart contract, or even participating in decentralized applications (dApps) built on top of smart contracts.

7. Review and verify smart contracts:

If you’re deploying your own smart contract, review and verify the code to ensure it meets your requirements. Consider seeking code audits from reputable third-party auditors to identify and address any potential security vulnerabilities or bugs.

8. Understand gas fees:

Be aware of gas fees when interacting with smart contracts. Gas fees are the transaction fees required to execute operations on the blockchain. Each operation within a smart contract consumes a specific amount of gas, so consider the cost and plan accordingly.

9. Stay updated and learn from the community:

Stay informed about the latest developments, updates, and best practices in the smart contract space. Engage in forums, community discussions, and platforms dedicated to smart contracts. This will help you expand your knowledge, learn from others, and stay ahead of emerging trends.

10. Experiment and contribute:

Experiment with existing smart contracts or create your own to develop innovative solutions and contribute to the growing ecosystem. Smart contracts open up new possibilities across various industries, from finance and supply chain to gaming and decentralized applications.

By utilizing cryptocurrencies for smart contracts, individuals can leverage the power of blockchain technology to execute secure and automated agreements, revolutionizing the way transactions and interactions occur in a variety of industries.

How to use cryptocurrency for tokenization

Tokenization refers to the process of converting real-world assets, such as real estate, artwork, or fractional ownership in a company, into digital tokens on a blockchain. Cryptocurrencies provide a powerful tool for tokenization, enabling the representation and transfer of ownership rights for various assets. Here’s a guide on how to use cryptocurrency for tokenization:

1. Choose a suitable blockchain platform:

Select a blockchain platform that supports tokenization. Ethereum is a popular choice due to its robust smart contract capabilities, but other platforms like Binance Smart Chain and Stellar also offer tokenization functionalities.

2. Understand the asset to be tokenized:

Thoroughly understand the asset that you want to tokenize. Identify the legal, regulatory, and practical considerations associated with tokenizing the asset. Consult with legal professionals and experts in the specific asset class to ensure compliance with relevant regulations.

3. Determine the tokenization structure:

Decide on the type of tokens to be created for the asset. Common types include equity tokens, utility tokens, security tokens, or non-fungible tokens (NFTs). Each type has different characteristics and implications regarding ownership rights, governance, and regulatory requirements.

4. Create a tokenization contract:

Develop a smart contract that defines the rules and conditions for the tokenized asset. This may include details regarding ownership, distribution, governance rights, voting mechanisms, and dividend or revenue-sharing arrangements. Work with reputable developers or auditors to ensure the integrity and security of the smart contract.

5. Launch the token sale:

If applicable, launch a token sale or Initial Coin Offering (ICO) to distribute the tokens and raise funds. Adhere to the regulatory requirements for token sales in your jurisdiction and consider implementing know-your-customer (KYC) and anti-money laundering (AML) procedures to ensure compliance.

6. List the tokens on exchanges:

List the tokens on cryptocurrency exchanges to provide liquidity and enable trading. Collaborate with exchanges that support the specific token standard used and meet the necessary regulatory requirements.

7. Generate awareness and market the tokens:

Develop a marketing strategy to generate awareness and interest in the tokenized asset. Educate potential investors or buyers about the benefits of tokenization, including increased liquidity, fractional ownership, and potential returns from the asset’s performance.

8. Provide ongoing token management:

Manage the tokens and provide ongoing updates and support to token holders. Communicate important information, such as governance decisions, changes in asset value, or distribution of dividends or rewards. Utilize community management tools and platforms to foster engagement.

9. Comply with regulatory requirements:

Ensure compliance with the applicable legal and regulatory frameworks for tokenization. Be aware of securities laws, tax obligations, and investor protection regulations. Consult with legal professionals to ensure the tokenization process meets the necessary standards.

10. Continuously monitor and adapt:

Monitor market trends, regulations, and technological advancements related to tokenization. Continuously assess the performance and viability of the tokenized asset and adapt the tokenization strategy as needed to maximize the benefits and opportunities offered by cryptocurrencies.

By utilizing cryptocurrencies for tokenization, individuals can unlock the potential of fractional ownership, increase liquidity for traditionally illiquid assets, and create innovative investment opportunities in a secure and transparent manner.