Introduction

Welcome to the world of cryptocurrencies, where digital assets have taken the financial landscape by storm. With the rise in popularity of cryptocurrencies like Bitcoin, Ethereum, and many others, it’s important to understand the tax implications associated with these digital currencies. While cryptocurrencies promise decentralization and anonymity, they are not exempt from taxation.

As the saying goes, “With great power comes great responsibility,” and this applies to the world of cryptocurrency as well. If you’ve dabbled in buying, selling, or trading cryptocurrencies, it’s crucial to be aware of your tax obligations. The taxation of cryptocurrencies varies across different countries, but the underlying principle remains the same – if you earn money from cryptocurrencies, you may be required to pay taxes on those earnings.

Why is it necessary to pay taxes on cryptocurrency? The primary reason is that governments view cryptocurrencies as assets or forms of property, rather than traditional currencies. Therefore, the gains made from buying and selling cryptocurrencies are subject to taxation, similar to gains from the sale of stocks, bonds, or real estate. The tax revenues generated from cryptocurrency transactions contribute to the functioning of the overall economy and public services.

In this comprehensive guide, we will dive into the various aspects of cryptocurrency taxation. From understanding how cryptocurrency taxes are calculated to reporting obligations, we will cover it all. Whether you’re a seasoned crypto investor or just starting your journey, this article will provide you with the knowledge you need to navigate the complex world of cryptocurrency taxes.

It’s important to note that the information in this guide should not be considered as legal or tax advice. Tax regulations and laws related to cryptocurrencies are ever-evolving, and it’s crucial to consult with a qualified tax professional to ensure compliance with the specific tax laws of your country.

Why Do You Need to Pay Taxes on Cryptocurrency?

One of the most common questions asked by cryptocurrency enthusiasts is why they need to pay taxes on their digital assets. After all, cryptocurrencies are often associated with decentralization and anonymity, making it tempting to believe that they are beyond the reach of government taxation. However, it is crucial to understand that cryptocurrencies are not exempt from taxation, and failing to comply with tax obligations can have serious consequences.

The primary reason why you need to pay taxes on cryptocurrencies is that most governments view them as assets or forms of property rather than traditional currencies. From the perspective of tax authorities, gains made through buying, selling, or trading cryptocurrencies are considered taxable events, just like gains from stocks, bonds, or real estate transactions. The increase in the value of your digital assets is seen as a source of income that is subject to taxation.

Furthermore, taxation is an essential part of the functioning of any economy. It helps governments generate revenue, which is then used to fund public services, infrastructure development, social programs, and other essential functions of the state. By imposing taxes on cryptocurrencies, governments ensure that individuals engaging in cryptocurrency transactions contribute their fair share to the economy.

Another reason for cryptocurrency taxation is to promote fairness and equity. Taxation is designed to ensure that individuals and businesses follow the same rules and contribute proportionally to the overall tax burden. By taxing cryptocurrencies, governments aim to prevent tax evasion and create a level playing field for all taxpayers.

Moreover, paying taxes on cryptocurrencies helps legitimize the digital asset class. As governments implement regulations and guidelines for cryptocurrency taxation, it adds credibility to the industry and establishes a framework for its wider adoption. This, in turn, can lead to increased acceptance of cryptocurrencies by the general public, financial institutions, and businesses.

It’s important to note that the tax regulations surrounding cryptocurrencies are still evolving, and there may be variations in how different countries approach cryptocurrency taxation. Some countries have implemented specific laws and guidelines, while others may treat cryptocurrencies under existing tax laws. It is crucial to stay updated with the tax regulations in your jurisdiction and consult with a tax professional who can provide guidance tailored to your specific situation.

How Are Cryptocurrency Taxes Calculated?

Calculating taxes on cryptocurrencies can be a complex process, as it involves determining the taxable events, calculating the gains or losses, and identifying the applicable tax rates. The exact method of calculating cryptocurrency taxes may vary depending on the tax regulations of your jurisdiction, but there are some common approaches used in many countries.

The most common method of calculating cryptocurrency taxes is through the identification of taxable events. Taxable events include activities such as the sale or exchange of cryptocurrencies, mining rewards, airdrops, staking, and receiving cryptocurrency as payment for goods or services. Each taxable event triggers a tax liability, and it is essential to keep accurate records of these events to ensure compliance with tax regulations.

Once the taxable events are identified, the next step is to calculate the gains or losses associated with each transaction. This is typically done by determining the difference between the purchase price and the selling price of the cryptocurrency. If you acquired the cryptocurrency through mining, the cost basis can be calculated using the fair market value of the cryptocurrency at the time it was mined.

If you have held the cryptocurrency for a certain period of time before selling it, you may be eligible for different tax rates. Many jurisdictions have a distinction between short-term and long-term capital gains. Short-term capital gains are typically taxed at higher rates, while long-term capital gains may benefit from lower tax rates or even preferential tax treatment.

It is crucial to keep detailed records of all cryptocurrency transactions, including dates, amounts, and the fair market value of the cryptocurrency at the time of the transaction. These records will be essential when calculating gains or losses and reporting them to the tax authorities.

Another factor to consider when calculating cryptocurrency taxes is the possibility of deductions or losses. If you experienced losses from cryptocurrency investments or transactions, you may be able to offset those losses against your gains, reducing your overall tax liability. However, the rules and limitations surrounding deductions and losses can vary, so it is important to consult with a tax professional to understand your specific situation.

It’s worth noting that cryptocurrency taxation is a relatively new area, and tax authorities are still navigating the complexities of this digital asset class. As a result, tax laws and regulations may undergo changes and updates in the future. It is essential to stay informed about any amendments to the tax laws in your jurisdiction and seek professional advice to ensure compliance with the latest requirements.

Capital Gains Tax

Capital gains tax is a common form of taxation imposed on the profits earned from the sale or exchange of capital assets, including cryptocurrencies. When you sell or exchange your cryptocurrencies for a profit, the capital gains tax may apply, depending on the specific tax regulations of your jurisdiction.

The capital gains tax is typically calculated by determining the difference between the purchase price (also known as the cost basis) and the selling price of the cryptocurrency. If the selling price is higher than the purchase price, the resulting gain is considered a capital gain and is subject to taxation.

There are two types of capital gains: short-term capital gains and long-term capital gains. The classification depends on the holding period of the cryptocurrency before it is sold or exchanged.

Short-term capital gains are typically generated from the sale of cryptocurrencies that were held for a year or less. These gains are usually subject to higher tax rates and are taxed at the individual’s ordinary income tax rate. The exact tax rate for short-term capital gains may vary depending on the tax laws of your jurisdiction.

On the other hand, long-term capital gains are generated from the sale of cryptocurrencies held for more than a year. Long-term capital gains may be eligible for lower tax rates or even preferential tax treatment in some jurisdictions. These lower rates are designed to incentivize long-term investment in assets such as cryptocurrencies.

It is important to note that the tax rates for capital gains can vary significantly based on factors such as the individual’s income level and tax bracket. Additionally, some countries provide tax exemptions or reduced rates for certain types of capital gains, such as gains from the sale of small amounts of cryptocurrencies.

When it comes to reporting and paying capital gains taxes on cryptocurrencies, it is crucial to keep detailed records of all transactions, including the dates of purchase and sale, the amounts involved, and the cost basis of the cryptocurrencies. These records will help determine the accurate capital gains and ensure compliance with tax laws.

Consulting with a tax professional who specializes in cryptocurrency taxation is highly recommended to ensure that you understand the specific capital gains tax regulations in your jurisdiction and to accurately calculate and report your capital gains.

Income Tax

Income tax is another important aspect of cryptocurrency taxation that individuals need to be aware of. In many jurisdictions, income tax applies to the earnings generated from various cryptocurrency-related activities, such as mining, staking, and receiving cryptocurrency as payment for goods or services.

Income tax is typically imposed on the value of the cryptocurrencies received as income at the time of receipt. The value is determined based on the fair market value of the cryptocurrency on that specific date. If you receive cryptocurrency as payment for goods or services, the fair market value can be calculated using reputable cryptocurrency exchanges or other market data sources.

For miners, the income derived from mining activities, which includes both the newly minted cryptocurrencies and transaction fees, is considered taxable income. The fair market value of the mined cryptocurrency at the time of receipt is used to compute the taxable income.

Similarly, if you earn income through staking, where you support the network by holding and validating cryptocurrency, any rewards or income earned from the staking process may be subject to income tax. The fair market value of the staking rewards at the time of receipt would be considered taxable income.

It’s important to keep detailed records of your earnings from various cryptocurrency-related activities to accurately calculate your taxable income. This includes documenting the dates and values of the cryptocurrencies received, as well as any associated expenses that may be deductible.

When reporting your cryptocurrency-related income for tax purposes, you will typically need to fill out the appropriate forms and statements designated by your tax authority. The income earned from cryptocurrency activities is added to your total income for the tax year and is subject to the applicable income tax rates based on your tax bracket.

It’s worth noting that tax authorities are increasingly focusing on cryptocurrency tax compliance, and failure to report cryptocurrency-related income can result in penalties and legal consequences. Therefore, it is essential to understand the income tax regulations specific to your jurisdiction and consult with a tax professional to ensure accurate reporting and compliance.

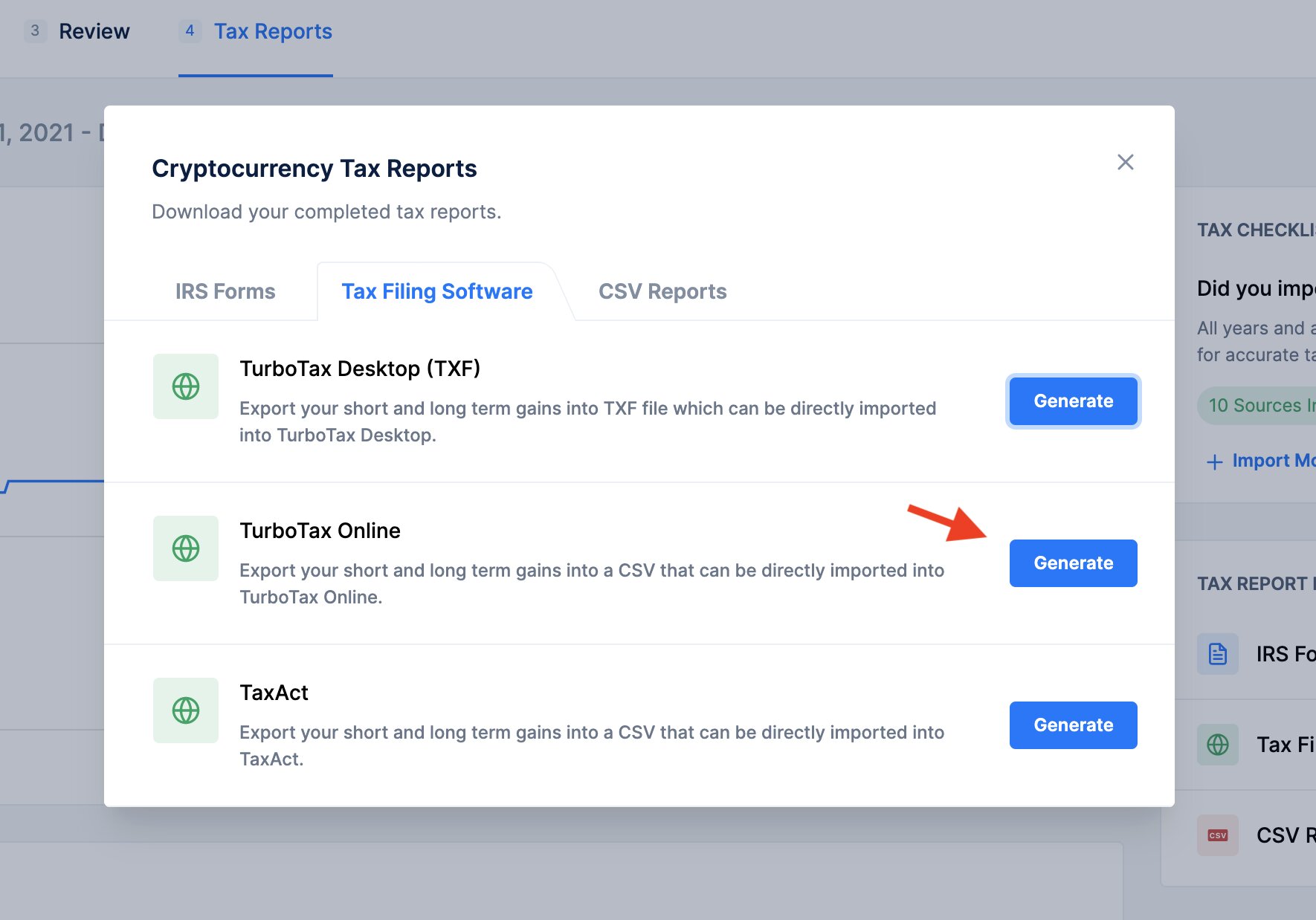

Reporting Cryptocurrency Taxes

Reporting cryptocurrency taxes is a vital step in ensuring compliance with tax regulations and fulfilling your obligations as a cryptocurrency investor or trader. The specific reporting requirements may vary based on the tax laws and regulations of your jurisdiction, but there are some common practices that you should be aware of.

One of the key aspects of reporting cryptocurrency taxes is maintaining accurate and detailed records of all cryptocurrency transactions. This includes information such as the dates of transactions, amounts involved, cost basis, fair market value at the time of the transaction, and any associated expenses. These records will help you calculate your gains or losses accurately and provide supporting documentation if required by tax authorities.

Many countries require individuals to report their cryptocurrency activities on their annual tax return. This typically involves disclosing the details of your cryptocurrency holdings, gains, and losses for the tax year. Some jurisdictions have specific tax forms or schedules dedicated to reporting cryptocurrency-related information, while others may require the use of general tax forms to report this income.

When reporting your cryptocurrency transactions, it’s important to follow the guidelines provided by your tax authority. Some jurisdictions may require you to report each individual transaction separately, while others may allow reporting of aggregated totals. It’s crucial to understand the reporting requirements specific to your jurisdiction to avoid mistakes or omissions.

In addition to reporting gains and losses, you may also need to report other forms of cryptocurrency income, such as mining rewards, staking income, or any income received from providing goods or services in exchange for cryptocurrencies. These forms of income should be accurately documented and reported on your tax return.

It’s important to note that tax authorities are increasingly focused on cryptocurrency tax compliance, and there are growing efforts to ensure individuals accurately report their cryptocurrency-related income. Failure to report cryptocurrency transactions or provide accurate information can result in penalties, fines, or even legal consequences.

Given the complexities of reporting cryptocurrency taxes, it is highly recommended to seek professional advice from a tax professional who specializes in cryptocurrency taxation. They can provide guidance tailored to your specific situation, ensure accurate reporting, and help you navigate the ever-changing landscape of cryptocurrency tax regulations.

Tax Implications of Mining Cryptocurrency

Mining cryptocurrency involves validating and processing transactions on a blockchain network, and it plays a crucial role in maintaining the integrity and security of various cryptocurrencies. However, mining cryptocurrency can have significant tax implications, and it’s important to understand how these activities may be taxed in your jurisdiction.

One of the primary tax implications of mining cryptocurrency is the recognition of income. When you successfully mine new cryptocurrencies, these newly minted coins are considered taxable income. The fair market value of the mined coins at the time of receipt is typically used to determine the taxable income.

It’s essential to document and track the fair market value of the mined coins accurately. Many countries require individuals to report the income generated from mining activities on their tax returns. Failure to report mining income can result in penalties or legal consequences.

In addition to the mining reward, transaction fees earned by miners are also subject to taxation. These fees are typically accrued for including transactions in the blocks they mine. Similar to the mining reward, the fair market value of the transaction fees at the time of receipt should be reported as income.

Whether you are considered a professional miner or a hobbyist miner can also impact the tax treatment of your mining activities. Professional miners, who engage in mining as a business and pursue it for profit, may have additional tax obligations and be subject to different tax rules compared to hobbyist miners.

Expenses associated with mining activities may also have tax implications. You may be eligible to deduct certain expenses related to mining, such as the costs of mining equipment, electricity expenses, cooling infrastructure, and maintenance fees. However, the specific rules and limitations surrounding expense deductions can vary depending on the tax laws of your jurisdiction.

Depending on your jurisdiction, you may also be subject to additional taxes, such as value-added tax (VAT) or goods and services tax (GST), on mining activities. These taxes may apply to both the income generated from mining and the purchase of mining equipment or services.

As with other cryptocurrency activities, it’s crucial to maintain accurate and detailed records of your mining activities, including dates, mining income, expenses, and supporting documentation. These records will help ensure accurate reporting and compliance with tax regulations.

Given the complexities of mining cryptocurrency and its tax implications, it is advisable to consult with a tax professional who specializes in cryptocurrency taxation. They can provide guidance specific to your jurisdiction and help you navigate the tax obligations associated with your mining activities.

Tax Treatment of Cryptocurrency Trading

Cryptocurrency trading involves buying, selling, and exchanging digital assets with the aim of making a profit. However, it’s important to understand that these trading activities can have significant tax implications. The tax treatment of cryptocurrency trading varies depending on the tax laws and regulations of your jurisdiction.

In many countries, cryptocurrency trading is subject to capital gains tax. When you sell or exchange cryptocurrencies for a profit, the gains are considered capital gains and may be subject to taxation. The precise tax rates and classifications (such as short-term or long-term capital gains) will depend on the specific tax laws of your jurisdiction.

It’s crucial to keep accurate records of your trading activities, including the dates of transactions, amounts involved, cost basis, and fair market value at the time of the transaction. These records will help you calculate your gains or losses accurately and ensure compliance with tax regulations.

Some jurisdictions may treat cryptocurrency trading as a business or investment activity rather than capital gains. In such cases, trading income may be subject to different tax rules and may be taxed at the individual’s ordinary income tax rate. It’s important to consult with a tax professional to understand how your trading activities will be classified and taxed.

Depending on your jurisdiction, you may also be eligible for certain deductions or allowances related to cryptocurrency trading. For example, you may be able to deduct certain expenses incurred in the process of buying, selling, or exchanging cryptocurrencies, such as transaction fees or trading platform fees. The tax laws governing expense deductions can vary, so it’s important to consult with a tax professional for guidance.

Another aspect to consider is the reporting obligations associated with cryptocurrency trading. Many countries require individuals to report their gains and losses from cryptocurrency trading on their tax returns. You may need to fill out specific forms or schedules dedicated to reporting cryptocurrency trading activities or include the information on general tax forms.

It’s worth noting that tax authorities are increasingly focused on cryptocurrency tax compliance, and there are efforts to ensure accurate reporting of trading activities. Failure to report cryptocurrency trading activities or provide accurate information can result in penalties, fines, or legal consequences.

Given the complexities of cryptocurrency trading and its tax implications, it is recommended to consult with a tax professional who specializes in cryptocurrency taxation. They can provide guidance specific to your jurisdiction, help you accurately calculate and report your gains and losses, and ensure compliance with tax laws.

Tax Considerations for ICOs and Token Sales

Initial Coin Offerings (ICOs) and token sales have become popular fundraising methods for cryptocurrency projects. However, participating in ICOs and token sales can have significant tax implications that individuals need to consider. The tax treatment of ICOs and token sales may vary depending on the jurisdiction and the nature of the tokens being sold.

One important tax consideration for ICOs and token sales is the classification of the tokens. The tax treatment can vary depending on whether the tokens are classified as securities, utility tokens, or something else. Different jurisdictions may have different criteria for determining the classification of tokens and may apply varying tax rules accordingly.

If the tokens are classified as securities, the sale or transfer of these tokens may be subject to capital gains tax. The gains made from selling securities tokens would be treated similarly to gains from the sale of stocks or other securities. It is essential to keep thorough records of the token purchase and sale prices for accurate calculation of gains or losses.

On the other hand, if the tokens are classified as utility tokens or something other than securities, the tax treatment may be different. In some jurisdictions, purchasing utility tokens may be considered as acquiring prepaid services or goods. The tax liability would arise when using the utility tokens for their intended purpose, such as accessing a platform or redeeming services.

It’s important to note that participating in ICOs and token sales may also trigger tax obligations if you acquire tokens through airdrops or token swaps. Airdropped tokens are often considered as taxable income, and you may need to report the fair market value of the tokens received as income at the time of receipt.

When it comes to reporting the tax implications of ICOs and token sales, it’s crucial to consult with a tax professional familiar with cryptocurrency taxation in your jurisdiction. They can guide you on the specific reporting requirements and help ensure accurate compliance with tax laws.

Additionally, tax authorities are increasing their focus on ICOs and token sales, aiming to ensure proper tax reporting and compliance. There may be specific disclosure requirements or reporting forms associated with ICOs and token sales that need to be adhered to.

As the cryptocurrency landscape evolves, tax regulations and laws related to ICOs and token sales are also subject to change. It’s important to stay updated with the latest guidelines and consult with a tax professional for the most up-to-date information and advice.

Tax Planning Strategies for Crypto Investors

Tax planning is an essential aspect of managing your cryptocurrency investments and can help optimize your tax liability. Here are some tax planning strategies that crypto investors can consider:

1. Holding Period: Consider the holding period of your cryptocurrencies before selling or exchanging them. Long-term investments held for more than a year may be eligible for preferential tax rates on capital gains, potentially reducing your tax liability.

2. Tax-Loss Harvesting: Offset capital gains by strategically selling cryptocurrencies that have incurred losses. Tax-loss harvesting allows you to reduce your overall tax liability by applying the losses against gains realized in the same tax year. However, be mindful of tax rules and limitations surrounding wash sales, which may restrict the immediate repurchase of the same or substantially identical cryptocurrencies.

3. Expense Deductions: Identify and track any eligible expenses related to your cryptocurrency investments, such as transaction fees, storage fees, and professional services fees. These expenses may be deductible, reducing your taxable income and lowering your tax liability. Ensure you maintain accurate records and consult with a tax professional to determine the deductibility of these expenses.

4. Tax-Advantaged Accounts: Explore the option of investing in cryptocurrencies through tax-advantaged accounts, such as Individual Retirement Accounts (IRAs) or Self-Directed Solo 401(k)s. These accounts offer potential tax benefits, such as tax-free growth or tax-deferred contributions, depending on the specific account type and your tax jurisdiction.

5. Gift and Donation Strategies: Consider gifting appreciated cryptocurrencies to reduce your taxable income and potentially leverage any applicable gift tax exemptions. Alternatively, you can donate cryptocurrencies to qualifying charitable organizations and potentially receive a deduction for the fair market value of the donated assets.

6. Jurisdiction Selection: Research and evaluate the tax implications of different jurisdictions for cryptocurrency investments. Some jurisdictions may offer more favorable tax rates or exemptions for specific types of cryptocurrency activities. However, be mindful of the legal and practical implications of operating in different jurisdictions.

7. Consult with a Tax Professional: Given the complexities of cryptocurrency taxation, it’s advisable to seek guidance from a tax professional experienced in cryptocurrency tax planning. They can provide personalized advice based on your specific circumstances and help you navigate the ever-evolving regulatory landscape.

Implementing these tax planning strategies can potentially help you minimize your tax liability and optimize your cryptocurrency investment returns. However, tax laws and regulations are subject to change, and it’s crucial to stay informed and consult with a tax professional for the most up-to-date guidance specific to your jurisdiction.

Tax Laws and Regulations in Different Countries

When it comes to the taxation of cryptocurrencies, tax laws and regulations can vary significantly from one country to another. Different countries have adopted diverse approaches in addressing the tax treatment of cryptocurrencies. Here, we provide a brief overview of tax laws and regulations in different countries:

United States: In the United States, the Internal Revenue Service (IRS) treats cryptocurrencies as property for tax purposes. Cryptocurrency transactions are subject to capital gains tax, with different rates depending on the holding period. The IRS has also issued guidelines for reporting cryptocurrency activities and imposes penalties for non-compliance.

United Kingdom: In the United Kingdom, Her Majesty’s Revenue and Customs (HMRC) treats cryptocurrencies as property for tax purposes. Individuals involved in trading or investing in cryptocurrencies are subject to capital gains tax. Mining cryptocurrency is considered a taxable activity, and income tax may apply to mining income.

Australia: Australian tax laws consider cryptocurrencies as assets subject to capital gains tax. Transacting with cryptocurrencies for goods or services is treated as a barter transaction. Certain cryptocurrencies used as a payment method are exempt from goods and services tax (GST).

Germany: Germany treats cryptocurrencies as private money. Cryptocurrency trading is subject to capital gains tax if the holding period is less than one year. Cryptocurrency holdings held for more than one year are generally tax-exempt.

Japan: Japan recognizes cryptocurrencies as legal property and treats gains from cryptocurrency transactions as miscellaneous income. Cryptocurrency exchanges are regulated and subject to registration and reporting requirements.

Canada: Canada treats cryptocurrencies as commodities subject to taxation. Cryptocurrency transactions are subject to capital gains tax, and individuals involved in mining or trading may be considered self-employed and liable for income tax.

Singapore: In Singapore, cryptocurrencies are treated as goods and subject to Goods and Services Tax (GST) when used in transactions. However, the buying, selling, or holding of cryptocurrencies is generally not subject to income tax or capital gains tax.

These are just a few examples of the tax laws and regulations in different countries. It’s important to remember that cryptocurrency taxation is a rapidly evolving field, and governments worldwide are establishing and updating their tax frameworks to address the unique challenges posed by cryptocurrencies.

As a cryptocurrency investor or trader, it’s crucial to stay informed about the tax laws and regulations in your jurisdiction. Consulting with a tax professional familiar with cryptocurrency taxation in your country can help you navigate the specific requirements and ensure compliance with the applicable tax rules.

Conclusion

Navigating the world of cryptocurrency taxation can be complex and challenging, but understanding and complying with tax laws and regulations is crucial for every cryptocurrency investor or trader. The tax implications of cryptocurrency activities, such as buying, selling, mining, and participating in ICOs, can vary depending on the jurisdiction and specific circumstances.

To ensure compliance with tax regulations and optimize your tax liability, it’s imperative to keep accurate and detailed records of all cryptocurrency transactions, including dates, amounts, cost basis, and fair market value. Maintaining organized records will help to accurately calculate gains or losses and report them to the tax authorities.

In addition to record-keeping, consulting with a tax professional who specializes in cryptocurrency taxation is highly recommended. They can provide valuable guidance tailored to your specific situation and help navigate the complex tax landscape. Tax professionals can also keep you updated on any changes to tax laws and regulations that may impact your cryptocurrency activities.

Remember to stay informed about the tax laws and regulations in your jurisdiction, as well as any reporting obligations or forms specific to cryptocurrency taxation. Tax authorities are increasingly focusing on cryptocurrency tax compliance, and failure to comply can result in penalties, fines, or legal consequences.

Lastly, tax planning strategies, such as considering holding periods, tax-loss harvesting, expense deductions, and utilizing tax-advantaged accounts, can help optimize your tax position. However, it’s important to note that tax laws may change, and strategies should be adapted accordingly.

By understanding the tax implications of cryptocurrency activities and staying compliant with tax laws, you can confidently navigate the world of cryptocurrencies while managing your tax obligations responsibly. With careful planning and adherence to tax regulations, you can focus on maximizing your investment returns within the bounds of the law.